|

시장보고서

상품코드

1844671

자동차용 토크 컨버터 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Torque Converter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

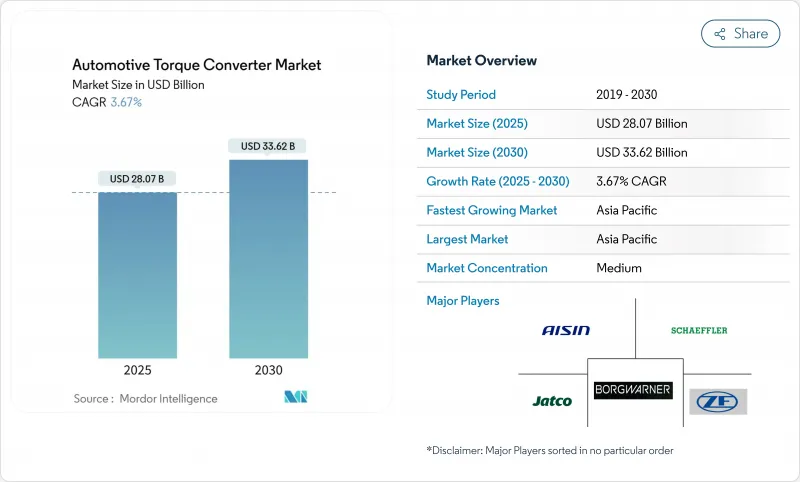

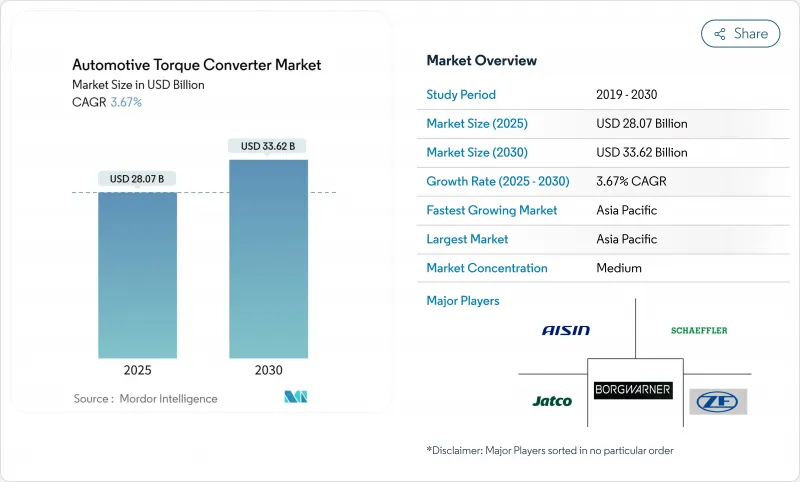

자동차용 토크 컨버터 시장은 2025년에 280억 7,000만 달러로 평가되었고, 2030년에는 336억 2,000만 달러에 이를 전망입니다.

측정된 표면적 성장 속도는 하이브리드 파워트레인, 다단 자동변속기, 상용차 생산 증가가 수요 패턴을 재편하면서 진행 중인 근본적 전환을 감추고 있습니다. 신흥국에서의 자동변속기 채택은 기본 물량 증가를 지속시키는 반면, 선진 지역은 연비와 배출 성능을 개선하는 하이브리드 전용 변환기 아키텍처에 투자를 집중하고 있습니다. 북미 지역의 공급망 근거리화, 팬데믹 이후 지속되는 경상용차 확대, 그리고 OEM의 8단 및 10단 기어박스 요구가 추가적인 추진력을 더하고 있습니다. 반면 순수 배터리 전기 구동계와 DCT 및 CVT 기술의 인기 증가는 일부 승용차 부문의 장기 전망을 다소 누그러뜨리고 있습니다. 알루미늄과 구리의 원자재 가격 변동은 부품 마진에 추가적인 불확실성을 가중시키고 있습니다.

세계의 자동차용 토크 컨버터 시장 동향 및 인사이트

신흥 시장의 급증하는 자동변속기 보급률

도시 교통 혼잡 심화와 가처분 소득 증가로 대규모 개발도상국에서 자동변속기 채택이 급증하고 있습니다. 중국의 자동변속기 시장은 수백만 대의 차량을 수동변속기에서 자동변속기 솔루션으로 전환시키고 있습니다. 인도에서도 유사한 추세가 관찰됩니다. 르노의 경쟁력 있는 가격의 키거 CVT는 100만 루피 미만 예산으로도 완전 자동화 옵션을 제공하며, 오랜 수동 변속기 선호를 약화시키고 있습니다. 규모의 경제 효과도 뒤따릅니다. 현지 생산량이 증가함에 따라 단위 비용이 하락하여 추가 보급이 가능해집니다. 앨리슨 트랜스미션의 첸나이 1억 달러 규모 확장 프로젝트는 2027년까지 생산량을 두 배로 늘리는 것을 목표로 하며, 이 수요 증가세에 대한 공급업체의 의지를 보여줍니다. 산시 패스트 오토 드라이브 그룹(Shaanxi Fast Auto Drive Group)과 같은 지역 선도 기업들은 확고한 제조 기반을 활용해 상용차 및 승용차 부문 전반에 걸쳐 증가하는 주문을 확보하고 있습니다.

하이브리드 및 마일드 하이브리드 붐, 록업 토크 컨버터 수요 견인

하이브리드 파워트레인은 엔진 정지 시 슬립을 최소화하고 원활한 토크 블렌딩을 가능하게 하는 정교한 록업 메커니즘을 갖춘 컨버터가 필요합니다. 포드의 레인저 PHEV는 변환기 앞에 전기 모터와 분리 클러치를 배치해 록업 작동 주기를 늘리는 새로운 통합 레이아웃을 선보였다. ZF의 BMW X5 xDrive40e용 플러그인 하이브리드 변속기는 기존 변환기를 통합 모터로 대체하면서도, 전기화 시스템에서 유압 커플링 원리가 어떻게 진화하는지 보여주며 연료 사용량을 최대 70%까지 절감합니다. 스텔란티스는 이미 유럽 시장에서 30종의 하이브리드 모델을 출시했으며, 각 모델은 전기화된 듀얼 클러치 변속기를 탑재해 CO2 배출량을 20% 절감합니다. 하이브리드가 완전 전기차(BEV)와의 가격 격차를 해소함에 따라, 자동차용 토크 컨버터 시장은 지속적인 록업 부품 혁신의 혜택을 누리고 있습니다.

BEV 구동계가 토크 컨버터를 배제

순수 전기차는 직접 모터 구동 방식을 사용해 기존 컨버터를 배제합니다. 보그워너가 폴스타 SUV용 전기 토크 벡터링 모듈로 전환한 사례는 기존 업체들이 유압 부품에서 벗어나 다각화하는 모습을 보여줍니다. 그러나 인프라 격차와 배터리 비용으로 인해 신흥 시장에서는 하이브리드와 내연기관 차량이 여전히 주류를 이루며, 2030년 이후까지 억제 효과가 완화될 전망입니다.

부문 분석

하이브리드 전용 자동변속기는 연평균 10.62% 성장할 것으로 예상되는 반면, 2024년 기준 유압식 자동변속기는 여전히 자동차용 토크 컨버터 시장 점유율의 40.23%를 차지했습니다. 이중 구조는 변환기가 기존 내연기관(ICE) 운전 사이클과 새로운 하이브리드 사이클을 모두 커버해야 함을 의미하며, 여기서 빈번한 엔진 재시동은 록업 내구성을 시험합니다. ZF와 같은 OEM은 8단 변속기에 전기 모터를 내장하면서, 엔진 연결을 부드럽게 하고 비틀림 스파이크를 흡수하는 슬림화된 유압 커플링을 유지합니다. 자동화 수동변속기는 연비 효율이 변속 품질보다 중요시되는 특수 중장비 차량군에서 여전히 사용되지만, CVT는 비용 제약이 있는 소형차 시장에서 점유율을 확대 중입니다. 해당 기간 동안 하이브리드가 중가 전기화 제품군을 주도함에 따라 순수 유압식 유변변속기는 성장 정체를 보일 것이나, 통합형 e-클러치 모듈을 지원하는 유변변속기는 추가 가치를 창출할 전망입니다.

하이브리드 변속기 성장으로 공급업체들은 기생 저항을 줄인 펌프 재설계와 전기 보조 저토크 조건에서 작동하는 다중 모드 록업 개발이 필수적입니다. 클러치 고속 사이클링으로 발생하는 열을 관리하기 위해 컨버터 케이싱은 고강도 강철 및 클래드 알루미늄으로 전환됩니다. 모터와 엔진 간 토크 전달이 강화되면서 소프트웨어 통합이 핵심 요소가 됩니다. 하드웨어와 함께 완전한 유압 제어 시스템을 제공하는 1차 공급업체들은 가격 결정력을 유지하는 반면, 독립형 컨버터 제조사들은 마진 압박에 직면합니다. 따라서 자동차용 토크 컨버터 시장은 글로벌 플랫폼에 대한 하이브리드 대응 설계를 신속히 검증할 수 있는 기업에 유리하게 작용합니다.

2024년 승용차가 자동차용 토크 컨버터 시장 점유율 63.57%로 매출을 주도했으나, 경상용차 부문이 연평균 8.28% 성장률로 가장 빠르게 성장 중입니다. 도시 화물, 음식 배달, 전자상거래 물류 분야는 정지-출발이 잦은 노선에서 운전자의 피로를 줄여주는 자동변속기를 우선적으로 선택합니다. 차량 관리자들은 총소유비용(TCO)에 주목하며, 높은 구입 비용 없이 연비 절감을 약속하는 8단 변속기와 결합된 컨버터 수요를 촉진하고 있습니다. 신흥 시장에서는 차량 공유 서비스도 수동 변속기에 익숙하지 않은 젊은 운전자층을 겨냥한 자동변속기를 적극 도입하고 있습니다. 반면 유럽 프리미엄 승용차 구매자들은 점차 하이브리드 또는 BEV를 선택하는 추세로, 기존 컨버터가 필요 없는 차량이 증가하며 수요 균형에 미묘한 변화가 발생하고 있습니다.

대형 상용차는 가장 작은 하위 그룹이지만 극한 토크와 높은 열 부하를 견디는 맞춤형 고용량 컨버터가 필요합니다. 주행 거리 및 출력 밀도 제약으로 광산 운반이나 지방자치단체 제설 작업 같은 분야는 완전 전기화에 저항성을 보인다. 앨리슨의 최신 시리즈는 1단 기어 잠금 기능과 이중 비틀림 댐퍼를 제공하여 더 부드러운 출발을 가능하게 하고 클러치 마모를 줄입니다. 이러한 특성으로 인해 초기 비용이 더 높음에도 불구하고 운전자들이 수동 변속기에서 전환하도록 장려합니다. 따라서 승용차의 전기화가 가속화되는 가운데 자동차용 토크 컨버터 시장은 상용 부문에서의 회복력 덕분에 혜택을 보고 있습니다.

지역 분석

아시아태평양 지역은 2024년 자동차용 토크 컨버터 시장 매출의 38.76%를 차지했으며, 중국의 최대 차량 수출국 부상과 지속적인 상용차 수요에 힘입어 2030년까지 연평균 7.27% 성장할 것으로 예상됩니다. 산시 패스트 오토 드라이브 그룹(Shaanxi Fast Auto Drive Group)과 같은 현지 선도 기업들은 하이브리드 트럭용 컨버터 포트폴리오를 확대하고 있으며, 일본은 JATCO의 광저우 100만 대 생산 공장을 통해 첨단 CVT를 공급하고 있습니다. 앨리슨(Allison)의 첸나이(Chennai) 생산 능력 두 배 확대로 부각된 인도의 가속화되는 자동변속기 채택은 이 지역의 중심적 역할을 더욱 공고히 합니다. 비용 경쟁력 있는 제조와 깊은 공급망은 성숙한 유압식 및 새로운 하이브리드 컨버터 설계에 대한 글로벌 조달의 중심지로 아시아태평양 지역을 자리매김하게 합니다.

북미는 혼합된 양상을 보이고 있습니다. 높은 자동화 보급률로 단위 물량은 견조하지만, 전기화로 인해 변속기는 더 전문화된 틈새 시장으로 밀려난다. 도시 화물 차량이 수동 변속기 대비 신뢰성 향상을 추구함에 따라 상용차 부문은 여전히 견고하며, PACCAR와 같은 OEM들은 8단 변속기에 연비 절감용 록업 기능을 통합하고 있습니다. 유럽의 엄격한 CO2 규제는 하이브리드 및 BEV로의 전환을 가속화합니다. BMW 모델용 ZF 플러그인 하이브리드 유닛은 변속기 내 전기 모터 통합 분야에서 유럽의 선도적 위상을 보여줌으로써, 점진적으로 진화하는 형태의 컨버터 수요를 유지하고 있습니다. 두 시장 모두 규제가 자동차용 토크 컨버터 시장을 완전히 제거하기보다는 동시에 제약과 재편을 동시에 일으킨다는 점을 보여줍니다.

남미, 중동, 아프리카는 자동변속기 보급률이 뒤처지지만 도시화가 심화되면서 수요 회복이 예상됩니다. 수입 관세를 회피하기 위한 현지 조립이 가속화되며, 1차 공급업체들은 비용 효율적인 제품 제공을 위해 합작 투자 기회를 모색 중입니다. 브라질과 걸프 지역의 차량 운영사들은 도로 연료 보조금이 지속되는 상황에서도 운전자 유지와 가동 시간 확보를 위해 자동변속기를 점점 더 선택하고 있습니다. 현재 규모는 작지만, 이 지역들은 주요 수익원을 보완하고 변환기 공급업체의 지역적 위험을 분산시킵니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 신흥 시장의 자동변속기 보급률 급증

- 하이브리드 및 마일드 하이브리드 붐이 잠금식 토크 컨버터 수요 촉진

- 8단/10단의 연비 향상에 대한 OEM의 압력

- 코로나 이후 글로벌 경상용차 생산 회복

- 차세대 고온 ATF 유체로 높은 스톨 토크 구현

- NVH 규제로 인한 고급 다중 감쇠 변환기 설계 촉진

- 시장 성장 억제요인

- BEV 구동계로 인한 토크 컨버터 제거

- 소형차에서 증가하는 DCT/CVT 점유율

- 변동성 있는 알루미늄 및 구리 가격으로 인한 BOM 비용 상승

- 전용 하이브리드 차량에서 변환기를 대체하는 e-클러치 모듈

- 가치 및 공급망 분석

- 규제 상황

- 기술적 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 변속기 유형별

- 자동 수동 변속기(AMT)

- 듀얼 클러치 변속기(DCT)

- 무단 변속기(CVT)

- 유압식 자동 변속기(기존 AT)

- 하이브리드 전용 AT(e-토크 컨버터)

- 차종별

- 승용차

- 소형 상용차

- 대형 상용차

- 컴포넌트별

- 펌프

- 터빈

- 스테이터

- 록업 클러치

- 하이브리드화 단계별

- ICE 전용

- 48V 마일드 하이브리드

- 풀/스트롱 하이브리드

- 플러그인 및 하이브리드

- 판매 채널별

- OEM

- 애프터마켓

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 이집트

- 나이지리아

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- Aisin Corporation

- BorgWarner Inc.

- ZF Friedrichshafen AG

- Schaeffler AG(LuK)

- Jatco Ltd.

- Allison Transmission Holdings

- Hyundai Transys Co., Ltd.

- Continental AG

- Valeo SA

- Punch Powertrain

- Exedy Corporation

- Kapec Co. Ltd.

- Precision Industries

- Sonnax Transmission Company

- Voith GmbH & Co. KGaA

- Subaru Corporation

- Robert Bosch GmbH

- General Motors(GM Powertrain)

제7장 시장 기회와 전망

HBR 25.11.07The Automotive Torque Converter Market reached USD 28.07 billion in 2025 and is forecast to climb to USD 33.62 billion by 2030, translating into a steady 3.67% CAGR.

The measured headline pace belies a deep transition as hybrid powertrains, multi-speed automatics, and rising commercial-vehicle production reshape demand patterns. Automatic-transmission adoption in emerging economies keeps baseline volumes rising, while developed regions channel investment toward hybrid-dedicated converter architectures that improve fuel economy and emissions performance. Supply-chain near-shoring in North America, continued light-commercial expansion after the pandemic, and OEM pressure for eight- and ten-speed gearboxes add further momentum. Conversely, pure battery-electric drivetrains and the growing popularity of DCT and CVT technologies temper long-term outlooks in some passenger-car segments. Raw-material cost swings in aluminum and copper inject additional uncertainty into component margins.

Global Automotive Torque Converter Market Trends and Insights

Soaring Automatic-Transmission Penetration in Emerging Markets

Escalating urban congestion and rising disposable incomes sharply increase automatic-transmission uptake in large developing nations. China's automatic transmission is shifting millions of vehicles from manual to automatic transmission solutions. Similar momentum is visible in India, where Renault's competitively priced Kiger CVT places a fully automatic option within sub-10-lakh budgets, eroding the long-standing manual bias.Scale effects follow: as local volumes grow, unit costs fall, unlocking further penetration. Allison Transmission's USD 100 million expansion in Chennai aims to double output by 2027, demonstrating supplier commitment to this demand wave. Regional champions such as Shaanxi Fast Auto Drive Group leverage entrenched manufacturing bases to capture incremental orders across commercial and passenger segments.

Hybrid & Mild-Hybrid Boom Drives Lock-up Torque-Converter Demand

Hybrid powertrains require converters with refined lock-up mechanisms that minimise slip during engine-off phases and enable seamless torque blending. Ford's Ranger PHEV places an e-motor and separator clutch ahead of the converter, highlighting new integration layouts that increase lock-up duty cycles. ZF's plug-in hybrid transmission for BMW's X5 xDrive40e replaces conventional converters with integrated motors, yet still demonstrates how hydraulic coupling principles evolve in electrified systems, cutting fuel use by up to 70%. Stellantis already fields 30 European hybrid models, each deploying electrified dual-clutch transmissions that deliver a 20% CO2 cut. As hybrids bridge the affordability gap to full BEVs, the automotive torque converter market benefits from sustained lock-up component innovation.

BEV Drivetrains Eliminate Torque Converters

Pure electric vehicles use direct motor drive, sidelining traditional converters. BorgWarner's pivot to electric torque-vectoring modules for Polestar SUVs illustrates incumbent diversification away from hydraulic components. However, infrastructure gaps and battery costs keep hybrids and ICEs prevalent in emerging markets, softening the restraining effect until after 2030.

Other drivers and restraints analyzed in the detailed report include:

- OEM Pressure for 8-/10-Speed Fuel-Efficiency Upgrades

- Recovery of Global Light-Commercial Production Post-COVID

- Rising DCT/CVT Share in Compact Cars

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid-dedicated automatics are forecast to grow 10.62% annually, while hydraulic automatics still held 40.23% of the automotive torque converter market share in 2024. The dual structure means converters must span legacy ICE duty and new hybrid cycles, where frequent engine restarts test lock-up durability. OEMs such as ZF embed electric motors into eight-speed boxes, retaining a slimmed hydraulic coupling that smooths engine engagement and absorbs torsional spikes. Automated manuals linger in specialised heavy-duty fleets because fuel efficiency outweighs shift quality, whereas CVTs gain ground in cost-constrained small cars. Over the period, converters supporting integrated e-clutch modules will capture incremental value even as pure hydraulic units plateau because hybrids dominate mid-price electrification offerings.

Hybrid transmission growth compels suppliers to redesign pumps for lower parasitic drag and develop multi-mode lock-ups that engage under electrically assisted low-torque conditions. Converter casings migrate toward high-strength steels and clad aluminium to manage added heat from rapid clutch cycling. Software integration becomes critical as torque hand-off between motor and engine intensifies. Tier-ones that provide complete hydraulic controls alongside hardware retain pricing power, while stand-alone converter makers face margin pressure. The automotive torque converter market therefore rewards firms able to validate hybrid-ready designs quickly for global platforms.

Passenger cars dominated revenue with a 63.57% of the automotive torque converter market share in 2024, yet light commercial vehicles are growing fastest at an 8.28% CAGR. Urban freight, food delivery, and e-commerce logistics prioritise automatic gearboxes that cut driver fatigue in stop-start routes. Fleet managers focus on total cost of ownership, boosting demand for converters paired with eight-speed boxes that promise fuel savings without steep acquisition costs. In emerging markets, ride-hailing services also push for automatic transmissions that appeal to younger drivers unfamiliar with manuals. Conversely, premium European passenger-car buyers increasingly choose hybrids or BEVs where traditional converters may be absent, creating a nuanced demand balance.

Heavy commercial vehicles, though the smallest subgroup, require bespoke high-capacity converters that withstand extreme torque and high thermal loads. Due to range and power density constraints, applications such as mining haulage or municipal snow removal are resistant to full electrification. Allison's latest series offers first-gear lock-up and twin torsional dampers, delivering smoother launches and reducing clutch wear. Such attributes encourage operators to shift from manuals despite higher upfront costs. The automotive torque converter market therefore benefits from commercial-segment resilience even as passenger-car electrification accelerates.

The Automotive Torque Converter Market Report is Segmented by Transmission Type (Automated Manual Transmission, Dual-Clutch Transmission, and More), Vehicle Type (Passenger Vehicle, Light Commercial Vehicles, and More), Component ( Pump, Turbine, and More), Hybridization Level ( ICE-Only, and More), Sales Channel (OEM, and Aftermarket) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 38.76% of the automotive torque converter market revenue in 2024 and should grow 7.27% per year to 2030, supported by China's ascent as the top vehicle exporter and sustained commercial-vehicle demand. Local champions such as Shaanxi Fast Auto Drive Group broaden converter portfolios for hybrid trucks, while Japan supplies cutting-edge CVT output via JATCO's one million-unit Guangzhou plant. India's accelerating automatic-transmission uptake, highlighted by Allison's Chennai capacity doubling, further cements the region's central role. Cost-competitive manufacturing and deep supply chains make APAC the nexus of global sourcing for mature hydraulic and new hybrid converter designs.

North America presents a mixed landscape: high baseline automatic penetration keeps unit volumes solid, yet electrification pushes converters into more specialised niches. Commercial-vehicle segments remain robust as urban freight fleets seek reliability upgrades over manual gearboxes, and OEMs such as PACCAR integrate fuel-saving lock-up features across eight-speed boxes. Europe's stringent CO2 rules quicken the pivot toward hybrids and BEVs. ZF's plug-in hybrid units for BMW models exemplify the region's leadership in integrating electric motors inside transmissions, sustaining converter demand in progressively evolved forms. Both markets illustrate how regulation simultaneously restrains and reshapes the automotive torque converter market rather than eliminating it outright.

South America, the Middle East, and Africa trail on automatic-transmission penetration yet promise catch-up demand as urbanisation deepens. Local assembly to bypass import tariffs gains momentum, with tier-ones scouting joint ventures for cost-sensitive offerings. Fleet operators in Brazil and the Gulf increasingly choose automatic gearboxes for driver retention and uptime, even where road-fuel subsidies persist. Although small today, these regions complement mainstream revenue centres and diversify geographic risk for converter suppliers.

- Aisin Corporation

- BorgWarner Inc.

- ZF Friedrichshafen AG

- Schaeffler AG (LuK)

- Jatco Ltd.

- Allison Transmission Holdings

- Hyundai Transys Co., Ltd.

- Continental AG

- Valeo SA

- Punch Powertrain

- Exedy Corporation

- Kapec Co. Ltd.

- Precision Industries

- Sonnax Transmission Company

- Voith GmbH & Co. KGaA

- Subaru Corporation

- Robert Bosch GmbH

- General Motors (GM Powertrain)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soaring Automatic-transmission Penetration In Emerging Markets

- 4.2.2 Hybrid And Mild-hybrid Boom Drives Lock-up Torque-converter Demand

- 4.2.3 OEM Pressure For 8-/10-speed Fuel-efficiency Upgrades

- 4.2.4 Recovery Of Global Light-commercial Production Post-covid

- 4.2.5 Next-gen High-temperature ATF Fluids Enable Higher Stall Torque

- 4.2.6 NVH Regulations Spur Advanced Multi-damping Converter Designs

- 4.3 Market Restraints

- 4.3.1 BEV Drivetrains Eliminate Torque Converters

- 4.3.2 Rising DCT/CVT Share In Compact Cars

- 4.3.3 Volatile Aluminum and Copper Prices Inflate BOM Cost

- 4.3.4 E-clutch Modules Replacing Converters In Dedicated Hybrids

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Transmission Type

- 5.1.1 Automated Manual Transmission (AMT)

- 5.1.2 Dual-Clutch Transmission (DCT)

- 5.1.3 Continuously Variable Transmission (CVT)

- 5.1.4 Hydraulic Automatic (Traditional AT)

- 5.1.5 Hybrid Dedicated AT (e-Torque Converter)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Vehicles

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Heavy Commercial Vehicles

- 5.3 By Component

- 5.3.1 Pump

- 5.3.2 Turbine

- 5.3.3 Stator

- 5.3.4 Lock-up Clutch

- 5.4 By Hybridization Level

- 5.4.1 ICE-Only

- 5.4.2 48-V Mild Hybrid

- 5.4.3 Full/Strong Hybrid

- 5.4.4 Plug-in Hybrid

- 5.5 By Sales Channel

- 5.5.1 OEM

- 5.5.2 Aftermarket

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 South Africa

- 5.6.5.4 Egypt

- 5.6.5.5 Nigeria

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Aisin Corporation

- 6.4.2 BorgWarner Inc.

- 6.4.3 ZF Friedrichshafen AG

- 6.4.4 Schaeffler AG (LuK)

- 6.4.5 Jatco Ltd.

- 6.4.6 Allison Transmission Holdings

- 6.4.7 Hyundai Transys Co., Ltd.

- 6.4.8 Continental AG

- 6.4.9 Valeo SA

- 6.4.10 Punch Powertrain

- 6.4.11 Exedy Corporation

- 6.4.12 Kapec Co. Ltd.

- 6.4.13 Precision Industries

- 6.4.14 Sonnax Transmission Company

- 6.4.15 Voith GmbH & Co. KGaA

- 6.4.16 Subaru Corporation

- 6.4.17 Robert Bosch GmbH

- 6.4.18 General Motors (GM Powertrain)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment