|

시장보고서

상품코드

1842468

일렉트로크로믹 재료 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Electrochromic Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

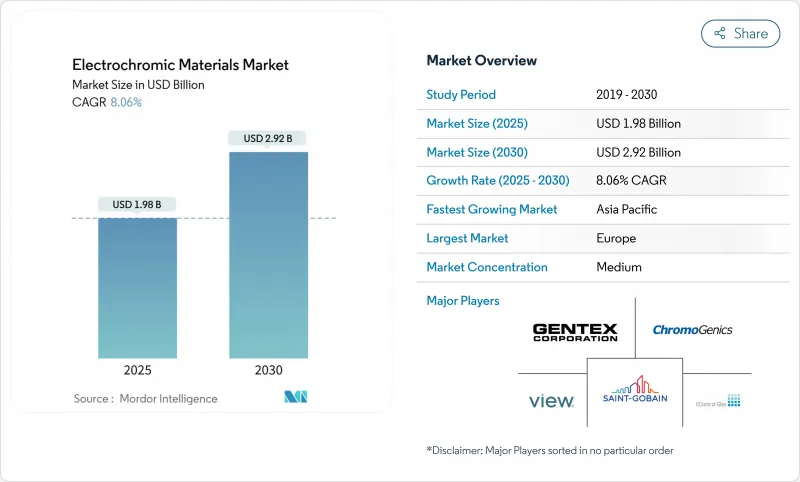

일렉트로크로믹 재료 시장은 2025년에 19억 8,000만 달러에 이를 전망으로, 2030년에는 29억 2,000만 달러로 성장하여 CAGR 8.06%로 성장할 것으로 예측됩니다.

이 성장은 에너지 효율 규제의 의무화, 장치 비용 저하, 그리고 건물, 자동차 및 항공기의 급속한 제품화를 반영합니다. 다이나믹 글레이징은 건물의 냉방 부하를 최대 39.5% 줄이고 일렉트로크로믹 재료 시장을 넷 제로 건축에 적합한 솔루션으로 자리매김하고 있습니다. 비용면의 약진에 의해 스마트 윈도우의 가격은 180-250 USD/m2에서 80 USD/m2로 하락하여, 보다 광범위한 개조 설치를 자극하고 있습니다. 유럽은 엄격한 탄소 규제로 선두를 이끌고 있지만 아시아태평양은 도시화 및 인프라 프로그램으로 급성장하고 있습니다. 제품 기술 혁신은 산화텅스텐의 내구성과 폴리머의 유연성에 중점을 두고 있으며, 경쟁은 저비용 제조 확대와 사이클 안정성 향상에 중점을 둡니다.

세계의 일렉트로크로믹 재료 시장의 동향과 인사이트

에너지 효율 규제가 스마트 윈도우의 채용을 가속

캘리포니아의 2025년 에너지 기준에서는 특정 창문 비율을 초과하는 건물에 발색 글레이징이 의무화되어 있으며, 미국의 다른 주가 평가하는 컴플라이언스 템플릿이 구축되어 있습니다. 2024년 국제 에너지 보존 규약에서는 U-팩터 제한과 공기 누설 임계값이 강화되어 건축가를 다이나믹 글레이징으로 유도하고 있습니다. 상하이의 2024년 광반사 평가 가이드라인은 아시아태평양의 규칙을 유럽의 규범에 맞추고자 하는 노력을 보여줍니다. ASHRAE 표준 90.1-2022는 정적 유리보다 일렉트로크로믹에 유리한 엔벨로프 컴플라이언스 경로를 명시하고 있습니다.

자동 조광 거울과 파노라마 선 루프에 대한 자동차 수요

Gentex는 2024년에 5,000만대 이상의 조광 디바이스를 출하하였으며, CES 2025에서 필름 베이스의 선루프를 발표하였습니다. Ambilight의 2세대 차량용 블랙 스마트 필름은 높은 적외선 차단율로 40배의 조광을 실현하여 전기자동차의 냉각 요건에 대응합니다. 현대의 나노냉각 필름은 시야를 어둡게 하지 않고 차내 온도를 10°C 내려 프리미엄 EV의 일렉트로크로믹 글레이징을 보완합니다. 자동차의 열 관리 의무화와 센서 통합의 동향은 일렉트로크로믹 재료 시장을 백미러 이외로도 확대하고 있습니다.

기존 코팅 유리에 비해 높은 단가

기존의 일렉트로크로믹 창유리는 1m2당 180-250달러이며 이러한 가격은 대량 채용의 방해가 되고 있습니다. 2024년에 발표된 무전극 장치는 비용을 1m2 당 80달러까지 줄여 Low-E 유리와 동등한 가격경쟁력을 보여주었습니다. 스케일링은 틈새 생산량에 의해 제한되지만, 자동차 생산량은 경제성 개선을 시사합니다.

부문 분석

금속 산화물은 2024년 매출의 49.42%를 차지하였으며, 산화텅스텐의 안정성이 입증된 일렉트로크로믹 재료 시장을 지원하고 있습니다. 이 부문의 사이클 내구성은 60°C에서 100,000 사이클을 초과하고 티타늄 인터칼레이트된 WO3는 85%의 광학 변조도와 95.61%의 가역성을 달성하였습니다. 전도성 폴리머는 PEDOT과 폴리아닐린의 유연성으로 롤러블 디스플레이에 적합하며 CAGR은 여전히 10.69%로 예상됩니다. MoS2를 도핑한 PEDOT는 70.28%의 발색 깊이를 달성하여 성능 갭을 줄이고 있습니다. 비올로겐과 플루시안 블루는 환경 감시에도 불구하고 틈새 컬러 스위치의 요구에 부응합니다.

금속 산화물 제조업체는 폴리머 필름에 적합한 얇은 코팅에 주목하고 있으며 폴리머 혁신기업은 UV 내성을 향상시키는 하이브리드 유기 금속 스택을 탐구합니다. 인듐-주석-옥사이드 타겟공급망은 아시아에, 고순도 삼산화텅스텐공급망은 유럽에 집중되어 있으며, 일렉트로크로믹 재료 시장에서 재료 안보의 우선사항이 부각되고 있습니다.

스마트 윈도우는 2024년에 46.04%의 점유율을 유지하였고 비용 저하로 프로젝트 파이프라인이 확대되면서 일렉트로크로믹 재료 시장의 핵심이 되고 있습니다. 건물 일체형 태양광 발전은 햇빛과 태양광 발전의 균형을 제공하므로 일렉트로크로믹층과의 조합이 증가하고 있습니다. 디스플레이는 물류 태그, 소매점 선반, 곡선형 자동차 클러스터에 적합한 바이스 테이블 인쇄 필름으로 인해 CAGR 11.02%로 성장을 지속하고 있습니다.

미러는 특히 북미의 경차 부문에서 안정적인 수익을 유지하고 있습니다. 필름은 개조 부문에서 점유율을 확대하고 코팅은 평면 유리로는 대응할 수 없는 맞춤형 모양을 제공합니다. 디바이스의 다양성은 단일 부문 순환성으로부터 공급업체를 보호하고 생산 계획을 원활하게 합니다.

지역 분석

유럽은 2030년 탄소 감축 목표의 구속력과 그린 리노베이션 프로젝트에 대한 보조금으로 2024년 매출의 33.15%를 유지했습니다. 스웨덴의 에너지청은 크로모제닉스에 450만 달러의 대출을 실시해, 국내의 일렉트로크로믹 생산 능력에 대한 정책적 신뢰를 보여주었습니다. 독일은 KfW의 효율화 우대 조치하에 설치를 주도하고 영국은 공공 건축물에 대한 스마트 윈도우 보조금을 확대하고 있습니다. 남유럽에서는 국가유산 개조 부문에서 눈부심 제어를 위한 높은 차광 수요가 증가하고 있습니다.

아시아태평양은 CAGR 11.07%로 가장 급성장하고 있는 지역이며, 중국의 적극적인 도시화와 광해 규제가 그 밑바탕이 되고 있습니다. 상하이의 2024년 반사법 규제는 규제 강화를 강조하고 있습니다. 일본은 자동차용 선루프 모듈공급 체인을 활용하고, 한국의 디스플레이 대기업은 플렉서블 일렉트로크로믹 대시보드를 공동 개발합니다. 정부의 넷 제로 로드맵과 높은 전기 요금이 투자 회수 계산을 가속화하여 일렉트로크로믹 재료 시장의 궤도를 확고하게 합니다.

북미에서는 캘리포니아주 조례와 항공우주산업 수요에 따라 일렉트로크로믹이 채용됩니다. 보잉과 에어버스의 제조 라인이 Gentex의 조광 창을 채용해, 안정된 재료 판매를 촉진하고 있습니다. 또한 상업 건물의 에너지 보수에 대한 연방 세액 공제가 기세를 늘리고 있습니다. 남미와 중동 및 아프리카는 아직 개발 도상지역이지만, 걸프의 공항과 접객 프로젝트는 사막의 태양 게인을 관리하는 동적 외관을 시험하고 있으며, 이는 중기적인 비즈니스 기회를 시사하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 스마트 윈도우 채용을 가속하는 에너지 효율 규제

- 자동 조광 미러 및 파노라마 선 루프에 대한 자동차 수요

- 경량화와 눈부심 감소를 목적으로 한 항공우주용 윈도우의 업그레이드

- 기존 건축물의 개조용 일렉트로크로믹 파사드 필름

- 정부에 의한 방위비 증가

- 시장 성장 억제요인

- 종래의 코팅 유리에 비해 높은 단가

- 사이클 안정성과 내구성의 과제

- 비올로겐 폐기물에 관한 환경 독성 기준의 보류

- 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 비올로겐

- 전도성 폴리머

- 금속 산화물

- 프러시안 블루

- 기타 제품 유형

- 디바이스 유형별

- 스마트 윈도우

- 미러

- 디스플레이

- 필름&코팅

- 기타 디바이스

- 폼 팩터별

- 유리 기판

- 폴리머 필름

- 잉크 및 도료

- 최종 사용자 산업별

- 자동차

- 전기 및 전자

- 건축 및 건설

- 항공우주 및 방위

- 기타 최종 사용자 산업

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- Changzhou YAPU new material Co., Ltd.

- ChromoGenics

- Crown Electrokinetics Corp.

- EControl-Glas GmbH & Co. KG

- GENTEX CORPORATION

- KIBING GROUP

- Kinestral Technologies(Halio)

- Ningbo Miruo Electronic Technology Co., Ltd.

- Polytronix, Inc.

- Ricoh

- Saint-Gobain

- View Inc.

- Zhuhai Kaivo Optoelectronic Technology Co., Ltd.

제7장 시장 기회와 전망

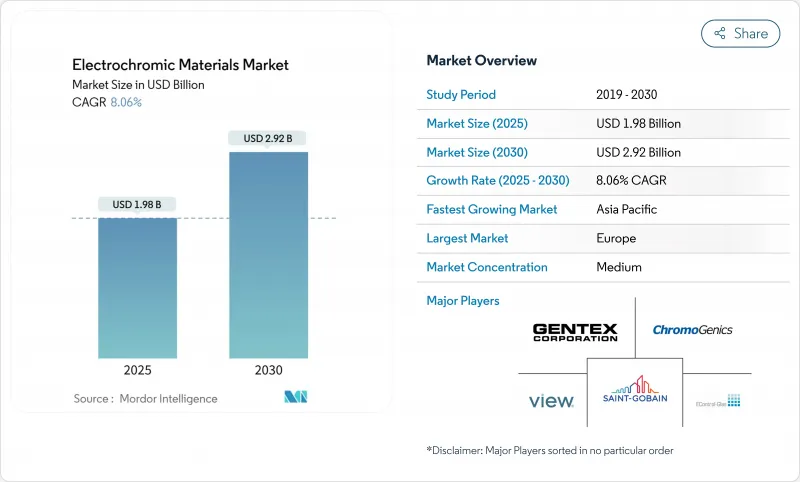

CSM 25.11.03The electrochromic materials market stands at USD 1.98 billion in 2025 and is projected to grow to USD 2.92 billion by 2030, advancing at an 8.06% CAGR.

The growth reflects mandatory energy-efficiency codes, falling device costs, and rapid product commercialization across buildings, vehicles, and aircraft. Dynamic glazing lowers building cooling loads by up to 39.5%, positioning the electrochromic materials market as a preferred solution for net-zero construction. Cost breakthroughs have cut smart-window prices to USD 80 per m2 from USD 180-250 per m2, stimulating wider retrofit adoption. Europe leads due to stringent carbon mandates, while Asia-Pacific grows fastest on urbanization and infrastructure programs. Product innovation pivots on tungsten-oxide durability and polymer flexibility, and competitive focus centers on scaling low-cost manufacturing and improving cycling stability.

Global Electrochromic Materials Market Trends and Insights

Energy-efficiency regulations accelerating smart-window adoption

California's 2025 Energy Code requires chromogenic glazing for buildings surpassing specific window-to-wall ratios, creating a compliance template that other U.S. states are evaluating. The 2024 International Energy Conservation Code tightens U-factor limits and air-leakage thresholds, steering architects toward dynamic glazing. Shanghai's 2024 guidelines on light-reflection assessments align Asia-Pacific rules with European norms sthj.sh.gov.cn. The Asian Development Bank underscores building efficiency as vital for decarbonizing rapidly growing cities, supporting sustained demand for the electrochromic materials market. ASHRAE Standard 90.1-2022 clarifies envelope compliance paths that favor electrochromic over static glass.

Automotive demand for auto-dimming mirrors and panoramic sunroofs

Gentex shipped more than 50 million dimmable devices in 2024 and introduced film-based sunroofs at CES 2025, reducing system weight and enabling larger panoramic apertures. Ambilight's second-generation whole-vehicle black smart film delivers 40X dimming with high infrared rejection, addressing electric-vehicle cooling requirements. Hyundai's nano-cooling film cuts cabin temperature by 10 °C without darkening the view, complementing electrochromic glazing in premium EVs. Automotive thermal management mandates and sensor-integration trends are expanding the electrochromic materials market far beyond rearview mirrors.

High unit cost versus conventional coated glass

Traditional electrochromic windows cost USD 180-250 per m2, deterring mass adoption. Electrode-free devices published in 2024 slash cost to USD 80 per m2, signaling a path to parity with low-E glass. Scaling remains limited by niche production volumes, but automotive volumes hint at improving economies.

Other drivers and restraints analyzed in the detailed report include:

- Aerospace window upgrades for weight and glare reduction

- Retro-fit electrochromic facade films for existing buildings

- Cycling-stability and durability challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal oxides accounted for 49.42% of 2024 revenue, anchoring the electrochromic materials market with proven tungsten-oxide stability. The segment's cycling durability surpasses 100,000 cycles at 60 °C, and titanium-intercalated WO3 reaches 85% optical modulation and 95.61% reversibility. Conducting polymers trail yet post a 10.69% CAGR, propelled by PEDOT and polyaniline flexibility that suits rollable displays. MoS2-doped PEDOT achieves 70.28% coloration depth, narrowing performance gaps. Viologens and Prussian Blue serve niche color-switching needs despite environmental scrutiny.

Metal-oxide makers pivot toward thinner coatings compatible with polymer films, while polymer innovators explore hybrid metal-organic stacks to improve UV tolerance. Supply chains remain concentrated in Asia for indium-tin-oxide targets and in Europe for high-purity tungsten trioxide, underscoring material security priorities for the electrochromic materials market

Smart windows retained a 46.04% stake in 2024 and will stay the backbone of the electrochromic materials market as cost drops expand project pipelines. Building-integrated photovoltaics increasingly pair with electrochromic layers to balance daylight and solar power. Displays, though smaller, log an 11.02% CAGR thanks to printed, bi-stable films suited to logistics tags, retail shelving, and curved automotive clusters.

Mirrors remain a stable revenue stream, especially in North American light vehicles. Films gain share in retrofits, while coatings enable custom shapes that flat glass cannot address. Device diversity protects suppliers from single-segment cyclicality and smooths production planning.

The Electrochromic Materials Market Report Segments the Industry by Product Type (Viologens, Conducting Polymers, and More), Device Type (Smart Windows, Mirrors, and More), Form Factor (Glass Substrates, Polymer Films, and More), End-User Industry (Automotive, Electrical and Electronics, and More) and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe retained 33.15% of 2024 revenue, propelled by binding 2030 carbon targets and subsidies for green-renovation projects. Sweden's energy agency converted a USD 4.5 million loan to ChromoGenics, signaling policy trust in domestic electrochromic capacity. Germany leads installations under KfW efficiency incentives, while the United Kingdom extends smart-window grants in public buildings. Southern Europe adds high-insolation demand for glare control in heritage retrofits.

Asia-Pacific is the fastest-growing region at an 11.07% CAGR, underpinned by China's aggressive urbanization and light-pollution rules that favor adaptive facades. Shanghai's 2024 reflection code underscores regulatory tightening. Japan leverages automotive supply chains for sunroof modules, while South Korea's display majors co-develop flexible electrochromic dashboards. Government net-zero roadmaps and high electricity tariffs accelerate payback calculations, cementing the electrochromic materials market trajectory.

North America adopts through leading California codes and aerospace demand. Boeing and Airbus lines integrate Gentex dimmable windows, driving steady material off-take. Federal tax credits for commercial-building energy retrofits add momentum. South America and Middle East & Africa remain nascent; however, Gulf airports and hospitality projects trial dynamic facades to manage desert solar gain, signaling medium-term opportunities.

List of Companies Covered in this Report:

- Changzhou YAPU new material Co., Ltd.

- ChromoGenics

- Crown Electrokinetics Corp.

- EControl-Glas GmbH & Co. KG

- GENTEX CORPORATION

- KIBING GROUP

- Kinestral Technologies (Halio)

- Ningbo Miruo Electronic Technology Co., Ltd.

- Polytronix, Inc.

- Ricoh

- Saint-Gobain

- View Inc.

- Zhuhai Kaivo Optoelectronic Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy-efficiency regulations accelerating smart-window adoption

- 4.2.2 Automotive demand for auto-dimming mirrors and panoramic sunroofs

- 4.2.3 Aerospace window upgrades for weight and glare reduction

- 4.2.4 Retro-fit electrochromic facade films for existing buildings

- 4.2.5 Increase in defense spending by the government

- 4.3 Market Restraints

- 4.3.1 High unit cost versus conventional coated glass

- 4.3.2 Cycling-stability & durability challenges

- 4.3.3 Pending ecotoxicity norms on viologen waste streams

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products & Services

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Viologens

- 5.1.2 Conducting Polymers

- 5.1.3 Metal Oxides

- 5.1.4 Prussian Blue

- 5.1.5 Other Product Types

- 5.2 By Device Type

- 5.2.1 Smart Windows

- 5.2.2 Mirrors

- 5.2.3 Displays

- 5.2.4 Films & Coatings

- 5.2.5 Other Devices

- 5.3 By Form Factor

- 5.3.1 Glass Substrates

- 5.3.2 Polymer Films

- 5.3.3 Inks & Paints

- 5.4 By End-User Industry

- 5.4.1 Automotive

- 5.4.2 Electrical and Electronics

- 5.4.3 Building and Construction

- 5.4.4 Aerospace and Defense

- 5.4.5 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Changzhou YAPU new material Co., Ltd.

- 6.4.2 ChromoGenics

- 6.4.3 Crown Electrokinetics Corp.

- 6.4.4 EControl-Glas GmbH & Co. KG

- 6.4.5 GENTEX CORPORATION

- 6.4.6 KIBING GROUP

- 6.4.7 Kinestral Technologies (Halio)

- 6.4.8 Ningbo Miruo Electronic Technology Co., Ltd.

- 6.4.9 Polytronix, Inc.

- 6.4.10 Ricoh

- 6.4.11 Saint-Gobain

- 6.4.12 View Inc.

- 6.4.13 Zhuhai Kaivo Optoelectronic Technology Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment