|

시장보고서

상품코드

1842456

독소루비신 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Doxorubicin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

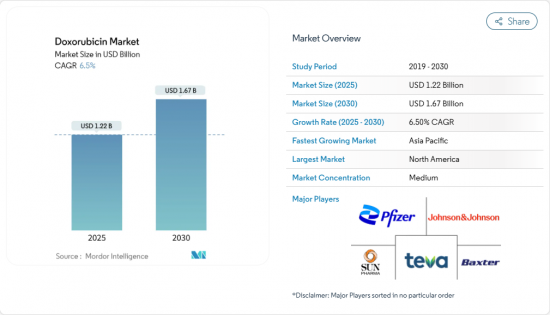

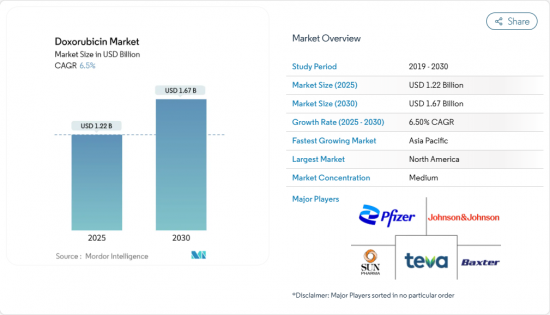

세계의 독소루비신 시장의 규모는 2025년에 12억 2,000만 달러, 2030년에는 16억 7,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR은 6.50%로 예상됩니다.

견고한 임상 증거로 이 약물은 많은 종양학 프로토콜의 중심에 계속 위치하고 있으며, 리포솜 전달의 지속적인 진보로 치료 영역이 확대되고 있습니다. 암 이환율의 지속성, 제네릭 의약품의 가용성 확대, 표적 제제의 기술 혁신은 높은 비용의 생물학적 제제와 시장 점유율을 겨루는 중에서도 수요를 강화하고 있습니다. 동시에 심독성에 대한 우려, 고위험 약물 취급 규칙의 엄격화, 전문 약국 모델로의 워크플로우의 시프트 등이 장기적인 흡수를 억제하고 있습니다.

세계의 독소루비신 시장의 동향과 인사이트

세계적인 암 이환율 증가로 화학요법량 증가

세계적인 암 이환율의 상승에 의해 독소루비신과 같은 광범위한 세포독성이 지속적으로 사용되고 있습니다. 정밀 생물학적 제제가 보급되는 가운데 임상의사는 재발 빈도가 높은 유방암에 대해 안트라사이클린-탁산 병용 요법에 계속 의존하고 있으며, 샌안토니오 유방암 심포지엄에서 발표된 최신 3상 데이터에서는 탁산 단독 요법에 비해 우수한 생존율을 보이고 있습니다. 고형암과 혈액암에 걸친 적응의 다양성에 의해 독소루비신의 투여량은 확대되고, 생물학적 제제의 신규 진입이 있음에도 불구하고, 독소루비신 시장은 강화되고 있습니다.

저렴한 제네릭 의약품 및 리포좀 독소루비신의 가용성 확대

일반 의약품과의 경쟁 심화는 환자의 접근을 확대하고 가격을 압박하고 있습니다. 루핀과 같은 신규 진입기업은 2024년 8월 미국에서 염산독소루비신 리포좀 주사제를 출시해 리포솜 제형의 범주를 확대하고 예산에 제약이 있는 의료 시스템에서 널리 채용되는 계기가 되었습니다. 이러한 저가의 대체품의 유입은 아시아태평양과 라틴아메리카에서 치료의 공정성을 지원하고 독소루비신 시장의 성장을 더욱 자극합니다.

엄격한 용량 상한 및 모니터링이 필요한 누적 심독성 위험

안트라사이클린 유발성 심근증은 가이드라인에 450-550mg/m2의 누적 용량 상한이 명시되어 일생 동안의 노출을 제한하고 있습니다. 덱스라졸산은 부분적인 보호를 제공하지만, FDA가 승인한 심근보호제는 이외에 존재하지 않기 때문에 처방자는 효능과 장기적인 심장의 안전성을 양립시킬 필요가 있습니다. 이 억제요인은 독소루비신 시장에서 반복 사이클의 사용을 늦추고 보다 안전한 전달 플랫폼 기술 혁신에 박차를 가하고 있습니다.

부문 분석

2024년 독소루비신 시장은 수십년에 걸친 임상 관행과 제네릭 의약품의 가격 경쟁력을 배경으로 기존 주사제의 매출 기여율이 52%를 유지했습니다. PEG화된 리포좀 독소루비신은 이전 시장 규모에 비해 극히 적지만, CAGR 7.5%로 확대되고 있으며, 심독성 경감과 순환시간 연장으로 독소루비신 시장 규모 확대에 매우 중요합니다. 유럽에서 Myocet 및 Celdoxome과 같은 고급 캐리어의 규제 승인은 지질 기반 벡터가 안전하게 누적 용량의 상한을 연장할 수 있다는 컨센서스 증가를 뒷받침합니다. pH를 트리거로 하는 나노 캐리어나 감온성 리포솜의 연구개발로 유망한 전임상 데이터를 얻을 수 있어, 디바이스 기반의 하이퍼써미아 트리거의 공동 개발에 의해 장래의 진출기업을 구조적으로 차별화하고, 이 제제 부문에서의 경쟁 강도를 강화할 수 있는 가능성을 시사하고 있습니다.

동결건조 분말 제제의 안정적인 공급이 계속됨에 따라 고급 콜드체인이 없는 지역 중에서도 특히 아프리카와 남미의 농촌 지역에서 치료 접근성이 보장됩니다. 독소루비신 시장 전반에 있어서, 비용에 중점을 둔 포트폴리오를 가진 제조업체들에게 해당 지역에서의 수요는 소폭이면서도 지속적인 수익원이 되고 있습니다.

지역 분석

북미는 2024년 세계 매출의 48%를 차지하였으며, 중심적인 지위를 유지하고 있습니다. 입원 환자에 대한 환급 구조, 폭넓은 보험 적용, 심근 보호 전달 시스템의 조기 도입이 판매량을 확보하고 있습니다. 그러나 리포좀 제제로 전환함으로써, 이 지역의 독소루비신 시장은 안정적인 성장을 유지할 전망입니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 8.3%로 성장해 주요 가속 엔진이 될 것으로 보입니다. 진단약의 보급률 상승, 중국과 인도의 민간보험 급증, 현지 제조에 대한 정부의 우대조치가 견조한 수요를 지지하고 있습니다. 썬 파머슈티컬 인더스트리즈는 3억 5,500만 달러를 투자한 체크포인트 세라퓨틱스사의 인수 등을 통해 암 영역에서의 사업 확대를 도모하고 있으며, 이는 혁신을 추구하고자 하는 현지 기업의 의향을 나타내고 있습니다. 현지 생산과 규제 당국의 신속한 대응을 통해 신제제의 시장 투입까지의 시간이 단축되고, 독소루비신 시장에서 현지공급자가 확고한 지위를 구축할 것으로 기대됩니다.

유럽은 정교한 환급 제도의 혜택을 받고 있지만 제네릭 의약품을 우대하는 예산 제약에 직면하고 있습니다. EMA에 의한 다수의 리포좀 제형의 승인은 임상의의 선택을 다양화하지만, 가격 설정에는 각국의 입찰 압력이 작용하고 있습니다. 남미에는 잠재적인 가능성이 있으며, 특히 브라질은 암 전문 병원의 확대와 바이오시밀러 의약품의 보급으로 환자 수가 증가하고 있습니다. 독소루비신 시장은 국내에서의 제제 제조 능력 향상으로 수입 의존도가 저하되어 국지적으로 활성화될 수 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계의 암 이환율의 상승과 화학요법량 증가

- 저렴한 제네릭 의약품과 리포좀 독소루비신의 이용 가능성 증가

- 치료 지수를 높이는 리포솜 나노캐리어 제제의 기술 진보

- 신흥 시장에서 정부가 주도하는 암 치료 프로그램 확대

- 혈액 악성 종양에 대한 독소루비신 병용 요법의 채용 증가

- 시장 성장 억제요인

- 엄격한 용량 제한 및 모니터링이 필요한 누적 심독성 위험

- 안트라사이클린계 약제를 대체하는 표적 치료제 및 면역종양약으로의 시프트

- 엄격한 위험물 취급 기준에 의한 유통 비용의 상승

- 공급망 분석

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 제형별

- 기존 독소루비신 주사제(용액)

- 동결건조 분말 제형

- PEG화 리포좀 독소루비신(PLD)

- 비PEG화 리포좀 독소루비신

- 용도(암 유형)별

- 유방암

- 난소암

- 백혈병

- 림프종

- 방광암

- 카포시육종

- 다발성 골수종

- 위암

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인/E-Commerce 약국

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Johnson & Johnson(Janssen)

- Sun Pharmaceutical Industries Ltd

- Pfizer Inc.

- Baxter International Inc.

- Teva Pharmaceutical Industries Ltd

- Cadila Pharmaceuticals Ltd

- Cipla Ltd

- Dr. Reddy's Laboratories Ltd

- Hikma Pharmaceuticals PLC

- Viatris(Mylan)

- Accord Healthcare

- Intas Pharmaceuticals Ltd

- Fresenius Kabi AG

- Celon Laboratories Pvt Ltd

- Zhejiang Hisun Pharmaceutical Co.

- Nantong Jinghua Pharmaceutical Co.

- Lupin Limited

- TTY Biopharm Co. Ltd

- Sandoz AG

제7장 시장 기회와 전망

CSM 25.11.03The global doxorubicin market is valued at USD 1.22 billion in 2025 and is projected to reach USD 1.67 billion by 2030, registering a 6.50% CAGR over the forecast period.

Robust clinical evidence keeps the agent at the center of many oncology protocols, and continuous advances in liposomal delivery expand its therapeutic window. Sustained cancer prevalence, wider generic availability, and targeted formulation innovations are reinforcing demand even as high-cost biologics compete for market share. At the same time, cardiotoxicity concerns, stricter hazardous-drug handling rules, and workflow shifts toward specialty pharmacy models temper longer-term uptake.

Global Doxorubicin Market Trends and Insights

Escalating Global Cancer Burden Elevating Chemotherapy Volumes

Rising worldwide cancer incidence is driving persistent use of broad-spectrum cytotoxics such as doxorubicin. Even as precision biologics proliferate, clinicians continue to rely on anthracycline-taxane combinations for breast tumors with high recurrence scores, showing superior survival versus taxane monotherapy in recent Phase 3 data presented at the San Antonio Breast Cancer Symposium. Versatility across solid and hematologic indications expands procedure volumes, reinforcing the doxorubicin market despite premium biologic entrants.

Growing Availability of Affordable Generic & Liposomal Doxorubicin

Intensifying generic competition is widening patient access and pressuring prices. New entrants such as Lupin introduced doxorubicin hydrochloride liposome injection in the United States in August 2024, enlarging the liposomal category and catalyzing broader adoption in budget-constrained health systems. This influx of lower-priced alternatives supports treatment equity in Asia-Pacific and Latin America, further stimulating doxorubicin market growth.

Cumulative Cardiotoxicity Risk Necessitating Strict Dose Caps & Monitoring

Anthracycline-induced cardiomyopathy limits lifetime exposure, with cumulative dose caps of 450-550 mg/m2 enshrined in guidelines. Although dexrazoxane offers partial protection, no other FDA-approved cardioprotective agent exists, forcing prescribers to juggle efficacy and long-term cardiac safety. This restraint slows repeat-cycle utilization within the doxorubicin market, spurring innovation in safer delivery platforms.

Other drivers and restraints analyzed in the detailed report include:

- Technological Progress in Liposomal & Nanocarrier Delivery

- Government-Led Cancer Care Expansion Programs in Emerging Markets

- Shift Toward Targeted Therapies and Immuno-Oncologics Displacing Anthracyclines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional injection maintained a 52% revenue contribution to the doxorubicin market in 2024, anchored in decades of clinical familiarity and competitive generic pricing. Pegylated liposomal doxorubicin, while only a fraction of earlier volume, is expanding at a 7.5% CAGR and is pivotal to enlarging the doxorubicin market size owing to reduced cardiac toxicity and prolonged circulation time. Regulatory approvals for advanced carriers such as Myocet and Celdoxome in Europe underscore a growing consensus that lipid-based vectors can safely extend cumulative dose ceilings. Research on pH-triggered nanocarriers and thermosensitive liposomes reveals promising preclinical data, suggesting that co-development of device-based hyperthermia triggers could structurally differentiate future entrants and compound competitive intensity in this formulation segment.

Continued supply stability of lyophilized powder formulations protects treatment access in regions lacking sophisticated cold chains, particularly parts of Africa and rural South America. Volume demand here, though modest, provides durable revenue streams for manufacturers with cost-focused portfolios inside the broader doxorubicin market.

The Doxorubicin Market Report is Segmented by Drug Formulation (Conventional Doxorubicin Injection (Solution), Lyophilized Powder for Reconstitution, and More), Application (Bladder Cancer, Ovarian Cancer, and More), Distribution Channel (Hospital Pharmacy, Retail Pharmacy, and Online / E-Commerce Pharmacy), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America remained the anchor geography with 48% of global revenue in 2024. Inpatient reimbursement structures, broad insurance coverage, and early adoption of cardioprotective delivery systems safeguard volume. Value-based contracts tying payments to progression-free survival may modify pricing headroom, yet the switch to liposomal variants is likely to sustain stable dollar growth for the regional doxorubicin market.

Asia-Pacific is set to be the principal acceleration engine, advancing at 8.3% CAGR to 2030. Rising diagnostic penetration, burgeoning private insurance pools in China and India, and government incentives for local manufacturing underpin robust demand. Sun Pharmaceutical Industries' oncology build-out via acquisitions such as the USD 355 million Checkpoint Therapeutics deal shows local players' intent to climb the innovation ladder. Indigenous production, combined with regulatory fast-tracking, is expected to shrink time-to-market for new formulations and entrench regional suppliers inside the doxorubicin market.

Europe benefits from a sophisticated reimbursement apparatus but faces budget constraints that favor generics. EMA approvals for multiple liposomal options diversify clinician choice yet subject pricing to national tender pressures. South America holds latent potential, particularly Brazil, where oncology hospital expansion and biosimilar uptake broaden patient throughput. Improvement in domestic fill-finish capabilities could lower import dependencies and stimulate localized segments of the doxorubicin market.

- Johnson & Johnson

- Sun Pharmaceuticals Industries

- Pfizer

- Baxter

- Teva Pharmaceutical Industries

- Cadila Pharmaceuticals Ltd

- Cipla

- Dr. Reddy's Laboratories

- Hikma Pharmaceuticals

- Viatris (Mylan)

- Accord Healthcare

- Intas Pharmaceutical

- Fresenius

- Celon Laboratories

- Zhejiang Hisun Pharmaceutical Co.

- Nantong Jinghua Pharmaceutical Co.

- Lupin

- TTY Biopharm Co. Ltd

- Sandoz Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Global Cancer Burden Elevating Chemotherapy Volumes

- 4.2.2 Growing Availability of Affordable Generic & Liposomal Doxorubicin

- 4.2.3 Technological Progress in Liposomal & Nanocarrier Delivery Enhancing Therapeutic Index

- 4.2.4 Government-Led Cancer Care Expansion Programs in Emerging Markets

- 4.2.5 Rising Adoption of Combination Regimens Featuring Doxorubicin for Hematologic Malignancies

- 4.3 Market Restraints

- 4.3.1 Cumulative Cardiotoxicity Risk Necessitating Strict Dose Caps & Monitoring

- 4.3.2 Shift Toward Targeted Therapies and Immuno-oncologics Displacing Anthracyclines

- 4.3.3 Stringent Hazardous-Drug Handling Standards Raising Distribution Costs

- 4.4 Supply-Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Drug Formulation

- 5.1.1 Conventional Doxorubicin Injection (Solution)

- 5.1.2 Lyophilized Powder for Reconstitution

- 5.1.3 Pegylated Liposomal Doxorubicin (PLD)

- 5.1.4 Non-Pegylated Liposomal Doxorubicin

- 5.2 By Application (Cancer Type)

- 5.2.1 Breast Cancer

- 5.2.2 Ovarian Cancer

- 5.2.3 Leukemia

- 5.2.4 Lymphoma

- 5.2.5 Bladder Cancer

- 5.2.6 Kaposi Sarcoma

- 5.2.7 Multiple Myeloma

- 5.2.8 Gastric Cancer

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacy

- 5.3.2 Retail Pharmacy

- 5.3.3 Online / E-commerce Pharmacy

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Johnson & Johnson (Janssen)

- 6.3.2 Sun Pharmaceutical Industries Ltd

- 6.3.3 Pfizer Inc.

- 6.3.4 Baxter International Inc.

- 6.3.5 Teva Pharmaceutical Industries Ltd

- 6.3.6 Cadila Pharmaceuticals Ltd

- 6.3.7 Cipla Ltd

- 6.3.8 Dr. Reddy's Laboratories Ltd

- 6.3.9 Hikma Pharmaceuticals PLC

- 6.3.10 Viatris (Mylan)

- 6.3.11 Accord Healthcare

- 6.3.12 Intas Pharmaceuticals Ltd

- 6.3.13 Fresenius Kabi AG

- 6.3.14 Celon Laboratories Pvt Ltd

- 6.3.15 Zhejiang Hisun Pharmaceutical Co.

- 6.3.16 Nantong Jinghua Pharmaceutical Co.

- 6.3.17 Lupin Limited

- 6.3.18 TTY Biopharm Co. Ltd

- 6.3.19 Sandoz AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment