|

시장보고서

상품코드

1844515

병원용품 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Hospital Supplies - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

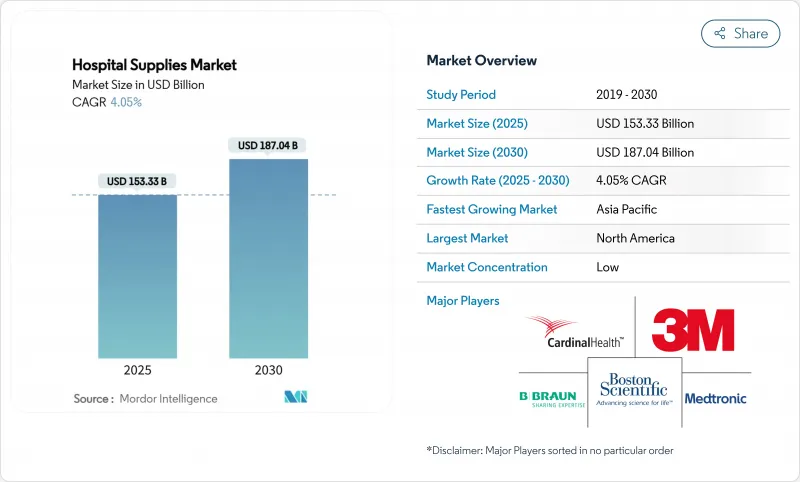

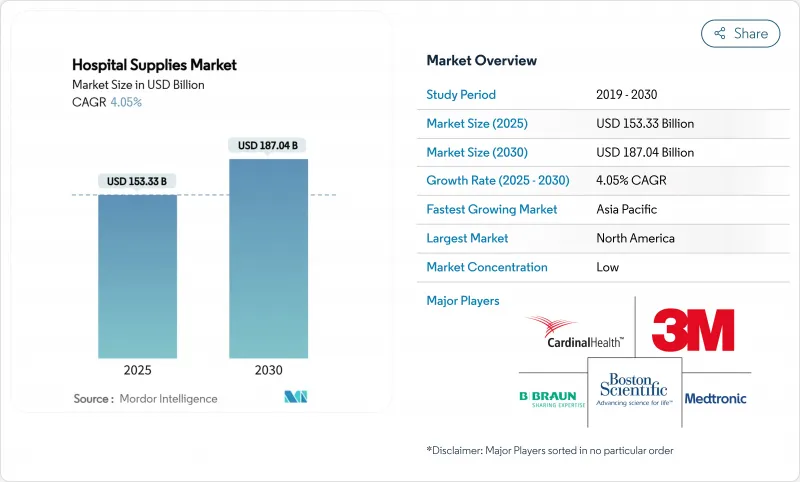

병원용품 시장 규모는 2025년에 1,533억 3,000만 달러로 평가되었고, 2030년에 1,870억 4,000만 달러에 이를 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 4.05%를 나타낼 전망입니다.

이러한 추세는 감염 관리 투자, 기술 기반 재고 시스템, 개발도상 지역의 가속화된 수요에 힘입어 유지되고 있습니다. 일회용 제품, 멸균 처리 장비, 디지털 공급망 솔루션은 여전히 구매 결정의 핵심 요소이며, 지속가능성 요구사항이 제품 선택에 영향을 미치기 시작했습니다. 아시아태평양 지역의 급속한 인프라 확장과 선진국의 팬데믹 이후 수술 대기 수요가 결합되면서 글로벌 경쟁 구도가 재편되고 있습니다. 물리적 제품과 분석 기반 효율성 도구를 결합한 공급업체들은 병원이 더 엄격한 예산 주기 내에서 임상 성과, 비용 통제, 규제 준수를 조화시키려 함에 따라 시장 점유율을 확보하고 있습니다.

세계의 병원용품 시장 동향 및 인사이트

전염성 및 만성 질환 발생률 증가

당뇨병, 심혈관 질환, 호흡기 질환 사례 증가로 인해 병원은 상처 치료 드레싱, 모니터링 키트, 인공호흡기 회로 등의 지속적인 공급을 보장하기 위해 재고 계획을 재검토해야 합니다. 당뇨병만 해도 성인 5억 3,700만 명이 영향을 받고 있으며, 2045년까지 7억 8,300만 명에 달할 것으로 예상되어 2024년 대비 특수 드레싱 사용량이 30% 증가할 전망입니다. 의료 시스템은 이제 전자 건강 기록 데이터를 예측 재고 알고리즘과 연계하여 예상 환자 수와 보충 주기 간 긴밀한 연계를 가능하게 합니다. 이러한 환자 중심 접근법은 다용도 멸균 공급품으로의 자본 배분을 유도하며, 성숙 시장과 신흥 시장 모두에서 병원용품 시장을 주도하고 있습니다.

병원 감염에 대한 대중 인식 증가

소비자들은 감염 관리 성과에 대한 인식을 바탕으로 의료기관을 선택하는 경향이 점점 더 강해지고 있습니다. 병원 감염(HAI) 한 건당 치료 비용이 28,400-33,800달러 추가 발생함에 따라, 병원 관리자들은 접촉 빈도가 높은 표면에 항균 소재를 도입하고 준수 지표를 공개하는 조치를 취하고 있습니다. 질병통제예방센터(CDC)는 입원 환자 31명 중 1명이 매일 병원 내 감염에 걸린다고 지적하며, 일회용 드레이프, 차단 가운, 자가 소독 장치 케이싱에 대한 병원용품 시장 투자를 촉진하고 있습니다. 검증 가능한 멸균 보증과 제품 추적성을 제공하는 공급업체가 경쟁 우위를 점하고 있습니다.

엄격한 규제 프레임 워크

에틸렌옥사이드 배출 억제 노력은 연간 약 200억 개의 의료 기기 멸균 경로를 위협하고 있습니다. FDA는 멸균 시설의 갑작스러운 폐쇄가 치료 연속성을 방해할 수 있다고 경고하며, 환경 정책이 병원용품 시장 물류에 미치는 파급 효과를 보여주었습니다. 기업들은 현재 대체 멸균제를 연구하고 중복 설비에 투자하며, 이미 타이트한 생산 일정에 비용과 복잡성을 더하고 있습니다.

부문 분석

일회용 병원용품은 2024년 병원용품 시장 점유율 47.21%를 유지하며 교차 오염 방지에 기여하는 역할을 강조했습니다. 묶음 수술 키트와 일회용 가운은 수술실 회전율을 높이고 세탁에 소요되는 노동력을 줄입니다. 그러나 지속가능성 정책으로 인해 선택적 재처리 및 재활용 가능 폴리머 시범 사업이 추진되면서 공급업체들은 수명 주기 배출량 공개 압박을 받고 있습니다. 멸균 및 소독 장비 부문은 중간 규모에 불과하지만 2030년까지 연평균 10.63%의 가장 빠른 성장률을 보일 전망입니다. 멸균 장비의 병원 공급 시장 규모는 장치 출하를 문서화된 미생물 사멸 기준과 연계하는 디지털 기록 관리 의무화와 함께 상승할 것으로 전망됩니다. 클라우드 기반 검증 소프트웨어를 저온 멸균기와 함께 번들로 제공하는 공급업체들은 1급 병원 시스템에서 주목받고 있습니다.

환자 검사 장치와 수술실 장비는 센서 어레이와 IoT 게이트웨이를 통합하고 있습니다. 스마트 청진기, 컴퓨터 보조 내비게이션, AI 기반 수술 중 영상 기술은 프리미엄 가격대를 주도하며, 상호운용성 점수가 구매 결정에 미치는 영향력이 커지고 있습니다. 이동 보조기 및 운반 장비는 고령화 인구 증가에 따른 압박감 완화 매트리스, 전동 호이스트, 비만 환자용 휠체어 수요 증가라는 인구통계학적 추세를 타고 있습니다. 입찰 평가 시 프레임워크에서는 초기 가격과 함께 지속가능성 인증, 예비 부품 가용성, 클라우드 지원 진단 기능이 중점적으로 고려됩니다.

지역 분석

북미의 선진 인프라와 엄격한 감염 관리 규정은 2024년 글로벌 매출의 34.34% 점유율을 확보했습니다. RFID 기반 스마트 캐비닛과 AI 지원 수요 계획 시스템의 대규모 도입은 분석 중심 가치 제안을 위한 공급업체 기회를 뒷받침합니다. 관세 불확실성이 가격 안정성을 위협하면서 카디널 헬스(Cardinal Health)와 같은 유통업체들은 2026년 병원용품 시장 탄력성에 영향을 미칠 수 있는 전가 메커니즘을 고려하게 되었습니다.

아시아태평양 지역은 중국, 인도, 동남아시아의 의료 역량 확장에 힘입어 8.29%의 연평균 성장률(CAGR)로 가장 강력한 성장을 보입니다. 3차 병원에 대한 신속한 투자와 현지 제조를 위한 정부 인센티브가 결합되면서 부품 조달이 최종 시장 가까이로 이동하고 있습니다. 병원 공급 시장의 멸균 소모품 규모는 인증 기관들이 서양의 감염 관리 기준을 채택함에 따라 급속히 증가하고 있습니다. 태국과 말레이시아의 의료 관광 성장으로 고품질이지만 비용 경쟁력 있는 일회용 제품의 조달 경로가 더욱 확대되고 있습니다.

유럽은 지속가능성 의무가 공급업체로 하여금 탄소 발자국을 검증하고 재활용 폴리머를 통합하도록 장려하며 기술 중심의 입장을 유지하고 있습니다. 독일은 물량 면에서 선두를 달리고 있으며, 스위스의 첨단 기술 틈새 시장 제조업체들은 해당 부문의 혁신을 주도하고 있습니다. 의료기기 규정(MDR)에 대한 규제 명확성은 선도적 도입 병원들이 스마트 라벨링 및 변조 방지 포장을 시범 운영하도록 장려하여 성숙한 병원 공급 시장에서 프리미엄 가격대를 유지하고 있습니다.

중동과 아프리카는 뚜렷한 차이를 보입니다. 걸프협력회의(GCC) 국가들은 최첨단 멸균실과 자동화 재고 시스템을 요구하는 플래그십 병원에 투자하고 있습니다. 한편 국제금융공사(IFC)의 아프리카 의료 장비 시설(AMEF)은 소규모 공급업체에 자금을 지원하여 동아프리카와 서아프리카 전역에 걸쳐 필수 기기에 대한 분산된 수요를 창출하고 있습니다. 교육, 유지보수, 소액 임대 방식을 묶어 제공하는 공급업체들은 가격에 민감하지만 물량이 풍부한 이러한 틈새 시장에서 입지를 넓히고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 전염성 및 만성 질환 발생률 증가

- 병원 감염에 대한 대중 인식 제고

- 개발도상국에서의 병원용품 수요 증가

- 병원 감염 관련 제재가 멸균 장비 투자 촉진

- 선진국에서 팬데믹 후 수술 건수 급증

- 정부 정책 및 의료 지출

- 시장 성장 억제요인

- 엄격한 규제 틀

- 재택치료 서비스 출현

- 첨단 기기의 높은 비용

- 공급망의 혼란

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(단위 : 달러)

- 제품별

- 환자 검사 장비

- 수술실 기기

- 이동 보조 및 운송 장비

- 멸균 및 소독 기기

- 일회용 병원용품

- 주사기 및 주사침

- 스마트 RFID 대응 소모품

- 기타 제품

- 최종 사용자별

- 공적 병원

- 사립 및 체인 병원

- 외래수술센터(ASC)

- 전문 클리닉 및 외상 센터

- 멸균성별

- 멸균 용품

- 비멸균 소모품

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- 3M

- B. Braun Melsungen AG

- Baxter International Inc.

- Becton, Dickinson and Company

- Boston Scientific Corporation

- Cardinal Health Inc.

- Medtronic

- GE HealthCare Technologies Inc.

- Johnson & Johnson

- Thermo Fisher Scientific Inc.

- Danaher Corporation

- Eurofins Scientific

- STERIS plc

- Getinge AB

- Smith Nephew Plc

- Stryker Corporation

- Terumo Corporation

- Ecolab Inc.

- HARTMANN Group

- Nipro Corporation

제7장 시장 기회와 전망

HBR 25.11.03The Hospital Supplies Market size is estimated at USD 153.33 billion in 2025, and is expected to reach USD 187.04 billion by 2030, at a CAGR of 4.05% during the forecast period (2025-2030).

This trajectory is supported by infection-control investments, technology-enabled inventory systems, and accelerating demand from developing regions. Disposable products, sterile processing equipment, and digital supply-chain solutions remain central to procurement decisions, while sustainability mandates are beginning to influence product selection. Asia-Pacific's rapid infrastructure build-out, coupled with post-pandemic surgery backlogs in developed nations, is reshaping global competitive dynamics. Suppliers that combine physical goods with analytics-driven efficiency tools are capturing share as hospitals seek to align clinical performance, cost control, and regulatory compliance within tighter budget cycles.

Global Hospital Supplies Market Trends and Insights

Increasing Incidences of Communicable and Chronic Diseases

Rising diabetes, cardiovascular, and respiratory case loads are forcing hospitals to re-think inventory plans to assure continuous availability of wound-care dressings, monitoring kits, and ventilation circuits. Diabetes alone affects 537 million adults and is projected to reach 783 million by 2045, pushing up specialized dressing use by 30% since 2024. Health systems now pair electronic health-record data with predictive stocking algorithms, enabling tighter alignment between anticipated caseloads and replenishment cycles. This patient-centric approach is steering capital allocations toward versatile sterile supplies, driving the hospital supplies market forward in both mature and emerging economies.

Growing Public Awareness about Hospital-Acquired Infections

Consumers increasingly select facilities based on perceived infection-control performance. Each HAI adds USD 28,400-33,800 in treatment costs, prompting administrators to adopt antimicrobial materials for high-touch surfaces and to publicize compliance metrics. The Centers for Disease Control and Prevention notes that 1 in 31 hospitalized patients contracts an HAI on any given day, spurring hospital supplies market investment into single-use drapes, barrier gowns, and self-disinfecting device casings. Suppliers offering verifiable sterility assurance and product traceability gain a competitive advantage.

Stringent Regulatory Framework

Efforts to curb ethylene-oxide emissions threaten the sterility pathways for roughly 20 billion medical devices annually. The FDA warned that abrupt closures of sterilization plants could disrupt care continuity, illustrating how environmental policy can ripple through hospital supplies market logistics. Firms now investigate alternative sterilants and invest in redundant capacity, adding cost and complexity to already tight production schedules.

Other drivers and restraints analyzed in the detailed report include:

- High Demand for Hospital Supplies in Developing Countries

- Hospital-Acquired Infection Penalties Catalyzing Investment in Sterilization Equipment

- Emergence of Home Care Services

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Disposable supplies retained a 47.21% hospital supplies market share in 2024, underscoring their role in combating cross-contamination. Bundled procedure packs and single-use gowns streamline operating-room turnover and reduce labor spent on laundering. However, sustainability policies have sparked pilot projects in selective re-processing and recyclable polymers, pressuring vendors to declare lifecycle emissions. Sterilization and disinfectant equipment, while only a mid-sized segment, is growing fastest at a 10.63% CAGR to 2030. The hospital supplies market size for sterilization equipment is forecast to climb in tandem with digital record-keeping mandates that tie device release to documented microbial kill parameters. Suppliers that bundle cloud-based validation software with low-temperature sterilizers see traction in tier-1 hospital systems.

Patient examination devices and operating-room equipment are integrating sensor arrays and IoT gateways. Smart stethoscopes, computer-assisted navigation, and AI-driven intraoperative imaging drive premium pricing tiers, with procurement decisions increasingly influenced by interoperability scores. Mobility aids and transportation equipment ride demographic trends as aging populations demand pressure-reducing mattresses, electric hoists, and bariatric wheelchairs. Sustainability credentials, spare-parts availability, and cloud-ready diagnostics are now weighted alongside upfront price when frameworks evaluate bids.

The Hospital Supplies Market Report is Segmented by Product (Patient Examination Devices, Operating Room Equipment, Mobility Aids and Transportation Equipment, and More), End User (Public Hospitals, Private & Chain Hospitals, and More), Sterility (Sterile Supplies, Non-Sterile Supplies), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's advanced infrastructure and strict infection-control mandates secured 34.34% share of global revenue in 2024. Large-scale adoption of RFID-enabled smart cabinets and AI-assisted demand-planning systems underpins supplier opportunities for analytics-rich value propositions. Tariff uncertainties threatened price stability, prompting distributors like Cardinal Health to consider pass-through mechanisms that could influence hospital supplies market elasticity in 2026.

Asia-Pacific delivers the strongest growth at an 8.29% CAGR, driven by healthcare capacity expansion in China, India, and Southeast Asia. Rapid investment in tertiary hospitals, coupled with government incentives for local manufacturing, shifts component sourcing closer to end-markets. The hospital supplies market size for sterilization consumables is rising briskly as accreditation bodies adopt Western infection-control benchmarks. Medical tourism growth in Thailand and Malaysia further widens procurement pipelines for high-quality but cost-competitive disposables.

Europe maintains a technology-oriented stance, with sustainability mandates encouraging suppliers to validate carbon footprints and integrate recycled polymers. Germany leads by volume, while Switzerland's high-tech niche manufactures propel segment innovation. Regulatory clarity around the Medical Device Regulation (MDR) encourages early-adopter hospitals to pilot smart labeling and tamper-evident packaging, sustaining premium price points in a mature hospital supplies market.

The Middle East and Africa witness marked divergence. Gulf Cooperation Council nations invest in flagship hospitals that demand state-of-the-art sterilization suites and automated inventory systems. Meanwhile, the International Finance Corporation's Africa Medical Equipment Facility funds small providers, creating distributed demand for essential devices across East and West Africa. Suppliers that bundle training, maintenance, and micro-leasing schemes gain traction in these price-sensitive yet volume-rich niches.

- 3M

- B. Braun

- Baxter

- Beckton Dickinson

- Boston Scientific

- Cardinal Health

- Medtronic

- GE HealthCare Technologies Inc.

- Johnson & Johnson

- Thermo Fisher Scientific

- Danaher

- Eurofins

- STERIS

- Getinge

- Smith+Nephew Plc

- Stryker

- Terumo

- Ecolab

- HARTMANN Group

- Nipro

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidences of Communicable and Chronic Diseases

- 4.2.2 Growing Public Awareness about Hospital Acquired Infections

- 4.2.3 High Demand for Hospital Supplies in Developing Countries

- 4.2.4 Hospital-Acquired Infection Penalties Catalyzing Investment in Sterilization Equipment

- 4.2.5 Surge in Surgical Volume Post-Pandemic in Developed Countries

- 4.2.6 Government Initiatives and Healthcare Spending

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Framework

- 4.3.2 Emergence of Home Care Services

- 4.3.3 High Costs of Advanced Equipment

- 4.3.4 Supply Chain Disruptions

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product

- 5.1.1 Patient Examination Devices

- 5.1.2 Operating Room Equipment

- 5.1.3 Mobility Aids & Transportation Equipment

- 5.1.4 Sterilization & Disinfectant Equipment

- 5.1.5 Disposable Hospital Supplies

- 5.1.6 Syringes & Needles

- 5.1.7 Smart RFID-Enabled Consumables

- 5.1.8 Other Products

- 5.2 By End User

- 5.2.1 Public Hospitals

- 5.2.2 Private & Chain Hospitals

- 5.2.3 Ambulatory Surgical Centers

- 5.2.4 Specialty Clinics & Trauma Centers

- 5.3 By Sterility

- 5.3.1 Sterile Supplies

- 5.3.2 Non-Sterile Supplies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 3M

- 6.3.2 B. Braun Melsungen AG

- 6.3.3 Baxter International Inc.

- 6.3.4 Becton, Dickinson and Company

- 6.3.5 Boston Scientific Corporation

- 6.3.6 Cardinal Health Inc.

- 6.3.7 Medtronic

- 6.3.8 GE HealthCare Technologies Inc.

- 6.3.9 Johnson & Johnson

- 6.3.10 Thermo Fisher Scientific Inc.

- 6.3.11 Danaher Corporation

- 6.3.12 Eurofins Scientific

- 6.3.13 STERIS plc

- 6.3.14 Getinge AB

- 6.3.15 Smith+Nephew Plc

- 6.3.16 Stryker Corporation

- 6.3.17 Terumo Corporation

- 6.3.18 Ecolab Inc.

- 6.3.19 HARTMANN Group

- 6.3.20 Nipro Corporation