|

시장보고서

상품코드

1844634

배출 제어 촉매 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Emission Control Catalysts - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

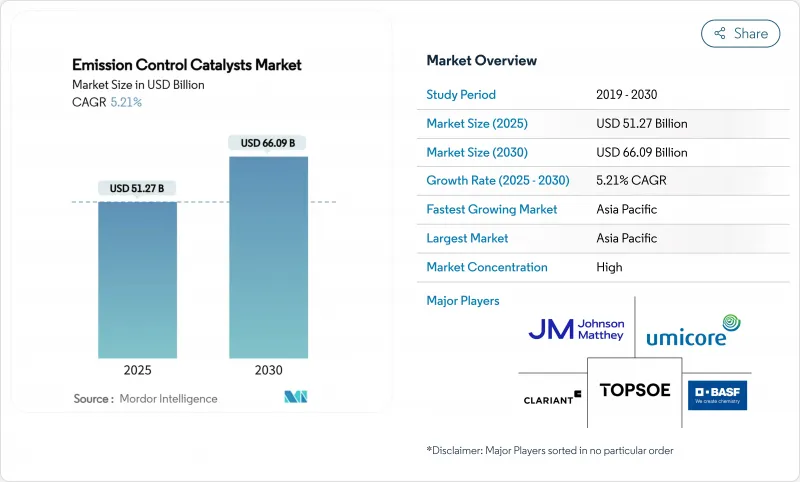

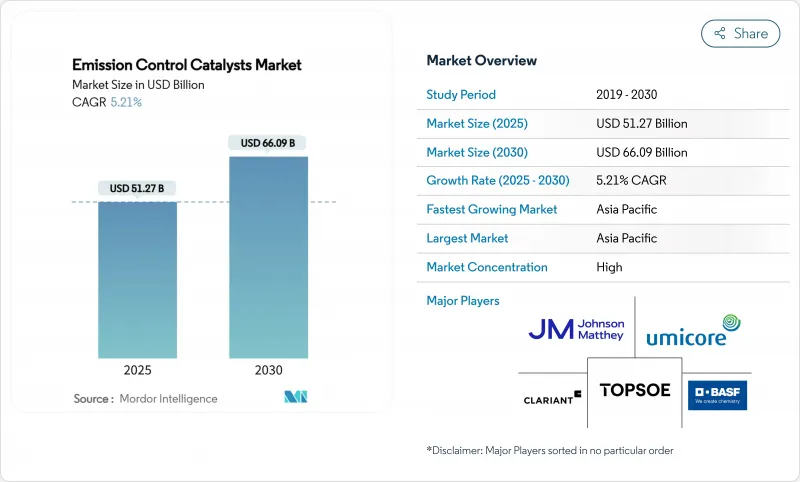

배출 제어 촉매 시장 규모는 2025년에 512억 7,000만 달러로 평가되었고, 2030년에는 660억 9,000만 달러에 이를 것으로 예측되며, CAGR 5.21%로 성장할 전망입니다.

전 세계적으로 강화된 배기 가스 기준, 신흥 경제국에서의 내연 기관 수요 회복, 지속적인 촉매 혁신이 이러한 성장을 뒷받침하고 있습니다. EU, 미국, 중국, 인도의 규제 기관들은 미세먼지 및 질소산화물(NOx) 배출 한도를 강화하여 신차에 첨단 후처리 기술의 거의 보편적인 채택을 촉진하고 있습니다. 자동차 제조사들은 동시에 성능 저하 없이 귀금속 부하를 줄이고 가격 변동성을 상쇄하며 백금 대체를 가속화하기 위해 촉매 조성을 개선하고 있습니다. 대기질 규제가 고정 배출원으로 확대됨에 따라 산업 및 발전 고객들도 유사한 기술을 채택하고 있습니다. 따라서 배출 제어 촉매 시장은 지속적인 자동차 판매량과 확대되는 산업적 채택이라는 이중 성장 동력의 혜택을 받아 견고한 전망을 뒷받침하고 있습니다.

세계의 배출 제어 촉매 시장 동향 및 인사이트

도로 및 비도로 배출 규제의 엄격한 강화

유로 7 규정은 허용 미립자 수준을 낮추고 실제 주행 테스트를 요구하여 가솔린 미립자 필터(GPF)와 업그레이드된 3원 촉매(Three-Way Catalysts)의 보편적 사용을 강제합니다. 중국 VI 및 인도 BS VI 규정도 유사한 목표를 가지고 있으며, 이는 아시아 전역의 차량 군에 SCR 및 GPF의 광범위한 도입을 촉진합니다. 북미의 Tier 4 비도로 기준은 건설 및 농업 기계에도 동등한 수준의 엄격함을 적용하여 촉매 수요를 확대합니다. 이러한 규제 체계들은 특히 개발도상국들이 모범 사례 법안을 도입함에 따라 배출 제어 촉매 시장이 성장 모멘텀을 유지하도록 보장합니다.

소형차와 대형차의 생산 대수가 급회복

2024년 세계 소형 상용차 생산 대수는 8% 증가했으며, 인프라 중심 경제권에서는 상용차 생산이 강하게 회복되어 촉매 단위 출하량 증가로 직접 연결되었습니다. 이러한 회복세는 새로운 규제 단계와 맞물려 생산량이 증가하는 가운데 OEM들이 더욱 정교한 후처리 장치를 장착하도록 강제하고 있습니다. 대형 차량 군의 전기화 진전은 여전히 미미하여 디젤 SCR 및 DOC 솔루션이 2030년까지 필수적일 전망입니다. 이러한 생산량 회복과 강화되는 기준 간의 상호작용은 촉매 공급업체의 건실한 주문 파이프라인을 뒷받침합니다.

가격 변동성 및 다가오는 팔라듐 공급 과잉이 OEM 구매를 위축

World Platinum Investment Council(세계백금투자평의회)은 재활용이 확대되고 광산 공급이 견조하게 추이하기 때문에 2025년에는 900koz 가까운 팔라듐이 공급 부족에서 공급 잉여로 변할 것으로 예상했습니다. 자동차 제조사들은 나노 공학 표면을 통해 백금 대체를 강화하고 전체 PGM 부하량을 낮춰 촉매 비용을 절감하는 방식으로 대응하고 있습니다. 단기적 변동성은 여전히 조달을 복잡하게 만들어 OEM들이 장기 계약 및 다각화된 조달 전략으로 기울게 합니다.

부문 분석

2024년 배출 제어 촉매 시장의 48.16%를 팔라듐은 48.16% 점유율로 가솔린 3원 촉매 분야의 우위를 공고히 했습니다. 백금 대체 증가로 백금은 약 35%로 뒤를 이었으며, 로듐은 독특한 NOx 선택성으로 12%의 틈새 시장을 유지했습니다. 2024년 배출 제어 촉매 시장 규모는 해당 세그먼트 합산 약 247억 달러를 기록했습니다. 향후 전망으로는 OEM 업체들이 팔라듐 과잉 위험 완화를 위해 금속 혼합 비율을 재조정함에 따라 백금의 연평균 복합 성장률(CAGR) 6.71%가 가장 높은 성장률을 보일 전망입니다. 액체 갈륨-팔라듐 합금 및 나노 구조 클러스터와 같은 신흥 응용 분야는 훨씬 낮은 부하량으로도 동등한 전환 효율을 제공하여 비용 절감 여지를 확대할 것으로 기대됩니다.

제조사들은 PGM 회수를 위해 폐쇄형 재활용을 확대 적용하며 공급 안정화와 현금 노출 감소 효과를 거두고 있습니다. 남아프리카 광산업체들은 자본 지출을 재검토 중이지만, 장기 촉매 연구에 따르면 저공해 연소 및 메탄올 엔진에서 팔라듐의 중요성은 지속될 전망입니다. 따라서 배출 제어 촉매 시장은 10년간 상대적 점유율이 변동하더라도 다중 금속 기반 구조를 유지할 것입니다.

3원 촉매는 2024년 매출의 55.19%를 차지했으며, 이는 전 세계 가솔린 차량에 거의 보편적으로 장착됨을 반영합니다. 디젤 산화 촉매, 디젤/GPF 필터, SCR 시스템은 합산 매출의 약 1/3을 차지했으며, 이들의 성장은 대형차 및 비도로 부문과 연계되어 있습니다. 신흥 나노 구조 설계는 현재 연평균 6.96% 성장률을 보이며 석유화학 및 저온 응용 분야에서 상업적 규모에 진입했습니다. 이 가운데 배출 제어 촉매 시장 점유율은 유로 7 및 중국 VII 규제를 반영해 가솔린 미립자 필터를 통합한 하이브리드 최적화 삼원촉매로의 전환이 점진적으로 가속화될 전망입니다.

적층 제조는 또 다른 전환점입니다. BASF의 X3D 프린팅 기술은 복잡한 채널 형상을 구현해 표면적을 증가시키고 배압을 감소시켜 상업 시험에서 효율을 1% 향상시켰습니다. AI 기반 구리-제올라이트 배합은 저온 SCR 전환율을 높여 도시 배송 트럭의 유로 7 기준 충족에 필수적입니다. 이러한 진보는 성능 차별화가 가격 결정력을 유지함에 따라 배출 제어 촉매 시장을 상품화로부터 보호합니다.

지역 분석

아시아태평양 지역은 2024년 배출 제어 촉매 시장에서 36.52%의 점유율로 선두를 차지했으며, 매출액은 187억 달러를 넘어섰습니다. 이 지역의 7.02% CAGR은 강력한 차량 생산, 급속한 산업화, 그리고 저온 SCR 및 범용 GPF 사용을 요구하는 중국 VI-B 규범 시행에 힘입어 추진됩니다. 인도의 BS VI 제도 역시 차량당 촉매 부하량을 증가시키는 동시에 연료 품질 개선으로 황 관련 중독을 감소시킵니다. 일본과 한국은 학계-산업계 컨소시엄을 통한 혁신적 나노촉매 프로젝트 지원을 바탕으로 연구 리더십을 발휘하고 있습니다. ASEAN 국가들은 유엔 수준의 동등성 기준을 따르며, 유로 6 수준으로 기준이 강화됨에 따라 점진적인 물량 증가 추세를 보이고 있습니다.

북미와 유럽은 2024년 매출의 53%를 차지했으며, 이들 시장은 단순한 단위 성장보다는 첨단 기술로 특징지어진다. 미국 환경보호청(EPA)의 2027년 이후 경차 규제는 차량군 평균 온실가스 배출량 50% 감축을 목표로 하여, 광범위한 하이브리드화 및 냉시동 시나리오에서의 귀금속(PGM) 사용 증가를 촉진합니다. 유로 7의 실제 주행 테스트 확대(브레이크 및 타이어 마모 포함)는 2차 여과 시스템 연구개발을 촉발하여 공급업체 포트폴리오를 확대합니다. 양 지역은 산업용 촉매 교체 주기도 주도하고 있습니다. 발전사는 노후 석탄 설비를 개조해 질소산화물(NOx) 배출 피크를 억제하고 있으며, 석유화학 업체들은 적층 제조 방식의 격자형 촉매를 시험 중입니다.

남미와 중동 및 아프리카 지역은 2024년 배출 제어 촉매 시장의 10.48%를 차지했으나 가장 높은 성장 잠재력을 보유하고 있습니다. 브라질의 에탄올-디젤 혼합 연료는 미립자 배출을 44% 감소시켰으나, 알데히드 유출 관리용 산화 촉매가 여전히 필요합니다. 걸프협력회의(GCC) 국가들은 연료 기준을 유로 5와 일치시키기 위해 움직이며, 고황 저항성 제형에 대한 새로운 수요를 촉발하고 있습니다. 사하라 이남 아프리카 전역의 디젤 발전기 세트 도입은 지역 대기질 법규가 성숙되면 고정식 촉매 수요를 점진적으로 증가시킬 것입니다. 전반적으로 규제 수렴이 가속화되면서 개발도상 지역 전반에 걸쳐 꾸준한 장기적 수요 증가가 예상됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 도로 및 비도로 배출 규제의 엄격한 강화

- 소형차 및 대형차 생산의 급속한 회복

- 대기질과 공중위생에 대한 관심 증가

- 산업 및 전력 부문의 채택 확대

- 자동차 산업의 확장

- 시장 성장 억제요인

- 가격 변동성 및 팔라듐 공급 과잉 우려로 인한 OEM 구매 위축

- 전기차(BEV) 보급 가속화로 인한 자동차 촉매 수요 성장 둔화

- 개발도상국 고황 함유 대체 연료로 인한 촉매 중독 현상

- 밸류체인 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 금속별

- 백금

- 팔라듐

- 로듐

- 기타 금속(바나듐, 구리-아연 등)

- 기술별

- 3원 촉매(TWC)

- 디젤 산화 촉매(DOC)

- 디젤/GPF 미립자 필터(DPF/GPF)

- 선택 촉매 환원(SCR)

- 린 NOx 트랩과 NSC

- 새로운 나노구조 촉매

- 용도별

- 이동 배기 가스 규제

- 거치 배기 가스 규제

- 최종 사용자 산업별

- 자동차

- 산업용

- 기타 최종 사용자 산업(항공우주, 발전 등)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- Aerinox Inc.

- ANAND Group

- BASF

- CATALER CORPORATION

- CDTi Advanced Materials Inc.

- Clariant

- CORMETECH

- Cummins Inc.,

- DCL International Inc.

- Evonik Industries AG

- Haldor Topsoe A/S

- Heraeus Precious Metals

- IBIDEN

- Johnson Matthey

- Kanadevia Corporation

- NEO

- NGK INSULATORS, LTD.

- Nikki-Universal Co., Ltd.

- SINOTECH Company Limited

- Umicore

제7장 시장 기회와 전망

HBR 25.11.07The emission control catalysts market size is valued at USD 51.27 billion in 2025 and is set to reach USD 66.09 billion by 2030, advancing at a 5.21% CAGR.

Heightened global emission standards, resilient internal-combustion demand in emerging economies, and continuous catalyst innovation sustain this expansion. Regulatory bodies in the EU, the US, China, and India have tightened particulate and NOx limits, spurring near-universal adoption of advanced after-treatment technologies in new vehicles. Automakers are simultaneously refining catalyst formulations to lower precious-metal loadings, offset price volatility, and accelerate platinum substitution without compromising performance. Industrial and power-generation customers are also adopting similar technologies as air-quality rules broaden to cover stationary sources. The emission control catalysts market therefore benefits from a dual growth engine-persistent automotive volumes and widening industrial uptake-underpinning its robust outlook.

Global Emission Control Catalysts Market Trends and Insights

Stringent tightening of on-road & off-road emission norms

Euro 7 rules lower permissible particulate levels and require real-world driving tests, compelling universal use of gasoline particulate filters and upgraded Three-Way Catalysts. Similar ambitions shape China VI and India BS VI regulations, which drive widespread SCR and GPF deployment across Asia's vehicle fleets. Tier 4 off-road standards in North America extend comparable stringency to construction and agricultural machinery, broadening catalyst demand. Together, these frameworks ensure the emission control catalysts market maintains growth momentum, especially as developing economies replicate best-practice legislation.

Rapid rebound of light-duty & heavy-duty vehicle production

Global light-vehicle output climbed 8% in 2024, while commercial-vehicle production recovered strongly in infrastructure-focused economies, translating directly into higher catalyst unit shipments. The upturn coincides with new regulatory phases, forcing OEMs to install more sophisticated after-treatment even as production volumes rise. Electrification progress in heavy-duty fleets remains modest, meaning diesel SCR and DOC solutions will stay essential through 2030. This interplay between volume rebound and tightening standards supports a healthy order pipeline for catalyst suppliers.

Price volatility & looming surplus of palladium depressing OEM purchasing

World Platinum Investment Council forecasts a swing from deficit to a surplus of nearly 900 koz of palladium by 2025 as recycling expands and mining supply stays firm. Automakers respond by intensifying platinum substitution and lowering overall PGM loadings through nano-engineered surfaces, trimming catalyst costs. Short-term volatility still complicates procurement, nudging OEMs toward long-term contracts and diversified sourcing strategies.

Other drivers and restraints analyzed in the detailed report include:

- Growing concern for air quality and public health

- Increasing adoption by industrial and power sector

- Accelerated BEV penetration eroding autocatalyst demand growth

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Palladium held 48.16% of the emission control catalysts market in 2024, underpinning its primacy in gasoline Three-Way Catalysts. Platinum followed at nearly 35% on the back of rising substitution, while rhodium's unique NOx selectivity kept its 12% niche. The combined segment represented roughly USD 24.7 billion of emission control catalysts market size in 2024. Looking ahead, platinum's 6.71% CAGR makes it the fastest riser as OEMs rebalance metal mixes to mitigate palladium surplus risk. Emerging applications such as liquid-gallium palladium alloys and nano-structured clusters promise equivalent conversion at far lower loadings, widening cost headroom.

Manufacturers increasingly deploy closed-loop recycling to reclaim PGMs, smoothing supply and lowering cash exposure. South African miners reevaluate capex, yet long-term catalyst research indicates continued palladium relevance in lean-burn and methanol engines. The emission control catalysts market therefore retains a multi-metal foundation even as relative shares shift through the decade.

Three-Way Catalysts controlled 55.19% revenue in 2024, reflecting their near-universal fitment on global gasoline vehicles. Diesel Oxidation Catalysts, Diesel/GPF filters, and SCR systems collectively equaled about one-third of revenues, their growth tied to heavy-duty and off-road sectors. Emerging nano-structured designs now grow at 6.96% CAGR, reaching critical commercial scale in petrochemical and low-temperature applications. Within this mix, emission control catalysts market share is expected to tilt progressively toward hybrid-optimized TWCs integrating gasoline particulate filters in response to Euro 7 and China VII legislation.

Additive manufacturing is another inflection point: BASF's X3D printing enables complex channel geometries that raise surface area and cut back-pressure, improving efficiency by 1% in commercial trials. AI-driven copper-zeolite formulations enhance low-temperature SCR conversion, a crucial requirement for Euro 7 compliance in urban delivery trucks. Such advances safeguard the emission control catalysts market from commoditization, as performance differentiation continues to command pricing power.

The Emission Control Catalysts Market Report is Segmented by Metal (Platinum, Palladium, and More), Technology (Three-Way Catalysts, Diesel Oxidation Catalysts, and More), Application (Mobile Emission Control and Stationary Emission Control), End-User Industry (Automotive, Industrial, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the emission control catalysts market with 36.52% share in 2024, exceeding USD 18.7 billion in sales. The region's 7.02% CAGR is propelled by robust vehicle production, rapid industrialization, and the implementation of China VI-B norms that demand low-temperature SCR and universal GPF usage. India's BS VI regime similarly boosts catalyst loading per vehicle, while fuel-quality upgrades reduce sulfur-related poisoning. Japan and South Korea contribute research leadership, backing breakthrough nano-catalyst projects with academic-industry consortia. ASEAN nations, following UN-level equivalence, represent an incremental volume tailwind as their standards tighten toward Euro 6 parity.

North America and Europe together held 53% of 2024 revenues, their markets defined by advanced technology rather than raw unit growth. The US EPA's 2027-plus light-vehicle rules target a 50% fleet-average GHG cut, compelling widespread hybridization and elevated PGM use in cold-start scenarios. Euro 7's real-world testing extension to brake and tire wear triggers R&D for secondary filtration systems, broadening supplier portfolios. Both regions also lead industrial catalyst replacement cycles, with utilities retrofitting aged coal assets to curb NOx peaks and petrochemical outfits trialing additive-manufactured lattice catalysts.

South America and the Middle East & Africa combined accounted for 10.48% of the emission control catalysts market in 2024 but present the highest catch-up potential. Brazil's ethanol-diesel blends cut particulate output by 44%, yet still require oxidation catalysts to manage aldehyde slip. Gulf Cooperation Council states move to align fuel standards with Euro 5, prompting fresh demand for high-sulfur-resistant formulations. Diesel genset adoption across Sub-Saharan Africa adds incremental stationary catalyst volumes once local air-quality legislation matures. Overall, rising regulatory convergence guides steady long-term uptake across developing regions.

- Aerinox Inc.

- ANAND Group

- BASF

- CATALER CORPORATION

- CDTi Advanced Materials Inc.

- Clariant

- CORMETECH

- Cummins Inc.,

- DCL International Inc.

- Evonik Industries AG

- Haldor Topsoe A/S

- Heraeus Precious Metals

- IBIDEN

- Johnson Matthey

- Kanadevia Corporation

- NEO

- NGK INSULATORS, LTD.

- Nikki-Universal Co., Ltd.

- SINOTECH Company Limited

- Umicore

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent tightening of on-road & off-road emission norms

- 4.2.2 Rapid rebound of light-duty & heavy-duty vehicle production

- 4.2.3 Growing concern for air quality and public health

- 4.2.4 Increasing adoption by industrial and power sector

- 4.2.5 Expansion of the automotive sector

- 4.3 Market Restraints

- 4.3.1 Price volatility & looming surplus of palladium depressing OEM purchasing

- 4.3.2 Accelerated BEV penetration eroding autocatalyst demand growth

- 4.3.3 Catalyst poisoning from higher-sulfur alternative fuels in developing regions

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Metal

- 5.1.1 Platinum

- 5.1.2 Palladium

- 5.1.3 Rhodium

- 5.1.4 Other Metals (Vanadium, Cu-Zn, etc.)

- 5.2 By Technology

- 5.2.1 Three-Way Catalysts (TWC)

- 5.2.2 Diesel Oxidation Catalysts (DOC)

- 5.2.3 Diesel/GPF Particulate Filters (DPF/GPF)

- 5.2.4 Selective Catalytic Reduction (SCR)

- 5.2.5 Lean NOx Traps & NSC

- 5.2.6 Emerging Nano-Structured Catalysts

- 5.3 By Application

- 5.3.1 Mobile Emission Control

- 5.3.2 Stationary Emission Control

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Industrial

- 5.4.3 Other End user Industries (Aerospace, Power Generation, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Aerinox Inc.

- 6.4.2 ANAND Group

- 6.4.3 BASF

- 6.4.4 CATALER CORPORATION

- 6.4.5 CDTi Advanced Materials Inc.

- 6.4.6 Clariant

- 6.4.7 CORMETECH

- 6.4.8 Cummins Inc.,

- 6.4.9 DCL International Inc.

- 6.4.10 Evonik Industries AG

- 6.4.11 Haldor Topsoe A/S

- 6.4.12 Heraeus Precious Metals

- 6.4.13 IBIDEN

- 6.4.14 Johnson Matthey

- 6.4.15 Kanadevia Corporation

- 6.4.16 NEO

- 6.4.17 NGK INSULATORS, LTD.

- 6.4.18 Nikki-Universal Co., Ltd.

- 6.4.19 SINOTECH Company Limited

- 6.4.20 Umicore

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment