|

시장보고서

상품코드

1844620

잠수함 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Submarine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

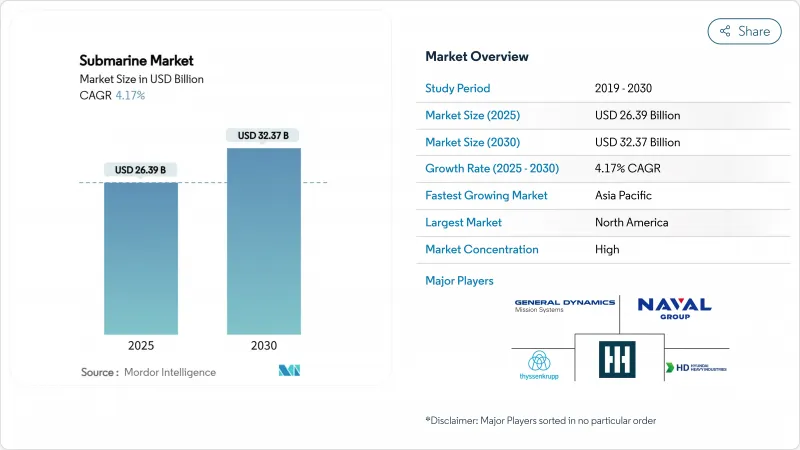

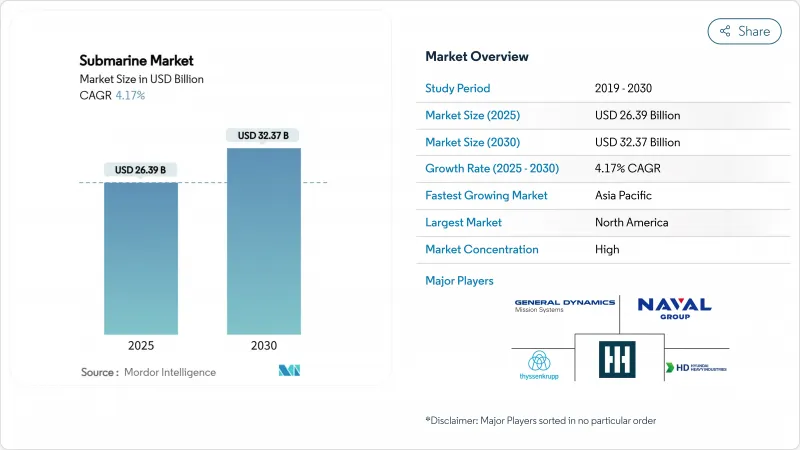

잠수함 시장 규모는 2025년에 263억 9,000만 달러, 2030년에는 323억 7,000만 달러에 이를 것으로 예상되며, CAGR은 4.17%를 나타낼 전망입니다.

잠수함의 취득에는 자본 집약적인 성격이 있어, 척당 수십억 달러의 가격표가 붙여져 30년 이상 사용되고 있습니다. 호주가 AUKUS 협정에 따라 원자력 잠수함에 커밋함으로써 조달의 우선 순위가 재검토되고 동맹국 공장은 능력과 기술 로드맵의 재조합을 강요하고 있습니다. 인도 태평양의 해양 마찰 격화는 특히 중국이 2035년까지 80척의 잠수함을 보유하는 것을 목표로 하고, 인근 국가들이 수중 근대화를 가속화하는 중 조달의 기세를 지속시키고 있습니다. 비용면의 우위성에서 디젤 일렉트릭 보트가 여전히 우위를 유지하고 있지만 장거리 억제에 대한 전략적 경사를 반영하여 원자력 유닛이 가장 빠른 판매 궤도를 누리고 있습니다. 북미는 미국 해군의 2,139억 달러의 조달 파이프라인을 배경으로 지출의 주도권을 유지하고 있습니다. 그러나 아시아태평양은 진화하는 위협의 도식에 맞추어 해군이 투자 규모를 확대하고 있기 때문에 성장 엔진이 되고 있습니다.

세계의 잠수함 시장 동향과 인사이트

Tier 1 해군 방위 근대화 예산 증가

잠수함 시장의 눈에 띄는 상승주기를 지원하는 것은 주요 해양 강대국의 예산 확대입니다. 미 해군만으로도 향후 10년간 원자력정에 2,139억 달러의 예산이 계상되고 있습니다. 독일은 함대 업그레이드를 위해 8억 유로(9억 4,530만 달러)를 승인했으며, 네덜란드는 바라쿠다급 대체를 위해 22억 유로(26억 달러)를 할당했습니다. 인도의 프로젝트 75(i)와 호주 AUKUS 프로그램은 수십억 달러의 파이프라인을 추가하고 수주장부를 건강하게 유지합니다. 잠수함의 계약은 수주부터 취역까지 7-10년이 걸리기 때문에 이러한 배분은 원청기업에 장기적인 현금흐름 전망을 주어 새로운 드라이독, 모듈식 건조라인, 저관찰성 재료의 연구에 대한 투자를 정당화합니다.

인도 태평양 해역의 긴장 격화

중국이 2035년까지 095형 SSN과 096형 SSBN을 포함한 80척의 잠수함을 보유하게 될 것으로 예측되고 있으며 인도 태평양 전역에서 경쟁 압력이 높아지고 있습니다. 일본의 '타이헤이'급, 한국의 'KSS-III', 호주의 미래 SSN은 동맹국의 카운터웨이트 백본을 형성합니다. 이 지역은 현재 신조선 수요의 가장 큰 공급원이 되고 있으며, 미국, 한국, 호주 조선소는 중복 주문을 흡수하기 위해 생산 능력을 강화하고 있습니다. 미국의 공격형 잠수함의 전방 전개가 서태평양의 기지를 자주 경유하게 되어, 데포 레벨의 유지관리 사이클의 처리량을 유지하는 압력이 강해지는 경향이 있습니다.

초고액 취득 비용과 수명주기 비용

버지니아급 신조정은 현재 48억 달러, 콜롬비아급 SSBN은 1척당 152억 달러를 넘어 해군의 자본 예산은 희박하고 있습니다. 라이프 사이클의 부담도 마찬가지로 어렵습니다. USS 보이스의 연료 보급 오버홀은 12억 달러에 이르고, 이는 수출 등급의 정상형 잠수함 가격에 필적하는 숫자입니다. 예산에 제약이 있는 해군은 종종 함대의 규모를 능력으로 교환하고, 유지 보수, 훈련, 군수품을 채우기 위해 선체 수를 줄입니다. 단가 급등은 장기적인 잠수함 시장 확대의 가장 큰 브레이크인 것을 계속합니다.

부문 분석

원자력 잠수함은 CAGR 5.45%로 가장 빠르게 성장하고 있지만, 디젤 전기 설계는 2024년 매출의 56.23%를 차지하며 수적 리드를 유지했습니다. AUKUS의 결정을 통해 공급망의 초점은 고농축 연료 코어와 원자로 모듈로 향했습니다. 호주가 미국, 영국, 프랑스, 러시아, 중국, 인도 및 원자력 사업자의 동반자로 인해 원자력 잠수함 시장 규모는 현저하게 확대됩니다. 그러나 소규모 해군이 저렴한 가격과 스텔스성을 중시하는 제약이 많은 얕은 해역에서는 기존 잠수함이 필수적인 것에 변함이 없습니다. 첨단 리튬 이온 및 연료전지 솔루션은 수중 내구성을 늘리고 비용에 민감한 조달에서 디젤 전기 선체에 두 번째 바람을 불어 넣습니다. 제조업체 각사는 현재, 장래의 기술 이전이나 라이프 사이클·지원을 용이하게 하기 위해, 추진력의 유형에 관계없이 공통의 전투 시스템·아키텍쳐를 제공하는 것을 일상적으로 실시했습니다.

함대 플래너는 추진력을 선택할 때 가격뿐만 아니라 임무 프로파일을 중시합니다. 원자력정은 억지력 순찰, 특수부대 투입, 하이엔드 대잠수함전에서 탁월한 전략적 도달범위를 제공합니다. 일반형 보트는 초크 포인트와 해안에서 감지를 피하기 위해 더 작은 음향 시그니처를 활용하여 성공을 거둘 수 있습니다. 대국간 경쟁이 치열해지는 가운데 듀얼트랙 수요는 두 범주 간의 균형 잡힌 성장을 보장하고 원청 기업의 수익 기반을 넓히는 동시에 단일 프로그램 지연과 관련된 시장 변동을 완화합니다.

공격형 잠수함은 멀티미션의 유연성으로 인해 2024년에는 49.12%의 수익 점유율을 획득했습니다. 그러나 탄도 미사일 보트가 가장 기세가 있어 2030년까지의 CAGR은 6.23%를 나타낼 전망입니다. 콜롬비아급, 중국의 096형, 인도의 S4급이 SSBN의 백로그 급증의 원인이 되고 있습니다. 따라서 탄도 미사일 플랫폼의 잠수함 시장 규모는 안전한 두 번째 공격 능력에 대한 재중시를 반영하여 증가하는 경향이 있습니다. 유도 미사일 유닛은 수많은 것, 핵의 역치를 깨지 않고, 통상형의 즉각 공격 옵션에 필수적인 것에 변함이 없고, 해군에게 에스컬레이션의 유연성을 부여하고 있습니다.

전략 독트린은 변화하고 있습니다. 핵보유국은 지속적인 해상억제를 우선시하고 전력태세의 신뢰성을 잠수탄도자산에 고정하고 있습니다. 동시에 공격형 잠수함은 매일 정보 수집, 항공 모호위, 대함 임무의 주력이 됩니다. 그 결과 조선 제조업체는 두 역할 모두에 대응할 수 있는 모듈 설계를 채택하게 되어 연구 개발비를 절감하고 개발 사이클을 단축할 수 있습니다.

지역 분석

북미는 미국 해군의 SSN과 SSBN 파이프라인이 전면에 나와 있기 때문에 세계 지출액의 36.36%를 차지하고 있습니다. 의회 예산은 안정되어 있는 것, 일렉트릭 보트사와 헌팅턴 잉가르스사의 생산 스트레스가 납기를 장기화시켜 눈앞의 수량 증가를 억제하고 있습니다. AUKUS는 호주 인력이 미국 야드에서 훈련을 받고 영국 설계자가 원자로 레이아웃에서 협력하는 등 외수를 늘리고 있습니다. 한편 캐나다는 최대 12척의 신조선을 요구하고 있지만 결정 시기는 2025년 이후로 연장됩니다.

아시아태평양은 중국, 일본, 한국, 인도, 호주가 주문을 급증시키고 있으며 CAGR 5.92%를 나타냅니다. 일본은 2025년 3월에 4척째의 타이게이급을 취역시켜 리튬이온의 안전성과 내구성 향상을 검증했습니다. 인도는 카르바리급의 건조 스케줄을 앞당겨 프로젝트 75(i)를 계약 체결을 향해 추진했습니다. 한국의 KSS-III의 발트해에서의 시험운용은 블루워터에 대한 의욕과 수출의 신뢰성을 강조하는 것입니다. 아시아태평양의 잠수함 시장 규모는 북미 시장 규모에 거의 필적하는 형태로 10년을 마칠 것으로 예측됩니다.

유럽은 리플레이스 주도의 성장을 기록합니다. 독일 해군의 연명 공사, 네덜란드의 바라쿠다 계약, 그리스 파파니콜리스의 업그레이드는 지역 야드를 바쁘게 만들고 있습니다. 폴란드 오르카 입찰과 튀르키예 SSN 개념 조사도 경쟁 입찰 기회를 늘리고 있습니다. NATO의 상호 운용성 요구 사항은 전투 시스템의 기준선을 계속 형성하고, 업그레이드 경로 공유 및 공급업체의 중복을 보장하며, 동맹 회원국의 장기 유지 비용을 절감합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- Tier1 해군의 방위 근대화 예산 증가

- 인도 태평양 해역의 긴장 격화

- 레거시 원자력 사업자의 함대 대체 사이클

- AIP와 리튬 이온 배터리의 채용에 의한 수중 내구성의 향상

- AUKUS 협정에 의한 동맹 함대의 확대

- 해저 데이터·케이블·인프라의 안전 확보가 필요

- 시장 성장 억제요인

- 초고액의 취득 비용과 라이프 사이클 비용

- 군비관리 및 핵확산 방지조약

- 잠수함 야드의 숙련 노동자의 병목

- 해저 반도체공급 체인 부족

- 밸류체인 분석

- 규제 상황

- 기술적 전망

- Porter's Porter's Five Forces

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 추진 유형별

- 원자력

- 디젤 전기(일반형 및 AIP)

- 전투 역할별

- 공격형(SSN/SSK)

- 탄도 미사일(SSBN)

- 유도 미사일(SSGN)

- 배수량 등급별

- 2,000톤 미만

- 2,000톤 이상 4,000톤 미만

- 4,000톤 이상

- 구성 요소별

- 선체 및 구조 모듈

- 추진 시스템

- 전투 및 센서 장비

- 에너지 저장 장치(배터리, AIP)

- 지역별

- 북미

- 미국

- 캐나다

- 남미

- 브라질

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 이스라엘

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- General Dynamics Mission Systems, Inc.(General Dynamics Corporation)

- Huntington Ingalls Industries, Inc.

- BAE Systems plc

- Naval Group

- thyssenkrupp Marine Systems GmbH(thyssenkrupp AG)

- HD Hyundai Heavy Industries Co. Ltd.

- Hanwha Corporation

- Mitsubishi Heavy Industries Ltd.

- Kawasaki Heavy Industries, Ltd.

- Saab AB

- NAVANTIA, SA, SME

- Fincantieri SpA

- United Shipbuilding Corporation

- China State Shipbuilding Corporation

- Jiangnan Shipyard

- ASC Pty Ltd.

- PT PAL Indonesia

- SIMA PERU SA

제7장 시장 기회와 전망

KTH 25.11.05The submarine market size is worth USD 26.39 billion in 2025 and is forecasted to climb to USD 32.37 billion in 2030, advancing at a steady 4.17% CAGR.

This controlled expansion reflects the capital-intensive nature of submarine acquisition, where each boat carries a multi-billion-dollar price tag and remains in service for 30 years or more. Australia's commitment to nuclear-powered submarines under the AUKUS pact has redrawn procurement priorities, forcing allied yards to realign capacity and technology roadmaps. Intensifying maritime frictions in the Indo-Pacific sustain procurement momentum, especially as China races toward an 80-boat fleet by 2035, prompting neighbors to accelerate underwater modernization. Diesel-electric boats still dominate through their cost advantages, yet nuclear units enjoy the fastest sales trajectory, mirroring a strategic tilt toward long-range deterrence. North America retains spending leadership on the back of the US Navy's USD 213.9 billion procurement pipeline. Still, the Asia-Pacific is the growth engine as regional navies scale investments to match the evolving threat picture.

Global Submarine Market Trends and Insights

Rising Defense-Modernization Budgets Among Tier-1 Navies

Expanding budgets across major sea powers underpin a visible upcycle in the submarine market. The US Navy alone has USD 213.9 billion earmarked for nuclear boats over the next decade. Parallel commitments are evident in Europe, where Germany approved EUR 800 million (USD 945.3 million) for fleet upgrades and the Netherlands allotted EUR 2.2 billion (USD 2.6 billion) for Barracuda-class replacements. India's Project 75(I) and Australia's AUKUS program add multi-billion-dollar pipelines that keep order books healthy. Because submarine contracts span 7-10 years from award to commissioning, these allocations give prime contractors long-term cash-flow visibility and justify investments in new dry-docks, modular construction lines, and research into low-observable materials.

Escalating Indo-Pacific Maritime Tensions

China's projected rise to 80 submarines by 2035, including Type 095 SSNs and Type 096 SSBNs, amplifies competitive pressure across the Indo-Pacific. Japan's Taigei-class, South Korea's KSS-III, and Australia's future SSNs form the backbone of an allied counterweight. The region is now the largest source of new-build demand, with yards in the United States, South Korea, and Australia pushing capacity to absorb overlapping orders. Forward-deployed US attack submarines rotate through Western Pacific bases more frequently, a trend intensifying pressure to sustain throughput in depot-level maintenance cycles.

Ultra-High Acquisition and Lifecycle Costs

A new Virginia-class boat now costs USD 4.8 billion, while each Columbia-class SSBN eclipses USD 15.2 billion, tightening naval capital budgets. Lifecycle burdens are equally daunting: the refueling-overhaul of USS Boise came to USD 1.2 billion, a figure rivalling the price of an export-grade conventional submarine. Budget-constrained navies often trade fleet size for capability, trimming hull counts to fund maintenance, training, and munitions. Escalating per-unit price tags remain the single largest brake on the submarine market expansion over the long term.

Other drivers and restraints analyzed in the detailed report include:

- Fleet-Replacement Cycles in Legacy Nuclear Operators

- Adoption of AIP and Li-ion Batteries Extending Submerged Endurance

- Skilled Labor Bottlenecks in Submarine Yards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Nuclear submarines represent the fastest-growing slice, advancing at 5.45% CAGR, while diesel-electric designs still hold the numerical lead with 56.23% of 2024 revenue. The AUKUS decision redirected supply-chain focus toward highly enriched fuel cores and reactor modules. The submarine market size for nuclear-powered craft is set to enlarge noticeably as Australia joins the United States, United Kingdom, France, Russia, China, and India in the nuclear operator club. Yet conventional boats remain indispensable in constrained, shallow theaters where smaller navies prize affordability and stealth. Advanced lithium-ion and fuel-cell solutions stretch submerged endurance, giving diesel-electric hulls a second wind in cost-sensitive procurements. Manufacturers now routinely offer common combat-system architectures across propulsion types to ease future technology transfers and life-cycle support.

Fleet planners weigh mission profiles rather than price alone when selecting propulsion. Nuclear boats offer unmatched strategic reach for deterrence patrols, special-forces insertion, and high-end anti-submarine warfare. Conventional boats thrive in chokepoints and littorals, leveraging smaller acoustic signatures to evade detection. As great-power competition intensifies, dual-track demand ensures balanced growth across both categories, broadening the revenue base for prime contractors while cushioning market volatility linked to single-program delays.

Attack submarines captured 49.12% revenue share in 2024 by their multi-mission flexibility. However, ballistic-missile boats deliver the most momentum with a 6.23% CAGR to 2030. The Columbia-class, China's Type 096, and India's S4-class collectively account for a surge in SSBN backlog. Therefore, the submarine market size for ballistic-missile platforms is on an upswing, reflecting renewed emphasis on secure second-strike capabilities. While fewer in number, guided-missile units remain essential for conventional prompt-strike options without breaching nuclear thresholds, giving navies escalatory flexibility.

Strategic doctrines are shifting: nuclear-armed states prioritize continuous-at-sea deterrence, anchoring force-posture credibility on submerged ballistic assets. In tandem, attack submarines become workhorses for day-to-day intelligence gathering, carrier escort, and anti-ship missions. The resulting portfolio mix encourages shipbuilders to adopt modular designs that can be configured for both roles, trimming R&D expense and shortening development cycles.

The Submarine Market Report is Segmented by Propulsion Type (Nuclear-Powered and Diesel-Electric Submarines), Combat Role (Attack, Ballistic-Missile, and More), Displacement Class (Less Than 2, 000 Tons, 2, 000 To 4, 000 Tons, and More), Component (Hull and Structural Modules, Propulsion Systems, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America holds 36.36% of global expenditure thanks to the US Navy's front-loaded SSN and SSBN pipeline. Although congressional appropriations remain stable, production stresses at Electric Boat and Huntington Ingalls lengthen delivery schedules, tempering near-term volume growth. AUKUS adds external demand, with Australian personnel training in American yards and British designers collaborating on reactor layouts. Canada, meanwhile, weighs a requirement for up to 12 new boats, but decision timelines extend beyond 2025.

Asia-Pacific is the fastest riser, showing a 5.92% CAGR, with China, Japan, South Korea, India, and Australia soaring in orders. Japan commissioned its fourth Taigei-class in March 2025, validating lithium-ion safety and endurance gains. India advances its Kalvari-class build schedule and pushes Project 75(I) toward contract award, structuring terms around technology transfer to state-owned yards. South Korea's Baltic Sea trials for KSS-III underscore its blue-water aspirations and export credibility. The submarine market size for Asia-Pacific is expected to close the decade, nearly matching the North American value.

Europe records measured, replacement-driven growth. German Navy life-extension work, the Dutch Barracuda deal, and Greece's Papanikolis upgrade keep regional yards occupied. Poland's Orka tender and Turkey's exploratory SSN concept studies add competitive bidding opportunities. NATO interoperability requirements continue to shape combat-system baselines, ensuring shared upgrade pathways and supplier overlap that reduce long-run sustainment costs for alliance members.

- General Dynamics Mission Systems, Inc. (General Dynamics Corporation)

- Huntington Ingalls Industries, Inc.

- BAE Systems plc

- Naval Group

- thyssenkrupp Marine Systems GmbH (thyssenkrupp AG)

- HD Hyundai Heavy Industries Co. Ltd.

- Hanwha Corporation

- Mitsubishi Heavy Industries Ltd.

- Kawasaki Heavy Industries, Ltd.

- Saab AB

- NAVANTIA, S.A., SME

- Fincantieri S.p.A.

- United Shipbuilding Corporation

- China State Shipbuilding Corporation

- Jiangnan Shipyard

- ASC Pty Ltd.

- PT PAL Indonesia

- SIMA PERU S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising defense-modernization budgets among Tier-1 navies

- 4.2.2 Escalating Indo-Pacific maritime tensions

- 4.2.3 Fleet-replacement cycles in legacy nuclear operators

- 4.2.4 Adoption of AIP and Li-ion batteries extending submerged endurance

- 4.2.5 AUKUS pact triggering allied fleet expansion

- 4.2.6 Need to secure subsea data-cable infrastructure

- 4.3 Market Restraints

- 4.3.1 Ultra-high acquisition and lifecycle costs

- 4.3.2 Arms-control and nuclear-proliferation treaties

- 4.3.3 Skilled labor bottlenecks in submarine yards

- 4.3.4 Supply-chain scarcity of marinized semiconductors

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Propulsion Type

- 5.1.1 Nuclear-Powered

- 5.1.2 Diesel-Electric (Conventional and AIP)

- 5.2 By Combat Role

- 5.2.1 Attack (SSN/SSK)

- 5.2.2 Ballistic-Missile (SSBN)

- 5.2.3 Guided-Missile (SSGN)

- 5.3 By Displacement Class

- 5.3.1 Less than 2,000 tons

- 5.3.2 2,000 to 4,000 tons

- 5.3.3 Greater than 4,000 tons

- 5.4 By Component

- 5.4.1 Hull and Structural Modules

- 5.4.2 Propulsion Systems

- 5.4.3 Combat and Sensor Suites

- 5.4.4 Energy Storage (Batteries, AIP)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Israel

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 General Dynamics Mission Systems, Inc. (General Dynamics Corporation)

- 6.3.2 Huntington Ingalls Industries, Inc.

- 6.3.3 BAE Systems plc

- 6.3.4 Naval Group

- 6.3.5 thyssenkrupp Marine Systems GmbH (thyssenkrupp AG)

- 6.3.6 HD Hyundai Heavy Industries Co. Ltd.

- 6.3.7 Hanwha Corporation

- 6.3.8 Mitsubishi Heavy Industries Ltd.

- 6.3.9 Kawasaki Heavy Industries, Ltd.

- 6.3.10 Saab AB

- 6.3.11 NAVANTIA, S.A., SME

- 6.3.12 Fincantieri S.p.A.

- 6.3.13 United Shipbuilding Corporation

- 6.3.14 China State Shipbuilding Corporation

- 6.3.15 Jiangnan Shipyard

- 6.3.16 ASC Pty Ltd.

- 6.3.17 PT PAL Indonesia

- 6.3.18 SIMA PERU S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment