|

시장보고서

상품코드

1844547

무선 재실감지 센서 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Wireless Occupancy Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

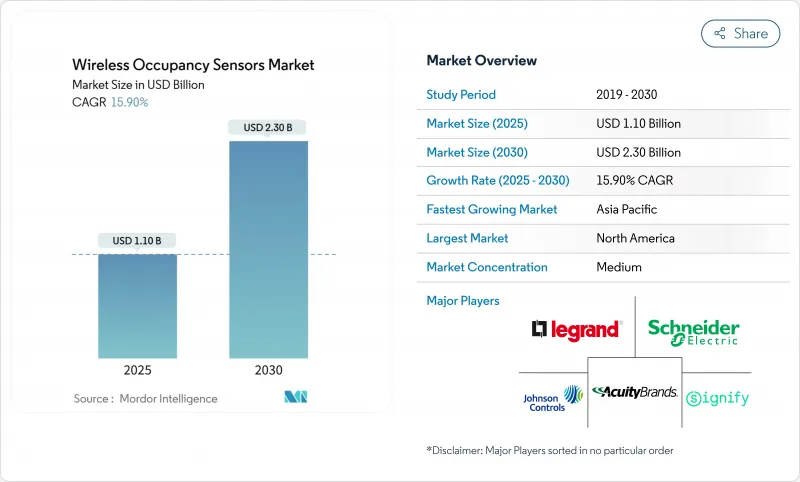

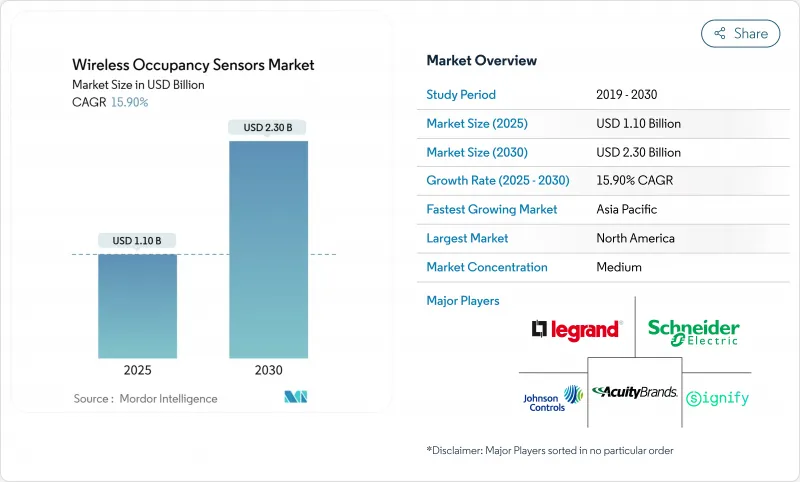

무선 재실감지 센서 시장 규모는 2025년에 11억 달러로 평가되었고, CAGR 15.9%를 나타낼 것으로 예측되며, 2030년에 23억 달러로 성장할 전망입니다.

스마트 빌딩 플랫폼에 대한 투자 급증, 에너지 효율 규제의 강화, 배터리 없는 에너지 수확 설계의 급속한 발전이 이러한 추세의 주요 동력입니다. 공급업체들은 오작동을 줄이고 감지 정확도를 높이는 AI 기반 센서 융합 알고리즘을 내장하고 있으며, 건물 소유주들은 운동 에너지, 태양열, 열 에너지 수확기가 제공하는 유지보수 감소 효과를 높이 평가합니다. 조명 업계 주요 기업들이 데이터 상호운용성 우위를 확보하기 위해 전문 센서 제조사들을 인수하면서 경쟁이 심화되고 있으며, 지역별 성장 양상은 규제 강도와 밀접한 관련이 있습니다. 북미는 ASHRAE 90.1-2019 및 캘리포니아 타이틀 24 요건의 혜택을 받는 반면, 아시아태평양 지역은 중국의 지능형 건물 의무화 정책과 일본의 에너지 효율 IoT 프로그램을 활용하고 있습니다. 이러한 수렴 요인들은 개조 및 그린필드 프로젝트의 강력한 파이프라인을 창출하여 무선 재실 센서 시장을 10년 동안 두 자릿수 성장 궤도에 유지할 것입니다.

세계의 무선 재실감지 센서 시장 동향 및 인사이트

엄격한 에너지 효율 의무화

유럽연합의 ‘건물 에너지 성능 지침’ 및 캘리포니아 타이틀 24와 같은 에너지 규정은 자동 조명 및 HVAC 제어를 요구하여 무선 재실감지 시장 솔루션에 대한 장기적 수요를 공고히 합니다. 뉴욕시의 로컬 로 88은 미준수 시 재정적 제재를 추가하여 단순한 투자 회수 계산 이상의 규제적 견인력을 확고히 합니다. 제조업체들은 EU에서는 5년마다, 미국 여러 주에서는 3년마다 예측 가능한 업등급 주기를 확인하며 지속적인 연구개발 투자를 장려합니다. 이러한 규제는 이전에 자동화를 선택 사항으로 여겼던 중소 규모 건물에서의 개조 작업도 촉진합니다. 종합적으로 이러한 조치들은 프로젝트 파이프라인을 가속화하여 예측 연평균 성장률(CAGR)에 3.2% 포인트를 추가합니다.

스마트 빌딩과 IoT의 급속한 보급

Cisco Spaces, Schneider Electric EcoStruxure와 같은 스마트 빌딩 플랫폼은 실시간 점유 데이터를 통합해 HVAC, 조명, 유지보수를 자동화하며, 센서를 단일 기능 장치에서 기업 분석에 데이터를 공급하는 데이터 노드로 전환합니다. Thread 및 Matter 프로토콜은 이제 상호운용성 문제를 해소하여 Bluetooth, Zigbee, Wi-Fi 장치가 독점 게이트웨이 없이도 공존할 수 있게 합니다. 아카라(Aqara)와 같은 벤더들은 애플 홈(Apple Home), 알렉사(Alexa), 구글(Google) 생태계에 즉시 연결되는 듀얼 PIR 및 mmWave 센서를 출시하여 소비자 접근성을 확대하고 있습니다. 이러한 네트워크 효과는 특히 아시아태평양 지역의 신규 상업 건물에서 더 빠른 도입 곡선을 이끌고 있습니다. 결과적으로 스마트 빌딩 보급률은 무선 재실감지 시장 CAGR에 4.1%포인트라는 가장 높은 상승 요인을 제공할 것입니다.

오작동 및 보정 문제

기존 PIR 센서는 HVAC 기류와 온도 변동을 잘못 감지하여 사람이 없는데도 조명이 켜지고 에너지 절감 효과를 저해합니다. 초음파 비행시간(TOF) 방식은 이러한 환경에서 감지 성능을 개선하지만, 설치자가 감도를 미세 조정해야 하여 인건비가 증가합니다. 듀얼 기술 융합은 오작동을 줄이지만 부품 수와 배터리 소모량을 두 배로 증가시킵니다. 고급 mmWave 레이더는 여전히 고가이며, 많은 전기 기술자에게 생소한 숙련된 설정이 필요합니다. AI 지원 자동 보정 표준이 성숙해질 때까지 이러한 기술적 마찰은 무선 재실감지 시장 CAGR에서 2.1% 포인트를 감소시킵니다.

부문 분석

저비용과 성숙도로 인해 수동 적외선(PIR) 센서는 2024년 46% 점유율을 유지하며 무선 재실감지 시장의 주력 제품으로 자리매김했습니다. PIR과 초음파 신호를 결합한 듀얼 테크(Dual-Tech) 장치는 에어컨이 가동되는 개방형 사무실에서 사용자들이 더 높은 정밀도를 요구함에 따라 20.5%의 CAGR을 기록할 것으로 전망됩니다. 초음파 단독 센서는 안정적인 온도 환경에서 음파 기반 동작 감지가 유리한 2위 자리를 차지했습니다. mmWave 레이더는 중요한 조명 및 HVAC 결정을 위해 1초 미만의 존재 확인이 필요한 의료, 공항, 프리미엄 오피스 구매자들의 관심을 끌고 있습니다. 컴퓨터 비전 및 음향 변형 제품은 여전히 틈새 시장이지만 소매 분석에서 인원 계수 정확도로 주목받고 있습니다.

공급업체 로드맵은 환경 패턴을 학습하여 오탐을 줄이는 AI 융합 엔진을 점점 더 많이 통합하여 무선 재실감지 시장에 대한 신뢰도를 높이고 있습니다. 아카라(Aqara)의 FP300은 이중 PIR, 밀리미터파, 온도, 습도, 조도 감지 기능을 결합해 명령 데이터를 매터(Matter) 네트워크로 전송합니다. 이러한 플랫폼은 무선 업데이트를 활용해 알고리즘 발전에 따른 투자 보호를 제공합니다. BOM 비용은 상승하지만, 수리 요청 감소로 인한 수명 주기 절감 효과가 프리미엄 가격을 정당화하며 대규모 기업 도입의 발판을 마련합니다.

조명 제어는 2024년에도 59%의 매출 점유율을 유지하며 상업 시설의 수십 년간 지속된 규정 기반 구축의 혜택을 누렸습니다. 그러나 HVAC 및 환기 시장은 19%의 연평균 성장률(CAGR)로 확장될 전망입니다. 팬데믹 이후 실내 공기질 기준에 맞춰 공기 흐름을 적정화하는 데 점유율 데이터가 필수적임이 입증되었기 때문입니다. 보안 및 감시 분야는 경보 작동 및 대피 경로 조명에 센서를 활용하여 예산 간 시너지를 제공합니다. 가장 높은 가치는 공간 활용도 분석에서 발생하는데, 고급 계수 기능이 프리미엄 부동산의 임대료 최적화를 가능하게 합니다.

허니웰의 포지 서스테이너빌리티+(Forge Sustainability+)는 점유율에 맞춰 조정된 HVAC가 쾌적성을 유지하면서 팬 에너지를 40% 절감할 수 있음을 보여줌으로써, 에너지 계약과 연계된 무선 점유율 센서 시장 규모에 새로운 ROI 레버를 제공합니다. 공급업체들은 하드웨어 마진을 넘어 데이터 구독을 수익화하는 클라우드 대시보드를 패키지화합니다. 자산 추적 오버레이는 동일한 인프라를 활용하여 시설 관리자에게 추가 자본 지출 없이 TAM을 확대하는 다중 서비스 플랫폼을 제공합니다.

지역 분석

북미는 2024년 매출 점유율 35%로 선두를 달렸으며, 이는 사실상 모든 상업 프로젝트에 센서 설치를 의무화하는 ASHRAE 90.1-2019 및 Title 24 규정의 영향입니다. 미국은 밀리미터파 레이더 연구개발을 주도하며, Novelda와 같은 기업들이 환자실 애플리케이션을 위한 미세 동작 추적이 가능한 초광대역 감지기를 공급하고 있습니다. 캐나다의 LEED 중심 개조 추진과 멕시코의 공장 확장은 간헐적인 무역 정책 불확실성에도 불구하고 지역 물량을 유지하고 있습니다. 무선 재실감지 시장은 에너지 효율 장비 업등급에 대한 연방 세제 혜택으로 계속해서 혜택을 보고 있습니다.

아시아태평양 지역은 가장 빠르게 성장하는 시장으로, 중국의 스마트시티 청사진과 일본의 제로에너지빌딩 목표가 센서 보급률을 높이며 연평균 17.8%의 성장률을 기록할 전망입니다. 인도의 100개 스마트시티 사업과 광범위한 5G 구축은 상업용 타워에 BLE 기반 설치가 확산될 토대를 마련했습니다. 한국은 전자제품 제조 역량을 활용해 납기 단축과 시스템 가격 인하를 실현하며 교육 및 의료 분야의 도입을 주도하고 있습니다. 풍부한 현지 부품 공급망은 글로벌 반도체 부족 사태로부터 지역을 보호하며 무선 재실감지 시장 성장 궤도를 공고히 합니다.

유럽은 건물 에너지 성능 지침(EPBD)의 혜택을 받으며, 이 지침은 주기적 성능 감사를 의무화해 지속적인 리모델링 사이클을 촉진합니다. 독일은 산업 자동화 시너지에서 두각을 나타내는 반면, 영국은 탄소 감축 기금을 공공 부문 리모델링 보조금으로 전환합니다. 프랑스는 수요 대응에 대한 보상을 건물에 지급하는 스마트 그리드-빌딩 간 데이터 교환을 탐구하여 센서를 규정 준수 비용이 아닌 수익 창출 자산으로 전환합니다. GDPR은 구매자를 에지 처리 솔루션으로 유도하여 기기 내 분석 기능을 보유한 공급업체를 선호하게 합니다. 이러한 요소들이 결합되어 무선 센서는 유럽의 탈탄소화 로드맵의 기초 요소로 자리매김합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 엄격한 에너지 효율 의무화

- 스마트 빌딩과 IoT의 급속한 보급

- 배터리가 필요없는 에너지 수확 센서

- 하이브리드 워크에 의한 공간 분석 수요

- ESG와 연동한 점유율 기반 HVAC 계약

- 제로 레이턴시 감지를 위한 AI 기반 mmWave 융합

- 시장 성장 억제요인

- 오작동 및 보정 문제

- 데이터 프라이버시와 사이버 보안에 대한 우려

- 고밀도 IoT 배포 환경에서의 RF 혼잡

- 배터리 폐기 규정 준수 비용

- 가치 및 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모와 성장 예측

- 기술별

- 패시브 적외선(PIR)

- 초음파

- 듀얼 테크놀로지(PIR+초음파)

- 마이크로파, 밀리파 레이더

- 기타 기술

- 용도별

- 조명 제어

- 에어컨, 환기

- 보안 및 모니터링

- 공간 이용 분석

- 기타 용도

- 건물 유형별

- 주거

- 상업

- 산업

- 공공시설

- 네트워크 접속별

- Zigbee

- Bluetooth/BLE

- Wi-Fi

- EnOcean(에너지 수확)

- LoRa 및 기타 LPWAN

- 최종 사용자 산업별

- 스마트 빌딩

- 의료시설

- 제조업

- 항공우주 및 방위

- 가전 및 스마트 홈

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장의 집중

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- Legrand SA

- Schneider Electric SE

- Acuity Brands Inc.

- Eaton Corporation plc

- Leviton Manufacturing Co. Inc.

- Johnson Controls International plc

- Signify NV

- Lutron Electronics Co. Inc.

- Honeywell International Inc.

- General Electric Co.

- Hubbell Incorporated

- ABB Ltd.

- Siemens AG

- Texas Instruments Inc.

- Crestron Electronics Inc.

- Enlighted Inc.(Siemens)

- RAB Lighting Inc.

- Autani LLC

- PointGrab Ltd.

- Delta Electronics Inc.

제7장 시장 기회와 전망

HBR 25.11.03The wireless occupancy sensors market size reached USD 1.1 billion in 2025 and is forecast to climb to USD 2.3 billion by 2030, advancing at a 15.9% CAGR.

Surging investment in smart-building platforms, tightening energy-efficiency regulations, and rapid advances in battery-free energy-harvesting designs are the primary engines behind this momentum. Vendors are embedding AI-enabled sensor-fusion algorithms that cut false triggers and raise detection accuracy, while building owners value the reduced maintenance that kinetic, solar, and thermal harvesters provide. Competition is intensifying as lighting majors buy specialist sensor makers to gain data-interoperability advantages, and regional growth profiles mirror regulatory rigor-North America benefits from ASHRAE 90.1-2019 and California Title 24 requirements, whereas Asia-Pacific leverages China's intelligent-building mandate and Japan's energy-efficient IoT programs. These converging factors are creating a robust pipeline of retrofit and greenfield projects that will keep the wireless occupancy sensors market on a double-digit growth path through the decade.

Global Wireless Occupancy Sensors Market Trends and Insights

Stringent Energy-Efficiency Mandates

Energy codes such as the European Union's Energy Performance of Buildings Directive and California Title 24 require automatic lighting and HVAC controls, anchoring long-term demand for wireless occupancy sensors market solutions. New York City's Local Law 88 adds financial penalties for non-compliance, cementing a regulatory pull that transcends simple payback calculations. Manufacturers see predictable upgrade cycles every five years in the EU and every three years in several U.S. states, which encourages sustained R&D spending. The mandates also catalyze retrofits in small and midsize buildings that previously viewed automation as discretionary. Collectively, these measures add 3.2 percentage points to the forecast CAGR by accelerating project pipelines.

Rapid Smart-Building & IoT Adoption

Smart-building platforms such as Cisco Spaces and Schneider Electric EcoStruxure integrate real-time occupancy data to automate HVAC, lighting, and maintenance, transforming sensors from single-function devices into data nodes that feed enterprise analytics. Thread and Matter protocols now remove interoperability headaches, letting Bluetooth, Zigbee, and Wi-Fi devices coexist without proprietary gateways. Vendors like Aqara ship dual PIR and mmWave sensors that join Apple Home, Alexa, and Google ecosystems out of the box, widening consumer reach. These network effects drive faster adoption curves, particularly in Asia-Pacific's new commercial builds. As a result, smart-building penetration will deliver the highest driver uplift at 4.1 percentage points to the wireless occupancy sensors market CAGR.

False Triggering & Calibration Issues

Conventional PIR sensors misread HVAC drafts and temperature swings, causing lights to turn on without occupants and eroding energy-savings claims. Ultrasonic Time-of-Flight devices improve detection in such environments, but installers must fine-tune sensitivity, boosting labor costs. Dual-tech fusion reduces false positives yet doubles component count and battery drain. Premium mmWave radar remains costly and needs skilled setup unfamiliar to many electricians. Until AI-assisted auto-calibration standards mature, these technical frictions subtract 2.1 percentage points from the wireless occupancy sensors market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Battery-Free Energy-Harvesting Sensors

- Hybrid-Work Demand for Space Analytics

- Data-Privacy & Cybersecurity Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passive Infrared maintained 46% share in 2024 thanks to low cost and maturity, positioning it as the volume anchor of the wireless occupancy sensors market. Dual-Tech devices that blend PIR and ultrasonic signals are projected to post a 20.5% CAGR as users demand higher precision in air-conditioned open offices. Ultrasonic standalone sensors hold the runner-up slot where stable temperatures favor sound-based motion detection. mmWave radar attracts healthcare, airport, and premium office buyers that need sub-second presence confirmation for critical lighting and HVAC decisions. Computer-vision and acoustic variants remain niche yet gain attention for people-counting accuracy in retail analytics.

Vendor roadmaps increasingly bundle AI fusion engines that learn environmental patterns to slash false positives, improving confidence in the wireless occupancy sensors market. Aqara's FP300 combines dual PIR, mmWave, temperature, humidity, and illuminance sensing to feed command data into Matter networks. Such platforms use over-the-air updates, protecting investment as algorithms evolve. While BOM costs rise, lifecycle savings from reduced callbacks justify the premium, setting the stage for larger enterprise rollouts.

Lighting Control retained 59% revenue dominance in 2024, benefiting from decades of code-driven deployment in commercial fit-outs. Yet HVAC & Ventilation is forecast to expand at a 19% CAGR, as occupancy data proves essential for right-sizing airflow to post-pandemic indoor-air-quality standards. Security & Surveillance uses sensors for alarm arming and egress path lighting, offering cross-budget synergies. The highest value accrues to Space-Utilization Analytics, where advanced counting functions enable rent optimization in premium real estate.

Honeywell's Forge Sustainability+ illustrates how occupancy-tuned HVAC can reduce fan energy by 40% while maintaining comfort, unlocking new ROI levers for the wireless occupancy sensors market size tied to energy contracts. Vendors package cloud dashboards that monetize data subscriptions beyond hardware margins. Asset-tracking overlays use the same infrastructure, giving facility managers a multi-service platform that widens TAM without extra capex.

The Wireless Occupancy Sensors Market Report is Segmented by Technology (Passive Infrared, Ultrasonic, Dual Tech, and More), Application (Lighting Control, HVAC & Ventilation, Security & Surveillance, and More), Building Type (Residential, Commercial, Industrial, and More), Network Connectivity (Zigbee, Bluetooth/BLE, and More), End-User Industry, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with a 35% revenue share in 2024, powered by ASHRAE 90.1-2019 and Title 24 codes that mandate sensors in virtually all commercial projects. The United States spearheads mmWave radar R&D, with firms such as Novelda delivering ultra-wideband detectors capable of micro-motion tracking for patient-room applications Novelda. Canada's LEED-centric retrofit drive and Mexico's factory expansion sustain regional volume despite occasional trade policy uncertainties. The wireless occupancy sensors market continues to benefit from federal tax incentives for energy-efficient equipment upgrades.

Asia-Pacific is the fastest-growing territory, projected to post a 17.8% CAGR as China's smart-city blueprint and Japan's Zero-Energy-Building targets boost sensor penetration. India's 100-Smart-Cities Mission and widespread 5G rollout create fertile ground for BLE-based installations in commercial towers. South Korea leverages its electronics manufacturing capacity to shorten lead times and reduce system prices, driving adoption in local education and healthcare sectors. Abundant local component supply shields the region from global chip shortages, reinforcing the wireless occupancy sensors market growth trajectory.

Europe benefits from the Energy Performance of Buildings Directive, which enforces periodic performance audits that spur continuous retrofit cycles. Germany excels in industrial automation synergies, while the United Kingdom channels carbon-reduction funds into public-sector retrofit grants. France explores smart-grid-to-building data exchanges that pay buildings for demand-response, making sensors revenue-generating assets instead of compliance costs. GDPR steers buyers toward edge-processed solutions, favoring vendors with on-device analytics. Together, these factors embed wireless sensors as a foundational element of Europe's decarbonization roadmap.

- Legrand SA

- Schneider Electric SE

- Acuity Brands Inc.

- Eaton Corporation plc

- Leviton Manufacturing Co. Inc.

- Johnson Controls International plc

- Signify N.V.

- Lutron Electronics Co. Inc.

- Honeywell International Inc.

- General Electric Co.

- Hubbell Incorporated

- ABB Ltd.

- Siemens AG

- Texas Instruments Inc.

- Crestron Electronics Inc.

- Enlighted Inc. (Siemens)

- RAB Lighting Inc.

- Autani LLC

- PointGrab Ltd.

- Delta Electronics Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent energy-efficiency mandates

- 4.2.2 Rapid smart-building and IoT adoption

- 4.2.3 Battery-free energy-harvesting sensors

- 4.2.4 Hybrid-work demand for space analytics

- 4.2.5 ESG-linked occupancy-based HVAC contracts

- 4.2.6 AI-enabled mmWave fusion for zero-latency detection

- 4.3 Market Restraints

- 4.3.1 False triggering and calibration issues

- 4.3.2 Data-privacy and cybersecurity concerns

- 4.3.3 RF congestion in dense IoT deployments

- 4.3.4 Battery-disposal compliance costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Passive Infrared (PIR)

- 5.1.2 Ultrasonic

- 5.1.3 Dual Tech (PIR + Ultrasonic)

- 5.1.4 Microwave / mmWave Radar

- 5.1.5 Other Technologies

- 5.2 By Application

- 5.2.1 Lighting Control

- 5.2.2 HVAC and Ventilation

- 5.2.3 Security and Surveillance

- 5.2.4 Space-Utilization Analytics

- 5.2.5 Other Applications

- 5.3 By Building Type

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Public and Institutional

- 5.4 By Network Connectivity

- 5.4.1 Zigbee

- 5.4.2 Bluetooth / BLE

- 5.4.3 Wi-Fi

- 5.4.4 EnOcean (Energy-Harvesting)

- 5.4.5 LoRa and Other LPWAN

- 5.5 By End-User Industry

- 5.5.1 Smart Buildings

- 5.5.2 Healthcare Facilities

- 5.5.3 Manufacturing

- 5.5.4 Aerospace and Defense

- 5.5.5 Consumer Electronics and Smart Home

- 5.5.6 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Israel

- 5.6.4.2 Saudi Arabia

- 5.6.4.3 United Arab Emirates

- 5.6.4.4 Turkey

- 5.6.4.5 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Legrand SA

- 6.4.2 Schneider Electric SE

- 6.4.3 Acuity Brands Inc.

- 6.4.4 Eaton Corporation plc

- 6.4.5 Leviton Manufacturing Co. Inc.

- 6.4.6 Johnson Controls International plc

- 6.4.7 Signify N.V.

- 6.4.8 Lutron Electronics Co. Inc.

- 6.4.9 Honeywell International Inc.

- 6.4.10 General Electric Co.

- 6.4.11 Hubbell Incorporated

- 6.4.12 ABB Ltd.

- 6.4.13 Siemens AG

- 6.4.14 Texas Instruments Inc.

- 6.4.15 Crestron Electronics Inc.

- 6.4.16 Enlighted Inc. (Siemens)

- 6.4.17 RAB Lighting Inc.

- 6.4.18 Autani LLC

- 6.4.19 PointGrab Ltd.

- 6.4.20 Delta Electronics Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment