|

시장보고서

상품코드

1842537

입자선 치료 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Particle Therapy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

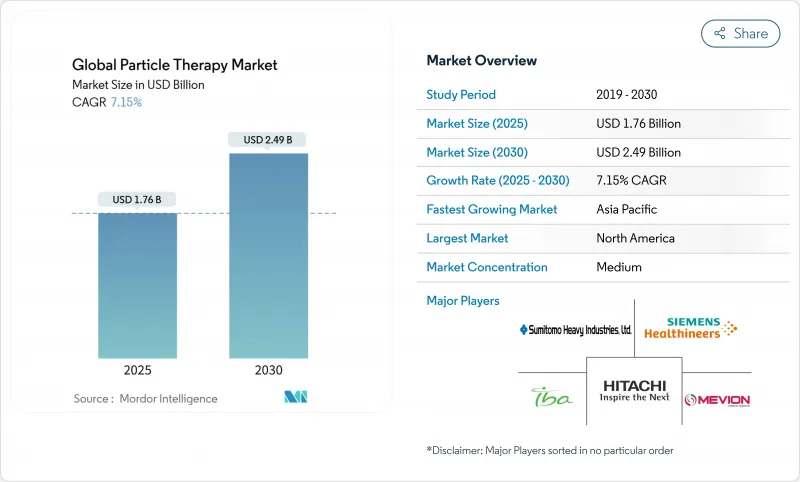

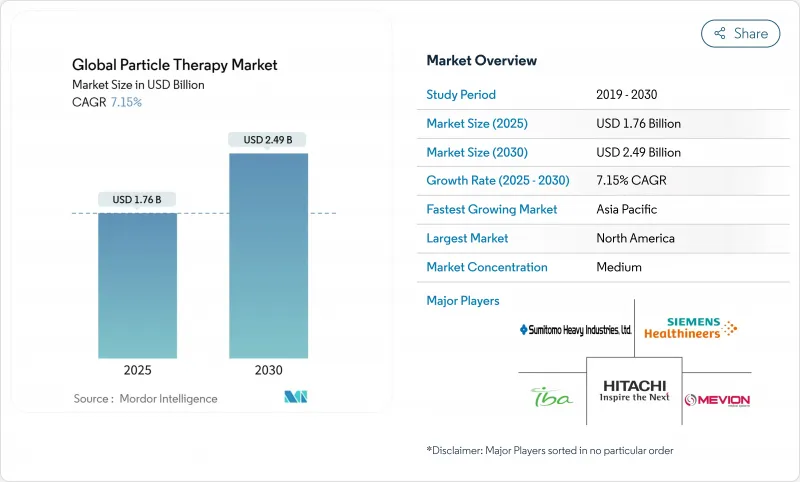

입자선 치료 시장은 2025년에 17억 6,000만 달러로 추정되고, 2030년에는 24억 9,000만 달러에 이를 것으로 예측됩니다.

현재의 성장은 정밀 종양학 장비에 대한 지속적인 투자, 세계적인 암 이환율의 꾸준한 상승, 지속적인 진료 보상 개선으로 인한 환자 적용 범위 확대로 인한 것입니다. 벤더는 토목 공사 예산을 최대 60%까지 줄일 수 있는 컴팩트한 싱글룸 시스템으로 수요를 획득하고 있으며, 중규모 병원이 여러 방을 갖춘 벙커를 건설하지 않고 이 분야에 진입할 수 있도록 하고 있습니다. 초고선량은 수 밀리초 내에 치료를 종료하고 정상 조직의 독성을 감소시키기 때문에 소아 및 성인 모두의 코호트에서 공진하는 이점이 있습니다. 메디케어의 2024년 지역 보험 적용 결정과 일본의 탄소 이온 치료 보험 수재를 필두로, 지지적인 정책 환경은 단기적인 수익의 확실성을 가져오고, 인공지능 계획 툴은 노동력 부족에 의한 워크플로우의 병목을 완화하고 있습니다. 이러한 요인을 종합하면, 입자선 치료 시장 전망은 밝고, 예측 기간 중에도 자본 형성은 견조하게 추이할 것으로 보입니다.

세계의 입자선 치료 시장 동향 및 인사이트

플래시 선량 전달의 진보

FLASH 방사선 치료는 40Gy/s를 넘는 선량률을 제공하고 치료 코스 전체를 1초 이하의 조사로 응축함으로써 주변 조직을 온존합니다. 스탠포드 대학과 펜실베니아 대학에서 실시한 전임상시험과 초기 단계의 인간시험에서는 종양제어가 동등하면서도 섬유증이나 피부염이 현저히 적은 것으로 보고되어 있어 폭넓은 프로토콜의 등록을 뒷받침하고 있습니다. 기존의 사이클로트론 라인은 최소한의 하드웨어 업그레이드로 FLASH를 통합할 수 있기 때문에 기존 병원에 있어서 비용 효율적인 차별화 요인이 됩니다. 규제 당국의 논의는 현재 기본 안전성보다 합의를 얻은 선량 검증 기술에 초점을 맞추고 있으며, 다시설 시험이 곧 가이드라인을 형성하는 3상 시험으로 발전할 것임을 보여줍니다. 독성과 관련된 합병증의 감소가 지불자에게 인식됨에 따라 가치 기반 상환 프레임 워크가 가속화되고 이 운전자의 성장 공헌이 강화될 것으로 예측됩니다.

세계적인 암 이환율 상승

WHO는 2022년에 2,000만 명의 신규암 환자를 기록하고, 2050년에는 3,500만 명에 달할 것으로 예측했습니다. 신흥국은 헬스케어 인프라가 대응할 수 있는 것보다 빠른 이환율의 성장을 목격하고 있어, 휴대형 또는 후부 가능한 입자 센터의 중요성을 높이고 있습니다. 일본이나 한국과 같은 고령화 사회에서는 생존자가 앞으로 20년은 살아가는 경우가 많기 때문에 종양 의사는 2차 악성 종양을 억제하는 치료를 요구하고 있습니다. 소아암 증가는 선진지역에서는 매년 0.8%로 완만하지만, 불균형에 높은 질조정 생존년(QALY) 이익을 가져, 입자선 치료의 가치 제안을 확고하게 하고 있습니다. 이러한 역학적 조류는 입자선 치료 시장의 수익원으로 직접 연결되는 환자 수의 꾸준한 확대를 지원합니다.

빔라인 인프라의 고액 CAPEX와 OPEX

비용 절감 후에도 턴키 프로젝트는 종종 5,000만 달러를 초과하여 기존 선형 업데이트 예산을 능가합니다. 차폐, 극저온 및 전력 조정 시스템은 운영 비용을 상승시키고 연간 서비스 계약은 300만 달러에 이릅니다. 종양학의 마진이 적은 병원에서는 지역의 지불자가 감가상각비와 서비스 오버헤드를 모두 커버하는 레이트로 환불을 하지 않는 한, 이 숫자를 정당화하는 데 고생합니다. 자본 보조금은 유한하기 때문에 하나의 큰 입자 프로젝트가 다른 장비 구매를 밀어 조직의 타성을 유발할 수 있습니다. 공급업체가 2,000만 달러 이하의 시스템을 대규모로 출시하기 전까지는 자본 집약도가 입자선 치료 시장의 가장 큰 발판인 것으로 보입니다.

부문 분석

양자선 치료는 2024년의 입자선 치료 시장 점유율 82.72%를 차지했으며, 견고한 제III상 근거의 기반, 지불자의 익숙함, 싱글룸 설치의 파이프라인에 지지되고 있습니다. 중립자선 치료는 저산소 종양 및 방사선 저항성 종양에 대한 상대적인 생물학적 효과가 우수함을 배경으로 2030년까지 연평균 복합 성장률(CAGR) 8.17%에서 성장하는 가장 빠른 치료법입니다. 연세대학 암센터(Yonsei Cancer Center)와 같은 조기 도입 기업은 한국성 전립선 프로토콜에서 97.5%의 5년 전체 생존율을 보고하고 양자선 벤치마크를 넘는 결과를 내고 있습니다. 메이요 클리닉이 곧 탄소 이온 장치를 가동시켜 입자선 치료 시장에서 중립자선 전문지식에 대한 수요가 파급되면 북미에서의 수용이 가속될 가능성이 있습니다. 컴팩트한 탄소 이온 플랫폼이 성숙함에 따라 경제적 장벽은 좁아져 2030년 이후 더욱 균형 잡힌 모달리티 믹스가 실현됩니다.

양자선 공급업체의 움직임도 변하지 않습니다. FLASH 기능, 강도 변조 스캔, AI 대응 데일리 리플래닝을 포함한 시스템은 임상 천장을 계속 확장하고 있습니다. 한편, 탄소 이온의 혁신자는 초전도 갠트리를 통합하여 자석의 질량과 시설 범위를 줄입니다. 양자선 플랫폼은 중립자선 빔 스티어링 알고리즘을 채용하고, 중립자선 시스템은 양자선 시대의 QA 자동화를 활용하는 등 기술의 상호 수분이 기대되고 있습니다. 이러한 경쟁은 입자 방사선 치료 시장의 활력을 유지하고 다중 양식 포트폴리오를 유지하는 공급업체에게 유리합니다.

레거시 허브는 연간 1,000명 이상의 환자를 치료하고 있으며, 스케일 메리트의 혜택을 받고 있기 때문에 멀티룸 센터는 2024년 입자선 치료 시장 규모의 63.17%를 차지했습니다. 그러나 CFO가 메가 프로젝트보다 모듈식 확장을 선호하기 때문에 싱글 룸 풋 프린트는 CAGR 7.92% 상승했습니다. 애틀랜틱 헬스가 기존 선형 보관실을 개조한 시설은 이 모델의 경제적 매력을 입증합니다. 현대의 컴팩트한 장치는 각 방에 대해 독립적인 사이클로트론으로 작동되기 때문에 빔 스위칭 설계의 역사적인 단점이었던 한 방에서 가동 중지 시간이 발생해도 전체 시설이 멈추지 않습니다.

엔지니어링 측면에서 자석의 소형화와 에너지 선택 시스템의 개선으로 싱글 룸 솔루션은 대규모와 동등한 임상 범위를 커버할 수 있게 되었고, 트레이드오프의 우려가 없어졌습니다. 벤더는 1개의 보관실에서 시작하여 증례 수가 늘어남에 따라 3개, 4개로 확장해 나가는 단계적인 구축을 판매하고 있어 관리자에게 자본 지출에 관한 옵션을 주고 있습니다. 임대 및 관민 파트너십이 성숙함에 따라 단일 보관실 증가가 다중 보관실 증가를 능가하고 입자선 치료 시장에서의 분산화 경향이 커질 것으로 예측됩니다.

본 보고서는 입자선 치료 시장 예측을 커버하고 유형별(양자선 치료, 중립자선 치료), 시스템별(멀티룸 시스템, 싱글룸 시스템), 암 유형별(소아암, 전립선암, 기타), 용도별(치료, 임상 연구), 지역별로 구분하고 있습니다. 상기 부문에 대해 시장 세분화을 게재하고 있습니다.

지역별 분석

북미는 2024년 입자선 치료 시장의 44.61%를 차지했습니다. 메디케어의 적용 범위가 확대됨에 따라 현금 흐름이 안정되고 40개가 넘는 운영센터의 확립된 파이프라인이 여러실의 확장을 계속하고 있습니다. 펜메디신의 2억 2,400만 달러에 달하는 로버츠 양자선 치료 센터의 확장은 중복성을 위해 독립적인 사이클로트론을 포함한 차세대 보관소에 대한 투자 의욕을 보여줍니다. 아카데믹 에코시스템은 안정적인 소개 흐름을 창출하고 자선 캠페인은 자본 비용의 일부를 흡수하며 예산 위험을 완화합니다. 미국은 또한 대부분의 상업 OEM 본사와 타사 서비스 회사를 보유하고 있으며 공급망의 안전성을 강화하고 있습니다. 캐나다는 여전히 국내 센터가 없는 이단아이지만, 온타리오주와 퀘벡주의 주 태스크포스가 입지선정조사를 진행하고 있으며, 지역 수요가 조만간 조달 입찰에 연결될 조짐을 보이고 있습니다.

아시아태평양은 CAGR 9.25%로 가장 급성장하는 지역으로, 공공 부문에 대한 지출과 노인 인구로의 인구통계학적 변화가 그 원동력이 되고 있습니다. 중국에서는 플래그쉽 시설과 비용 파괴적인 진출 기업이 혼합되어 있습니다. 산동성에 있는 P-Cure사의 초소형 시스템은 3,000만 달러 미만의 가격으로, 입자선 치료를 2차 도시에 도입하는 지역 전략의 일례입니다. 한국에서는 2024년 연세대학의 중립자선 시설이 가동되어 전립선암 이외의 광범위한 증례 등록이 이미 예비 데이터로 뒷받침되고 있습니다. 호주의 브래그 센터는 공급업체의 재구성에 직면하고 있는 것, 초당파의 헌신을 유지하고 있으며, 규제 당국의 승인이 구조적 장애가 아니라 일시적인 것임을 보여줍니다. 지역 정부는 종종 가속기 조달과 국내 제조 의무화를 설정하여 공급망의 현지화를 장려하고 장기 운영 경비를 절감하고 있습니다.

유럽에서는 기술 향상과 생산 능력 증가라는 이중 이야기가 전개되고 있습니다. 독일의 탄소 이온 센터는 일상적인 치료 및 여러 시설에서의 임상시험 양면에서 리더십을 발휘하고 있으며, 이 지역을 중립자선 전문 기술의 세계적인 허브로 자리잡고 있습니다. 프랑스와 이탈리아에서는 관민 공동 사업이 양자선 치료의 범위를 확대하고, 드레스덴에서는 MRI 가이드 양자선 프로토타입이 임상 준비를 향해 전진하고 있습니다. 국경을 넘어서는 소개 협정을 통해 소국은 이웃 센터에 복잡한 사례를 보내 이용을 최적화할 수 있습니다. 한편, 중동 및 아프리카, 남미는 초기 단계의 가능성을 지니고 있습니다. 아르헨티나의 230톤 사이클로트론 설치는 라틴아메리카가 입자선 치료 시장에 처음으로 진입했음을 보여주며, 사우디아라비아와 아랍 에미리트 연합에서는 예비 실현 가능성 조사가 진행 중입니다. 이를 종합하면 지리적 분산이 공급업체의 위험을 분산하고 장기적인 성장을 유지하는 다층적 수요 프로파일을 생성하게 됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고령자 인구 증가 및 질병 부담 증가

- 인지도 향상 및 조기 진단에 대한 대처

- 상환 및 보험 적용 확대

- 연구개발 투자 증가 및 지속적인 의약품 승인

- 장시간 작용형 지속 점적 제제의 채용

- A-시누클레인을 표적으로 한 AI 주도의 의약품 재이용 파이프라인

- 시장 성장 억제요인

- 현재 치료제와 관련된 부작용

- 높은 치료비 및 연구개발비

- 레보도파 아피스 공급망에 있어서의 제약

- 질환 수식성에 관한 규제상의 불확실성

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 작용기전별

- 도파민 작용제

- 항콜린제

- MAO-B 억제제

- 아만타딘

- 칼비도파-레보도파

- 아데노신 A2A 길항제

- 기타 작용 기작

- 투여 경로별

- 경구

- 경피

- 피하

- 점적

- 경비

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인 약국

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- AbbVie Inc.

- Amneal Pharmaceuticals LLC

- Viatris

- Boehringer Ingelheim Intl. GmbH

- GSK plc

- Teva Pharmaceutical Industries Ltd

- Pfizer Inc.

- Novartis AG

- F. Hoffmann-La Roche Ltd

- ABL bio

- Kissei Pharmaceutical Co., Ltd.

- AstraZeneca

- Prevail Therapeutics

- Newron Pharmaceuticals SpA

- Kyowa Kirin Co., Ltd.

- ACADIA Pharmaceuticals Inc.

- UCB SA

- Sunovion Pharmaceuticals Inc.

- Neurocrine Biosciences, Inc.

- Lundbeck A/S

- Voyager Therapeutics, Inc.

- Supernus Pharmaceuticals, Inc.

제7장 시장 기회 및 전망

AJY 25.10.29The particle therapy market stands at USD 1.76 billion in 2025 and is projected to reach USD 2.49 billion by 2030, reflecting a healthy 7.15% CAGR.

The current growth comes from sustained investments in precision oncology equipment, a steady rise in global cancer incidence, and continuous reimbursement improvements that are widening patient eligibility. Vendors are capturing demand through compact single-room systems that trim civil-works budgets by up to 60%, allowing mid-sized hospitals to enter the field without building multi-room bunkers. Clinical momentum behind FLASH-dose delivery is further enlarging the total addressable patient pool, because ultra-high dose rates finish treatment in milliseconds and reduce normal-tissue toxicity, an advantage that resonates with both pediatric and adult cohorts. A supportive policy environment-most notably Medicare's 2024 local-coverage determinations and Japan's national insurance listing of carbon-ion therapy-provides near-term revenue certainty, while artificial-intelligence planning tools are easing workflow bottlenecks created by workforce shortages. Collectively, these factors sustain the particle therapy market's positive outlook and signal that capital formation will stay robust well into the forecast window.

Global Particle Therapy Market Trends and Insights

Advances in FLASH-dose Delivery

FLASH radiotherapy delivers dose rates above 40 Gy/s, condensing an entire curative course into a single sub-second exposure that spares surrounding tissue . Pre-clinical and early-phase human studies at Stanford and the University of Pennsylvania report comparable tumor control yet markedly lower fibrosis and dermatitis, supporting broader protocol enrollment. Existing cyclotron lines can integrate FLASH with minimal hardware upgrade, making it a cost-effective differentiator for incumbent hospitals. Regulatory discussions now focus on consensus dose-verification techniques rather than foundational safety, signaling that multi-center trials will soon evolve into guideline-shaping phase III studies. As payers recognize lower toxicity-related complications, value-based reimbursement frameworks are expected to accelerate, reinforcing the driver's growth contribution.

Rising Global Cancer Incidence

WHO recorded 20 million new cases in 2022 and forecasts 35 million by 2050, a trajectory that intensifies demand for modality portfolios capable of minimizing late-stage side effects. Emerging economies are witnessing faster incidence growth than their healthcare infrastructure can match, magnifying the relevance of portable or retrofittable particle centers. In aging societies like Japan and South Korea, oncologists seek treatments that limit secondary malignancies because survivors often live another two decades. The rise in pediatric cancers, though modest at 0.8% annually in developed regions, carries disproportionately high quality-adjusted life-year (QALY) gains, cementing particle therapy's value proposition. This epidemiological tide underpins steady patient volume expansion that feeds directly into particle therapy market revenue streams.

High CAPEX & OPEX of Beamline Infrastructure

Even after cost reductions, turnkey projects often exceed USD 50 million, dwarfing conventional linac replacement budgets. Shielding, cryogenics, and power-conditioning systems escalate operating costs, with annual service contracts reaching USD 3 million. Hospitals with thin oncology margins struggle to justify these figures unless local payers reimburse at rates that cover both depreciation and service overhead. Because capital grants are finite, a single large particle project can crowd out other equipment purchases, causing institutional inertia. Until vendors unlock sub-USD 20 million systems at scale, capital intensity will remain the most significant drag on the particle therapy market.

Other drivers and restraints analyzed in the detailed report include:

- Improved Reimbursement Frameworks (US & JP)

- Technological Shift to Compact Single-Room Systems

- AI-based Adaptive Treatment Planning

- Shortage of Particle-Physics Trained Staff

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Proton therapy accounted for an 82.72% particle therapy market share in 2024, buoyed by a robust base of phase III evidence, payer familiarity and a pipeline of single-room installations. Heavy-ion therapy is the fastest mover, growing at 8.17% CAGR to 2030 on the back of superior relative biological effectiveness against hypoxic or radioresistant tumors. Early adopters such as Yonsei Cancer Center reported five-year overall survival of 97.5% in localized prostate protocols, results that transcend proton benchmarks. North American acceptance could accelerate once Mayo Clinic's forthcoming carbon-ion unit enters service, creating spill-over demand for heavy-ion expertise within the particle therapy market. As compact carbon-ion platforms mature, the economic barrier narrows, signaling a more balanced modality mix beyond 2030.

Proton vendors have not remained static. Systems incorporating FLASH capability, intensity-modulated scanning and AI-enabled daily replanning continue to widen the clinical ceiling. Meanwhile, carbon-ion innovators are integrating superconducting gantries to cut magnet mass and facility span. Technology cross-pollination is expected, with proton platforms adopting heavy-ion beam-steering algorithms and heavy-ion systems leveraging proton-era QA automation. The competitive interplay keeps the particle therapy market dynamic and favors suppliers who maintain a multi-modality portfolio.

Multi-room centers held 63.17% share of the particle therapy market size in 2024 because legacy hubs treat 1,000+ patients yearly and benefit from economies of scale. However, single-room footprints are climbing 7.92% CAGR as CFOs prioritize modular expansion over mega-projects. Facilities like Atlantic Health's retrofit of an existing linac vault-notably completed 40% faster than a greenfield build-prove the model's economic appeal. The newest compact units operate with independent cyclotrons per room, so downtime in one suite no longer halts the entire complex, a historical disadvantage of beam-switching designs.

On the engineering front, magnet miniaturization and improved energy selection systems allow single-room solutions to match the clinical reach of their larger cousins, eliminating trade-off concerns. Vendors market phased build-outs that start with one vault and scale to three or four as case volume rises, giving administrators capital-spend optionality. As leasing and public-private partnerships mature, single-room growth is expected to outstrip multi-room additions, reinforcing the decentralizing trend within the particle therapy market.

The Report Covers Particle Therapy Market Forecast and It is Segmented by Type (Proton Therapy and Heavy Ion Therapy), System (Multi-Room Systems, and Single-Room Systems), Cancer Type (Pediatric Cancer, Prostate Cancer, and More), Application (Therapeutic and Clinical Research), and Geography. The Market Values are Provided (in USD Million) for the Above Segments.

Geography Analysis

North America controlled 44.61% of the particle therapy market in 2024. Medicare's broadened coverage stabilized cash flows, and an established pipeline of more than 40 operational centers continues to undertake multi-room expansions. Penn Medicine's USD 224 million Roberts Proton Therapy Center extension illustrates the region's willingness to invest in next-generation vaults that include independent cyclotrons for redundancy. Academic ecosystems funnel steady referral streams, while philanthropic campaigns absorb portions of capital costs, mitigating budget risk. The United States also houses most commercial OEM headquarters and third-party service firms, reinforcing supply-chain security. Canada remains an outlier with no domestic center, but provincial task forces in Ontario and Quebec have advanced site-selection studies, a sign that regional demand will soon convert into procurement tenders.

Asia-Pacific is the fastest-growing region at 9.25% CAGR, fueled by public-sector spending and demographic shifts toward older populations. China hosts an expanding mix of flagship institutions and cost-disruptive entrants. P-Cure's ultra-compact system in Shandong, priced below USD 30 million, exemplifies a local strategy to bring particle therapy into secondary cities . South Korea commissioned the Yonsei heavy-ion facility in 2024, and preliminary data already support broader case enrollment beyond prostate cancer. Australia's Bragg Centre, though facing vendor realignment after delays, retains bipartisan commitment, indicating that regulatory approvals are temporary rather than structural obstacles. Regional governments often pair accelerator procurement with domestic-manufacturing mandates, stimulating supply-chain localization that lowers long-term operating expenditures.

Europe presents a dual narrative of technological sophistication and incremental capacity growth. Germany's carbon-ion centers deliver both routine care and multi-site trial leadership, positioning the region as a global hub for heavy-ion expertise. Public-private joint ventures in France and Italy are expanding proton reach, while MRI-guided proton prototypes in Dresden edge toward clinical readiness. Cross-border referral agreements allow smaller nations to send complex cases to neighboring centers, optimizing utilization. Meanwhile, the Middle East, Africa and South America hold early-stage potential. Argentina's 230-tonne cyclotron installation signals Latin America's first foray into the particle therapy market, and preliminary feasibility studies are underway in Saudi Arabia and the United Arab Emirates. Collectively, geographic diversification spreads supplier risk and creates multi-tier demand profiles that sustain long-run growth.

- Abbvie

- Amneal Pharmaceuticals

- Viatris

- Boehringer Ingelheim Intl. GmbH

- GlaxoSmithKline

- Teva Pharmaceutical Industries

- Pfizer

- Novartis

- Roche

- ABL bio

- KISSEI PHARMACEUTICAL

- AstraZeneca

- Prevail Therapeutics

- Newron Pharmaceuticals S.p.A.

- Kyowa Kirin

- ACADIA Pharmaceuticals Inc.

- UCB

- Sunovion Pharmaceuticals

- Neurocrine Biosciences

- Lundbeck A/S

- Voyager Therapeutics, Inc.

- Supernus Pharmaceuticals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Geriatric Population & Rising Disease Burden

- 4.2.2 Growing Awareness & Early Diagnosis Initiatives

- 4.2.3 Expanding Reimbursement & Insurance Coverage

- 4.2.4 Increasing R&D Investment & Continuous Drug Approvals

- 4.2.5 Adoption Of Long-Acting Continuous Infusion Formulations

- 4.2.6 Ai-Driven Drug-Repurposing Pipelines Targeting A-Synuclein

- 4.3 Market Restraints

- 4.3.1 Adverse Events Associated With Current Therapeutics

- 4.3.2 High Treatment & R&D Costs

- 4.3.3 Supply-Chain Constraints For Levodopa Apis

- 4.3.4 Regulatory Uncertainty Around Disease-Modifying Claims

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD million)

- 5.1 By Mechanism of Action

- 5.1.1 Dopamine Agonists

- 5.1.2 Anticholinergics

- 5.1.3 MAO-B Inhibitors

- 5.1.4 Amantadine

- 5.1.5 Carbidopa-levodopa

- 5.1.6 Adenosine A2A Antagonists

- 5.1.7 Other Mechanisms of Action

- 5.2 By Route of Administration

- 5.2.1 Oral

- 5.2.2 Transdermal

- 5.2.3 Subcutaneous

- 5.2.4 Infusion

- 5.2.5 Intranasal

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Amneal Pharmaceuticals LLC

- 6.3.3 Viatris

- 6.3.4 Boehringer Ingelheim Intl. GmbH

- 6.3.5 GSK plc

- 6.3.6 Teva Pharmaceutical Industries Ltd

- 6.3.7 Pfizer Inc.

- 6.3.8 Novartis AG

- 6.3.9 F. Hoffmann-La Roche Ltd

- 6.3.10 ABL bio

- 6.3.11 Kissei Pharmaceutical Co., Ltd.

- 6.3.12 AstraZeneca

- 6.3.13 Prevail Therapeutics

- 6.3.14 Newron Pharmaceuticals S.p.A.

- 6.3.15 Kyowa Kirin Co., Ltd.

- 6.3.16 ACADIA Pharmaceuticals Inc.

- 6.3.17 UCB S.A.

- 6.3.18 Sunovion Pharmaceuticals Inc.

- 6.3.19 Neurocrine Biosciences, Inc.

- 6.3.20 Lundbeck A/S

- 6.3.21 Voyager Therapeutics, Inc.

- 6.3.22 Supernus Pharmaceuticals, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment