|

시장보고서

상품코드

1844668

크로마토그래피 레진 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Chromatography Resins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

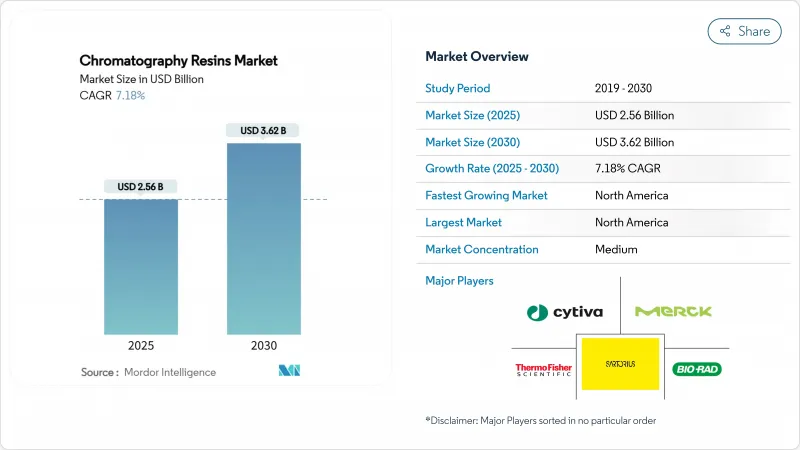

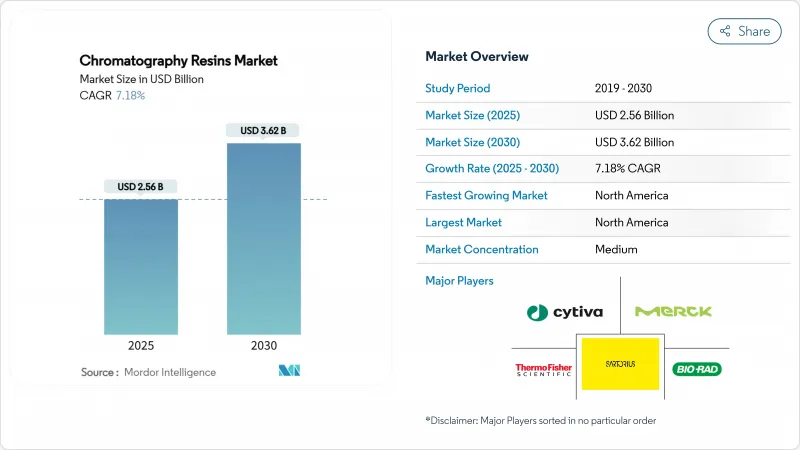

크로마토그래피 레진 시장 규모는 2025년에 25억 6,000만 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR은 7.18%를 나타낼 것으로 예측되며, 2030년에는 36억 2,000만 달러에 달할 전망입니다.

꾸준한 성장은 바이오의약품 정제 과정에서 해당 부문의 핵심적 역할을 반영합니다. 다운스트림 공정 단계는 여전히 전체 의약품 제조 비용의 약 60%를 차지합니다(Avantor). 제품 순도에 대한 규제 강화, 고속 유동 레진가 필요한 연속 바이오공정 채택 증가, 치료제 파이프라인 확대가 수요를 함께 끌어올리고 있습니다. 사이티바(Cytiva)와 팔(Pall)의 15억 달러 규모 다단계 확장 같은 생산 능력 투자는 지역별 공급 격차를 줄이고 안정적인 조달 전략을 강화하고 있습니다. 동시에 개발사들은 재현성 확보를 위해 합성 매트릭스로 전환하는 한편, 지속가능성 요구에 따라 천연 아가로즈 등급이 틈새 시장에서 모멘텀을 얻고 있습니다.

세계의 크로마토그래피 레진 시장 동향 및 인사이트

단일클론항체 제조 수요 증가

세계의 mAb 생산량은 2030년까지 연평균 13.23% 성장률로 지속 증가할 전망이며, 항체 역가가 10g/L를 초과함에 따라 레진 소비량도 함께 증가하여 Protein A 베드의 용량 한계를 압박하고 있습니다. Toyopearl GigaCap S-650M과 같은 고용량 대체재는 90g/L 이상의 동적 결합능력을 제공하여 기존 매체의 성능을 두 배 이상 뛰어넘습니다. 항암제 적응증이 치료 가치의 51%를 차지하며, 자가면역 파이프라인이 가장 빠르게 확장되면서 정제 수요가 확대되고 있습니다. 북미는 항체 생산량의 41.04% 점유율을 유지하지만, 아시아태평양 지역은 연평균 13.24% 성장률로 레진 수요 중심지를 다각화하고 있습니다. 현재 체외 생산이 mAb 공급량의 78%를 차지하며, 다운스트림 레진 기술이 글로벌 바이오의약품 접근성을 뒷받침하는 핵심 요소임을 보여줍니다.

신흥 시장에서 백신 파이프라인 확대

팬데믹 이후 인도, 중국, 브라질, 인도네시아의 생산 능력 확대로 백신 수요가 지속적으로 증가하며, 바이러스 및 플라스미드 불순물을 효율적으로 제거하는 레진 수요가 높아지고 있습니다. 바이오-래드(Bio-Rad)의 CHT 세라믹 하이드록시아파타이트(CHT Ceramic Hydroxyapatite)는 인플루엔자 및 뎅기 바이러스 입자의 75% 이상을 포집하면서 숙주 단백질을 90%까지 제거합니다. Repligen/Navigo의 스파이크 단백질 친화성 레진와 같은 신규 리간드는 mRNA 및 바이러스 벡터 백신을 위한 맞춤형 솔루션을 대표합니다. EMA부터 WHO에 이르는 규제 기관들은 이제 강력한 바이러스 제거 연구를 요구하며, 이는 레진 개발사들로 하여금 대규모 백신 플랫폼을 위한 높은 선택성과 유동성 안정성을 검증하도록 촉진하고 있습니다.

높은 레진 조달 및 검증 비용

프로테인 A 레진 가격이 리터당 9,000-1만 2,000달러로 상승했음에도 대부분의 제품은 40g/L 미만으로 결합하여 임상 및 상업 생산 예산에 부담을 주고 있습니다. 15주를 초과하는 긴 리드 타임으로 인해 기업들은 안전 재고를 늘리고 운전자본을 묶어야 합니다. 공급업체 또는 로트 변경 시마다 비교 시험이 필요해져 일정이 연장되고 방대한 문서 작업이 요구되어 전체 검증 비용이 증가합니다. 중소 기업 및 신흥 시장 공장은 이러한 비용을 감당하기 어려워 국내 생산 규모 확대가 지연되고 있습니다.

부문 분석

합성 기반 소재는 2024년 매출의 76.34%를 차지했으며, 이는 제조업체들이 배치 간 일관성과 높은 기계적 강도를 선호함을 반영합니다. 이러한 특성 덕분에 더 높은 컬럼, 더 빠른 유속, 간편한 규모 확대가 가능해지며, 이는 생산 주기가 지속적으로 단축되는 크로마토그래피 레진 시장에 매우 중요합니다. 반면 천연 매체(주로 아가로즈)는 불안정 단백질을 보호하는 온화한 화학적 특성을 유지하여 틈새 백신 및 유전자 치료 벡터 시장에 적합합니다. 천연 부문 8.61%의 예상 연평균 성장률(CAGR)은 재생 가능한 원료와 낮은 환경 발자국에 대한 관심 재점화를 시사하며, 특히 친환경 제조 인센티브가 존재하는 유럽에서 두드러집니다.

도입 패턴은 이중 구조를 보여줍니다. 다국적 기업들은 연속 항체 포집을 위해 합성 폴리메타크릴레이트 베드를 설치하는 반면, 지역 계약 제조업체들은 다중 제품 라인을 위해 아가로즈나 셀룰로오스로 생산 능력을 확장합니다. 외래 병원체 위험에 대한 규제적 주목은 기업의 선호도를 합성재로 더욱 전환시키고 있지만, 생체 적합성 우려는 여전히 천연 등급을 소아과 및 세포 치료 파이프라인으로 끌어들이고 있습니다. 두 형식 모두 고급 리간드 화학 기술을 강화함에 따라, 크로마토그래피 레진 시장에서 경쟁은 기본 매트릭스보다는 동적 용량 및 알칼리 안정성과 같은 성능 속성을 중심으로 전개될 것입니다.

이온 교환 레진는 2024년 매출의 39.25%를 차지하며 포집, 중간체, 정제 단계 전반에 걸친 수십 년간의 역할을 공고히 했습니다. 이들의 넓은 작동 범위, 확장성, 상대적 경제성은 거의 모든 치료용 단백질에 적합합니다. 그러나 혼합 모드 및 다중 모드 매체는 연간 8.25% 복합 성장률을 보일 전망입니다. 이온성, 소수성, 수소 결합 상호작용이 결합되어 응집체와 숙주 세포 단백질을 단일 단계로 제거함으로써 완충액 사용량과 스키드 설치 공간을 줄일 수 있기 때문입니다.

고가임에도 IgG 포집에는 여전히 단백질 A 컬럼이 필수적이며, 소수성 상호작용 장치는 연속 정제 공정에서 응집을 완화합니다. 크기 배제 장치는 전단력 없이 완충액 교환 또는 탈염을 수행하며, 이 틈새 시장의 크로마토그래피 레진 규모는 연평균 8.12% 성장률로 꾸준히 확대될 전망입니다. 이중특이성 항체와 바이러스 벡터 수요에 힘입어 리간드 결합 맞춤형 솔루션이 파일럿 규모로 꾸준히 도입되고 있습니다. 공정 고도화 로드맵은 다중 모드 침대가 순차적 이온 교환 및 HIC 공정을 점차 대체할 것임을 시사하며, 이는 크로마토그래피 레진 시장 내 가치 구조의 변화를 강조합니다.

크로마토그래피 레진 시장 보고서는 원산지(천연 기반 및 합성 기반), 기술(이온 교환 크로마토그래피 레진, 친화성 크로마토그래피 레진 등), 제품 유형(단백질-A, 이온 교환 등), 최종 사용자 산업(제약, 수자원 및 환경 기관 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류됩니다.

지역 분석

북미는 2024년 매출 기여도 42.75%로 선두를 달렸으며, 2030년까지 8.48%의 가장 빠른 지역 CAGR을 기록할 것으로 예상됩니다. 사이티바(Cytiva)와 팔(Pall)의 15억 달러 규모 프로그램, 그리고 퓨로라이트(Purolite)의 펜실베이니아 신규 아가로즈 공장 등 공격적인 투자는 리드 타임 단축과 바이오프로세스 공급망 안정화를 목표로 합니다. 2024년 강화된 FDA 분석 가이드라인은 전 세계적으로 레진 일관성에 대한 기대치를 높이며, 북미의 규제 기준 허브 지위를 공고히 하고 있습니다.

유럽은 오랜 GMP 전문성과 지속가능성에 대한 강조 증가를 결합하여 가치 기준 2위를 차지했습니다. EMA 공정 검증 규정은 고해상도 분리를 요구하며 재활용 가능하거나 폐기물 발생이 적은 매트릭스를 선호합니다. Merck KGaA의 다름슈타트 3억 유로 연구 허브, Tosoh Bioscience의 독일 확장 등 투자는 국내 공급망을 강화합니다. 친환경 제조 인센티브는 크로마토그래피 레진 시장 내 생물 기반 아가로즈 및 폐쇄형 용매 시스템으로의 전환을 촉진합니다.

아시아태평양 지역은 중국, 일본, 한국의 생물학적 제제 프로그램과 아세안(ASEAN) 백신 계획에 힘입어 가장 활발한 구조적 확장을 기록하고 있습니다. 도시의 요카이치 신규 공장은 지역 수요에 맞춘 생산 능력 조정의 사례다. 정책 입안자들은 현지 단클론항체(mAb) 및 세포치료제 공장에 보조금을 지원하며, 다국적 기업들의 현지 생산 확대에 따라 고용량 레진 소비를 촉진하고 있습니다. 인도와 인도네시아는 팬데믹 대비 비축 물량을 늘리며 연속 유동 호환 배지의 고객 기반을 확장 중입니다.

남미에서는 브라질과 아르헨티나에서 점진적인 확장이 이루어지고 있으며, 바이러스 제거를 위한 이중 리간드 혼합 모드 베드를 점점 더 많이 요구하는 공중보건 백신 수요에 초점을 맞추고 있습니다. 중동과 아프리카는 아직 초기 단계이지만, 인슐린, 혈장, 백신 자급자족을 추구하는 걸프 국가 제약 클러스터 주변에서 성장의 조짐을 보이고 있습니다. 비OECD 지역은 현재 전체 시장에서 차지하는 비중은 적지만 두 자릿수 성장 가능성을 보여주고 있어 크로마토그래피 레진 시장의 글로벌화를 강조하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 단일클론항체(mAb) 생산에 대한 수요 증가

- 신흥 시장에서 백신 파이프라인 확대

- 일회용 다운스트림 시스템으로의 전환

- 고순도 생물학적 제제에 대한 규제 압력

- 연속 생물공정에서 고유량 레진 필요성

- 시장 성장 억제요인

- 높은 레진 조달 비용과 밸리데이션 비용

- 숙련된 다운스트림 공정의 전문가의 부족

- 일회용 막 크로마토그래피와의 경쟁

- 밸류체인 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 유래별

- 천연 유래

- 아가로스

- 셀룰로오스

- 합성 유래

- 실리카겔

- 산화알루미늄

- 폴리스티렌

- 기타 합성 기반 레진

- 천연 유래

- 제품 유형별

- 단백질 A

- 이온 교환

- 혼합 모드 및 다중 모드

- 소수성 상호작용

- 사이즈 배제

- 리간드 결합 맞춤형 레진

- 기술별

- 친화성 크로마토그래피 레진

- 이온 교환 크로마토그래피 레진

- 소수성 상호작용 크로마토그래피 레진

- 사이즈 배제 크로마토그래피 레진

- 기타 기술

- 최종 사용자 산업별

- 의약품

- 생명공학

- 신약 개발

- 의약품 제조

- 물 및 환경기관

- 음식 및 식품 산업

- 기타 최종 사용자 산업

- 의약품

- 지역별

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 지역별

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- Avantor, Inc

- Bio-Rad Laboratories, Inc.

- Bio-Works

- Cytiva

- Dupont

- JSR Life Sciences, LLC

- Kaneka Eurogentec SA

- Merck KGaA

- Mitsubishi Chemical Corporation

- Purolite

- Repligen Corporation

- Sartorius Stedim Biotech

- Sepax Technologies

- Thermo Fisher Scientific

- Thermo Vectorlabs

제7장 시장 기회와 전망

HBR 25.11.07The Chromatography Resins Market size is estimated at USD 2.56 billion in 2025, and is expected to reach USD 3.62 billion by 2030, at a CAGR of 7.18% during the forecast period (2025-2030).

Steady growth reflects the segment's integral role in biopharmaceutical purification, where downstream steps still consume close to 60% of total drug-manufacturing costs Avantor. Heightened regulatory focus on product purity, rising adoption of continuous bioprocessing that needs high-flow resins, and widening therapeutic pipelines together lift demand. Capacity investments-such as Cytiva and Pall's USD 1.5 billion multiphase expansion-are shortening regional supply gaps and reinforcing secure sourcing strategies. At the same time, developers are moving toward synthetic matrices to gain reproducibility, while natural agarose grades gain niche momentum under sustainability mandates.

Global Chromatography Resins Market Trends and Insights

Rising Demand for Monoclonal-Antibody Production

Global mAb volumes keep climbing at a projected 13.23% CAGR to 2030, and resin consumption rises in parallel as antibody titers top 10 g/L, pushing Protein A beds to capacity limits. High-capacity alternatives such as Toyopearl GigaCap S-650M deliver dynamic binding above 90 g/L, more than doubling traditional media. Oncology indications account for 51% of therapeutic value, with autoimmune pipelines expanding fastest and broadening purification needs. North America retains 41.04% share of antibody output, yet Asia-Pacific advances at 13.24% CAGR, diversifying resin demand centers. In-vitro production now holds 78% of mAb supply, underscoring how downstream resin technology underwrites global access to biologics.

Expanding Vaccine Pipelines Across Emerging Markets

Post-pandemic capacity build-outs in India, China, Brazil and Indonesia keep vaccine demand buoyant, elevating need for resins that efficiently clear viral and plasmid impurities. Bio-Rad's CHT Ceramic Hydroxyapatite captures more than 75% of influenza and dengue viral particles while trimming host proteins by 90%. New ligands such as Repligen/Navigo's spike-protein affinity resin exemplify purpose-built solutions for mRNA and viral-vector vaccines. Regulatory agencies from EMA to WHO now stipulate robust viral clearance studies, driving resin developers to validate higher selectivity and flow robustness for large-scale vaccine platforms.

High Resin Procurement and Validation Cost

Protein A resin prices have climbed to USD 9,000-12,000 per liter, yet most products bind under 40 g/L, stressing budgets for both clinical and commercial runs. Lengthy lead times-often beyond 15 weeks-force firms to raise safety stocks and tie up working capital. Each supplier or lot change triggers comparability testing, extending timelines and requiring extensive documentation that inflates overall validation expenses. Smaller firms and emerging-market plants find it harder to absorb these costs, slowing domestic production scale-up.

Other drivers and restraints analyzed in the detailed report include:

- Transition Toward Single-Use Downstream Systems

- Regulatory Push for Higher-Purity Biologics

- Scarcity of Skilled Downstream-Processing Professionals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic-based materials represented 76.34% of 2024 revenue, reflecting manufacturers' preference for lot-to-lot consistency and high mechanical strength. Such characteristics enable taller columns, faster flow, and straightforward scale-up, vital to the chromatography resins market where production cycles continue to shorten. In contrast, natural media-chiefly agarose-retain gentler chemistries that safeguard labile proteins, positioning them for niche vaccines and gene-therapy vectors. The natural segment's 8.61% forecast CAGR signals renewed interest in renewable feedstocks and lower environmental footprints, especially in Europe where green- manufacturing incentives exist.

Adoption patterns illustrate a two-tier structure: multinationals install synthetic polymethacrylate beds for continuous antibody capture, whereas regional contract manufacturers expand capacity with agarose or cellulose for multi-product suites. The regulatory spotlight on adventitious-agent risk further pivots enterprise preference toward synthetics, yet biocompatibility concerns still pull natural grades into pediatric and cell-therapy pipelines. With both formats strengthening advanced ligand chemistries, competition will revolve less around base matrix and more around performance attributes such as dynamic capacity and alkaline stability in the chromatography resins market.

Ion-exchange resins accounted for 39.25% of 2024 sales, cementing a decades-long role across capture, intermediate, and polishing stages. Their broad operating window, scalability, and relative affordability suit virtually every therapeutic protein. However, mixed-mode and multimodal media are projected to compound at 8.25% annually, because combined ionic, hydrophobic, and hydrogen-bond interactions allow single-step removal of aggregates and host-cell proteins, trimming buffer usage and skid footprint.

Protein A columns remain essential for IgG capture despite premium pricing, while hydrophobic-interaction units mitigate aggregation in continuous polishing. Size-exclusion devices fulfill buffer exchange or desalting without shear, an area where the chromatography resins market size for this niche is projected to widen steadily with a 8.12% CAGR. Ligand-coupled custom solutions are steadily entering pilot scale, driven by bispecific antibodies and viral vectors. Process-intensification roadmaps suggest multimodal beds will increasingly displace sequential ion-exchange-plus-HIC operations, underscoring shifting value pools inside the chromatography resins market

The Chromatography Resins Market Report is Segmented by Origin (Natural-Based and Synthetic-Based), Technology (Ion Exchange Chromatography Resins, Affinity Chromatography Resins, and More), Product Type (Protein-A, Ion Exchange and More), End-User Industry (Pharmaceuticals, Water and Environmental Agencies, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

North America led with a 42.75% revenue contribution in 2024 and mirrors the fastest regional CAGR at 8.48% through 2030. Aggressive investments-Cytiva and Pall's USD 1.5 billion program and Purolite's new Pennsylvania agarose plant-aim to shorten lead times and insulate bioprocess supply chains. FDA analytical guidelines that tightened in 2024 cascade global expectations for resin consistency, anchoring North America's status as regulatory reference hub.

Europe ranked second in value terms, combining long-standing GMP expertise with rising emphasis on sustainability. EMA process-validation rules force high-resolution separation and lean toward recyclable or lower-waste matrices. Investments such as Merck KGaA's EUR 300 million research hub in Darmstadt and Tosoh Bioscience's German expansion reinforce domestic supply. Green manufacturing incentives further nudge producers toward bio-based agarose and closed-loop solvent systems inside the chromatography resins market.

Asia-Pacific records the briskest structural expansion, spurred by Chinese, Japanese and Korean biologics programs as well as ASEAN vaccine initiatives. Tosoh's new Yokkaichi plant exemplifies capacity alignment with regional demand. Policymakers funnel grants into local mAb and cell-therapy plants, raising consumption of high-capacity resins as multinationals localize production. India and Indonesia add volume in pandemic- readiness stockpiles, extending the customer base for continuous-flow compatible media.

South America sees gradual build-up in Brazil and Argentina, focusing on public-health vaccine needs that increasingly seek dual-ligand mixed-mode beds for viral clearance. The Middle East and Africa remain nascent but exhibit pockets of growth around Gulf state pharma clusters pursuing insulin, plasma, and vaccine self-sufficiency. Collectively, non-OECD regions contribute modest shares today yet represent double-digit growth prospects, underscoring the globalization of the chromatography resins market.

- Avantor, Inc

- Bio-Rad Laboratories, Inc.

- Bio-Works

- Cytiva

- Dupont

- JSR Life Sciences, LLC

- Kaneka Eurogentec S.A.

- Merck KGaA

- Mitsubishi Chemical Corporation

- Purolite

- Repligen Corporation

- Sartorius Stedim Biotech

- Sepax Technologies

- Thermo Fisher Scientific

- Thermo Vectorlabs

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for monoclonal-antibody (mAb) production

- 4.2.2 Expanding vaccine pipelines across emerging markets

- 4.2.3 Transition toward single-use downstream systems

- 4.2.4 Regulatory push for higher-purity biologics

- 4.2.5 Need for high-flow resins in continuous bioprocessing

- 4.3 Market Restraints

- 4.3.1 High resin procurement and validation cost

- 4.3.2 Scarcity of skilled downstream-processing professionals

- 4.3.3 Competition from disposable membrane chromatography

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Origin

- 5.1.1 Natural-based

- 5.1.1.1 Agarose

- 5.1.1.2 Cellulose

- 5.1.2 Synthetic-based

- 5.1.2.1 Silica Gel

- 5.1.2.2 Aluminum Oxide

- 5.1.2.3 Polystyrene

- 5.1.2.4 Other Synthetic Based Resins

- 5.1.1 Natural-based

- 5.2 By Product Type

- 5.2.1 Protein-A

- 5.2.2 Ion-Exchange

- 5.2.3 Mixed-Mode and Multimodal

- 5.2.4 Hydrophobic-Interaction

- 5.2.5 Size-Exclusion

- 5.2.6 Ligand-Coupled Custom Resins

- 5.3 By Technology

- 5.3.1 Affinity Chromotography Resins

- 5.3.2 Ion-Exchange Chromotography Resins

- 5.3.3 Hydrophobic-Interaction Chromotography Resins

- 5.3.4 Size-Exclusion Chromotography Resins

- 5.3.5 Other Technologies

- 5.4 By End-user Industry

- 5.4.1 Pharmaceuticals

- 5.4.1.1 Biotechnology

- 5.4.1.2 Drug Discovery

- 5.4.1.3 Drug Production

- 5.4.2 Water and Environmental Agencies

- 5.4.3 Food and Beverages

- 5.4.4 Other End-user Industries

- 5.4.1 Pharmaceuticals

- 5.5 By Geography

- 5.5.1 By Geography

- 5.5.1.1 Asia-Pacific

- 5.5.1.1.1 China

- 5.5.1.1.2 Japan

- 5.5.1.1.3 India

- 5.5.1.1.4 South Korea

- 5.5.1.1.5 ASEAN Countries

- 5.5.1.1.6 Rest of Asia-Pacific

- 5.5.1.2 North America

- 5.5.1.2.1 United States

- 5.5.1.2.2 Canada

- 5.5.1.2.3 Mexico

- 5.5.1.3 Europe

- 5.5.1.3.1 Germany

- 5.5.1.3.2 United Kingdom

- 5.5.1.3.3 France

- 5.5.1.3.4 Italy

- 5.5.1.3.5 Spain

- 5.5.1.3.6 Russia

- 5.5.1.3.7 NORDIC Countries

- 5.5.1.3.8 Rest of Europe

- 5.5.1.4 South America

- 5.5.1.4.1 Brazil

- 5.5.1.4.2 Argentina

- 5.5.1.4.3 Rest of South America

- 5.5.1.5 Middle-East and Africa

- 5.5.1.5.1 Saudi Arabia

- 5.5.1.5.2 South Africa

- 5.5.1.5.3 Rest of Middle-East and Africa

- 5.5.1 By Geography

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Avantor, Inc

- 6.4.2 Bio-Rad Laboratories, Inc.

- 6.4.3 Bio-Works

- 6.4.4 Cytiva

- 6.4.5 Dupont

- 6.4.6 JSR Life Sciences, LLC

- 6.4.7 Kaneka Eurogentec S.A.

- 6.4.8 Merck KGaA

- 6.4.9 Mitsubishi Chemical Corporation

- 6.4.10 Purolite

- 6.4.11 Repligen Corporation

- 6.4.12 Sartorius Stedim Biotech

- 6.4.13 Sepax Technologies

- 6.4.14 Thermo Fisher Scientific

- 6.4.15 Thermo Vectorlabs

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment