|

시장보고서

상품코드

1851267

스페인의 병원 용품 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Spain Hospital Supplies - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

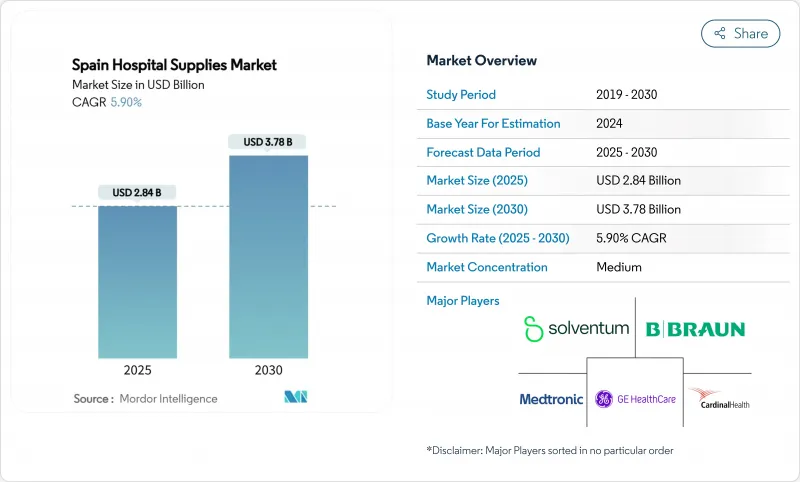

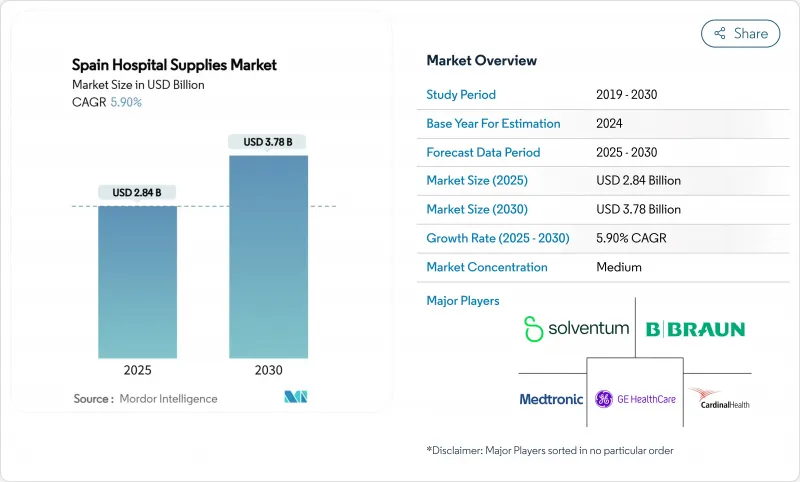

스페인의 병원 용품 시장 규모는 2025년에 28억 4,000만 달러로 추정되고, 2030년에는 37억 8,000만 달러에 이를 것으로 예측됩니다.

스페인의 견고한 공공 부문의 기반은 재건 및 회복 시설(Recovery and Resilience Facility)에 대한 적극적인 투자와 함께 다른 유럽의 헬스케어 시스템이 더 큰 변동을 보이는 동안 이 일관된 궤도를 지원합니다. 평균 수명 증가, 90세 이상 인구층의 급격한 확대, 감염 예방 기준의 엄격화에 의해 기기의 갱신 사이클이 강화되는 한편, 디지털 조달의 의무화에 의해 주문의 이행이 가속하고 있습니다. 세계 다국적 기업과 국내 전문가들은 가치, 컴플라이언스 지원, 신속한 물류와 경쟁하고 균형 잡힌 상태에서도 역동적인 경쟁을 창출하고 있습니다. 의료기기 규제(MDR)와 유럽 의료 데이터 공간을 통한 EU의 지속적인 조화는 표준화의 이점과 컴플라이언스 비용 증가를 촉진합니다.

스페인의 병원 용품 시장 동향 및 인사이트

전염병 및 만성질환 발생률 증가

감시 데이터에 따르면, EU 병원 환자의 7.1%가 의료 관련 감염을 경험했으며, 그 중 가장 중요한 것은 호흡기 질환입니다. 스페인의 국민 모두 보험제도는 이러한 사례에 대한 치료를 보증하고 있어 진단 키트, 멸균 소모품, 호흡기 서포트 기기의 예측 가능한 대량 조달로 이어지고 있습니다. 2024년 국민 모두 보험법안은 일시 체류자 및 망명 희망자에게도 적용 범위를 확대해 수혜자층을 확대했습니다. 병원이 만성기 의료 및 감염 통제 경로를 통합함에 따라 공급업체는 소모품 및 자동 멸균 장치를 결합한 대량 입찰의 혜택을 받으며 분석 장비는 입원 환자와 외래 환자를 가로지르는 종단적인 질병 관리를 지원합니다.

증가하는 원내 감염에 대한 인식

EU 전역에서 연간 추정 350만 명의 HAI 환자와 9만 명 이상의 관련 사망이 발생하고 있으며, 그 절반까지는 감염 관리의 강화에 의해 예방 가능합니다. 스페인 병원은 MDR 시판 후 감시 규칙에 따른 CE 마크가 붙은 일회용 기기 및 트레이서블 멸균 시스템을 선호하여 사용함으로써 대응하고 있습니다. 입찰 사양서에서는 항균 표면이나 폐쇄계 약제 이송 솔루션에 대한 언급이 늘어나 ISO에 준거한 클린 룸 제조의 인증을 취득한 벤더에게 보상금을 지불하게 되어 있습니다. 조달 팀이 아웃 브레이크 봉쇄 비용과 선행 제품의 프리미엄을 비교하고 정량화함에 따라 감염 제어 포트폴리오는 전략적 가중치를 늘리고 있습니다.

엄격한 규제 프레임워크

MDR은 2024년 5월까지 레거시 장치를 최신 품질 관리 기준에 적합하도록 의무화하고 있지만, 이행 유예 기간은 2028년 12월까지입니다. 스페인 AEMPS는 또한 모든 의료기기의 국내 등록을 의무화하고, 규칙(EU) 2024/1860에 따라 공급 중단 통지를 의무화하고 있습니다. 소규모 제조업체는 위험 기반 분류, 독특한 장비 식별 라벨, 정기적 안전 업데이트 보고서에 대한 높은 컴플라이언스 비용에 직면하고 있습니다. 그 결과, 유통업체는 MDR 승인 제품을 중심으로 포트폴리오를 통합하여 브랜드 선택을 좁히고 혁신적인 중소기업 시장 진출 일정을 장기화할 수 있습니다.

부문 분석

일회용 병원 용품은 2024년 스페인 병원 용품 시장 점유율의 45.51%를 차지했는데, 이는 일회용 안전 프로토콜이 근본적으로 중시되고 있음을 반영합니다. 멸균 및 소독 기기는 2030년까지 CAGR 7.65%로 성장할 전망이며, HAI에 대한 의식의 고조 및 MDR 추적 가능성 룰로부터 이익을 얻고 있습니다. 멸균 시스템의 스페인 병원 용품 시장 규모는 병원이 열에 약한 장비를 보호하는 저온 및 과산화수소 장비로 업그레이드됨에 따라 꾸준히 확대될 것으로 예측됩니다.

수술실 장비 및 진단 장비는 계속 부흥 계획 보조금과 관련된 예산 배분을 받고, 주사기와 주사 바늘의 사양은 실리콘 오일 비말에 대한 안과의 안전 경고를 받아 진화하고 있습니다. 잔량이 0인 CE 마크가 달린 마이크로볼륨 주사기 공급업체는 틈새 시장이지만 고가치 주문을 획득하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 감염증 및 만성질환 증가

- 원내 감염에 대한 의식의 고조

- 스페인 인구의 급속한 고령화

- 디지털화가 가속하는 공공 조달

- EU의 RRF 자금에 의한 병원 인프라의 현대화

- 국내 단일 용도 플라스틱의 능력 증강

- 시장 성장 억제요인

- 엄격한 규제 프레임워크

- 재택 간병 서비스에 대한 시프트

- EU 플라스틱세에 의한 투입 비용 변동

- 세분화된 지역 예산 조달 사이클

- 공급망 분석

- 규제 상황

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품별

- 환자 검사 장비

- 수술실 설비

- 이동 보조기구 및 수송 기기

- 멸균 및 소독 기기

- 일회용 병원 용품

- 주사기 및 주사 바늘

- 기타 제품

- 최종 사용자 시설별

- 공립 병원

- 민간 병원

- 전문 클리닉

- 진단 및 이미지 센터

- 유통 채널별

- 직접 입찰

- 단체 구입 조직(GPOs)

- 온라인 B2B 플랫폼

- 소매 및 지역 약국

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Solventum Corporation

- B. Braun SE

- Baxter International Inc.

- Becton, Dickinson and Company

- Cardinal Health Inc.

- Medtronic plc

- GE HealthCare Technologies Inc.

- Thermo Fisher Scientific Inc.

- Johnson & Johnson(Ethicon, DePuy)

- Fresenius Medical Care AG & Co. KGaA

- Grifols SA

- Werfen

- Palex Medical

- Izasa Medical

- Smith & Nephew plc

- Stryker Corporation

- Dragerwerk AG & Co. KGaA

- Siemens Healthineers AG

- Olympus Corporation

- Terumo Corporation

제7장 시장 기회 및 향후 전망

AJY 25.11.21The Spain hospital supplies market size reached USD 2.84 billion in 2025 and is forecast to climb to USD 3.78 billion by 2030, translating into a 5.90% CAGR over the period.

Spain's solid public-sector foundation, together with targeted Recovery and Resilience Facility investments, underpins this consistent trajectory even as other European healthcare systems show greater volatility. Rising life expectancy, a sharply expanding population segment aged 90 years and above, and stricter infection-prevention standards reinforce equipment renewal cycles, while digital procurement mandates accelerate order fulfilment. Global multinationals and domestic specialists compete on value, compliance support and rapid logistics, creating a balanced yet dynamic competitive field. Continued EU harmonisation through the Medical Device Regulation (MDR) and the European Health Data Space is driving both standardisation benefits and added compliance costs.

Spain Hospital Supplies Market Trends and Insights

Rising Incidence of Infectious & Chronic Diseases

Surveillance data show that 7.1% of EU hospital patients experience healthcare-associated infections, with respiratory conditions at the forefront. Spain's universal health system guarantees treatment for those cases, translating into predictable bulk procurement of diagnostic kits, sterile consumables and respiratory support devices. The 2024 Universal Health-Care Bill extended coverage to temporary residents and asylum seekers, widening the beneficiary pool. As hospitals integrate chronic-care and infection-control pathways, suppliers benefit from bundled tenders that combine disposables with automated sterilisation units, while analytics-enabled devices support longitudinal disease management across inpatient and outpatient settings.

Growing Awareness of Hospital-Acquired Infections

An estimated 3.5 million HAI cases and more than 90,000 related deaths occur annually across the EU, up to half of which are preventable through stronger infection-control practices. Spanish hospitals respond by favouring CE-marked single-use devices and traceable sterilisation systems that comply with MDR post-market surveillance rules. Tender specifications increasingly reference antimicrobial surfaces and closed-system drug-transfer solutions, rewarding vendors that certify ISO-compliant clean-room manufacturing. As procurement teams quantify the cost of outbreak containment versus up-front product premiums, infection-control portfolios gain strategic weight.

Stringent Regulatory Framework

The MDR requires legacy devices to align with updated quality-management standards by May 2024, while transitional grace periods run no later than December 2028. Spain's AEMPS further obliges in-country registration of all medical devices and mandates supply-interruption notifications under Regulation (EU) 2024/1860. Smaller manufacturers face high compliance costs for risk-based classification, unique-device identification labelling and periodic safety-update reports. Consequently, distributors consolidate their portfolios around MDR-approved products, potentially narrowing brand choice and lengthening market-entry timelines for innovative SMEs.

Other drivers and restraints analyzed in the detailed report include:

- Rapidly Ageing Spanish Population

- Digitalised Public Procurement Accelerating Fulfilment

- Shift Toward Home-Care Services

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Disposable hospital supplies accounted for 45.51% of Spain hospital supplies market share in 2024, reflecting persistent emphasis on single-use safety protocols. Sterilisation and disinfection equipment, posting a 7.65% CAGR to 2030, benefits from rising HAI awareness and MDR traceability rules. The Spain hospital supplies market size for sterilisation systems is projected to expand steadily as hospitals upgrade to low-temperature and hydrogen-peroxide units that protect heat-sensitive devices.

Operating-room equipment and diagnostic instruments continue to receive budget allocations tied to Recovery Plan grants, while syringe and needle specifications evolve following ophthalmology safety alerts on silicone-oil droplets. Suppliers of CE-marked micro-volume syringes with zero residual volume capture niche but high-value orders.

The Spain Hospital Supplies Market is Segmented by Product (Patient Examination Devices, Operating Room Equipment, Mobility Aids and Transportation Equipment, Sterilisation & Disinfection Equipment, and More), End-User Facility (Public Hospitals, Private Hospitals, and More), Distribution Channel (Direct Public Tenders, Online B2B Platforms, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Solventum Corporation

- B. Braun

- Baxter

- Beckton Dickinson

- Cardinal Health

- Medtronic

- GE HealthCare Technologies Inc.

- Thermo Fisher Scientific

- Johnson & Johnson (Ethicon, DePuy)

- Fresenius

- Grifols

- Werfen

- Palex Medical

- Izasa Medical

- Smiths Group

- Stryker

- Dragerwerk

- Siemens Healthineers

- Olympus

- Terumo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence Of Infectious & Chronic Diseases

- 4.2.2 Growing Awareness Of Hospital-Acquired Infections

- 4.2.3 Rapidly Ageing Spanish Population

- 4.2.4 Digitalised Public Procurement Accelerating Fulfilment

- 4.2.5 EU RRF Funds Modernising Hospital Infrastructure

- 4.2.6 Domestic Single-Use Plastics Capacity Expansions

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Framework

- 4.3.2 Shift Toward Home-Care Services

- 4.3.3 EU Plastic-Tax Driven Input-Cost Volatility

- 4.3.4 Fragmented Regional-Budget Procurement Cycles

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Patient Examination Devices

- 5.1.2 Operating-Room Equipment

- 5.1.3 Mobility Aids & Transport Equipment

- 5.1.4 Sterilisation & Disinfection Equipment

- 5.1.5 Disposable Hospital Supplies

- 5.1.6 Syringes & Needles

- 5.1.7 Other Products

- 5.2 By End-User Facility

- 5.2.1 Public Hospitals

- 5.2.2 Private Hospitals

- 5.2.3 Specialised Clinics

- 5.2.4 Diagnostic & Imaging Centres

- 5.3 By Distribution Channel

- 5.3.1 Direct Public Tenders

- 5.3.2 Group-Purchasing Organisations (GPOs)

- 5.3.3 Online B2B Platforms

- 5.3.4 Retail & Community Pharmacies

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Solventum Corporation

- 6.3.2 B. Braun SE

- 6.3.3 Baxter International Inc.

- 6.3.4 Becton, Dickinson and Company

- 6.3.5 Cardinal Health Inc.

- 6.3.6 Medtronic plc

- 6.3.7 GE HealthCare Technologies Inc.

- 6.3.8 Thermo Fisher Scientific Inc.

- 6.3.9 Johnson & Johnson (Ethicon, DePuy)

- 6.3.10 Fresenius Medical Care AG & Co. KGaA

- 6.3.11 Grifols S.A.

- 6.3.12 Werfen

- 6.3.13 Palex Medical

- 6.3.14 Izasa Medical

- 6.3.15 Smith & Nephew plc

- 6.3.16 Stryker Corporation

- 6.3.17 Dragerwerk AG & Co. KGaA

- 6.3.18 Siemens Healthineers AG

- 6.3.19 Olympus Corporation

- 6.3.20 Terumo Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment