|

시장보고서

상품코드

1842617

의료기기 위탁 생산 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Medical Device Contract Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

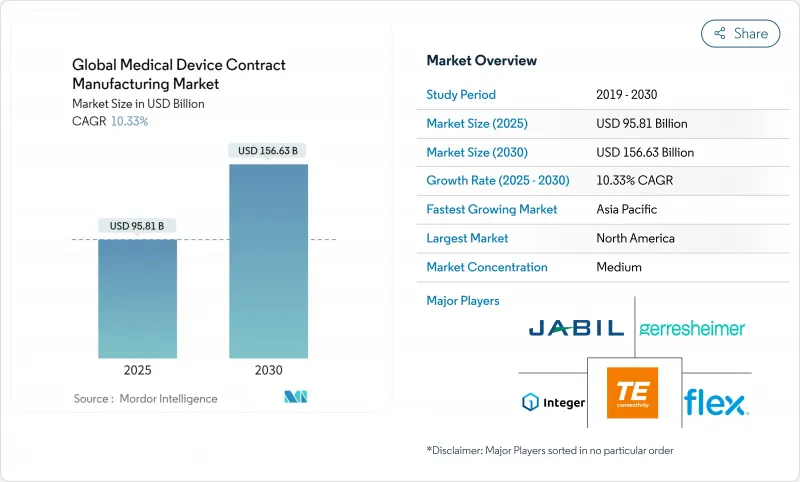

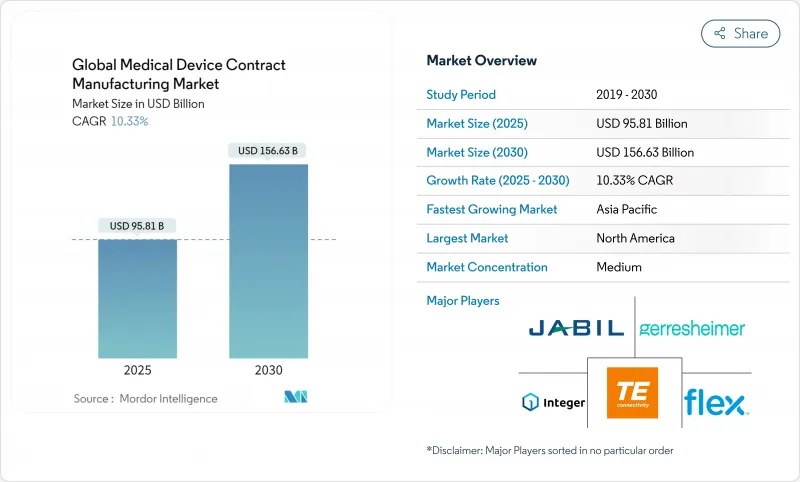

세계의 의료기기 위탁 생산 시장의 규모는 2025년에 958억 1,000만 달러, 2030년에는 1,566억 3,000만 달러에 이를 것으로 예측되며, 기간 중 CAGR은 10.33%로 예상됩니다.

급성장의 배경으로는 OEM이 비용 압력을 처리하기 위해 아웃소싱을 가속화하고 COVID 후 엄격한 규제를 극복하고 고급 디지털 생산을 채택하는 추세를 들 수 있습니다. 커넥티드 약물전달과 클래스 III 생명유지장치 등 일렉트로닉스와 소프트웨어를 통합한 고가치치료는 계속 전문 CMO로 이행하고 있습니다. 투자자들은 밸류체인의 더 많은 부분을 얻기 위해 특히 정밀 공학, 멸균, 포장 등 수직 통합을 지지합니다. 한편, 니어 쇼어링 전략, 스마트 팩토리 투자 확대, 고령화 사회의 지속적인 수요는 북미, 유럽, 아시아태평양의 선진 허브에서 총체적으로 대규모 생산 능력 요건을 창출하고 있습니다.

세계의 의료기기 위탁 생산 시장의 동향과 인사이트

비용 압력에 밀린 OEM 아웃소싱

OEM이 전략적 아웃소싱을 강화하는 주된 이유는 비용 억제, 제품화 가속화, 전문 기술에 대한 액세스 강화 때문입니다. 경영진의 42%는 CMO로의 생산 이관의 주요 계기로 비용 최적화를 꼽았습니다. 다년간의 파트너십을 통해 설계, 승인, 시판 후 서비스를 번들로 제공하고 있으며, OEM은 자본 지출을 억제할 수 있는 반면 CMO는 예측 가능한 수익원을 확보할 수 있습니다. 규모가 큰 기업은 보다 크고 복잡한 프로그램을 흡수하기 위해 클린룸, 부가제조 및 대량 자동화에 대한 투자를 계속하고 있습니다. 그 결과, 의료기기 위탁 생산 시장은 거래 공급에서 통합 라이프사이클 관리로 꾸준히 전환하고 있습니다.

COVID 후 IVD 및 POC 진단 급증

POC의 지속적인 보급으로 IVD의 수량은 팬데믹의 피크를 훨씬 넘어 계속 증가하고 있습니다. 진단제 개발자들은 현재 전자기기의 소형화와 안전한 펌웨어 업그레이드를 요구하는 커넥티비티와 AI 분석을 통합하고 있으며, OEM은 강력한 전기기계와 소프트웨어 검증 기술을 갖춘 CMO로 향하고 있습니다. 진단 장비 아웃소싱의 하위 부문은 퀄리티 바이 디자인과 신속한 프로토타이핑에 의해 개발 사이클이 단축되어 CAGR 9.8%로 확대되고 있습니다. 2025년에 도입된 데이터 표준의 조화로 인해 심사 기간이 더욱 단축되므로 견고한 QMS와 여러 지역의 규제에 대한 인사이트를 결합한 공급업체가 유리합니다.

OEM 통합이 CMO 마진을 압박

M&A에 의해 강화된 대규모 다국적 장치 제조업체는 더 큰 구매 레버리지를 행사하고 공급업체 등록을 정기적으로 최적화합니다. 그 결과 수량이 집중되고 적극적인 가격 협상이 이루어지며 CMO는 운영 능력과 서비스의 차별화를 통해 수익성을 지켜야 합니다. 공급업체 중에는 2014년부터 2020년 중반까지 84건의 합병을 성립시켜 통합 바이어에게 어필할 수 있는 폭넓은 포트폴리오를 가지는 지역 선도기업으로 대응하고 있는 곳도 있습니다. 그러나 주요 10개사의 CMO는 여전히 의료기기 위탁 생산 시장의 24.9%를 차지하는 것에 불과하고, 틈새 전문가가 활약할 여지가 남아 있습니다.

부문 분석

체외 진단용 의약품은 2025년 매출의 28.2%를 차지할 전망으로 의료기기 위탁 생산 시장의 최대 슬라이스로서의 지위를 굳히고 있습니다. 위탁 생산업체는 분자진단, 면역 측정, 중앙 집중식 실험실에서 포인트 오브 케어로 전환한 휴대용 분석 장비에 대한 지속적인 수요를 지원합니다. 고처리량 시약 충전, 정밀 플라스틱 성형, 카트리지 조립 라인은 완전 자동화된 품질 게이트 아래에서 작동하여 높은 납품 목표를 달성합니다.

약물전달 플랫폼은 규모가 작지만 2030년까지 연평균 복합 성장률(CAGR) 12.4%로 가장 급속히 확대될 전망입니다. 센서, 무선 모듈, 사용자 피드백 루프가 내장된 온바디 펌프, 웨어러블 인젝터, 커넥티드 인할러는 다양한 분야에 걸쳐 통합이 필요합니다. CMO는 무균 충전 마감 장비, 실리콘 프리 시린지 코팅, 의료 등급 표준을 준수하는 확장 가능한 전자 장비 조립을 구축하여 대응합니다. 2mL 이상의 생물학적 제형에서 차세대 가스식 자동 주사기가 새로운 모드의 잠재력을 열어줍니다. 재사용 가능한 케이싱과 모듈식 약제 카세트는 폐기물을 줄이고 지속가능성 의무화를 강화하며 의료기기 위탁 생산 업계 전체의 양적 성장을 지원합니다.

지역 분석

북미는 2025년에 39.1%의 점유율로 선두를 유지할 전망이며 왕성한 연구개발 자금, 탄탄한 임상 네트워크, 디지털 수술과 커넥티드 세라퓨틱스의 조기 도입에 의해 뒷받침됩니다. 미국 CMO는 인더스트리 4.0 파일럿 플랜트를 완전한 네트워킹 공장으로 확대하고 AI 예측 유지보수와 종이없는 배치 기록을 도입하여 2033년까지 예상되는 380만 명의 노동력 격차를 완화할 것으로 예상됩니다. 멕시코는 니어쇼어 거점으로서 지역공급망을 강화하고 USMCA에 의한 관세의 명확화와 주요 유통 거점으로의 당일 트럭 운송을 활용합니다.

아시아태평양은 중국과 인도 정부가 하이테크 제조업에 적극적이므로 CAGR 10.5%로 상승하여 가장 빠른 성장 궤도를 보일 전망입니다. 중국의 의료기술 기업은 최대 38억 유로(43억 달러) 상당의 국가 지원을 받아 현지 CMO가 고급 카테터, 내시경, 임플란트 조립품으로 경쟁할 수 있게 되었습니다. 일본 공급업체는 이미징 광학 및 소형 모터 분야에서 전문적인 틈새 시장을 유지하고 있으며, 한국 기업은 MEMS 센서 및 웨어러블 치료제의 배터리 관리에 주력하고 있습니다. 급성장하는 인재 풀과 비용 우위성으로 구미 OEM 기업은 혁신 센터의 병설을 유치하고 의료기기 위탁 생산 시장은 지역 전체로 확대되고 있습니다.

독일, 스위스, 아일랜드는 마이크로 머시닝, 콤비네이션 제품 살균, 고품질 폴리머 성형에 뛰어나며 유럽은 정밀 공학을 계속 이끌고 있습니다. 엄격한 MDR 규칙이 인증을 장기화하고 있기 때문에 미국의 신흥 기업의 대부분은 우선 미국내에서 시작해, 설계가 확정되면 유럽의 공장으로 재이전하는 전략을 취하고 있습니다. 동유럽 국가는 경쟁력있는 노동력과 EU 수준의 품질을 제공하는 중량 일회용 제품의 견인 역할을 합니다. 중동 및 아프리카에서는 확대되는 현지 건강 관리 수요에 대응하기 위해 일회용 장비 생산을 점차 확대하고 있으며 브라질과 코스타리카가 중남미 시장의 성장을 견인합니다. 팬데믹 시대의 공급 충격으로 단일 사업장의 취약성이 부각된 후 다지역 분산은 핵심 탄력 전략이 되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- OEM 아웃소싱에 의한 비용 압력

- COVID 후의 IVD 및 PoC 진단제의 급증

- 복잡한 클래스 III 디바이스 파이프라인의 확대

- 고령화에 의한 기기 대수 증가

- 관세와 지정학적 리스크를 상쇄하는 니어쇼어링

- CMO에 의한 스마트 팩토리/인더스트리 4.0의 채용

- 시장 성장 억제요인

- OEM 통합에 의한 CMO 마진의 압박

- 세계 규제 경로의 차이

- 숙련된 의료기술 제조인력 부족

- 특수 수지와 칩 공급의 불안정성

- 밸류체인 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 디바이스별

- 체외 진단(IVD) 기기

- 화상 진단 기기

- 심혈관 디바이스

- 약물전달 기기

- 주사기

- 펜형 주사기

- 기타

- 내시경 기기

- 안과용 기기

- 정형외과용 기기

- 치과용 기기

- 기타 기기

- 서비스별

- 디바이스 개발 및 제조 서비스

- 디바이스 엔지니어링

- 프로세스 개발

- 디바이스 제조

- 품질 관리 서비스

- 검사 및 시험

- 포장 검증

- 조립 및 완성품 서비스

- 디바이스 개발 및 제조 서비스

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Jabil Inc.

- Flex Ltd.

- Integer Holdings Corp.

- Gerresheimer AG

- TE Connectivity Ltd.

- Nordson Corporation

- Celestica Inc.

- Synecco

- Teleflex Incorporated

- Sanmina Corporation

- Phillips-Medisize(Molex)

- Viant Medical

- Nissha Medical Technologies

- Heraeus Medical Components

- SteriPack Group

- Biomerics

- Nortech Systems Inc.

제7장 시장 기회와 전망

CSM 25.11.03The global medical device contract manufacturing market size stands at USD 95.81 billion in 2025 and is projected to reach USD 156.63 billion by 2030, reflecting a 10.33% CAGR across the period.

Rapid expansion is underpinned by OEMs accelerating outsourcing to manage cost pressure, navigating stringent post-COVID regulations, and adopting advanced digital production. High-value therapies that integrate electronics and software, such as connected drug-delivery and Class III life-support devices, continue to migrate toward specialist CMOs. Investors are backing vertical integration plays, especially in precision engineering, sterilization, and packaging, to capture more of the value chain. Meanwhile, near-shoring strategies, expansion of smart-factory investments, and sustained demand from an aging population collectively create sizable capacity requirements in North America, Europe, and advanced Asia Pacific hubs.

Global Medical Device Contract Manufacturing Market Trends and Insights

Cost-Pressure-Driven OEM Outsourcing

OEMs cite cost containment, faster commercialization, and access to specialist skills as prime reasons to deepen strategic outsourcing. Forty-two percent of senior executives name cost optimization as the leading trigger for shifting volume to CMOs. Multi-year partnerships increasingly bundle design, regulatory, and post-market services, enabling OEMs to limit capital spend while CMOs secure predictable revenue streams. Scale players continue to invest in cleanrooms, additive manufacturing, and high-volume automation to absorb larger, more complex programs. As a result, the medical device contract manufacturing market is steadily moving from transactional supply toward integrated lifecycle management.

Post-COVID Surge in IVD & PoC Diagnostics

Sustained adoption of point-of-care testing keeps IVD volumes elevated well beyond the pandemic peak. Diagnostics developers now embed connectivity and AI analytics that demand electronics miniaturization and secure firmware upgrades, pushing OEMs toward CMOs with strong electromechanical and software validation skills. The diagnostic device outsourcing sub-segment is expanding to a 9.8% CAGR, with quality-by-design and rapid prototyping reducing development cycles. Harmonized data standards introduced in 2025 further compress review timelines, favoring suppliers that pair robust QMS with multi-regional regulatory insight.

OEM Consolidation Squeezing CMO Margins

Large device multinationals, fortified by M&A, wield greater purchasing leverage and regularly optimize supplier rosters. The resulting volume concentration triggers aggressive price negotiations, pressing CMOs to defend profitability via operational excellence and service differentiation. Some suppliers respond by merging 84 deals closed between 2014 and mid-2020, creating regional champions with broader portfolios that appeal to consolidated buyers. Yet the top 10 CMOs still account for only 24.9% of the medical device contract manufacturing market, leaving room for niche specialists to flourish.

Other drivers and restraints analyzed in the detailed report include:

- Complex Class III Device Pipeline Expansion

- Aging Population Amplifying Device Volumes

- Divergent Global Regulatory Pathways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

IVD devices generate 28.2% of 2025 revenue, cementing their status as the largest slice of the medical device contract manufacturing market. Contract manufacturers support sustained demand for molecular diagnostics, immunoassays, and portable analyzers that migrated from centralized labs to point-of-care settings. High-throughput reagent filling, precision plastic molding, and cartridge assembly lines operate under fully automated quality gates to meet tight turnaround targets.

Drug-delivery platforms, while smaller, post the fastest expansion at 12.4% CAGR through 2030. On-body pumps, wearable injectors, and connected inhalers that incorporate sensors, wireless modules, and user-feedback loops require multidisciplinary integration. CMOs respond by building sterile fill-finish suites, silicone-free syringe coating, and scalable electronics assembly under medical-grade standards. For biologics exceeding 2 mL, next-generation gas-powered autoinjectors open new modal possibilities. Reusable casings and modular drug cassettes lower waste, reinforcing sustainability mandates and underpinning volume growth across the medical device contract manufacturing industry.

The Medical Device Contract Manufacturing Market is Segmented by Device (In-Vitro Diagnostic Devices, Drug-Delivery Devices {Syringes, Pen Injectors, and More} and More), Service (Device Development & Manufacturing Services {Device Engineering, and More}, Quality Management Services, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retains leadership with a 39.1% share in 2025, supported by robust R&D funding, deep clinical networks, and early adoption of digital surgery and connected therapeutics. CMOs in the United States scale Industry 4.0 pilots into fully networked plants, deploying AI predictive maintenance and paperless batch records to mitigate a projected 3.8-million-person labor gap by 2033. Mexico strengthens the regional supply chain as a near-shore base, leveraging USMCA tariff clarity and same-day trucking to major distribution hubs.

Asia Pacific records the fastest trajectory, rising at a 10.5% CAGR as Chinese and Indian governments court high-tech manufacturing. Chinese MedTech firms enjoy state support worth up to EUR 3.8 billion (USD 4.3 billion), enabling local CMOs to compete on sophisticated catheter, endoscope, and implant assemblies. Japanese suppliers retain specialist niches in imaging optics and miniaturized motors, while South Korean players focus on MEMS sensors and battery management for wearable therapeutics. A burgeoning talent pool and cost advantage entice Western OEMs to co-locate innovation centers, expanding the medical device contract manufacturing market across the region.

Europe continues to anchor precision engineering, with Germany, Switzerland, and Ireland excelling in micro-machining, combination-product sterilization, and high-grade polymer molding. Stringent MDR rules lengthen certification timelines, prompting many US startups to initially launch stateside before back-transferring to European plants once design is frozen. Eastern European economies gain traction for mid-volume disposables, offering competitive labor yet EU-aligned quality. The Middle East and Africa gradually scale single-use device production to serve expanding local healthcare demand, while Brazil and Costa Rica drive Latin American growth. Multi-regional diversification remains a core resilience strategy after pandemic-era supply shocks highlighted single-site vulnerabilities.

List of Companies Covered in this Report:

- Jabil

- Flex

- Integer Holdings Corp.

- Gerresheimer

- TE Connectivity Ltd.

- Nordson

- Celestica

- Synecco

- Teleflex

- Sanmina Corporation

- Phillips-Medisize (Molex)

- Viant Medical

- Nissha Medical Technologies

- Heraeus Medical Components

- SteriPack Group

- Biomerics

- Nortech Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-Pressure?Driven OEM Outsourcing

- 4.2.2 Post-COVID Surge in IVD & PoC Diagnostics

- 4.2.3 Complex Class III Device Pipeline Expansion

- 4.2.4 Aging Population Amplifying Device Volumes

- 4.2.5 Near-Shoring to Offset Tariff & Geopolitical Risks

- 4.2.6 Smart-Factory/Industry 4.0 Adoption by CMOs

- 4.3 Market Restraints

- 4.3.1 OEM Consolidation Squeezing CMO Margins

- 4.3.2 Divergent Global Regulatory Pathways

- 4.3.3 Shortage Of Skilled Medtech Manufacturing Talent

- 4.3.4 Specialty Resin & Chip Supply Volatility

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Device

- 5.1.1 In-vitro Diagnostic (IVD) Devices

- 5.1.2 Diagnostic Imaging Devices

- 5.1.3 Cardiovascular Devices

- 5.1.4 Drug-Delivery Devices

- 5.1.4.1 Syringes

- 5.1.4.2 Pen Injectors

- 5.1.4.3 Others

- 5.1.5 Endoscopy Devices

- 5.1.6 Ophthalmology Devices

- 5.1.7 Orthopedic Devices

- 5.1.8 Dental Devices

- 5.1.9 Other Devices

- 5.2 By Service

- 5.2.1 Device Development & Manufacturing Services

- 5.2.1.1 Device Engineering

- 5.2.1.2 Process Development

- 5.2.1.3 Device Manufacturing

- 5.2.2 Quality Management Services

- 5.2.2.1 Inspection & Testing

- 5.2.2.2 Packaging Validation

- 5.2.3 Assembly & Finished-Goods Services

- 5.2.1 Device Development & Manufacturing Services

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Jabil Inc.

- 6.3.2 Flex Ltd.

- 6.3.3 Integer Holdings Corp.

- 6.3.4 Gerresheimer AG

- 6.3.5 TE Connectivity Ltd.

- 6.3.6 Nordson Corporation

- 6.3.7 Celestica Inc.

- 6.3.8 Synecco

- 6.3.9 Teleflex Incorporated

- 6.3.10 Sanmina Corporation

- 6.3.11 Phillips-Medisize (Molex)

- 6.3.12 Viant Medical

- 6.3.13 Nissha Medical Technologies

- 6.3.14 Heraeus Medical Components

- 6.3.15 SteriPack Group

- 6.3.16 Biomerics

- 6.3.17 Nortech Systems Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment