|

시장보고서

상품코드

1844453

스페인의 심혈관 기기 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Spain Cardiovascular Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

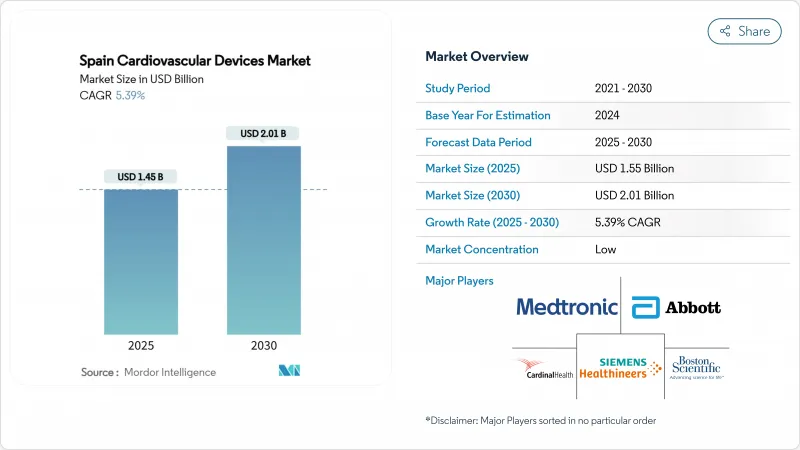

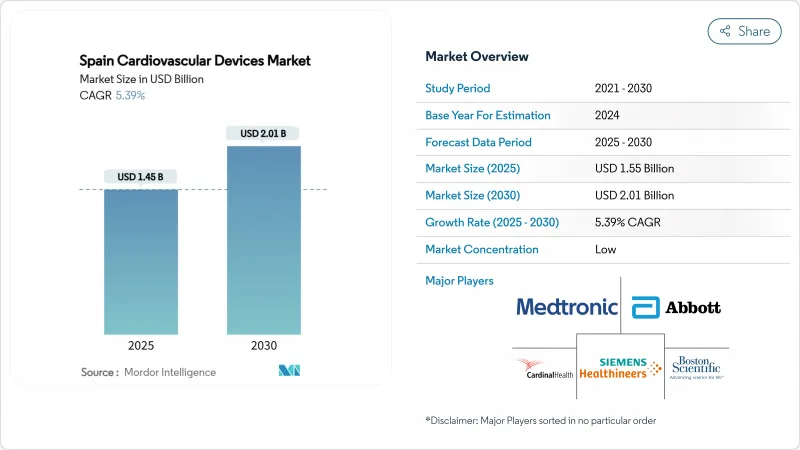

스페인의 심혈관 기기 시장 규모는 2025년에 15억 5,000만 달러, 2030년에는 20억 1,000만 달러에 이르고, 2025-2030년의 연평균 복합 성장률(CAGR)은 5.39%를 나타낼 전망입니다.

이 성장은 전반적인 예산 규율을 유지하면서 공립 병원 시설을 현대화하려는 정부의 이니셔티브를 반영합니다. 스페인의 심혈관 기기 시장에서는 치료 장비와 수술 장비가 가장 큰 점유율을 차지하고 있지만, 병원은 질병의 조기 발견과 입원 기간 단축을 목표로 진단 및 모니터링 기술의 진보가 가속화되고 있습니다. 인터벤셔널 하드웨어에 디지털 모니터링 서비스를 번들로 제공하는 제조업체는 이미 광범위한 경상 수익원으로부터 이익을 얻고 있습니다. 한편, 민간 심장병 네트워크를 통한 투자 가속화는 총 수요를 높이고 프리미엄 기능에 대한 기대를 높이기 위해 공급업체는 공공 기관을 위한 표준 제품과 민간 센터를 위한 하이엔드 솔루션의 균형을 맞추어야 합니다.

스페인의 심혈관 기기 시장 동향과 통찰

2022-2029년 국가 순환기 보건 계획이 공공 조달을 촉진

이 계획에서는 심혈관 기기의 현대화에 2억 1,500만 유로가 할당되어 노후화된 영상 진단 시스템과 카테터 검사실의 갱신이 가속화되고 있습니다. 표준화된 다년간 서비스 계약은 입찰 주기를 단축하고 교육을 보장하므로 기본 진단 플랫폼에 대한 양 주도 성장과 첨단 기술에 대한 가치 주도 수요를 촉진합니다. 서비스가 충분하지 않은 지역 병원은 최신 심장 초음파에 신속하게 액세스할 수 있으며, 플래그십 센터는 완전히 통합된 카테라보 스위트를 채택합니다. 점진적인 포트폴리오를 가진 공급업체는 성능 스펙트럼의 양쪽 끝을 충족하여 점유율을 얻습니다.

급속한 고령화로 장비 수요 증가

65세 이상의 노인들은 심장 수술의 불균형 비율을 차지하고 있으며 지중해 연안에 모여 있기 때문에 이용률이 높은 핫스팟이 형성되고 있습니다. 80대 노인은 현재 경 카테터 판막 치환술을 받는 환자가 가장 급증하고 있는 그룹이며, 병원은 스케줄과 애프터 케어 프로토콜을 검토할 필요가 있습니다. 제조업체 각 회사는 재입원 위험을 줄이기 위해 소형 임플란트와 배터리 수명이 길어집니다. 노인 친화적인 기술을 채택한 병원에서는 지역 평균을 웃도는 이용 효율을 얻을 수 있는 경우가 많습니다.

지역 입찰가 격차가 판매 가격을 압축

안달루시아, 발렌시아 등 자치주는 직접 협상 수준보다 15-20% 낮은 기준 가격을 강제합니다. 이 모델은 총 소유 비용을 선호하고 소모품, 유지 보수 및 교육을 번들로 입찰을 장려합니다. 중견 공급업체는 이익률이 낮은 카테고리에서 철수하고 규모를 활용하는 기업에 점유율이 집계됩니다. 현재의 규칙이 계속되면 병원은 상품 분야에서의 선택이 줄어들 수 있습니다.

부문 분석

2024년 스페인 심장혈관 장비 시장 점유율은 관상동맥 스텐트와 심장 리듬 관리 임플란트가 견인했으며 치료 장비와 수술 장비가 57.20%를 차지했습니다. 동시에 진단 및 모니터링 기기의 스페인 심혈관계 기기 시장 규모는 AI 유도 영상 진단과 조기 발견을 위한 국고 조성으로 2030년까지 연평균 복합 성장률(CAGR) 6.03%로 성장할 전망입니다. 또한 고급 트랜스 카테터 장비는 구식 수술 장비의 수명주기를 단축하고 입원 기간을 단축하는 저 침습 시스템으로 조달을 이동시킵니다. 모듈형 소프트웨어 라이선스를 핵심 하드웨어로 패키징할 수 있는 공급업체는 이에 비례하여 제조 비용을 늘리지 않고도 수익을 올릴 수 있습니다.

진단 시스템의 도입은 더 이상 아카데믹 센터에 국한되지 않습니다. 분수 흐름 예비 플랫폼과 3D 심장 에코는 전국 순환기 건강 계획 하에서 표준화된 조달 가이드라인에 힘입어 지역 병원에 침투하고 있습니다. 동시에 치료 분야에서는 회복 시간 단축으로 인한 비용 효과가 지불자에게 인식됨에 따라 구조적 심장 인터벤션에 중점을 두고 있습니다. 장비 혁신으로 재원일수 단축을 달성한 병원은 종종 실적 기반 대출을 받을 자격이 있으며 최신 임플란트에 대한 수요를 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트·지원

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 2022-2029년 국가 순환기 보건 계획이 공립 병원에서의 기기 조달을 촉진

- 스페인 인구의 급속한 고령화에 의한 심장 기기 수요 증가

- TAVR과 TMVR의 보험 상환이 구조 심장 기기의 보급을 가속

- 민간 심장병 네트워크의 확대가 하이엔드 CRM 및 화상 기기를 견인

- 디지털 심장 원격 감시 플랫폼에 대한 자금 증가

- 시장 성장 억제요인

- 평균 판매 가격을 압축하는 지역 입찰 가격 상한선

- 스페인에서 신제품 출시를 지연시키는 MDR 재인증 백로그

- 마드리드 및 카탈루냐 외곽의 중재 심장 전문의 부족으로 시술량 제한

- 공급업체 현금 흐름에 영향을 미치는 120일 병원 결제 주기

- 가치/공급망 분석

- 규제 전망

- 기술적 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 디바이스별

- 진단 및 모니터링 기기

- 심전도 시스템

- 원격 심장 모니터

- 심장 MRI

- 심장 CT

- 심 에코/초음파 검사

- 분획 혈류 예비능(FFR) 시스템

- 치료 및 수술용 기기

- 관상동맥 스텐트

- 약제 용출 스텐트

- 베어 메탈 스텐트

- 생체 흡수성 스텐트

- 카테터

- PTCA 풍선 카테터

- IVUS/OCT 카테터

- 심장 리듬 관리

- Pacemakers

- 이식형 제세동기

- 심장 재동기 치료 기기

- 심장 벨브

- TAVR/TAVI

- 기계식 밸브

- 조직/생체 인공 밸브

- 보조 인공 심장

- 인공 심장

- 그래프트 & 패치

- 기타 심장혈관 외과용 기기

- 진단 및 모니터링 기기

- 적응증별

- 관상동맥질환

- 부정맥

- 심부전

- 심장 판막증

- 최종 사용자별

- 병원

- 재택치료

- 기타

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Medtronic Plc

- Boston Scientific Corporation

- Abbott Laboratories

- Edwards Lifesciences Corporation

- Philips Healthcare

- Siemens Healthineers AG

- Terumo Corporation

- Biotronik SE & Co. KG

- MicroPort Scientific Corporation

- LivaNova PLC

- Cardinal Health(Cordis)

- B. Braun Melsungen AG

- Meril Life Sciences Pvt Ltd

- Acist Medical Systems

- Getinge AB(Maquet)

- WL Gore & Associates

- Johnson & Johnson(Biosense Webster)

- Teleflex

제7장 시장 기회와 전망

SHW 25.11.03The Spain cardiovascular devices market size stands at USD 1.55 billion in 2025 and is projected to reach USD 2.01 billion by 2030, yielding a compound annual growth rate (CAGR) of 5.39% for 2025-2030.

This growth reflects the government's effort to modernize public hospital equipment while maintaining overall budget discipline. Therapeutic and surgical devices command the largest Spain cardiovascular devices market share, whereas diagnostic and monitoring technologies are advancing faster as hospitals look to detect disease earlier and shorten inpatient stays. Manufacturers that bundle interventional hardware with digital monitoring services already benefit from broader recurring revenue streams. Meanwhile, accelerated investment by private cardiology networks lifts total demand and raises expectations for premium functionality, forcing suppliers to balance standardized offerings for public institutions with high-end solutions for private centers.

Spain Cardiovascular Devices Market Trends and Insights

National Cardiovascular Health Plan 2022-2029 Catalyzing Public Procurement

The plan allocates EUR 215 million for cardiovascular equipment modernization, accelerating replacement of aging imaging systems and catheterization labs. Standardized multi-year service contracts shorten bid cycles and guarantee training, which spurs volume-led growth for basic diagnostic platforms and value-driven demand for advanced technologies. Hospitals in underserved regions gain faster access to updated cardiac ultrasound, while flagship centers adopt fully integrated cath-lab suites. Suppliers with tiered portfolios capture share by meeting both ends of the performance spectrum.

Rapidly Ageing Population Expanding Device Demand

Citizens older than 65 generate a disproportionate share of cardiac procedures, and their clustering along the Mediterranean coastline creates utilization hotspots. Octogenarians are now the fastest-growing group for transcatheter valve replacement, prompting hospitals to revise scheduling and after-care protocols. Manufacturers have answered with smaller implants and longer battery life, which reduce rehospitalization risk. Hospitals that embrace geriatric-friendly technology often see utilization efficiencies that exceed regional averages.

Regional Tender Price Caps Compress Selling Prices

Autonomous communities such as Andalusia and Valencia enforce reference pricing 15-20% below direct-negotiation levels. The model prioritizes total cost of ownership, encouraging bids that bundle disposables, maintenance, and training. Mid-tier suppliers leave low-margin categories, consolidating share among firms that leverage scale. Hospitals could face fewer options in commodity segments if the current rules persist.

Other drivers and restraints analyzed in the detailed report include:

- Reimbursement of TAVR & TMVR Accelerating Structural Heart Uptake

- Expansion of Private Cardiology Networks Driving Premium Equipment

- MDR Recertification Backlog Delaying Product Launches

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Therapeutic and surgical devices held 57.20% of Spain cardiovascular devices market share in 2024, buoyed by coronary stents and cardiac rhythm-management implants. Concurrently, the Spain cardiovascular devices market size for diagnostic and monitoring equipment is expected to grow at 6.03% CAGR through 2030 thanks to AI-guided imaging and national funding for early detection. Advanced transcatheter tools also shorten the life cycle of older surgical devices, shifting procurement toward minimally invasive systems that shorten hospital stays. Vendors that can package modular software licenses with core hardware capture incremental revenue without proportionally higher production costs.

Diagnostic adoption is no longer confined to academic centers. Fractional flow-reserve platforms and 3D echocardiography are penetrating regional hospitals, encouraged by standardized procurement guidelines under the National Cardiovascular Health Plan. At the same time, the therapeutic segment is intensifying its focus on structural heart interventions as payers recognize the cost benefits of shorter recovery times. Hospitals that achieve lower length-of-stay metrics through device innovation often qualify for performance-based financing, bolstering demand for the latest implants.

The Spain Cardiovascular Devices Market Report is Segmented by Device Type (Diagnostic & Monitoring Devices, Therapeutic & Surgical Devices), Indication (Coronary Artery Disease, Arrhythmia, Heart Failure, Valvular Heart Disease), End User (Hospitals, Home Care Settings, Others), and Geography (Spain). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Medtronic

- Boston Scientific

- Abbott Laboratories

- Edward Lifesciences

- Koninklijke Philips

- Siemens Healthineers

- Terumo

- BIOTRONIK

- MicroPort

- LivaNova

- Cardinal Health

- B. Braun

- Meril Life Science

- Acist Medical Systems

- Getinge AB (Maquet)

- W. L. Gore & Associates

- Johnson & Johnson

- Teleflex

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 National Cardiovascular Health Plan 2022-2029 Catalyzing Device Procurement in Public Hospitals

- 4.2.2 Rapidly Ageing Spanish Population Expanding Cardiac Device Demand

- 4.2.3 Reimbursement of TAVR & TMVR Accelerating Structural Heart Device Uptake

- 4.2.4 Expansion of Private Cardiology Networks Driving High-End CRM & Imaging Equipment

- 4.2.5 Rising Funds for Digital Cardiac Tele-monitoring Platforms

- 4.3 Market Restraints

- 4.3.1 Regional Tender Price-Caps Compressing Average Selling Prices

- 4.3.2 MDR Recertification Backlog Delaying New Product Launches in Spain

- 4.3.3 Shortage of Interventional Cardiologists Outside Madrid & Catalonia Limiting Procedure Volumes

- 4.3.4 120-Day Hospital Payment Cycles Impacting Vendor Cash-Flow

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Device

- 5.1.1 Diagnostic & Monitoring Devices

- 5.1.1.1 ECG Systems

- 5.1.1.2 Remote Cardiac Monitor

- 5.1.1.3 Cardiac MRI

- 5.1.1.4 Cardiac CT

- 5.1.1.5 Echocardiography / Ultrasound

- 5.1.1.6 Fractional Flow Reserve (FFR) Systems

- 5.1.2 Therapeutic & Surgical Devices

- 5.1.2.1 Coronary Stents

- 5.1.2.1.1 Drug-Eluting Stents

- 5.1.2.1.2 Bare-Metal Stents

- 5.1.2.1.3 Bioresorbable Stents

- 5.1.2.2 Catheters

- 5.1.2.2.1 PTCA Balloon Catheters

- 5.1.2.2.2 IVUS/OCT Catheters

- 5.1.2.3 Cardiac Rhythm Management

- 5.1.2.3.1 Pacemakers

- 5.1.2.3.2 Implantable Cardioverter Defibrillators

- 5.1.2.3.3 Cardiac Resynchronization Therapy Devices

- 5.1.2.4 Heart Valves

- 5.1.2.4.1 TAVR/TAVI

- 5.1.2.4.2 Mechanical Valves

- 5.1.2.4.3 Tissue/Bioprosthetic Valves

- 5.1.2.5 Ventricular Assist Devices

- 5.1.2.6 Artificial Hearts

- 5.1.2.7 Grafts & Patches

- 5.1.2.8 Other Cardiovascular Surgical Devices

- 5.1.1 Diagnostic & Monitoring Devices

- 5.2 By Indication

- 5.2.1 Coronary Artery Disease

- 5.2.2 Arrhythmia

- 5.2.3 Heart Failure

- 5.2.4 Valvular Heart Disease

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Home care Settings

- 5.3.3 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Medtronic Plc

- 6.3.2 Boston Scientific Corporation

- 6.3.3 Abbott Laboratories

- 6.3.4 Edwards Lifesciences Corporation

- 6.3.5 Philips Healthcare

- 6.3.6 Siemens Healthineers AG

- 6.3.7 Terumo Corporation

- 6.3.8 Biotronik SE & Co. KG

- 6.3.9 MicroPort Scientific Corporation

- 6.3.10 LivaNova PLC

- 6.3.11 Cardinal Health (Cordis)

- 6.3.12 B. Braun Melsungen AG

- 6.3.13 Meril Life Sciences Pvt Ltd

- 6.3.14 Acist Medical Systems

- 6.3.15 Getinge AB (Maquet)

- 6.3.16 W. L. Gore & Associates

- 6.3.17 Johnson & Johnson (Biosense Webster)

- 6.3.18 Teleflex

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment