|

시장보고서

상품코드

1842651

중국의 차량 렌탈 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)China Vehicle Rental - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

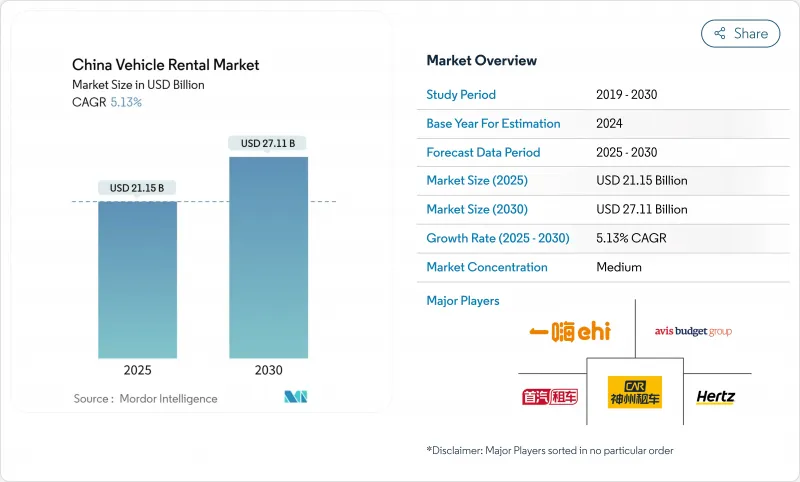

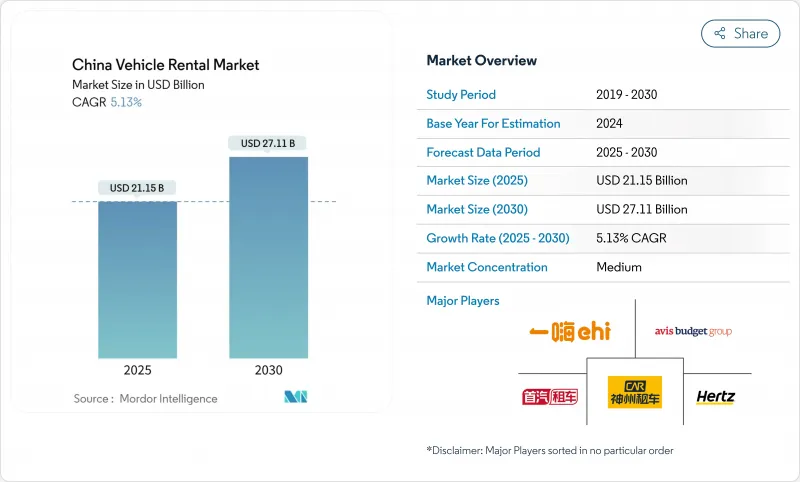

중국의 차량 렌탈 시장 규모는 2025년에 211억 5,000만 달러로 추정되며, 예측 기간(2025-2030년)의 CAGR은 5.13%를 나타내, 2030년에는 271억 1,000만 달러에 달할 것으로 예상됩니다.

국내 레저 여행 회복, 1급 도시에서의 번호판 할당 엄격화, 전국적인 80% 신에너지 차량 의무화 등이 소비자 채널과 기업 채널을 불문하고 수요를 증가시킵니다. Tier-2 및 Tier-3 도시에서 중간층의 면허 취득 운전자 수 증가, 인공지능 대응 예약 앱의 급속한 보급 및 전기 모델에 대한 정책 기울기는 지난 5년간 어느 기간보다 빨리 차량 구성을 재구성했습니다.

중국의 차량 렌탈 시장 동향과 인사이트

국내 관광 회복이 레저 렌탈을 뒷받침

2024년 메이데이 연휴 중 2억 9,500만 명이 국내 여행을 떠나 200억 달러 이상이 소비되었다고 당국이 보고한 뒤 레저 예약이 급증하여 현 수준의 관광지에서 차량 수요가 높아졌습니다. 야나기주와 시박 등의 도시에서는 대중교통보다 자가용 차량으로의 접근을 선호하는 최초의 여행자들이 모여 내륙부의 많은 곳에서 평균 대여 기간이 4일을 넘어섰습니다. Zuzuche는 4개월 이내에 3,000개의 국내 공급업체 파트너를 획득하여 디지털 마켓플레이스 플랫폼의 확장성 이점을 입증했습니다. 문화유산의 야간관광은 늦은 밤까지 높은 이용률을 유지하고, 비싼 가격 설정을 지원했습니다. 문화관광부는 2025년 국내 여행자 수가 60억 명을 넘을 것으로 예측하고 있으며, 레저가 중국의 차량 렌탈 시장의 핵심임을 뒷받침하고 있습니다.

Tier-1 도시의 번호판 할당이 대여 수요에 박차를 가한다.

베이징의 연간 추첨에서는 자가용차의 신규 넘버 플레이트는 10만대가 상한으로, 70%가 EV용으로 되어 있습니다. 이러한 제한으로 인해 많은 통근자에게는 소유하는 것보다 매일 대여하는 것이 더 저렴합니다. 천진시는 연간 8만장의 그린 넘버를 발행할 계획이지만, 화석연료의 제한을 유지하고 비용압력을 유지하고 있습니다. 넘버 플레이트의 할당으로 영향을 받은 도시에서는 연료 소비량과 테일 파이프 배출량이 50% 가까이 삭감되었지만, 동시에 자동차를 자산이 아니라 가끔 유틸리티로 간주하는 렌탈 이용자의 확실한 흐름을 만들어내고 있습니다. 이 정책은 또한 차량을 EV로 치우쳐 정부의 이산화탄소 배출 목표를 강화하고 중국의 차량 렌탈 시장을 재구성하고 있습니다.

라이드 헤일링 및 로봇 택시의 대체 위험

바이두의 Apollo Go는 2023년 4분기에 기존 택시의 60-70% 싼 운임으로 83만 9,000대의 자율주행에 성공하여 파괴적인 가격 격차를 보였습니다. Pony.ai는 2025년까지 1,000대의 차량을 보유하는 것을 목표로 하고 있으며, WeRide는 2025년 2월 베이징 대흥 국제공항을 연결하는 무인 서비스를 시작했습니다. 로봇 택시 사업자는 24시간 365일 이용 가능하고 운전자 관련 경비가 적다는 이점이 있으며, 지금까지 공항 교통이나 도시내의 용사를 위해 차량 렌탈을 선호하고 이용하고 있던 수요를 전환합니다. 컨설턴트 회사의 예측에서 로봇 택시 분야는 2030년까지 약 760억 달러에 달한다고 하고 있으며, 기존 기업이 자율주행 파트너십을 확보할 수 없으면 중국의 차량 렌탈 시장에 경쟁적 역풍이 불고 있음을 보여줍니다.

부문 분석

2024년 중국의 차량 렌탈 시장 점유율은 레저·관광이 51.27%를 차지했으며, 휴가 여행의 7.6% 증가와 현 수준의 문화적 명소에 대한 새로운 관심의 고조에 지지를 받았습니다. 단기간의 드라이브 휴가나 가족 단관에서는 셀프 드라이브 카가 선호되며, 피크 시 평균 이용률은 74%를 나타낼 전망입니다. CAGR 5.22%를 나타낼 것으로 예측되는 업무도항은 국경의 재개나 기업의 ESG 목표가 소유 차량보다 차량 렌탈을 선호하기 때문에 혜택을 받습니다.

레저 손님은 유행 전 평균보다 2.1일 길게 예약하고, 출장객은 보고 작성을 위해 텔레매틱스와 배출 가스 대시보드를 번들 한 운전자와 패키지를 선택하는 경향이 강해지고 있습니다. 관광 명소와의 플랫폼 통합을 통해 한 번의 클릭으로 자동차와 티켓 번들을 가능하게 하여 대여당 수익 창출이 확대되었습니다.

온라인 예약은 2024년에는 수익의 64.38%를 나타냈습니다. 이는 마찰이 없는 모바일 이동이 테이블 스테이크가 된 것을 증명하는 것으로, 2030년까지의 CAGR도 5.41%를 나타낼 전망입니다. 예측 가격 설정 엔진은 검색에서 예약까지의 시간을 평균 4분으로 단축하고 부수적인 업셀을 18% 증가시켜 고객 1인당 평생 가치를 높입니다. 그러나 옴니채널 핸드오버 스테이션에서는 점원이 없어도 QR코드로 키를 꺼낼 수 있어 편리성의 격차가 줄어들고 있습니다.

클라우드 CRM과 자동차 IoT 센서에 대한 투자가 계속되고 있으며, 이용 데이터를 플랫폼에 피드백함으로써 여러 지역에서 재고를 즉시 회전시킬 수 있습니다. 그 결과, 동적 온라인 배차를 이용하는 플릿 오퍼레이터는 정적 오프라인 예약에 의존하는 동업 타사보다 차량 1대당 매출이 12% 높고, 이 차이는 중국의 차량 렌탈 시장에서 확대될 것으로 예측됩니다.

셀프 드라이브 계약은 2024년 총 매출의 71.32%를 차지했으며, 이는 개인 여행을 선호하는 문화적 배경과 운전에 대한 자신감이 높아졌다는 것을 의미합니다. 그러나 기업의 조달 팀은 운전자와 함께 포장하는 것이 안전하고 ESG 감사 추적을 준수한다고보고 있기 때문에 연간 5.45%를 나타낼 전망입니다. 운전자가 장착된 차량은 NEV의 보급률이 60%를 넘어 전체 평균을 넘어 베이징과 심천의 중심 업무지구의 저배출 가스지역에 적합합니다.

자율주행은 가족을 위한 여정, 야외 캠프 동향, 익숙하지 않은 지역에서의 앱 기반 네비게이션의 용이성 등으로 견조한 성장을 유지하고 있습니다. 동시에 운전자와 함께 상품은 이벤트 물류와 홍콩으로의 국경 셔틀 버스로 다양화되어 중국의 차량 렌탈 시장 내 대응 가능한 수요를 확대하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 국내 관광의 회복이 레저 렌탈을 뒷받침

- Tier 1 도시의 번호판 할당이 렌탈 수요를 촉진

- 면허를 가지는 중간층 증가

- 차량전화의 의무화에 의해 제로·에미션 존이 오픈

- 디지털 및 모바일 예약 플랫폼으로의 이동

- 기업의 ESG 목표가 장기적인 녹색계약을 촉진

- 시장 성장 억제요인

- 라이드 헤일링과 로봇 택시에 의한 대체 리스크

- 차량 취득 및 자금 조달 비용 상승

- 주마다의 플레이트 할당의 변동으로 인한 차량 운영 차질

- EV 잔존 가치의 불확실성이 수익성을 압박

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Five Forces 분석

- 신규 진입자의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측

- 용도별

- 레저/관광

- 비즈니스 여행

- 예약 유형별

- 오프라인 접근

- 온라인 접근

- 최종 사용자별

- 자가 운전

- 운전기사 동반

- 차량 클래스별

- 이코노미

- 중형

- 럭셔리

- SUV/MPV

- 구동 방식별

- 내연기관(ICE)

- 하이브리드 자동차(HEV)

- 배터리 전기자동차(BEV)

- 렌탈 기간별

- 단기(1주일 이하)

- 중기(1주일-1개월)

- 장기(1개월 이상)

- 서비스 채널별

- 공항 내

- 공항 외/도심

- 지역별

- 중국 동부

- 중국 중남부

- 중국 북부

- 중국 서부

- 중국 동북부

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- Beijing China Auto Rental(CAR Inc.)

- eHi Car Service

- Shouqi Car Rental

- Avis Budget Group

- Hertz Corporation

- Shenzhen Topone Car Rental

- Didi Car Rental

- EVCard

- Gofun Travel

- Xiangdao Chuxing

- UCAR Inc.

- Zuzuche

- Caocao Mobility

- PonyCar

- T3 Go Mobility

- Shenzhou Joy Travel

- Tongcheng-Elong Car Rental

- Huizuche

- Hello Chuxing Car Rental

- Meituan Car Rental

제7장 시장 기회와 전망

KTH 25.10.29The China Vehicle Rental Market size is estimated at USD 21.15 billion in 2025, and is expected to reach USD 27.11 billion by 2030, at a CAGR of 5.13% during the forecast period (2025-2030).

A rebound in domestic leisure travel, stricter license-plate quotas in tier-1 cities, and a nationwide 80% new-energy fleet mandate are aligning to keep demand elevated across consumer and corporate channels. Rising middle-class licensed-driver numbers in tier-2 and tier-3 cities, the rapid diffusion of AI-enabled booking apps, and a policy tilt toward electric models are reshaping fleet composition faster than in any prior five-year period.

China Vehicle Rental Market Trends and Insights

Domestic Tourism Rebound Fuels Leisure Rentals

Leisure bookings surged after authorities reported 295 million domestic trips during the 2024 May Day holiday, spending more than 20 billion and lifting vehicle demand in county-level destinations. Cities such as Liuzhou and Zibo attracted first-time visitors who preferred self-drive access over public transport, pushing average rental duration above four days in many inland locations. Zuzuche responded by onboarding 3,000 domestic supplier partners inside four months, demonstrating the platform scalability advantage of digital marketplaces. Cultural-nighttime tourism at heritage sites kept utilization high into late evenings, supporting premium pricing windows. Momentum remains intact as the Ministry of Culture and Tourism forecasts domestic trips to exceed 6 billion in 2025, cementing leisure as the backbone of the China vehicle rental market.

License-Plate Quotas in Tier-1 Cities Spur Rental Demand

Beijing's annual lottery caps private cars at 100,000 new plates, 70% reserved for EVs, while Shanghai auctions often exceed CNY 95,000 per plate. These restrictions make daily rental cheaper than ownership for many commuters. Tianjin plans to issue 80,000 more green plates yearly but retains fossil-fuel limits, keeping cost pressure in place. Plate quotas have cut fuel consumption and tailpipe emissions by nearly 50% in affected cities, but they have simultaneously created a reliable flow of renters who view cars as occasional utilities rather than assets. The policy also skews fleets toward EVs, reinforcing government carbon goals and reshaping the China vehicle rental market.

Ride-Hailing & Robotaxi Substitution Risk

Baidu's Apollo Go completed 839,000 autonomous rides in Q4 2023 at fares 60-70% beneath traditional taxis, illustrating a disruptive price gap. Pony.ai targets a 1,000-vehicle fleet by 2025, while WeRide launched unmanned services linking Beijing Daxing International Airport in February 2025. Robotaxi operators benefit from 24/7 availability and lower driver-related expenses, diverting demand that historically favored rentals for airport transfers and intra-city errands. Consultancy forecasts place the robotaxi segment at nearly USD 76 billion by 2030, signalling competitive headwinds for the China vehicle rental market if incumbents cannot secure autonomous partnerships.

Other drivers and restraints analyzed in the detailed report include:

- Growing Licensed-Driver Middle Class

- Shift to Digital & Mobile Booking Platforms

- Rising Vehicle Acquisition & Financing Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Leisure and tourism held 51.27% of China vehicle rental market share in 2024, underpinned by a 7.6% jump in holiday trips and renewed interest in county-level cultural sites. Short road vacations and family reunions make self-drive cars the preferred option, driving average utilization to 74% during peak weeks. Business travel trails in absolute size but records the highest growth; its projected 5.22% CAGR benefits from border reopenings and corporate ESG targets favoring rental over owned fleets.

Second-order effects are already visible in spending patterns: leisure customers reserve 2.1 days longer than pre-pandemic averages, while business travelers increasingly opt for chauffeur-driven packages that bundle telematics and emissions dashboards for reporting purposes. Platform integrations with tourist attractions enable one-click car plus ticket bundles, extending the monetization window per rental.

Online reservations captured 64.38% of revenue in 2024-proof that frictionless mobile journeys have become table stakes, it is also growing at a CAGR of 5.41% through 2030. Predictive pricing engines reduce search-to-booking windows to four minutes on average and increase ancillary upselling by 18%, raising lifetime value per customer. Offline stores still matter in lower-tier cities where walk-in foot traffic remains notable, but omnichannel hand-over stations now allow QR-code key retrieval without staff, closing the convenience gap.

Investment continues to tilt toward cloud CRM and in-car IoT sensors that feed usage data back to the platform, enabling same-day inventory rotation across multiple districts. As a result, fleet operators using dynamic online allocation achieve 12% higher revenue-per-vehicle than peers relying on static offline reservations, a differential expected to expand in the China vehicle rental market.

Self-drive contracts controlled 71.32% of total revenue in 2024, fuelled by the cultural preference for independent travel and growing confidence behind the wheel. Yet chauffeur-driven packages advance at 5.45% annually because corporate procurement teams view them as safer and more compliant with ESG audit trails. Chauffeur fleets feature NEV penetration above 60%, exceeding the broader average and positioning them well for low-emission zones in Beijing or Shenzhen Central Business Districts.

Self-drive growth remains robust through family-oriented itineraries, outdoor camping trends, and the ease of app-based navigation in unfamiliar provinces. Simultaneously, chauffeur products diversify into event logistics and cross-border shuttles into Hong Kong, expanding addressable demand inside the China vehicle rental market.

The China Vehicle Rental Market Report is Segmented by Application (Leisure/Tourism and Business Travel), Booking Type (Offline Access and Online Access), End-User Type (Self-Driven and Chauffeur-Driven), Vehicle Class (Economy and More), Powertrain (ICE, HEV and BEV), Rental Duration (Short-Term and More), Service Channel (On-Airport and More), and Region. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Beijing China Auto Rental (CAR Inc.)

- eHi Car Service

- Shouqi Car Rental

- Avis Budget Group

- Hertz Corporation

- Shenzhen Topone Car Rental

- Didi Car Rental

- EVCard

- Gofun Travel

- Xiangdao Chuxing

- UCAR Inc.

- Zuzuche

- Caocao Mobility

- PonyCar

- T3 Go Mobility

- Shenzhou Joy Travel

- Tongcheng-Elong Car Rental

- Huizuche

- Hello Chuxing Car Rental

- Meituan Car Rental

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Domestic tourism rebound fuels leisure rentals

- 4.2.2 License-plate quotas in Tier-1 cities spur rental demand

- 4.2.3 Growing licensed-driver middle class

- 4.2.4 Fleet-electrification mandates open zero-emission zones

- 4.2.5 Shift to digital & mobile booking platforms

- 4.2.6 Corporate ESG targets drive long-term green subscriptions

- 4.3 Market Restraints

- 4.3.1 Ride-hailing & robotaxi substitution risk

- 4.3.2 Rising vehicle acquisition & financing costs

- 4.3.3 Provincial plate-quota volatility disrupts fleet logistics

- 4.3.4 EV residual-value uncertainty pressures profitability

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Application

- 5.1.1 Leisure / Tourism

- 5.1.2 Business Travel

- 5.2 By Booking Type

- 5.2.1 Offline Access

- 5.2.2 Online Access

- 5.3 By End-User Type

- 5.3.1 Self-Driven

- 5.3.2 Chauffeur-Driven

- 5.4 By Vehicle Class

- 5.4.1 Economy

- 5.4.2 Mid-Scale

- 5.4.3 Luxury

- 5.4.4 SUV / MPV

- 5.5 By Powertrain

- 5.5.1 Internal Combustion Engine (ICE)

- 5.5.2 Hybrid Electric Vehicle (HEV)

- 5.5.3 Battery Electric Vehicle (BEV)

- 5.6 By Rental Duration

- 5.6.1 Short-Term (Less than or equal to 1 Week)

- 5.6.2 Medium-Term (1 Week to 1 Month)

- 5.6.3 Long-Term (More than 1 Month)

- 5.7 By Service Channel

- 5.7.1 On-Airport

- 5.7.2 Off-Airport / Downtown

- 5.8 By Region

- 5.8.1 East China

- 5.8.2 South-Central China

- 5.8.3 North China

- 5.8.4 West China

- 5.8.5 Northeast China

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Beijing China Auto Rental (CAR Inc.)

- 6.4.2 eHi Car Service

- 6.4.3 Shouqi Car Rental

- 6.4.4 Avis Budget Group

- 6.4.5 Hertz Corporation

- 6.4.6 Shenzhen Topone Car Rental

- 6.4.7 Didi Car Rental

- 6.4.8 EVCard

- 6.4.9 Gofun Travel

- 6.4.10 Xiangdao Chuxing

- 6.4.11 UCAR Inc.

- 6.4.12 Zuzuche

- 6.4.13 Caocao Mobility

- 6.4.14 PonyCar

- 6.4.15 T3 Go Mobility

- 6.4.16 Shenzhou Joy Travel

- 6.4.17 Tongcheng-Elong Car Rental

- 6.4.18 Huizuche

- 6.4.19 Hello Chuxing Car Rental

- 6.4.20 Meituan Car Rental

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment