|

시장보고서

상품코드

1842672

만성 골수성 백혈병 치료 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Chronic Myelogenous Leukemia Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

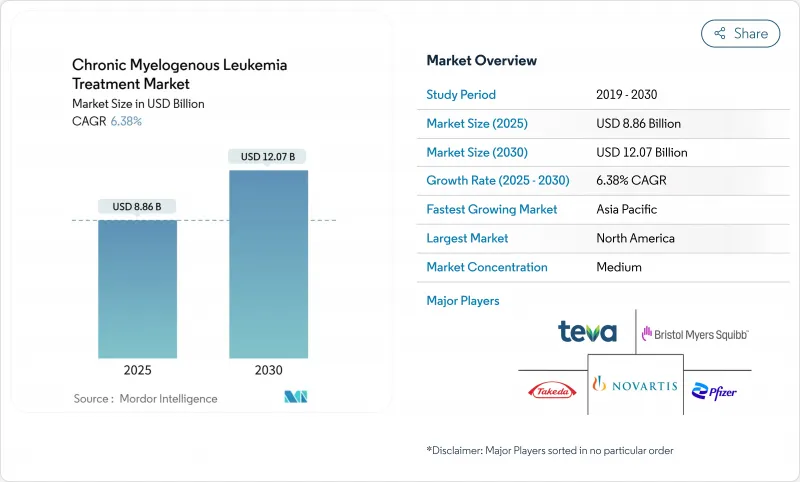

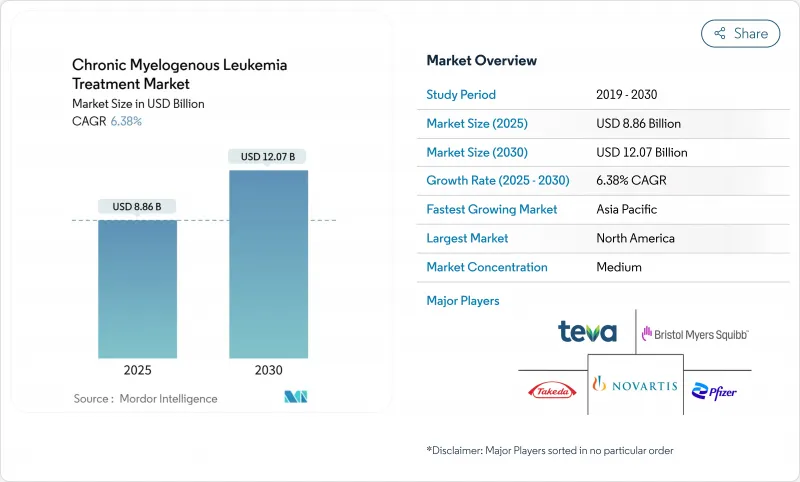

만성 골수성 백혈병 치료 시장은 2025년에는 88억 6,000만 달러에 다다를 것으로 예상되며, 2030년에는 120억 7,000만 달러로 CAGR 6.38%로 성장할 것으로 예측됩니다.

이 시장 확대는 CML이 과거의 치명적인 진단에서 정밀의료에 의해 관리되는 만성 질환으로 꾸준히 전환하고 있기 때문입니다. 차세대 티로신 키나아제 억제제(TKI)의 견조한 보급, 무치료 관해에 대한 임상적 관심 증가, 분자 모니터링에 대한 광범위한 접근이 수요를 지원하고 있습니다. 간편한 경구 요법에 대한 환자의 선호도 변화와 획기적인 신약에 대한 규제 당국의 지원은 수익 가능성을 더욱 높입니다. 한편, 당면한 제네릭 2G TKI와의 가격 경쟁은 혁신적인 약물의 상승을 저해하지 않고 환자의 접근을 확대할 것으로 기대됩니다.

세계의 만성 골수성 백혈병 치료 시장의 동향과 인사이트

CML 발병률과 유병률 상승

CML의 세계 진단 수는 인구동태의 고령화와 함께 확대되고 있으며, 2024년에는 미국에서 새롭게 8,930명의 사례가 발생한 것으로 나타났습니다. 일상적인 혈액 검사에 의한 조기 발견은 TKI에 잘 반응하는 만성기의 증례를 증가시킵니다. 생존율 향상으로 장기 치료를 필요로 하는 유병자층이 확대되는 반면 저중소득국(LMIC)에서는 진단이 불충분하기 때문에 향후 큰 성장의 여지가 있습니다. 유럽과 미국의 의료제도는 이미 분자진단을 표준 치료로 통합하고 있으며, 검사 시설의 인프라가 성숙함에 따라 아시아태평양에서도 비슷한 보급이 예상됩니다.

차세대 TKI의 혁신

올베렘바티닙(olverembatinib)과 같은 돌연변이 특이적 약물은 어려운 T315I 내성을 다루고 중국에서 혁신치료제로 지정되었습니다.

다중 TKI에 의한 표적 외독성 및 심혈관 사건

닐로티닙과 포나티닙은 동맥 사건과의 연관성을 지적받고 있으며, 기준선의 심혈관 위험 평가와 빈번한 모니터링이 필요합니다. TKI의 연속 사용은 위험을 증가시키기 때문에 더 빠른 초기 TFR과 더 좁은 키나아제 억제 프로파일을 제공하는 대체 돌연변이 특이적 약물에 관심이 집중되고 있습니다.

부문 분석

표적 치료는 2024년에 74.56%의 매출을 확보하였고 2030년까지 만성 골수성 백혈병 치료 시장을 지원할 전망입니다. 의사의 높은 이해도, 가이드라인에 널리 도입된 점, 분자학적 주효율이 높은 점 등이 그 우위성을 유지하고 있습니다. 면역요법은 이제 시작되었지만, 펩티드 백신과 CAR-T 프로그램이 지속적인 관해 신호를 보고하면서 CAGR은 9.56%로 가장 높을 것으로 예측됩니다. 면역요법의 만성 골수성 백혈병 치료 시장에서의 규모는 장기적인 분자 조절의 임상 증거가 증가함에 따라 확대될 것으로 예측됩니다. 이탈리아의 주요 연구에서는 백신 수용자의 80%가 펩티드 특이적 CD4 반응을 얻었고, 16.5%는 48개월 동안 TFR을 지속했습니다.

줄기세포 이식은 만성기 수혜자의 5년 무병 생존율이 80%이며 치유의 가능성을 유지하고 있지만, TKI가 조기 진행을 완화함에 따라 그 점유율은 축소되고 있습니다. 이식 후 시클로 포스파미드는 기증자 풀을 확장하고 특히 유전적으로 다양한 집단에 혜택을 제공합니다. 화학요법은 여전히 급성 전환기로 제한되지만, CD20 및 기타 마커를 표적으로 하는 단일클론항체는 조기 임상시험을 거쳐 진행되고 있습니다.

2024년 만성 골수성 백혈병 치료 시장 점유율의 62.31%는 일차치료이며, 이매티닙의 긴 수명과 이차치료의 가용성의 정도에 의해 지원됩니다. 3차치료 이후의 치료법은 환자의 수명이 연장됨에 따라 내성 변이가 축적되기 때문에 CAGR은 7.88%로 예측됩니다. NCCN 가이드라인은 최초의 TKI 선택을 Sokal 또는 ELTS 위험 점수, 연령, 합병증 부담에 맞추는 경향이 커지고 있습니다. 애시미닙과 올베렘바티닙에 의한 돌연변이 유도 시퀀싱은 삼차치료로의 흡수를 증가시킬 것으로 보입니다. 만성 골수성 백혈병 치료에서 후기 치료 시장 규모는 임상가가 병용 요법과 돌연변이 특이적 요법을 채택하여 역대 최고치를 경신할 것으로 예측됩니다.

지역 분석

북미는 2024년 세계 매출의 40.33%를 차지하였으며, FDA의 조기 승인, 종합적인 보험 적용, 분자 연구소의 세계 최고 밀도에 의해 뒷받침되고 있습니다. 미국의 아카데믹 허브가 TFR 시험과 병용 시험을 개척해 세계적인 임상 벤치마크를 설정하고 있습니다. 캐나다는 국민 건강보험 제도에 의해 TKI에의 액세스는 확산되고 있지만, 신약의 채용은 각 주의 처방 심사에 따라 지연될 수 있습니다.

아시아태평양은 CAGR 8.34%로 향후 성장을 견인할 전망입니다. 중국은 국가 보험 환급 의약품 목록을 통해 획기적인 치료제를 신속하게 도입하고 인도는 민간 보험의 보급률 상승을 활용하여 TKI를 구입합니다. 일본에서는 초고령화 사회가 안정된 수요를 유지하고, 한국에서는 정밀의료에 대한 노력이 AI 기반 모니터링을 촉진합니다. 지역 격차는 뿌리 깊으며 인도와 인도네시아의 농촌 지역에서는 실시간 PCR의 능력이 아직 부족하여 최적의 치료법 조정이 지연되었습니다.

유럽은 성숙하지만 혁신친화적인 무대입니다. Project Orbis의 협력은 EMA와 FDA의 동시 심사를 가능하게 하고 접근 격차를 줄였습니다. 독일과 영국은 적응 시험 디자인의 선두를 달리고 있지만, 남유럽에서는 예산의 제약으로 프리미엄 요법의 도입이 늦어지고 있습니다. 중동 및 아프리카는 여전히 신흥 시장이며, 그 확장은 실험실 네트워크에 대한 투자와 기증자 자금을 통한 투약 프로그램에 달려 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- CML의 발병률 및 유병률의 상승

- 차세대 TKI의 획기적인

- 연구개발자금과 임상시험량 증가

- 무치료 관해(TFR) 프로토콜로의 이동

- 제네릭 2G TKI의 등장에 의한 치료 비용 절감

- 투여량 최적화를 위한 AI에 의한 분자 모니터링

- 시장 성장 억제요인

- 멀티 TKI에 의한 표적 외독성과 심혈관 이벤트

- 엄격한 규제와 약물감시 요건

- 어드히어런스 불량에 의한 TKI 내성 증가

- LMICs에서의 불충분한 분자 모니터링 접근

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모와 성장 예측

- 치료 유형별

- 표적요법

- 화학요법

- 생물학적 요법

- 줄기세포 이식

- 면역요법

- 기타 치료

- 치료 단계별

- 일차치료

- 이차치료

- 삼차치료 이후

- 투여 경로별

- 경구

- 정맥내 투여

- 피하 투여

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인 약국

- 전문 클리닉

- 환자 연령층별

- 소아

- 성인

- 노인

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Novartis AG

- Bristol Myers Squibb Co.

- Pfizer Inc.

- Takeda Pharmaceutical Co. Ltd.

- Incyte Corp.

- Merck & Co., Inc.

- F. Hoffmann-La Roche Ltd.

- Sanofi SA

- Boehringer Ingelheim GmbH

- Teva Pharmaceutical Industries Ltd.

- Viatris Inc.

- Cipla Ltd.

- Amneal Pharmaceuticals LLC

- Accord Healthcare Inc.

- Fresenius Kabi AG

- Ascentage Pharma Group Corp.

- Hansoh Pharmaceutical Group Co. Ltd.

- Sun Pharma Industries Ltd.

- Dr. Reddy's Laboratories Ltd.

- Hikma Pharmaceuticals plc

- Aurobindo Pharma Ltd.

제7장 시장 기회와 전망

CSM 25.11.03The Chronic Myelogenous Leukemia Treatment market is valued at USD 8.86 billion in 2025 and is projected to climb to USD 12.07 billion by 2030, advancing at a 6.38% CAGR.

Expansion stems from the steady transition of CML from a once-fatal diagnosis to a chronic condition managed through precision medicine. Robust uptake of next-generation tyrosine-kinase inhibitors (TKIs), rising clinical focus on treatment-free remission, and broader access to molecular monitoring underpin demand. Shifting patient preferences toward convenient oral regimens, paired with regulatory support for breakthrough drugs, further elevate revenue potential. Meanwhile, price competition from imminent generic 2G TKIs is expected to widen patient access without eroding premium uptake of innovative agents.

Global Chronic Myelogenous Leukemia Treatment Market Trends and Insights

Rising Incidence & Prevalence of CML

Global CML diagnoses are expanding alongside aging demographics, with 8,930 new U.S. cases anticipated in 2024. Earlier detection through routine blood tests leads to more chronic-phase presentations that respond favorably to TKIs. Improved survival enlarges the prevalent patient pool requiring long-term therapy, while underdiagnosis in low- and middle-income countries (LMICs) leaves room for significant future growth. Healthcare systems in Europe and North America already integrate molecular diagnostics as standard of care, setting the stage for similar penetration in Asia Pacific as laboratory infrastructure matures.

Breakthroughs in Next-Gen TKIs

The FDA's 2024 accelerated approval of asciminib for newly diagnosed patients showcases a novel myristoyl-pocket mechanism that achieved a 68% major molecular response versus 49% with comparator TKIs.Mutation-specific agents like olverembatinib address difficult T315I resistance and received breakthrough status in China, signaling a pipeline pivot toward precision targeting that curtails off-target toxicity.

Off-Target Toxicities & Cardiovascular Events with Multi-TKIs

Nilotinib and ponatinib have been linked to arterial events that necessitate baseline cardiovascular risk assessments and frequent monitoring. Sequential TKI use compounds risk, prompting interest in earlier TFR or alternative mutation-specific drugs that offer narrower kinase inhibition profiles.

Other drivers and restraints analyzed in the detailed report include:

- Escalating R&D Funding & Clinical-Trial Volume

- Shift Toward Treatment-Free Remission (TFR) Protocols

- Stringent Regulatory & Pharmacovigilance Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Targeted therapy secured 74.56% revenue in 2024 and underpins the Chronic Myelogenous Leukemia Treatment market through 2030. Widespread physician familiarity, broad guideline inclusion, and deep molecular response rates maintain its primacy. Immunotherapy, while nascent, is forecast for the highest 9.56% CAGR as peptide vaccines and CAR-T programs report durable remission signals. The Chronic Myelogenous Leukemia Treatment market size for immunotherapy is projected to expand alongside growing clinical evidence of long-term molecular control. In pivotal Italian studies, 80% of vaccine recipients mounted peptide-specific CD4+ responses and 16.5% sustained TFR for 48 months.

Stem-cell transplantation retains curative potential with 80% five-year disease-free survival in chronic-phase recipients, yet its share shrinks as TKIs mitigate early progression. Post-transplant cyclophosphamide broadens donor pools, particularly benefitting genetically diverse populations. Chemotherapy remains limited to blast-phase crises, while monoclonal antibodies aimed at CD20 and other markers advance through early trials.

First-line regimens held 62.31% of Chronic Myelogenous Leukemia Treatment market share in 2024, anchored by imatinib's longevity and wider availability of 2G alternatives. Third-line and beyond therapies are forecast for 7.88% CAGR as resistance mutations accumulate over extended patient lifespans. NCCN guidelines increasingly tailor initial TKI choice to Sokal or ELTS risk scores, age, and comorbidity burden. Mutation-guided sequencing with asciminib and olverembatinib is set to lift third-line uptake. The Chronic Myelogenous Leukemia Treatment market size for later-line settings is projected to reach new highs as clinicians adopt combination and mutation-specific regimens.

Chronic Myelogenous Leukemia Treatment Market Report is Segmented by Treatment Type (Targeted Therapy, Chemotherapy, and More), Line of Therapy (First-Line, Second-Line and More), Route of Administration (Oral, Intravenous and More), Distribution Channel (Hospital Pharmacies, Retail Pharmacies and More), Patient Age Group (Pediatric, Adults and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 40.33% of global revenue in 2024, supported by early FDA approvals, comprehensive insurance coverage, and the world's highest density of molecular labs. U.S. academic hubs pioneer TFR studies and combination trials that set clinical benchmarks worldwide. Canadian universal coverage widens TKI access, though adoption of brand-new agents can lag due to provincial formulary reviews.

Asia Pacific leads future growth at an 8.34% CAGR. China fast-tracks breakthrough therapies through the National Reimbursement Drug List, while India leverages rising private insurance penetration to pay for TKIs. Japan's super-aged society sustains steady demand, and South Korea's precision-medicine initiatives promote AI-based monitoring. Regional disparities persist: rural areas in India and Indonesia still lack real-time PCR capacity, delaying optimal therapy adjustments.

Europe constitutes a mature but innovation-friendly arena. Project Orbis collaboration allows simultaneous EMA-FDA reviews, shrinking access gaps. Germany and the United Kingdom spearhead adaptive trial designs, whereas budget constraints in Southern Europe can slow uptake of premium therapies. The Middle East and Africa remain nascent markets whose expansion hinges on lab-network investments and donor-funded medication programs.

- Novartis

- Bristol-Myers Squibb

- Pfizer

- Takeda Pharmaceuticals

- Incyte Corp.

- Merck

- Roche

- Sanofi

- Boehringer Ingelheim

- Teva Pharmaceutical Industries

- Viatris

- Cipla

- Amneal Pharmaceuticals

- Accord Healthcare

- Fresenius

- Ascentage Pharma Group Corp.

- Hansoh Pharmaceutical Group Co. Ltd.

- Sun Pharma Industries Ltd.

- Dr. Reddy's Laboratories Ltd.

- Hikma Pharmaceuticals

- Aurobindo Pharma Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence & Prevalence Of CML

- 4.2.2 Breakthroughs In Next-Gen TKIs

- 4.2.3 Escalating R&D Funding & Clinical-Trial Volume

- 4.2.4 Shift Toward Treatment-Free Remission (TFR) Protocols

- 4.2.5 Imminent Wave Of Generic 2G TKIs Reducing Therapy Cost

- 4.2.6 AI-Enabled Molecular Monitoring For Dose Optimisation

- 4.3 Market Restraints

- 4.3.1 Off-Target Toxicities & Cardiovascular Events With Multi-Tkis

- 4.3.2 Stringent Regulatory & Pharmacovigilance Requirements

- 4.3.3 Rising Real-World TKI Resistance From Poor Adherence

- 4.3.4 Inadequate Molecular-Monitoring Access In LMICs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Treatment Type

- 5.1.1 Targeted Therapy

- 5.1.2 Chemotherapy

- 5.1.3 Biologic Therapy

- 5.1.4 Stem Cell Transplantation

- 5.1.5 Immunotherapy

- 5.1.6 Other Treatment Types

- 5.2 By Line of Therapy

- 5.2.1 First-line

- 5.2.2 Second-line

- 5.2.3 Third-line & Beyond

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Intravenous

- 5.3.3 Subcutaneous

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.4.4 Specialty Clinics

- 5.5 By Patient Age Group

- 5.5.1 Pediatric

- 5.5.2 Adults

- 5.5.3 Geriatric

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Novartis AG

- 6.3.2 Bristol Myers Squibb Co.

- 6.3.3 Pfizer Inc.

- 6.3.4 Takeda Pharmaceutical Co. Ltd.

- 6.3.5 Incyte Corp.

- 6.3.6 Merck & Co., Inc.

- 6.3.7 F. Hoffmann-La Roche Ltd.

- 6.3.8 Sanofi SA

- 6.3.9 Boehringer Ingelheim GmbH

- 6.3.10 Teva Pharmaceutical Industries Ltd.

- 6.3.11 Viatris Inc.

- 6.3.12 Cipla Ltd.

- 6.3.13 Amneal Pharmaceuticals LLC

- 6.3.14 Accord Healthcare Inc.

- 6.3.15 Fresenius Kabi AG

- 6.3.16 Ascentage Pharma Group Corp.

- 6.3.17 Hansoh Pharmaceutical Group Co. Ltd.

- 6.3.18 Sun Pharma Industries Ltd.

- 6.3.19 Dr. Reddy's Laboratories Ltd.

- 6.3.20 Hikma Pharmaceuticals plc

- 6.3.21 Aurobindo Pharma Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.1.1 .