|

시장보고서

상품코드

1842620

종양 정보 시스템 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Oncology Information System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

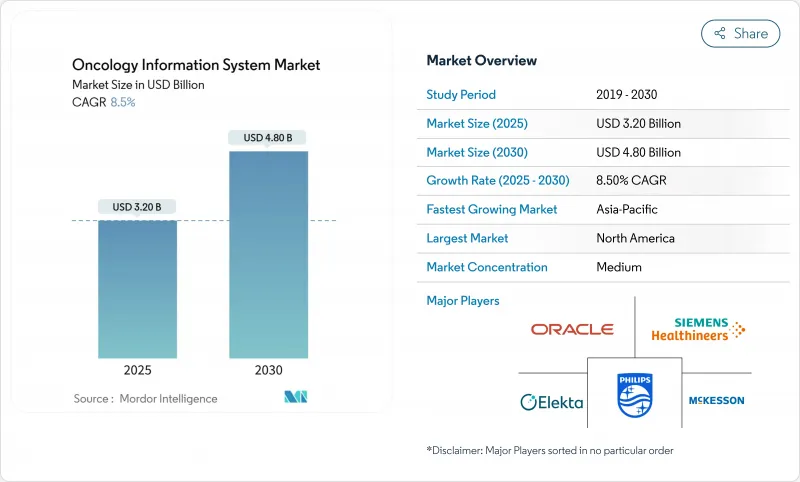

종양 정보 시스템 시장 규모는 2025년에 32억 2,000만 달러, 2030년에는 48억 5,000만 달러에 이를 것으로 예상되며, CAGR은 8.50%를 나타낼 전망입니다.

시장의 현재의 기세는 세계적인 암 이환율의 급상승, 21세기 치료법 등의 상호운용성의 의무화, 임상 워크플로우에의 인공지능의 급속한 통합에 의해 지지되고 있습니다. 치료 제공업체는 데이터 중심의 의사 결정 지원을 통해 복잡한 여러 치료 계획을 관리하고 비용을 줄이고 결과를 개선하기 위해 정교한 플랫폼을 도입했습니다. 병원은 전사적 배포를 가능하게 하는 규모의 이점을 통해 혜택을 받으며, 종양 클리닉은 가치 기반 상환 요건을 충족하기 위해 클라우드 호스팅 서비스를 활용합니다. 종양 정보 시스템 시장은 대규모 설비투자(2024-2025년 인수액은 40억 달러 이상)와 내장해성과 컴플라이언스가 뛰어난 아키텍처의 필요성을 강조하는 사이버 보안 위협 증가에 의해 더욱 형성되고 있습니다.

세계의 종양 정보 시스템 시장 동향과 인사이트

세계적인 암 이환율 상승

세계의 암 이환율은 계속 상승하고 있으며, 미국만으로도 매년 170만명이 새롭게 암으로 진단되어 데이터 관리와 케어 코디네이션에 전례없는 수요가 발생하고 있습니다. 현재 종양학 워크플로우에는 유전체 시퀀싱, 멀티모달 이미징, 실세계 증거가 포함되어 있으며, 이들 모두에 맞춤형 의료를 지원할 수 있는 통합 플랫폼이 필요합니다. 생존율이 30년간 33% 향상됨으로써 장기적인 모니터링이 필요한 암 생존자의 코호트가 증가하고 정보 인프라가 더욱 확장되고 있습니다. 고령화 사회로의 인구통계학적 변화는 이러한 압력을 증폭시키고 건강 관리 조직이 집학 팀과 평생에 걸친 케어 경로를 지원하는 종양 정보 시스템 시장의 전개 규모를 확대하도록 촉구하고 있습니다.

종양 IT 현대화를 위한 정부 자금 지원

공공 부문의 투자는 첨단 암 정보학의 도입을 가속화하고 있습니다. 미국 암 문샷에서는 전자 의료 기록 전체에서 표준화된 종양학 데이터 요소에 적격한 자금이 할당되어 CDC의 AIMS 플랫폼과 NOAH 허브는 주암 등록에 실시간 병리검사 분석을 가져왔습니다. 뉴욕주는 병원 근대화에 1억 8,800만 달러를 기여해 통합암 프로그램을 우선시했습니다. 영국에서는 Cancer 360 기술에 20억 파운드를 확보하고 NHS 기관 전체에서 통일된 종양 정보 레이어를 구축하고 있습니다. 이러한 이니셔티브는 상호 운용성 규칙을 강화하고 민간 투자를 자극하며 종양 정보 시스템 시장의 성장을 강화합니다.

높은 총 소유 비용과 도입 비용

지역 종양 클리닉은 자본 지출과 장기적인 절약을 비교 검토해야합니다. 메이요 클리닉의 자동 선량 반올림 연구는 3년 동안 3,975만 달러를 절약할 가능성을 보여주었지만, 기술, 교육 및 시스템 유지보수를 위해 많은 투자를 필요로 했습니다. 종양 강화 모델에서는 소규모 클리닉에 부담을 주는 보고 의무와 케어 관리 의무가 추가됩니다. 비용 효과적인 프레임워크는 안전성 향상, 부작용 감소, 직원 생산성 향상 등 금전 이외의 이익을 강조합니다.

부문 분석

병원 및 클리닉이 워크플로우 매핑, 시스템 구성, 교육, 지속적인 지원을 도입 파트너에 의존하기 때문에 2024년 종양 정보 시스템 시장 점유율은 서비스가 51.01%를 차지했습니다. 카디널 헬스가 Integrated Oncology Network를 11억 달러로 인수한 것은 번들된 전문 서비스가 기업 고객의 도입과 정착성을 높이는 방법을 보여줍니다. 서비스 종양 정보 시스템 시장 규모는 맞춤형 통합을 필요로 하는 양성자 치료 및 CAR-T 모니터링의 전개가 확대됨에 따라 연동하여 확대될 것으로 예측됩니다.

소프트웨어는 가장 빠르게 성장하는 구성 요소이며 2030년까지 연평균 복합 성장률(CAGR)은 8.98%를 나타낼 전망입니다. GE Healthcare의 CareIntellect for Oncology는 치료 내역과 의사결정 지원을 단일 대시보드에 통합하여 데이터 수집 시간을 몇 시간에서 몇 분으로 단축합니다. RaySearch Laboratories는 계획 품질 분석을 RayCare에 통합하여 AI를 활용한 자동화로 공급업체가 어떻게 차별화하는지 보여줍니다. 공급자가 FHIR 업그레이드, 클라우드 마이그레이션, 사이버 보안 강화 등을 아웃소싱함으로써 컨설팅, 유지보수, 관리 서비스의 하위 부문이 증가. 그 결과, 소프트웨어 라이선싱과 경상 서비스가 종양 정보 시스템 시장 전체에서 예측 가능한 현금 흐름을 생성하는 혼합 수익 모델이 되었습니다.

종양 정보 시스템 시장 보고서는 제품 및 서비스(소프트웨어 및 서비스), 용도(종양학 의료, 방사선 종양학, 외과 종양학), 최종 사용자(병원, 연구센터, 전문 클리닉), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)으로 구분됩니다. 시장 세분화는 위 부문의 금액(달러)을 제공합니다.

지역별 분석

북미는 2024년에 종양 정보 시스템 시장 점유율의 45.23%를 차지하며 Cures Act에 의한 상호운용성의 의무화, 견고한 상환 메커니즘, 확립된 전자 의료 기록의 보급에 지지되었습니다. CDC의 데이터 현대화 이니셔티브와 같은 연방 프로그램은 실시간암 감시를 가속화하고 공급자를 클라우드 우선 아키텍처로 향하게 합니다. 학술센터는 기술기업과 제휴하여 AI 솔루션을 개척하여 이 지역의 리더로서의 자세를 강화하고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있으며 2030년까지 연평균 복합 성장률(CAGR)은 9.85%를 나타낼 전망입니다. 중국의 트리니티 스마트 호스피탈 청사진은 통합 EMR과 스마트 서비스의 표준을 개설하여 지역 의료 시스템을 레거시 아키텍처에서 도약시킵니다. 한국의 K-CURE Public Cancer Library는 226만 명의 환자의 익명화된 기록을 집계하고 2,500만 달러의 정부기금이 AI 주도의 신약 개발을 지원합니다. 일본의 의료 DX 프로그램은 환자 데이터를 중앙 집중화하는 국가 정보 플랫폼을 구축하고, 인도의 모든 인도 의학 연구소는 유방암과 난소암을 조기에 발견하기 위해 AI 이미지 분석을 도입하고 있습니다. 이러한 협조적인 노력은 표준을 강화하고 조달을 용이하게 하며 종양 정보 시스템 시장 전체 수요를 환기시킵니다.

유럽에서는 이미지 데이터와 AI 툴의 검증을 위한 협력 네트워크를 구축하는 European Cancer Imaging Initiative 및 JANE 프로젝트와 같은 범지역적 이니셔티브가 이에 이어집니다. 회원국은 클라우드 기반 등록 및 점유율 분석에 공동 투자하고 공급업체에게 FHIR 대응 및 GDPR(EU 개인정보보호규정) 준수 인증을 촉구합니다. 중동 및 아프리카와 라틴아메리카는 원격 종양학, 원격 모니터링 및 기본 EMR 업그레이드를 완전한 종양 정보 시스템 시장 개발을 위한 기본 단계로 번들하는 관민 파트너십을 통해 종종 단계적 도입을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계의 암 이환율의 상승

- 종양 IT 근대화를 위한 정부 자금 지원

- 상호 운용성의 의무화(21세기 치료법 등)

- 복수 시설의 암 네트워크에 있어서 클라우드 호스트형 OIS의 채용

- ROI를 높이는 AI 주도의 임상 판단 지원

- 실시간 결과 추적을 요구하는 가치 기반 상환 모델

- 시장 성장 억제요인

- 높은 총소유비용과 도입비용

- 종양정보학 전문가 부족

- 사이버 보안 및 환자 데이터 프라이버시 위험

- 새로운 양성자료 치료 데이터 포맷과의 통합 갭

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 종양

- 소프트웨어

- 환자 정보 시스템

- 치료 계획 시스템

- 서비스

- 컨설팅

- 구현 및 통합

- 유지보수 및 지원

- 소프트웨어

- 용도별

- 내과 종양학

- 방사선 종양학

- 외과 종양학

- 최종 사용자별

- 병원

- 종양 클리닉

- 연구 및 학술 센터

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동

- GCC

- 남아프리카

- 기타 중동

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Oracle Health(Cerner)

- Siemens Healthineers(Varian)

- Elekta AB

- McKesson Corporation

- Koninklijke Philips NV

- F. Hoffmann-La Roche(Flatiron Health)

- Accuray Incorporated

- RaySearch Laboratories

- Optum Inc.

- Epic Systems Corporation

- GE HealthCare

- Tempus Labs Inc.

- ViewRay Inc.

- Merative(IBM Watson Health)

- Medisolv Inc.

- IntelliCyt Corporation

- CEDAR Oncology Solutions

- Carevive Systems

- EndoSoft LLC

- MIM Software Inc.

- Flatiron OncoEMR(Altos)

제7장 시장 기회와 전망

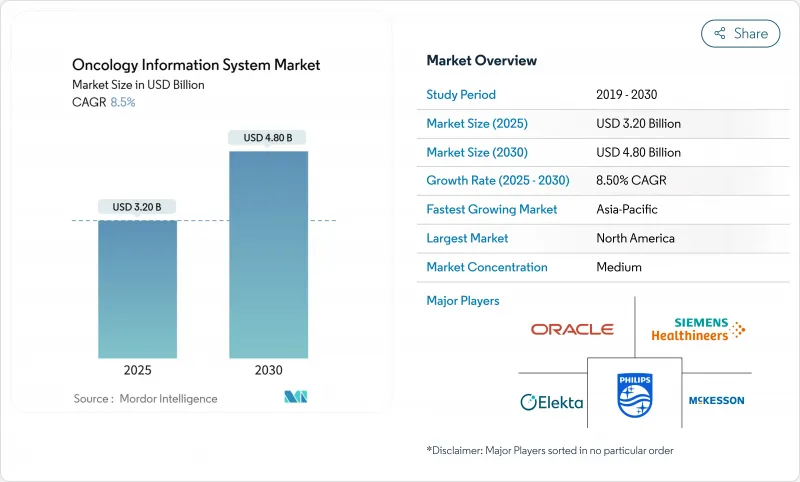

KTH 25.11.05The oncology information system market size stands at USD 3.22 billion in 2025 and is forecast to reach USD 4.85 billion by 2030, advancing at an 8.50% CAGR.

The market's current momentum is underpinned by the sharp rise in global cancer incidence, interoperability mandates such as the 21st Century Cures Act, and rapid integration of artificial intelligence into clinical workflows. Providers are deploying sophisticated platforms to manage complex, multimodality treatment plans, reduce costs, and improve outcomes through data-driven decision support. Hospitals benefit from economies of scale that enable enterprise-wide rollouts, while oncology clinics leverage cloud-hosted offerings to meet value-based reimbursement requirements. The oncology information system market is further shaped by large capital investments-more than USD 4 billion in acquisitions in 2024-2025-and by escalating cybersecurity threats that underscore the need for resilient, compliant architectures.

Global Oncology Information System Market Trends and Insights

Rising Incidence of Cancer Worldwide

Global cancer burden continues to climb, with 1.7 million new cases diagnosed each year in the United States alone, placing unprecedented demands on data management and care coordination . Oncology workflows now incorporate genomic sequencing, multi-modal imaging, and real-world evidence, all of which require an integrated platform capable of supporting personalized medicine. Improved survival rates-up 33% over three decades-have created a growing cohort of cancer survivors who need long-term monitoring, further stretching information infrastructure . Demographic shifts toward aging populations amplify these pressures, pushing healthcare organizations to scale oncology information system market deployments that support multidisciplinary teams and lifelong care pathways.

Government Funding for Oncology IT Modernization

Public-sector investment is accelerating adoption of advanced cancer informatics. The United States Cancer Moonshot allocates targeted funds for standardized oncology data elements across electronic health records, while the CDC's AIMS platform and NOAH hub bring real-time pathology and laboratory analytics to state cancer registries. New York State committed USD 188 million to hospital modernization, prioritizing integrated cancer programs. The United Kingdom set aside GBP 2 billion for Cancer 360 technology, creating unified oncology information layers across NHS institutions . Such initiatives tighten interoperability rules and stimulate private investment, reinforcing growth in the oncology information system market.

High Total Cost of Ownership & Implementation

Community oncology practices must weigh capital outlays against long-term savings. Mayo Clinic's automated dose rounding study showed potential savings of USD 39.75 million over three years yet required sizable upfront investment for technology, training, and system maintenance. The Enhancing Oncology Model adds reporting and care-management obligations that strain smaller clinics. Cost-benefit frameworks underline non-financial gains-improved safety, fewer adverse events, and higher staff productivity-yet the cash flow challenge remains acute until reimbursement adjusts.

Other drivers and restraints analyzed in the detailed report include:

- Interoperability Mandates (21st Century Cures Act)

- AI-Driven Clinical Decision Support Boosting ROI

- Shortage of Oncology-Informatics Professionals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services held 51.01% of oncology information system market share in 2024 as hospitals and clinics relied on implementation partners for workflow mapping, system configuration, training, and ongoing support. Cardinal Health's USD 1.1 billion purchase of Integrated Oncology Network illustrates how bundled professional services amplify adoption and stickiness for enterprise clients. The oncology information system market size for services is projected to expand in tandem with growing proton-therapy and CAR-T monitoring deployments that demand bespoke integrations.

Software is the fastest-growing component, tracking an 8.98% CAGR through 2030. GE HealthCare's CareIntellect for Oncology consolidates treatment history and decision support into a single dashboard, cutting data-gathering time from hours to minutes. RaySearch Laboratories integrates plan-quality analytics into RayCare, showing how vendors differentiate on AI-enabled automation. Consulting, maintenance, and managed-service subsegments rise as providers outsource FHIR upgrades, cloud migrations, and cybersecurity hardening. The result is a blended revenue model in which software licensing and recurring services generate predictable cash flows across the oncology information system market.

The Oncology Information System Market Report is Segmented by Product and Service (Software and Services), Application (Medical Oncology, Radiation Oncology, and Surgical Oncology), End User (Hospitals, Research Centers, and Specialty Clinics), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Provides the Value (USD) for the Abovementioned Segments.

Geography Analysis

North America accounted for 45.23% of oncology information system market share in 2024, supported by the Cures Act interoperability mandate, robust reimbursement mechanisms, and well-established electronic health record penetration. Federal programs such as the CDC's data-modernization initiative accelerate real-time cancer surveillance, nudging providers toward cloud-first architectures. Academic centers partner with technology firms to pioneer AI solutions, reinforcing the region's leadership stance.

Asia-Pacific is the fastest-growing region, projecting a 9.85% CAGR through 2030. China's Trinity smart-hospital blueprint outlines standards for unified EMRs and smart services, positioning local health systems to leapfrog legacy architectures . South Korea's K-CURE Public Cancer Library aggregates anonymized records for 2.26 million patients, while a USD 25 million government fund backs AI-driven drug discovery. Japan's medical DX program builds a national information platform to unify patient data, and India's All India Institute of Medical Sciences deploys AI image analytics to detect breast and ovarian cancers earlier. These coordinated efforts tighten standards, ease procurement, and seed demand across the oncology information system market.

Europe follows with pan-regional initiatives such as the European Cancer Imaging Initiative and JANE project, which create federated networks for imaging data and AI tool validation. Member states co-invest in cloud-based registries and shared analytics, encouraging vendors to certify FHIR readiness and GDPR compliance. Middle East & Africa and Latin America show incremental adoption, often through public-private partnerships that bundle tele-oncology, remote monitoring, and basic EMR upgrades as foundational steps toward a full oncology information system market rollout.

- Oracle Health (Cerner)

- Siemens Healthineers (Varian)

- Elekta

- Mckesson

- Koninklijke Philips

- F. Hoffmann-La Roche (Flatiron Health)

- Accuray

- RaySearch Laboratories

- Optum

- Epic Systems

- GE Healthcare

- Tempus Labs Inc.

- ViewRay Inc.

- Merative (IBM Watson Health)

- Medisolv

- IntelliCyt Corporation

- CEDAR Oncology Solutions

- Carevive Systems

- EndoSoft

- MIM Software

- Flatiron OncoEMR (Altos)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising incidence of cancer worldwide

- 4.2.2 Government funding for oncology IT modernization

- 4.2.3 Interoperability mandates (e.g., 21st Century Cures Act)

- 4.2.4 Cloud-hosted OIS adoption across multi-site cancer networks

- 4.2.5 AI-driven clinical-decision support boosting ROI

- 4.2.6 Value-based reimbursement models demanding real-time outcomes tracking

- 4.3 Market Restraints

- 4.3.1 High total cost of ownership & implementation

- 4.3.2 Shortage of oncology-informatics professionals

- 4.3.3 Cyber-security & patient-data-privacy risks

- 4.3.4 Integration gaps with emerging proton-therapy data formats

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 Oncology

- 5.1.1 Software

- 5.1.1.1 Patient-information systems

- 5.1.1.2 Treatment-planning systems

- 5.1.2 Services

- 5.1.2.1 Consulting

- 5.1.2.2 Implementation & Integration

- 5.1.2.3 Maintenance & Support

- 5.1.1 Software

- 5.2 By Application

- 5.2.1 Medical Oncology

- 5.2.2 Radiation Oncology

- 5.2.3 Surgical Oncology

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Oncology Clinics

- 5.3.3 Research & Academic Centers

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Oracle Health (Cerner)

- 6.3.2 Siemens Healthineers (Varian)

- 6.3.3 Elekta AB

- 6.3.4 McKesson Corporation

- 6.3.5 Koninklijke Philips N.V.

- 6.3.6 F. Hoffmann-La Roche (Flatiron Health)

- 6.3.7 Accuray Incorporated

- 6.3.8 RaySearch Laboratories

- 6.3.9 Optum Inc.

- 6.3.10 Epic Systems Corporation

- 6.3.11 GE HealthCare

- 6.3.12 Tempus Labs Inc.

- 6.3.13 ViewRay Inc.

- 6.3.14 Merative (IBM Watson Health)

- 6.3.15 Medisolv Inc.

- 6.3.16 IntelliCyt Corporation

- 6.3.17 CEDAR Oncology Solutions

- 6.3.18 Carevive Systems

- 6.3.19 EndoSoft LLC

- 6.3.20 MIM Software Inc.

- 6.3.21 Flatiron OncoEMR (Altos)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment