|

시장보고서

상품코드

1842638

정맥주사용 면역글로불린 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Intravenous Immunoglobulin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

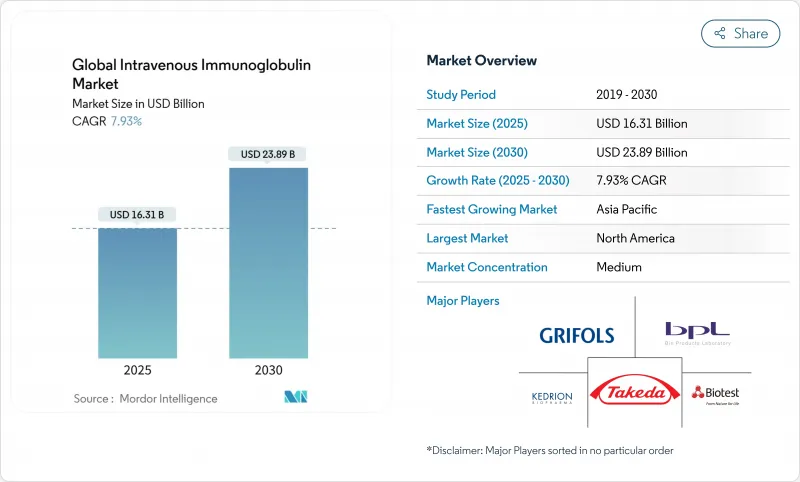

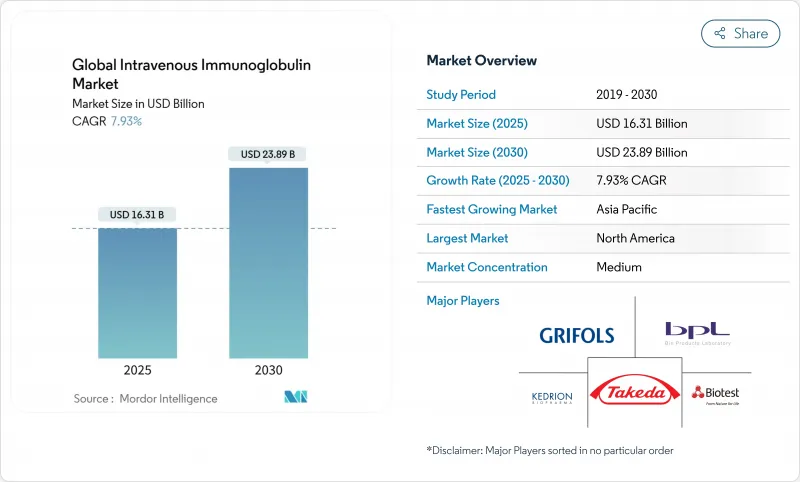

정맥주사용 면역글로불린 시장 규모는 2025년에 163억 1,000만 달러에 이르고, 2030년에는 238억 9,000만 달러에 달할 것으로 예측되며, CAGR은 7.93%를 나타낼 전망입니다.

원발성 면역 결핍증 이외의 임상용도 증가, 인구동태의 고령화, 분획제제 제조업체의 지속적인 설비투자 등이 수요의 펀더멘탈스를 강화하고 있습니다. 북미는 상환경로가 확립되어 1인당 지출액이 높기 때문에 정맥주사용 면역글로불린 시장을 선도하고 있지만 아시아태평양은 급속한 헬스케어 접근성 향상과 정책개혁이 뒷받침하고 있습니다. 만성 염증성 탈수성 다발성 신경병증과 같은 신경학적 적응증의 확대는 정맥주사용 면역글로불린 시장의 기회 전망을 확대하고 있습니다.

세계의 정맥주사용 면역글로불린 시장 동향과 인사이트

노년 인구 증가

노화로 인한 면역력의 감소는 감염 및 자가면역 질환에 대한 감수성을 증가시키고, 정맥주사용 면역글로불린 시장의 장기적인 수요를 지원합니다. 아시아태평양은 그 영향을 가장 강하게 받고 있습니다. 인구의 급속한 고령화는 진단 범위와 보험 적용 범위의 확대로 이어지기 때문입니다. 인구 동향은 또한 암 치료와 관련된 2차적 면역 결핍을 증폭시켜 사용량을 더욱 끌어올리고 있습니다. 일본의 의료기술지출의 궤적은 고령화가 어떻게 특 수요법의 소비를 촉진하는지를 뒷받침하고 있습니다. 이러한 요인들이 결합되어 향후 10년간의 분수기의 수량 파이프라인은 예측 가능할 것입니다.

면역글로불린 요법의 채용 확대

만성 염증성 탈수성 다발 신경염에 대한 다케다 의약품의 껌 마가드 용액과 같은 약사 승인은 보다 광범위한 면역조절의 유용성을 검증하고 임상의에게 받아들여지는 것을 가속화하고 있습니다. 자가면역성 뇌염과 패혈증의 새로운 데이터는 여러 고소득 시장에서 상환이 완화되는 가운데 적응 외 처방을 뒷받침하여 신뢰성을 높이고 있습니다. 증거의 축적은 새로운 환자층의 획득과 투여 기간의 연장을 가능하게 하고, 정맥주사용 면역글로불린 시장 전체의 소비량이 증가합니다.

엄격한 규제 당국의 승인 및 기증자 심사 기준

특히 규제 당국의 감독이 엄격한 유럽 연합(EU)과 미국에서는 공여자 자격에 대한 엄격한 규칙과 철저한 검증 절차로 인해 리드 타임이 길어지고 오버헤드가 증가합니다. 배치 릴리스 요구사항 및 바이러스 안전성 벤치마크는 자본 및 문서화 부담을 부과하여 정맥주사용 면역글로불린 시장에서 신규 진출기업의 진전을 감속시킬 수 있습니다.

부문 분석

2024년, IgG는 정맥주사용 면역글로불린 시장의 74.75%를 차지했고, 이 부문은 2030년까지 연평균 복합 성장률(CAGR) 8.54%를 나타낼 전망입니다. 그리포르스의 정제 공정은 일관되게 98% 이상의 IgG 순도를 실현하여 브랜드 차별화를 강화하고 있습니다. 고강도 제형은 현재 주입 시간을 단축하고 병원 스케줄링 압력을 완화하며 환자의 편안함을 향상시키고 있습니다.

제조업체 각사는 연속 크로마토그래피를 우선하여 수율을 높이고 비용을 낮추어 정맥주사용 면역글로불린 시장 전체의 금리를 더욱 확대하고 있습니다. Yimmugo 및 ALYGLO와 같은 새로운 브랜드의 규제 클리어런스는 경쟁력을 높이는 동시에 더 광범위한 공급 안전을 보장합니다. IgA와 IgM은 점막 장애와 보체 매개 장애에 특화된 틈새 위치를 유지합니다.

지역 분석

북미는 오랜 보험 적용과 광범위한 혈장 채취 인프라로 2024년 정맥주사용 면역글로불린 시장의 42.34%를 유지했습니다. 메디케어 정책은 사용 기준을 제시하고 있으며, 상업 지불자는 이를 거의 그대로 반영하기 때문에 수요가 예측하기 쉽고, 새로운 제형의 채용도 빠릅니다. 전문적인 수액 네트워크와 성숙하고 있는 재택 서비스는 환자의 편의성과 업무 효율을 높입니다.

2030년까지 연평균 복합 성장률(CAGR)은 8.45%를 나타내 아시아태평양이 가장 빠르게 성장하고 있습니다. 중국의 국가 상환 의약품 목록 협상으로 2024년에는 IVIG의 평균 가격이 63% 인하되어 지금까지 손이 닿지 않았던 코호트에도 치료법이 펼쳐졌습니다. 일본의 의료기술평가 개정은 혁신적인 생물제제에 대한 자금제공을 지지하고 인도의 생산연동형 인센티브는 현지 분획능력을 자극하고 이들 모두가 정맥주사용 면역글로불린 시장의 기반을 확대합니다.

유럽은 안정적인 성장을 보이지만 미국 혈장에 대한 공급 의존성은 취약성을 돋보이게 합니다. ESG 주도의 자급자족정책과 집중조달은 도너풀의 다양화와 투명성 향상을 제조업체에 육박합니다. 외래 주입으로의 점진적인 변화는 입원 비용 절감과 정맥주사용 면역글로불린 시장 전체의 품질 기준 유지를 목적으로 합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고령 인구 증가

- 면역글로불린 요법의 채용 증가

- 면역 결핍 및 출혈성 질환의 유병률 상승

- 혈장 분획 기술의 진보

- 아시아에서의 적응외의 신경학적 사용과 상환의 완화

- 지역의 혈장 수집 허브가 공급의 안전성을 촉진

- 시장 성장 억제요인

- 엄격한 규제 당국의 승인과 기증자의 심사 기준

- 높은 치료비와 콜드체인 비용

- 피하 Ig(SCIG)로의 변화에 의한 IVIG량의 감소

- 혈장 조달에 관한 ESG의 조사에 의한 컴플라이언스 비용의 상승

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 진입자의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 면역글로불린 클래스별

- IgG

- IgA

- IgM

- 기타

- 용도별

- 저감마글로불린혈증

- 만성 염증성 탈수초성 다발신경병증(CIDP)

- 원발성 면역결핍증(PID)

- 중증근무력증

- 다발성 운동신경병증

- 기타 용도

- 최종 사용자별

- 병원

- 전문 클리닉 및 신경센터

- 재택치료

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Takeda Pharmaceutical Co.

- CSL Behring

- Grifols SA

- Octapharma AG

- Baxter International Inc.

- Kedrion SpA

- Biotest AG

- Bio Products Laboratory Ltd

- LFB Group

- China Biologic Products Holdings

- Shanghai RAAS Blood Products

- Hualan Biological Engineering

- ADMA Biologics Inc.

- Emergent BioSolutions Inc.

- Kamada Ltd

- GC Pharma

- Intas Pharmaceuticals(Lonza Tie-up)

- BioTest Pharma(US)

- South African National Blood Service

- Sanquin Plasma Products

제7장 시장 기회와 전망

KTH 25.10.29The intravenous immunoglobulin market size reached USD 16.31 billion in 2025 and is forecast to climb to USD 23.89 billion by 2030, translating into a 7.93% CAGR, which keeps the intravenous immunoglobulin market among the most resilient plasma-derived therapeutic spaces.

Rising clinical use beyond primary immunodeficiency, demographic ageing, and sustained capacity investments by fractionators all reinforce demand fundamentals. North America leads the intravenous immunoglobulin market because of well-established reimbursement pathways and high per-capita spending, whereas rapid healthcare access gains and policy reform propel Asia-Pacific. IgG retains dominant status, and expanding neurological indications such as chronic inflammatory demyelinating polyneuropathy broaden the intravenous immunoglobulin market opportunity landscape.

Global Intravenous Immunoglobulin Market Trends and Insights

Rise in Geriatric Population

Age-related immune decline increases susceptibility to infections and autoimmune disorders, which sustains long-term demand within the intravenous immunoglobulin market. Asia-Pacific feels the effect most, as rapid population ageing aligns with broader diagnostic reach and insurance coverage. The demographic trend also amplifies secondary immunodeficiencies linked with cancer therapies, further lifting usage. Japan's medical technology spending trajectory underscores how ageing catalyzes specialty-therapy consumption. Together these factors form a predictable volume pipeline for fractionators over the next decade.

Increased Adoption of Immunoglobulin Therapy

Regulatory approvals such as Takeda's GAMMAGARD LIQUID for chronic inflammatory demyelinating polyneuropathy have validated broader immunomodulatory utility and accelerated clinician acceptance. Emerging data in autoimmune encephalitis and sepsis reinforce confidence, encouraging off-label prescribing as reimbursement loosens in several high-income markets. The evidence base unlocks new patient pools and extends dosing durations, thereby raising overall consumption inside the intravenous immunoglobulin market.

Stringent Regulatory Approval & Donor-Screening Norms

Tight donor eligibility rules and exhaustive validation steps lengthen lead times and add overhead, especially in the European Union and United States, where regulatory scrutiny remains intense. Batch-release requirements and viral safety benchmarks impose capital and documentation burdens that may decelerate new-entrant progress inside the intravenous immunoglobulin market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Prevalence of Immunodeficiency & Bleeding Disorders

- Advancements in Plasma-Fractionation Technology

- High Therapy & Cold-Chain Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

IgG commanded 74.75% of the intravenous immunoglobulin market in 2024, and the segment is growing at an 8.54% CAGR to 2030, which underlines how indispensable IgG remains for both replacement and immunomodulation. Grifols' purification process consistently delivers >=98% IgG purity, strengthening brand differentiation. High-strength formulations now shorten infusion time, easing hospital scheduling pressures and improving patient comfort.

Manufacturers have prioritized continuous chromatography to boost yield and lower cost, which further bolsters margins across the intravenous immunoglobulin market. Regulatory clearances for new brands such as Yimmugo and ALYGLO increase competitive dynamics yet simultaneously assure broader supply security. IgA and IgM retain niche status focused on mucosal and complement-mediated disorders.

The Intravenous Immunoglobulin Market Report Segments the Industry Into by Type (IgG, Iga, Igm, and Others), by Application (Hypogammaglobulinemia, Chronic Inflammatory Demyelinating Polyneuropathy, Primary Immunodeficiency, and More), End User (Hospitals, Specialty Clinics & Neurology Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America kept 42.34% of the intravenous immunoglobulin market in 2024 due to long-standing insurer coverage and extensive plasma collection infrastructure. Medicare policies outline usage criteria that commercial payers largely mirror, facilitating predictable demand and rapid adoption of new formulations. Specialized infusion networks and maturing home-based services advance patient convenience and operational efficiency.

Asia-Pacific is growing fastest at an 8.45% CAGR through 2030. China's National Reimbursement Drug List negotiations produced average IVIG price reductions of 63% in 2024, opening therapy to previously unreachable cohorts. Japan's revised health technology assessments uphold funding for innovative biologics, while India's production-linked incentives stimulate local fractionation capacity, all of which enlarge the intravenous immunoglobulin market base.

Europe shows stable progression, yet supply dependence on United States plasma highlights vulnerability. ESG-driven self-sufficiency policies and centralized procurement place pressure on manufacturers to diversify donor pools and enhance transparency. Gradual shifts toward outpatient infusions aim to reduce hospitalization costs and maintain quality benchmarks across the intravenous immunoglobulin market.

- Takeda Pharmaceutical Co.

- CSL Behring

- Grifols

- Octapharma

- Baxter

- Kedrion Biopharma

- Biotest

- Bio Products Laboratory

- LFB Group

- China Biologic Products Holdings

- Shanghai RAAS Blood Products

- Hualan Biological Engineering

- ADMA Biologics

- Emergent Bio Solutions

- Kamada Ltd

- GC Biopharma

- Intas Pharmaceuticals (Lonza Tie-up)

- BioTest Pharma (US)

- South African National Blood Service

- Sanquin Plasma Products

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Geriatric Population

- 4.2.2 Increased Adoption of Immunoglobulin Therapy

- 4.2.3 Rising Prevalence of Immunodeficiency & Bleeding Disorders

- 4.2.4 Advancements in Plasma-fractionation Technology

- 4.2.5 Off-label Neuro-logical Use & Relaxed Reimbursement in Asia

- 4.2.6 Regional Plasma-collection Hubs Driving Supply Security

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Approval & Donor-screening Norms

- 4.3.2 High Therapy & Cold-chain Costs

- 4.3.3 Shift toward Subcutaneous Ig (SCIG) Reducing IVIG Volumes

- 4.3.4 ESG Scrutiny of Plasma Sourcing Raising Compliance Costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value - USD)

- 5.1 By Immunoglobulin Class

- 5.1.1 IgG

- 5.1.2 IgA

- 5.1.3 IgM

- 5.1.4 Others

- 5.2 By Application

- 5.2.1 Hypogammaglobulinemia

- 5.2.2 Chronic Inflammatory Demyelinating Polyneuropathy (CIDP)

- 5.2.3 Primary Immunodeficiency Diseases (PID)

- 5.2.4 Myasthenia Gravis

- 5.2.5 Multifocal Motor Neuropathy

- 5.2.6 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Specialty Clinics & Neurology Centers

- 5.3.3 Home-Care Settings

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Takeda Pharmaceutical Co.

- 6.3.2 CSL Behring

- 6.3.3 Grifols SA

- 6.3.4 Octapharma AG

- 6.3.5 Baxter International Inc.

- 6.3.6 Kedrion SpA

- 6.3.7 Biotest AG

- 6.3.8 Bio Products Laboratory Ltd

- 6.3.9 LFB Group

- 6.3.10 China Biologic Products Holdings

- 6.3.11 Shanghai RAAS Blood Products

- 6.3.12 Hualan Biological Engineering

- 6.3.13 ADMA Biologics Inc.

- 6.3.14 Emergent BioSolutions Inc.

- 6.3.15 Kamada Ltd

- 6.3.16 GC Pharma

- 6.3.17 Intas Pharmaceuticals (Lonza Tie-up)

- 6.3.18 BioTest Pharma (US)

- 6.3.19 South African National Blood Service

- 6.3.20 Sanquin Plasma Products