|

시장보고서

상품코드

1844601

이탈리아의 안과용 기기 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Italy Ophthalmic Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

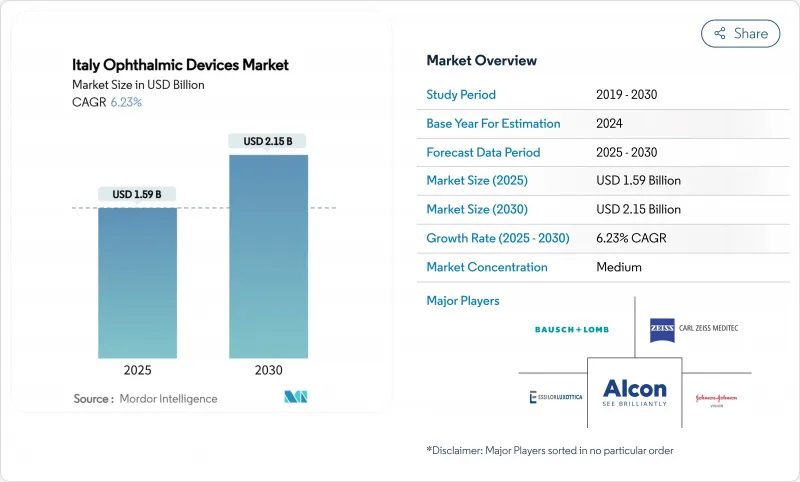

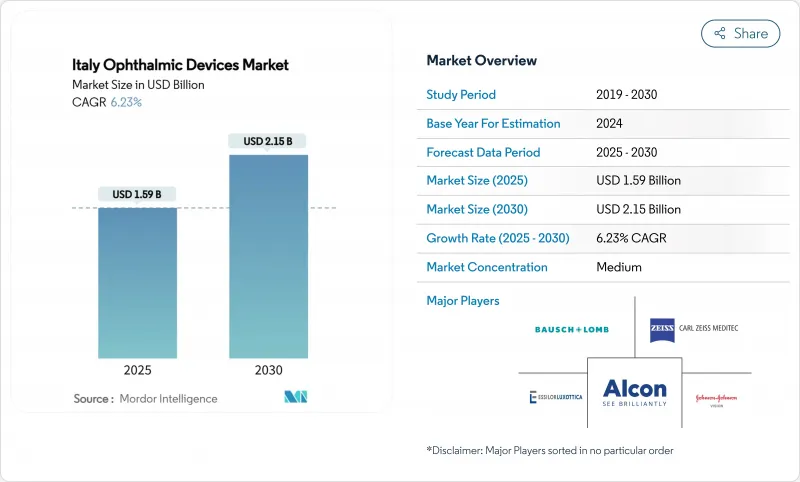

이탈리아의 안과용 기기 시장 규모는 2025년에 15억 9,000만 달러, 2030년에는 21억 5,000만 달러에 이르며, CAGR 6.23%를 나타낼 것으로 예측됩니다.

이 궤도는 급속한 노화, 남유럽 당뇨병 클러스터, 의료 요구와 패션성 높은 안경 수요를 융합하는 밀라노의 독특한 능력에 의해 지원됩니다. 복잡한 수술은 병원이 독점하고 있지만 피아노 나치오날레 디 리프레자 에 레지리엔자(PNRR)가 외래 인프라를 현대화하기 위해 외래 수술 센터(ASC)가 급속히 확대되고 있습니다. 동시에 기업의 광학 체인은 시장 통합을 깊게 하는 반면 EU-MDR 규칙은 신제품 출시 속도를 늦추고 숙련된 컴플라이언스 기능을 가진 기존 기업을 간접적으로 보호하고 있습니다. 이러한 역학은 이탈리아 안과용 기기 시장의 경쟁 리듬을 형성하고 있습니다.

이탈리아의 안과용 기기 시장 동향 및 인사이트

이탈리아 북부에서 당뇨병 망막증 및 AMD의 유병률 상승

북부 이탈리아의 당뇨병 망막증(DR) 이환율은 성인 당뇨병을 앓고 있는 환자의 39%에 달했으며, 이 부담은 스펙트럼 도메인 OCT 스캐너, 초광시야 안저 카메라, 원격 안과 키트에 대한 수요를 높이고 있습니다. 스크리닝의 진찰률은 50% 미만에 그치고 있으며, 망막 화상을 3차 의료 기관에 전송해, 신속한 판독을 실시하는 지역 밀착형 프로그램의 여지가 있습니다. DR의 직접 치료비는 환자 1인당 EUR 4,050-5,799이며, 이 비용은 병태를 조기에 발견하는 기술에 환불을 하는 지불자를 납득시키는 것입니다. 이에 따라 벤더는 인공지능에 의한 트리어지 알고리즘을 하드웨어에 번들함으로써, 판독 시간을 단축하고, 이탈리아의 안과용 기기 시장에서의 수익 증가를 도모하고 있습니다.

밀라노에 집적하는 패션 산업이 견인하는 1인당 안경 소비액의 높이

밀라노의 세계적인 패션 견인력으로 안경은 라이프 스타일의 액세서리로 재인식되었으며, 거시 경제가 불안정한 시기에도 '메이드 인 이탈리아'라는 라벨은 프리미엄 가격으로 판매 할 수 있습니다. 2024년 수출 총액은 전년 대비 0.6% 감소한 약간의 하락에도 불구하고 52억 3,600만 유로이며, 하이엔드 프레임의 회복력을 야기했습니다. 젊은 전문가들은 재생 아세테이트와 바이오 폴리머를 선호하고 금리를 확대하는 지속가능성 이야기를 추진합니다. 옴니채널 기업체인은 디지털 대응 피팅으로 브랜드 스토리텔링을 증폭시켜 이탈리아의 안과용 기기 시장에 대한 지배력을 강화하고 있습니다.

긴 EU-MDR 적합 승인 사이클이 제품 상시를 지연시킵니다.

2021년 EU-MDR 시스템에서는 데이터 요구사항, 시판 후 감시 단계, 고유 장비 식별 의무가 증가했습니다. 국내 소규모 혁신자는 현재 최대 18개월의 인증 지연에 직면하고 있으며, 상품화의 이정표가 밀려나고 비용이 상승하고 있습니다. 노티파이드 바디의 용량이 한정되어 있기 때문에 신규 신청보다 인증 갱신이 우선되어 다국적의 기존 기업이 타이밍 적으로 우위에 서서 이탈리아의 안과용 기기 시장에 대한 기술 혁신의 흐름이 느껴지고 있습니다.

부문 분석

비전 케어 기기는 2024년 이탈리아 안과용 기기 시장의 64.21%를 차지했습니다. 프리미엄 아세테이트 프레임은 현재 250 유로 가까이에서 판매되고 있으며 블루라이트 흡수용 스마트 코팅이 자주 포함되어 있습니다. 콘택트렌즈는 위생 중시의 쫓는 바람을 타고 도시의 전문가가 가격보다 편리성을 선택하는 가운데, 일일 일회용이 1개월 일회용을 웃돌고 있습니다. 한편, 진단 및 모니터링 기기는 가장 급성장하고 있는 분야이며, 병원이 AI 트리어지 소프트웨어와 연동하는 스펙트럼 도메인 OCT 유닛으로 업그레이드함에 따라, CAGR 8.35%로 확대하고 있습니다. 최근 OCT 세분화의 정확도가 0.9792로 검증된 Attention-Based DenseNet 모델은 이미징 투자에 임상적인 기세를 더합니다. 이러한 역학은 이탈리아의 안과용 기기 시장공급업체에게 수년에 걸쳐 수요의 확실성을 높이는 것입니다.

2세대 포인트 오브 케어 안압계, 핸드헬드 안저 카메라, 클라우드 링크 슬릿 램프는 이탈리아 안과용 기기 시장의 기술적 범위를 더욱 확대하고 있습니다. 공급업체는 전자 의료 기록(EHR) 데이터를 통합하는 분석 대시보드를 번들로 제공하여 임상의가 질병 진행을 추적하고 소개를 간소화할 수 있는 경우가 늘어나고 있습니다. 따라서 병원은 조달 컴플라이언스를 단순화하기 위해 단일 소스 파트너를 찾고 있기 때문에 포트폴리오의 두께가 차별화 요인이 되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 북 이탈리아에서 당뇨병성 망막증 및 AMD의 유병률 상승

- 밀라노에 집적하는 패션 산업이 견인하는 1인당 안경 소비액의 높이

- 펨토세컨드 및 엑시머 레이저 플랫폼의 공적 병원에의 급속한 도입

- 정부 「Piano Nazionale Di Ripresa(PNRR)」에 의한 ASC 업그레이드에의 자금 원조

- 기업의 광학 소매 체인 확대

- 국내의 안내 렌즈 수탁 제조거점이 조달 비용을 인하

- 시장 성장 억제요인

- 긴 EU-MDR 적합 승인 사이클에 의한 제품 출시의 지연

- 국가위생국(SSN)의 입찰에 의한 가격 제한

- 남부 지역에서 안과 의사의 부족

- 수술 후 안내염의 소송 위험 증가

- 규제 전망

- Porter's Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 기기 유형별

- 진단 및 모니터링 기기

- OCT 스캐너

- 안저 및 망막 카메라

- 자동굴절계 및 각막경

- 각막 지형도 시스템

- 초음파 영상 시스템

- 시야계 및 안압계

- 기타 진단 및 모니터링 기기

- 수술용 기기

- 백내장 수술 기기

- 유리체망막 수술 기기

- 굴절 수술 기기

- 녹내장 수술 기기

- 기타 수술 기기

- 시력 관리 기기

- 안경테 및 렌즈

- 콘택트렌즈

- 진단 및 모니터링 기기

- 질환별

- 백내장

- 녹내장

- 당뇨병성 망막병증

- 기타 질환

- 최종 사용자별

- 병원

- 안과 전문 클리닉

- 외래 수술 센터(ASC)

- 기타 최종 사용자

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Alcon Inc.

- Johnson & Johnson Vision

- EssilorLuxottica SA

- Carl Zeiss Meditec AG

- Bausch Lomb Corp.

- Hoya Corp.

- CooperVision Inc.

- Topcon Corp.

- Nidek Co. Ltd.

- HAAG-Streit Group

- Heidelberg Engineering GmbH

- Quantel Medical SAS

- Leica Microsystems GmbH

- Glaukos Corp.

- Menicon Co. Ltd.

제7장 시장 기회와 전망

KTH 25.11.05The Italy ophthalmic devices market size is USD 1.59 billion in 2025 and is forecast to reach USD 2.15 billion by 2030, expanding at a 6.23% CAGR.

This trajectory is powered by a rapidly aging population, a southern European diabetes cluster, and Milan's unique ability to merge medical need with fashion-forward eyewear demand. Hospitals dominate complex surgery volumes, yet ambulatory surgery centers (ASCs) are scaling quickly as Piano Nazionale di Ripresa e Resilienza (PNRR) grants modernize outpatient infrastructure. At the same time, corporate optical chains deepen market consolidation while EU-MDR rules slow the speed of new product launches, indirectly protecting incumbents with seasoned compliance functions. These dynamics collectively shape the competitive rhythm of the Italy ophthalmic devices market.

Italy Ophthalmic Devices Market Trends and Insights

Rising Prevalence of Diabetic Retinopathy & AMD In Northern Italy

Northern provinces now report diabetic retinopathy (DR) rates as high as 39% among adults with diabetes, a burden that elevates demand for spectral-domain OCT scanners, ultra-wide-field fundus cameras, and tele-ophthalmology kits. Screening uptake hovers below 50%, creating latitude for community-based programs that route retinal images to tertiary centers for rapid reads. Direct DR treatment costs lie between EUR 4,050 and 5,799 per patient, an outlay that convinces payers to reimburse technologies that catch pathology sooner rather than later. In response, vendors bundle artificial-intelligence triage algorithms with hardware to shorten interpretation times and unlock incremental revenue in the Italy ophthalmic devices market.

High Per-Capita Eyewear Spending Driven by Fashion Industry Clustering in Milan

Milan's global fashion pull reframes glasses as lifestyle accessories, allowing "Made in Italy" labels to command premium price points even during macroeconomic volatility. Exports still totaled EUR 5.236 billion in 2024 despite a fractional 0.6% dip from the prior year, underscoring the resilience of high-end frames. Younger professionals favor recycled acetate and bio-based polymers, driving a sustainability narrative that enhances margins. Omnichannel corporate chains amplify brand storytelling with digitally enabled fittings, strengthening their grip on the Italy ophthalmic devices market.

Lengthy EU-MDR Conformity Approval Cycles Delaying Product Launches

The 2021 EU-MDR regime increases data requirements, post-market surveillance steps, and unique device identification mandates. Smaller domestic innovators now face certification delays up to 18 months, pushing commercialization milestones and elevating costs. Limited notified-body capacity prioritizes certificate renewals over new submissions, giving multinational incumbents a timing advantage and slowing innovation flow into the Italy ophthalmic devices market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Public-Hospital Adoption of Femtosecond & Excimer Laser Platforms

- Government PNRR Funding for ASC Upgrades

- Price Caps Imposed By Servizio Sanitario Nazionale (SSN) Tenders

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vision care devices secured 64.21% of the Italy ophthalmic devices market in 2024, propelled by domestic design strength and high per-capita eyewear replacement cycles. Premium acetate frames now retail near EUR 250 and frequently integrate smart coatings for blue-light absorption, reflecting consumer readiness to invest in performance and aesthetics. Contact lenses ride a hygiene-focused tailwind, with daily disposables outpacing monthlies as urban professionals choose convenience over price. Meanwhile diagnostic & monitoring devices represent the fastest-growing slice, expanding at an 8.35% CAGR as hospitals upgrade to spectral-domain OCT units that interface with AI triage software. The Attention-Based DenseNet model recently validated for OCT segmentation with 0.9792 accuracy adds clinical momentum for imaging investments. These dynamics cement multi-year demand certainty for suppliers in the Italy ophthalmic devices market.

Second-generation point-of-care tonometers, handheld fundus cameras, and cloud-linked slit lamps further widen the technological scope of the Italy ophthalmic devices market. Vendors increasingly bundle analytics dashboards that integrate Electronic Health Record (EHR) data, allowing clinicians to track disease progression and streamline referrals. Portfolio depth thus becomes a differentiator as hospitals seek single-source partners to simplify procurement compliance.

The Italy Ophthalmic Devices Market Report is Segmented by Device Type (Diagnostic & Monitoring Devices, Surgical Devices, and Vision Care Devices), Disease Indication (Cataract, Glaucoma, Diabetic Retinopathy, Other Disease Indications), End-User (Hospitals, Specialty Ophthalmic Clinics, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Alcon

- Johnson & Johnson

- EssilorLuxottica S.A.

- Carl Zeiss

- Bausch + Lomb Corp.

- Hoya Corp.

- CooperVision Inc.

- Topcon Corp.

- Nidek

- HAAG-Streit

- Heidelberg Engineering

- Quantel Medical SAS

- Danaher

- Glaukos Corp.

- Menicon Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Diabetic Retinopathy & AMD In Northern Italy

- 4.2.2 High Per-Capita Eyewear Spending Driven by Fashion Industry Clustering in Milan

- 4.2.3 Rapid Public-Hospital Adoption of Femtosecond & Excimer Laser Platforms

- 4.2.4 Government "Piano Nazionale Di Ripresa (PNRR) " Funding for ASC Upgrades

- 4.2.5 Expansion of Corporate Optical Retail Chains

- 4.2.6 Domestic IOL Contract-Manufacturing Base Lowering Procurement Costs

- 4.3 Market Restraints

- 4.3.1 Lengthy EU-MDR Conformity Approval Cycles Delaying Product Launches

- 4.3.2 Price Caps Imposed By Servizio Sanitario Nazionale (SSN) Tenders

- 4.3.3 Shortage of Ophthalmologists in Southern Regions

- 4.3.4 Rising Post-Operative Endophthalmitis Litigation Risk

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Diagnostic & Monitoring Devices

- 5.1.1.1 OCT Scanners

- 5.1.1.2 Fundus & Retinal Cameras

- 5.1.1.3 Autorefractors & Keratometers

- 5.1.1.4 Corneal Topography Systems

- 5.1.1.5 Ultrasound Imaging Systems

- 5.1.1.6 Perimeters & Tonometers

- 5.1.1.7 Other Diagnostic & Monitoring Devices

- 5.1.2 Surgical Devices

- 5.1.2.1 Cataract Surgical Devices

- 5.1.2.2 Vitreoretinal Surgical Devices

- 5.1.2.3 Refreactive Surgical Devices

- 5.1.2.4 Glaucoma Surgical Devices

- 5.1.2.5 Other Surgical Devices

- 5.1.3 Vision Care Devices

- 5.1.3.1 Spectacles Frames & Lenses

- 5.1.3.2 Contact Lenses

- 5.1.1 Diagnostic & Monitoring Devices

- 5.2 By Disease Indication

- 5.2.1 Cataract

- 5.2.2 Glaucoma

- 5.2.3 Diabetic Retinopathy

- 5.2.4 Other Disease Indications

- 5.3 By End-user

- 5.3.1 Hospitals

- 5.3.2 Specialty Ophthalmic Clinics

- 5.3.3 Ambulatory Surgery Centers (ASCs)

- 5.3.4 Other End-users

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Alcon Inc.

- 6.3.2 Johnson & Johnson Vision

- 6.3.3 EssilorLuxottica S.A.

- 6.3.4 Carl Zeiss Meditec AG

- 6.3.5 Bausch + Lomb Corp.

- 6.3.6 Hoya Corp.

- 6.3.7 CooperVision Inc.

- 6.3.8 Topcon Corp.

- 6.3.9 Nidek Co. Ltd.

- 6.3.10 HAAG-Streit Group

- 6.3.11 Heidelberg Engineering GmbH

- 6.3.12 Quantel Medical SAS

- 6.3.13 Leica Microsystems GmbH

- 6.3.14 Glaukos Corp.

- 6.3.15 Menicon Co. Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment