|

시장보고서

상품코드

1844631

면역 분석 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Immunoassays - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

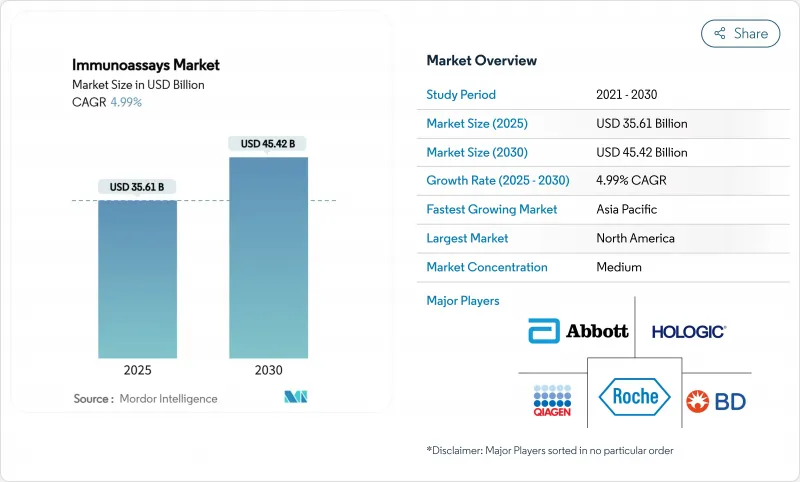

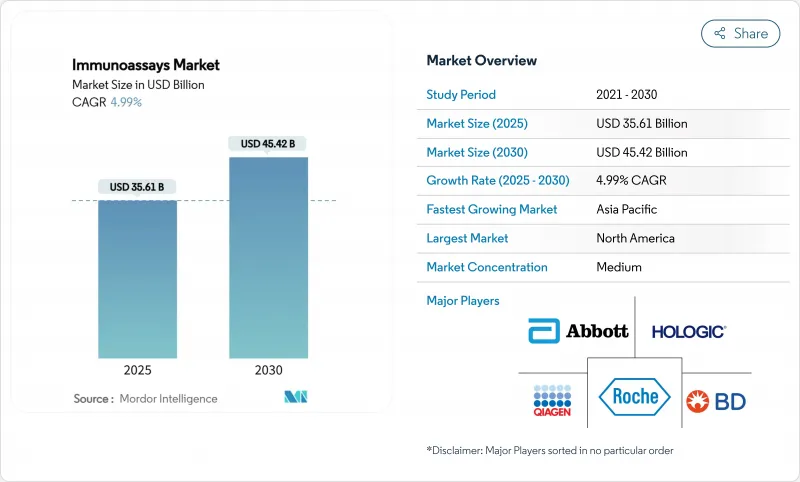

면역분석 시장은 2025년 356억 1,000만 달러로 평가되었고, 2030년에는 454억 2,000만 달러에 이를 것으로 예측되며, CAGR 4.99%로 성장할 전망입니다.

이러한 성장 추세는 종양학 바이오마커, 인공지능 기반 플랫폼, 실시간 생물공정 모니터링에 대한 수요 증가에 힘입어 성숙하면서도 꾸준히 확장되는 시장을 반영합니다. 현재 인공지능 강화 장치는 면역분석 검출 한계를 페토몰 수준까지 낮추고 있으며, 라이스 대학교의 유세포 분석 장비가 지역사회 진료소에서 실험실 수준의 정확도를 제공하는 사례에서 확인할 수 있습니다. 치료 약물 모니터링 분야의 화학발광 면역분석법(CLIA) 도입 확대와 신흥국에서의 감염병 감시 프로그램 강화도 시장 성장에 기여하고 있습니다. 한편, 진단 분야 주요 기업들의 통합과 틈새 혁신 기업에 대한 벤처 자금 유입은 경쟁 구도를 심화시키고 있으나, 교차 반응성 문제, 높은 자본 비용, 엄격한 다지역 규제로 인해 시장 도입 속도는 다소 둔화되고 있습니다.

세계의 면역분석 시장 동향 및 인사이트

만성 및 감염성 질환 유병률 증가

암, 심혈관 질환, 감염성 질환 부담이 가중되면서 전 세계 검사량이 지속적으로 재정의되고 있습니다. 순환 종양 DNA와 기존 단백질 바이오마커를 결합한 다중 매개변수 패널은 조기 진단 및 치료법 선택을 개선하고 있으며, CA724, 페리틴, B2-마이크로글로불린이 흉부암 지표로 확인된 연구가 이를 입증합니다. 심혈관대사 치료 분야에서는 고급 지단백질(a) 검사가 도입되었으며, 로슈의 티나-퀀트(Tina-quant) 검사는 FDA 승인을 받은 최초의 몰(mole) 기반 Lp(a) 측정법을 제공합니다. WHO 품질 보증 네트워크가 지원하는 전염병 감시는 시약 소비와 장비 설치를 더욱 가속화합니다.

고처리량 분석기의 급속한 기술 발전

자동화와 머신러닝은 이제 일상적인 실험실 워크플로우의 기반이 됩니다. 메이오 클리닉의 신장 결석 분광 분석용 AI 모델은 정확도를 유지하면서 검체당 검토 시간을 단축했습니다. 레비티의 CLIA 플랫폼은 시간당 60건의 검사를 48분 내 처리하며 단일클론 항체 특이성을 제공하는데, 이는 정밀 종양학 및 내분비학에 필수적인 조합입니다. 마이크로플루이딕 바이오센서는 유체 제어와 광학 검출을 단일 칩에 통합하여 검사 공간을 축소하고 진정한 무인 운영을 가능하게 합니다.

엄격한 다중 관할권 규제 승인

개발사들은 FDA, 유럽 IVDR, 여러 아시아 규제 체계 간 상이한 증거 요구사항에 직면하여 일정과 예산이 증가합니다. 동반진단(CDx)은 기관 간 협조 단계를 추가하는 반면, AI 기반 또는 다중 검사에 대한 지침은 여전히 파편화되어 있습니다. 글로벌 조화 부족으로 병행 검증 연구와 현장 감사가 필요해져 R&D 파이프라인과 제품 출시에서 자원이 소모됩니다.

부문 분석

시약 및 키트는 2024년 229억 달러의 매출을 기록하며 면역분석 시장 최대 비중을 차지했고, 공급업체에 예측 가능한 반복 수익원을 제공했습니다. 물량 증가는 검증되고 배치 간 일관성이 보장된 소모품이 필요한 일상적 감염병 패널, 만성질환 모니터링, 확대되는 글로벌 감시 프로그램에서 비롯됩니다. 다중 분석기 플랫폼 간 시약 상호운용성이 점점 더 중요해지면서, 제조사들은 린 실험실(Lean-Lab) 이니셔티브를 지원하는 범용 화학물질 및 CE 인증 대량 포장 제품에 투자하고 있습니다.

분석기 및 장비 부문은 연평균 성장률(CAGR) 5.34%로 가장 빠르게 확장되는 분야로, 실험실이 완전 자동화 및 고처리량 운영으로 전환하는 추세를 반영합니다. AI 기반 스케줄링 모듈은 이제 실행 순서와 유지보수 주기를 최적화하여 기술자 부족 문제를 완화합니다. 한편, 미들웨어는 면역분석 데이터를 LIS(실험실 정보 시스템) 및 병원 EHR(전자의무기록)과 연결하여 통합 임상 의사 결정 지원을 주도합니다. 그 결과, 기기용 면역분석 시장 규모는 2025년 76억 달러에서 2030년 99억 달러로 증가할 것으로 전망됩니다.

ELISA는 표준화된 프로토콜, 낮은 소모품 비용, 수십 년간 축적된 성능 증거를 바탕으로 2024년 매출 점유율 55.34%를 차지했습니다. 학술 및 지역사회 실험실 모두 사이토카인 패널, 내분비 마커, 자가면역 질환 검사에 ELISA를 계속 활용하며 강력한 기초 수요를 유지하고 있습니다. 그러나 감도 한계와 상대적으로 긴 배양 시간으로 인해 ELISA는 신흥 초저농도 분석물 응용 분야에 적합하지 않습니다.

연화광면역분석법(CLIA)은 연평균 복합 성장률(CAGR) 5.41%로 성장하며, 더 높은 분석 감도와 넓은 동적 범위를 제공하여 치료 약물 모니터링 및 종양 표지자 정량화에 선호되는 방법입니다. 멀티플렉스 마이크로어레이 플랫폼은 수십 개의 분석물을 동시에 검출하여 처리량을 높이며, 이는 현재 전환형 종양학 프로그램에서 필수적인 기능입니다. 결과적으로, ELISA가 상당한 설치 기반을 유지하고 있음에도 CLIA가 차지하는 면역분석 시장 점유율은 10년 말까지 30%로 상승할 것으로 전망됩니다.

지역 분석

북미는 강력한 보험급여 체계, NIH(미국국립보건원) 자금 지원, 획기적 진단법 대상 FDA 신속 심사 절차 등에 힘입어 2024년 41.12%의 매출 점유율을 유지했습니다. 로슈의 B세포 림프종 검사법과 같은 최근 승인 사례는 해당 지역의 혁신 속도를 보여줍니다. 바이오젠, 벡만 콜터, 후지리바이오의 알츠하이머 표지자 공동 연구는 면역분석 기반 동반진단법의 가치를 다시 한번 입증합니다. 미국은 노후 분석기를 시료 전처리 통합 완전 자동화 라인으로 교체 중이며, 캐나다는 보편적 접근성을, 멕시코는 공공 부문 입찰을 고감도 감염병 플랫폼으로 집중하고 있습니다.

아시아태평양 지역은 2030년까지 연평균 5.54% 성장률로 가장 빠르게 성장하는 지역입니다. 중국의 ‘메이드 인 차이나 2025’ 계획은 진단 장비 자급률을 가속화하고 있으며, 켐클린의 자동화 시스템은 시범 운영에서 전국적 도입 단계로 진전 중입니다. 인도의 체계화된 진단 시장은 웰니스 패키지와 가격 투명성에 힘입어 대도시 허브를 넘어 3 및 4선 도시로 확장되고 있습니다. 일본은 신속 승인 프로그램을 통해 재생의학 및 항암제 동반진단 검사를 장려하는 반면, 한국은 세액 공제 및 병원 테스트 베드를 통해 스타트업을 지원합니다. 동남아시아 국가들은 결핵 및 뎅기열 감시를 목표로 한 다자간 자금 지원의 혜택을 받아 벤치탑 플랫폼의 첫 구매자 기회를 창출하고 있습니다.

유럽은 IVDR 전환 과제로 출시 일정이 지연되고 있음에도 주요 수익 기여 지역으로 남아 있습니다. 독일과 프랑스는 중앙 집중식 검사 수요를 주도하고, 영국은 국민건강보험(NHS) 자금으로 조기 암 검진을 우선시하며, 스페인은 일차 진료 클리닉에서 현장진단(POCT) 프로그램을 확대하고 있습니다. 한편 중동 및 아프리카는 현재 규모는 작지만 걸프 국가 병원 건설과 아프리카 질병통제예방센터(CDC) 조달 계획 덕분에 검사량이 두 자릿수 성장률을 보이고 있습니다. 남미는 브라질의 통합 의료 서비스 업그레이드를 활용해 신생아 및 산전 검진을 확대하는 한편, 아르헨티나는 수입 제한 속에서 현지 시약 생산을 추진하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성 및 감염성 질환 유병률 증가

- 고처리량 분석기의 급속한 기술 발전

- 현장진단/가정용 신속검사 확대

- 정부 지원 글로벌 감시 및 예방접종 프로그램

- AI/ML 기반 초저농도 분석물 검출 플랫폼

- 실시간 생물공정 모니터링을 위한 PAT 면역분석법

- 시장 성장 억제요인

- 엄격한 다중 관할권 규제 승인

- 멀티플렉스 및 자동화 시스템의 높은 자본 비용

- 신개념 분석법의 교차 반응성 및 매트릭스 간섭

- 고순도 항체공급 체인 병목

- 가치 및 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 제품 및 서비스별

- 시약 및 키트

- 분석기기

- 소프트웨어 & 서비스

- 기술별

- 효소 결합 면역흡착 측정법(ELISA)

- 화학발광 면역분석(CLIA)

- 형광면역분석법(FIA)

- 방사면역측정법(RIA)

- 측면 유동 면역분석법(LFIA)

- 다중 및 마이크로어레이 면역분석법

- 기타(웨스턴 블롯, 면역 PCR)

- 용도별

- 감염증

- 종양학

- 심장병학

- 내분비학

- 자가면역질환

- 치료제 모니터링

- 신약 개발

- 기타

- 검체 유형별

- 혈액 및 혈청

- 타액

- 소변

- 기타 체액

- 최종 사용자별

- 병원

- 임상연구소

- 제약 및 생명공학 기업

- 학술기관 및 연구기관

- 현장 진료/재택치료

- 기타

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- F. Hoffmann-La Roche AG

- Siemens Healthineers AG

- Danaher Corporation(Beckman Coulter)

- Thermo Fisher Scientific Inc.

- Becton, Dickinson and Company

- Bio-Rad Laboratories Inc.

- Hologic Inc.

- Luminex Corporation

- Qiagen NV

- Sysmex Corporation

- Agilent Technologies Inc.

- PerkinElmer Inc.

- bioMerieux SA

- DiaSorin SpA

- Ortho Clinical Diagnostics

- Tosoh Bioscience

- Mindray Medical International

- Merck KGaA(Millipore Sigma)

- QuidelOrtho Corporation

제7장 시장 기회와 전망

HBR 25.11.07The immunoassays market is valued at USD 35.61 billion in 2025 and is projected to reach USD 45.42 billion by 2030, advancing at a 4.99% CAGR.

The forward trajectory reflects a mature yet steadily expanding space, underpinned by accelerating demand for oncology biomarkers, artificial-intelligence-enabled platforms, and real-time bioprocess monitoring. AI-enhanced devices now push immunoassay detection limits down to femtomolar ranges, as seen in Rice University's flow-cytometry instrument that delivers laboratory-grade accuracy in community clinics. Market growth also benefits from chemiluminescence immunoassay (CLIA) uptake in therapeutic drug monitoring and from heightened infectious-disease surveillance programs across emerging economies. Meanwhile, consolidation among diagnostics majors and venture funding in niche innovators intensify competitive dynamics, even as cross-reactivity issues, high capital costs, and stringent multi-region regulations temper adoption.

Global Immunoassays Market Trends and Insights

Rising Prevalence of Chronic & Infectious Diseases

Escalating cancer, cardiovascular, and infectious-disease burdens continue to redefine testing volumes worldwide. Multi-parameter panels that combine circulating tumor DNA with traditional protein biomarkers are improving early diagnosis and therapy selection, as evidenced by research identifying CA724, ferritin, and B2-microglobulin as thoracic cancer indicators. Cardiometabolic care has embraced advanced lipoprotein(a) assays, with Roche's Tina-quant test delivering the first molar-based Lp(a) measurement cleared by the FDA. Communicable-disease surveillance, supported by WHO quality-assurance networks, further accelerates reagent consumption and instrument installations.

Rapid Technological Advances in High-Throughput Analyzers

Automation and machine learning now underpin daily laboratory workflows. The Mayo Clinic's AI model for kidney-stone spectral analysis cut per-sample review time while preserving accuracy. CLIA platforms from Revvity deliver 60 tests per hour with 48-minute turnaround and monoclonal antibody specificity, a combination essential for precision oncology and endocrinology. Microfluidic biosensors integrate fluid control and optical detection on a single chip, shrinking assay footprints and permitting true walk-away operation.

Stringent Multi-Jurisdictional Regulatory Approvals

Developers face divergent evidence expectations across the FDA, European IVDR, and multiple Asian frameworks, inflating timelines and budgets. Companion diagnostics add layers of inter-agency coordination, while guidance for AI-enabled or multiplex assays remains fragmented. Lack of global harmonization compels parallel validation studies and onsite audits, draining resources from R&D pipelines and product launches.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Point-of-Care/Home-Based Rapid Tests

- Government-Funded Global Surveillance & Immunization Programs

- High Capital Cost of Multiplex & Automated Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents and kits generated USD 22.9 billion in revenue in 2024, translating into the single largest slice of the immunoassays market and providing predictable, recurring income streams for suppliers. Volume growth comes from routine infectious-disease panels, chronic-disease monitoring, and expanding global surveillance programs that require validated, lot-consistent consumables. Reagent interoperability across multiple analyzer platforms is increasingly important, prompting manufacturers to invest in universal chemistries and CE-marked bulk packs that support lean-lab initiatives.

Analyzers and instruments, the fastest-expanding category at a 5.34% CAGR, reflect laboratory moves toward full automation and high-throughput operations. AI-enabled scheduling modules now optimize run order and maintenance cycles, easing technician shortages. Meanwhile, middleware connects immunoassay data with LIS and hospital EHRs, driving integrated clinical decision support. As a result, the immunoassays market size for instruments is projected to rise from USD 7.6 billion in 2025 to USD 9.9 billion in 2030.

ELISA occupied 55.34% revenue share in 2024, anchored by standardized protocols, low consumable cost, and decades of accumulated performance evidence. Academic and community laboratories alike continue to rely on ELISA for cytokine panels, endocrine markers, and autoimmune screening, sustaining strong base demand. Yet sensitivity ceilings and relatively long incubation times limit ELISA's suitability for emerging ultra-low-analyte applications.

Chemiluminescence immunoassays, growing at a 5.41% CAGR, offer higher analytical sensitivity and wider dynamic range, making them the method of choice for therapeutic drug monitoring and tumor-marker quantification. Multiplex microarray platforms add throughput by simultaneously detecting dozens of analytes, a capability now indispensable in translational oncology programs. Consequently, the immunoassays market share commanded by CLIA is forecast to climb toward 30% by decade-end, even as ELISA retains a sizeable installed base.

The Immunoassays Market Report is Segmented by Product & Service (Reagents & Kits, Analyzers & Instruments, and More), Technology (ELISA, CLIA, and More), Application (Infectious Diseases, Oncology, and More), Specimen Type (Blood & Serum, Saliva, and More), End User (Hospitals, Clinical Laboratories, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained 41.12% revenue share in 2024, supported by strong reimbursement frameworks, NIH funding, and rapid FDA review pathways for breakthrough diagnostics. Recent clearances such as Roche's B-cell lymphoma assay illustrate the region's innovation cadence. Collaboration between Biogen, Beckman Coulter, and Fujirebio on Alzheimer's markers further demonstrates the value placed on immunoassay-based companion diagnostics. The United States continues to replace aging analyzers with fully automated lines integrating sample prep, while Canada emphasizes universal access and Mexico channels public-sector tenders toward high-sensitivity infectious-disease platforms.

Asia-Pacific is the fastest-growing region at 5.54% CAGR through 2030. China's Made-in-China 2025 plan accelerates diagnostic self-sufficiency, with Chemclin's automated systems moving from pilot to national rollout. India's organized diagnostics sector is expanding beyond metropolitan hubs into tier-3 and tier-4 cities, aided by wellness packages and price transparency. Japan incentivizes regenerative-medicine and oncology companion tests via fast-track approval programs, while South Korea supports start-ups through tax credits and hospital test beds. Southeast Asian nations benefit from multilateral funding aimed at tuberculosis and dengue surveillance, creating first-time buyer opportunities for bench-top platforms.

Europe remains a major revenue contributor, although IVDR transition challenges extend launch timelines. Germany and France anchor centralized testing demand, the United Kingdom prioritizes early cancer detection via NHS funding, and Spain expands point-of-care programs in primary-care clinics. Meanwhile, the Middle East and Africa, though smaller today, show double-digit test-volume growth thanks to Gulf state hospital construction and African CDC procurement initiatives. South America leverages Brazil's unified health-service upgrades to expand neonatal and prenatal screening, while Argentina pushes for local reagent production amid import restrictions.

- Abbott Laboratories

- Roche

- Siemens Healthineers

- Danaher

- Thermo Fisher Scientific

- Beckton Dickinson

- Bio-Rad Laboratories

- Hologic

- Luminex

- QIAGEN

- Sysmex

- Agilent Technologies

- PerkinElmer

- bioMerieux

- DiaSorin

- Ortho Clinical Diagnostics

- Tosoh

- Mindray

- Merck

- QuidelOrtho

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Chronic and Infectious Diseases

- 4.2.2 Rapid Technological Advances in High-throughput Analyzers

- 4.2.3 Expansion of Point-of-care/Home-based Rapid Tests

- 4.2.4 Government-funded Global Surveillance & Immunization Programs

- 4.2.5 AI/ML-enabled Ultra-low-analyte Detection Platforms

- 4.2.6 PAT Immunoassays for Real-time Bioprocess Monitoring

- 4.3 Market Restraints

- 4.3.1 Stringent Multi-jurisdictional Regulatory Approvals

- 4.3.2 High Capital Cost of Multiplex & Automated Systems

- 4.3.3 Cross-reactivity & Matrix Interferences in Novel Assays

- 4.3.4 Supply-chain Bottlenecks for High-purity Antibodies

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value - USD million)

- 5.1 By Product & Service

- 5.1.1 Reagents & Kits

- 5.1.2 Analyzers & Instruments

- 5.1.3 Software & Services

- 5.2 By Technology

- 5.2.1 Enzyme-Linked Immunosorbent Assay (ELISA)

- 5.2.2 Chemiluminescence Immunoassay (CLIA)

- 5.2.3 Fluorescence Immunoassay (FIA)

- 5.2.4 Radioimmunoassay (RIA)

- 5.2.5 Lateral Flow Immunoassay (LFIA)

- 5.2.6 Multiplex & Microarray Immunoassays

- 5.2.7 Others (Western Blot, Immuno-PCR)

- 5.3 By Application

- 5.3.1 Infectious Diseases

- 5.3.2 Oncology

- 5.3.3 Cardiology

- 5.3.4 Endocrinology

- 5.3.5 Autoimmune Disorders

- 5.3.6 Therapeutic Drug Monitoring

- 5.3.7 Drug Discovery & Development

- 5.3.8 Others

- 5.4 By Specimen Type

- 5.4.1 Blood & Serum

- 5.4.2 Saliva

- 5.4.3 Urine

- 5.4.4 Other Body Fluids

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Clinical Laboratories

- 5.5.3 Pharmaceutical & Biotechnology Companies

- 5.5.4 Academic & Research Institutes

- 5.5.5 Point-of-Care / Home-Care Settings

- 5.5.6 Others

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 F. Hoffmann-La Roche AG

- 6.3.3 Siemens Healthineers AG

- 6.3.4 Danaher Corporation (Beckman Coulter)

- 6.3.5 Thermo Fisher Scientific Inc.

- 6.3.6 Becton, Dickinson and Company

- 6.3.7 Bio-Rad Laboratories Inc.

- 6.3.8 Hologic Inc.

- 6.3.9 Luminex Corporation

- 6.3.10 Qiagen N.V.

- 6.3.11 Sysmex Corporation

- 6.3.12 Agilent Technologies Inc.

- 6.3.13 PerkinElmer Inc.

- 6.3.14 bioMerieux SA

- 6.3.15 DiaSorin S.p.A.

- 6.3.16 Ortho Clinical Diagnostics

- 6.3.17 Tosoh Bioscience

- 6.3.18 Mindray Medical International

- 6.3.19 Merck KGaA (Millipore Sigma)

- 6.3.20 QuidelOrtho Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment