|

시장보고서

상품코드

1844676

고성능 섬유 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)High-Performance Fibers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

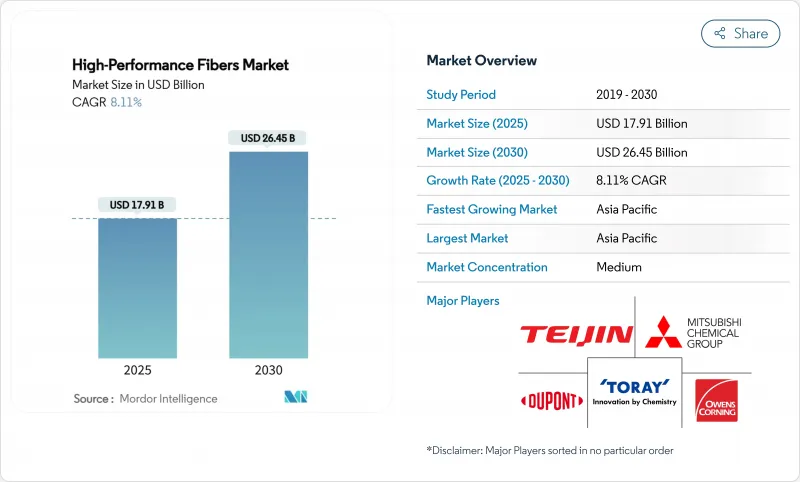

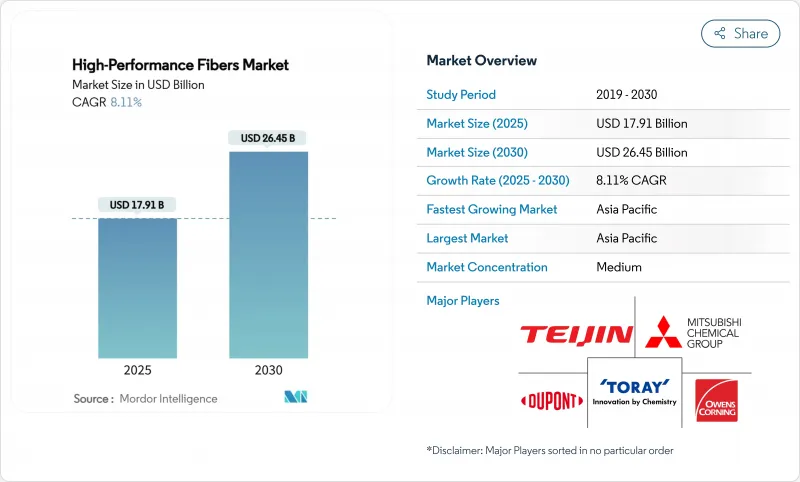

고성능 섬유 시장 규모는 2025년에 179억 1,000만 달러로 평가되었고, 예측기간(2025-2030년)의 CAGR은 8.11%를 나타낼 것으로 예측되며 2030년에 264억 5,000만 달러로 성장할 전망입니다.

탄소섬유, 아라미드섬유, 유리섬유 및 특수 섬유가 항공우주 분야의 틈새 시장에서 재생에너지 장비, 무공해 차량, 데이터 집약적 통신 네트워크의 주류 역할로 전환되면서 수요 증가 속도가 가속화되고 있습니다. 현재 100m를 초과하는 상업용 풍력 터빈 블레이드, Type-IV 수소 압력 용기, 5G 광케이블은 모두 탁월한 강도 대비 중량비와 열적 안정성을 갖춘 소재를 필요로 합니다. 중국의 공격적인 생산 능력 확대로 평균 판매 가격이 압박받고 있지만, 증가하는 물량과 새로운 응용 분야는 계속해서 매출을 끌어올리고 있습니다. 정책 입안자들의 탈탄소화 의무와 북미 및 유럽의 공급망 현지화 계획이 결합되어 장기적인 성장을 더욱 공고히 하고 있습니다.

세계의 고성능 섬유 시장 동향 및 인사이트

경량 해양 풍력 블레이드 수요 급증

100m를 넘는 터빈 블레이드는 기존 모델보다 훨씬 많은 양의 탄소 섬유를 소비하며, 자동 섬유 배치 기술이 생산 비용을 낮추면서 일부 제조업체에게 풍력 산업이 항공우주 산업을 제치고 최대 단일 수요처로 부상하고 있습니다. 강성, 내식성, 낙뢰 보호 기능을 균형 있게 확보하기 위해 탄소 섬유와 유리 섬유를 결합한 하이브리드 소재가 채택되고 있습니다. 자체 섬유 생산 라인을 보유한 중국 및 유럽 블레이드 제조사들은 북해와 동중국해에서의 급속한 설비 확충 과정에서 비용 우위를 점하고 있습니다.

항공우주 및 방위산업으로부터의 높은 수요

전투기 함대 현대화, 무인 항공 시스템, 우주 발사체 개발로 방위 예산은 초고탄성 탄소섬유 및 세라믹 섬유에 지속적으로 투자되고 있습니다. 상업 항공 회복으로 복합재 비중이 높은 와이드바디 플랫폼 주문이 재개된 한편, ‘전기화 확대’ 항공기 구조는 전자기 차폐 요구사항을 도입하여 하이브리드 탄소-아라미드 적층을 선호하게 합니다.

휘발성 폴리아크릴로니트릴(PAN)-전구체 공급망

2024년 폴리아크릴로니트릴 가격의 30-40% 급등은 후방 통합이 부족한 독립 스핀너들의 마진을 축소시켰다. 전구체 생산 능력을 장악한 도레이와 중국 내 주요 기업들은 가격 급등으로부터 보호받았으나, 여러 서구 생산업체들은 원료 공급 전망이 안정화될 때까지 확장 계획을 연기했습니다. 미국 내 바이오 기반 아크릴로니트릴 시범 프로젝트는 원료 다각화를 도모할 수 있으나, 상업적 생산까지는 수년이 소요될 전망입니다.

부문 분석

탄소섬유는 2024년 고성능 섬유 시장 점유율의 43.18%를 차지했으며, 자동차 경량화 의무화 및 재생에너지 인프라 확대로 2030년까지 연평균 9.08% 성장할 것으로 전망됩니다. 중푸 쉔잉(Zhongfu Shenying)과 같은 아시아 기반 생산자들은 비용에 민감한 산업 부문에 진출하기 위해 장쑤성에 연간 30,000톤 규모의 신규 생산 능력(8억 6,600만 달러)을 투입하고 있습니다. 아라미드는 탄도 및 통신 응용 분야에서 계속해서 우위를 점하고 있습니다. 네덜란드에 위치한 테이진(Teijin)의 산업 규모 재활용 공장은 이제 아라미드 원사를 새로운 섬유로 재가공하여 수명 주기 배출량을 낮추고 있습니다. 유리 섬유는 건설 및 표준 자동차 패널용 저비용 주력 소재로 자리매김한 반면, 전기차 배터리 팩의 열적 및 화학적 내구성 요구로 폴리페닐렌 설파이드(PPS)는 두 자릿수 성장을 기록 중입니다. 초고분자량 폴리에틸렌(UHMWPE)과 세라믹 섬유는 각각 극저온 저장 및 초음속 플랫폼 분야에서 틈새 역할을 수행합니다.

산업용 등급 탄소섬유의 급속한 가격 하락이 조달 전략을 재편하고 있습니다. 자동차 제조사들은 공급 안정화를 위해 다년 계약을 체결하는 반면, 풍력 터빈 OEM 업체들은 물량 확보를 대가로 가격 상한선을 협상하는 위탁 가공 계약을 추진 중입니다. 재료 제조사들은 고생산성 블레이드 생산 목표를 달성하기 위해 탄소 토우와 저점도 에폭시 수지를 결합하고 있습니다. 동시에 고성능 섬유 시장에서는 PAN 의존도를 낮추고 환경적 신뢰도를 높이기 위해 리그닌 유래 탄소에 대한 벤처 투자가 증가하고 있습니다. 아직 상용화 단계는 아니지만, 파일럿 라인을 통해 스포츠 용품 적층재에 적합한 35 Msi 이상의 탄성률 섬유가 생산되어 향후 10년 내 기존 공급망을 교란할 가능성을 시사하고 있습니다.

지역 분석

아시아태평양 지역은 2024년 고성능 섬유 시장 점유율의 40.25%를 차지하며 주도하고 있으며, 이는 중국의 재생에너지 보급 확대와 공격적인 차량 전기화 일정에 힘입은 결과입니다. 중국의 5개년 계획은 연간 100GW 이상의 해상풍력 설비 증설을 지원하며, 이는 대형 블레이드에 사용되는 섬유 사용량을 두 배로 증가시킬 것입니다. 국내 생산사들은 T1000급 탄소섬유에 대한 서방 독점을 깨뜨려, 현지 OEM이 첨단 전투기의 방위 및 항공우주 규격을 충족할 수 있게 했습니다. 일본의 도레이(Toray)와 테이진(Teijin)은 프리미엄 틈새 시장을 계속 장악하고 있으며, 한국은 PPS 및 유리섬유를 배터리 하우징과 전자 기판에 활용하고 있습니다.

인플레이션 감축법(IRA)과 미국산 구매 정책의 지원을 받는 북미는 국내 탄소섬유 생산을 우선시하고 있습니다. 워싱턴주, 앨라배마주, 퀘벡에 신설되는 생산라인은 2027년까지 연간 15,000톤 이상을 추가 생산하여 아시아산 전구체 의존도를 완화하고 전투기 프로그램 및 우주 발사체와 관련된 국가 안보 목표에 부합할 것입니다. 멕시코의 전기차 조립 능력 증가는 아라미드 및 유리 섬유 수입을 국경 남쪽으로 끌어들이고 있어, 지역 변환업체들이 최종 조립 허브 인근에 입지하도록 촉진하고 있습니다.

유럽 시장의 진화는 지속가능성과 순환경제 원칙을 강조하며, 기존 소재보다 바이오 기반 및 재활용 섬유 솔루션을 점차 우대하는 규제 체계를 구축 중입니다. 해당 지역의 풍력 에너지 부문은 상당한 탄소섬유 수요를 창출하는 반면, 자동차 응용 분야는 배출 감축 목표를 지원하는 경량화 솔루션에 집중하고 있습니다. 독일 자동차 제조사들은 재용융이 용이한 열가소성 탄소 구조체를 검증 중이며, 북유럽 에너지 개발사들은 해상 프로토타입에 바이오 기반 에폭시 매트릭스를 시험 중입니다. 지역 성장은 아시아의 속도에 뒤처지지만, 엄격한 품질 및 환경 기준으로 인해 평균 판매 가격이 더 높습니다. 남미와 중동의 신흥 수요는 인프라 및 재생 에너지 메가 프로젝트와 연계되어 기회적 성격을 띠지만, 통화 변동성과 기술 인력 부족으로 인해 제약을 받고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 경량 해상 풍력 블레이드 수요 급증

- 항공우주 및 방위산업으로부터의 높은 수요

- Type-IV 수소 압력 용기 상용화

- 5G 광케이블의 아라미드 원사 전환

- 스포츠 및 보호 제품에 대한 높은 수요

- 시장 성장 억제요인

- 휘발성 폴리아크릴로니트릴(PAN) 전구체공급망

- 다중 재료 복합재 재활용 인프라 제한

- 중국 과잉 생산 능력에 따른 가격 압박

- 밸류체인 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 유형별

- 탄소섬유

- 복합재료

- 탄소섬유 강화 폴리머(CFRP)

- 탄소-탄소 강화(RCC)

- 섬유제품

- 마이크로 전극

- 촉매

- 아라미드 섬유

- 메타-아라미드

- 파라계 아라미드

- 유리 섬유

- 폴리페닐렌설파이드(PPS)

- 기타 유형(초고분자량 폴리에틸렌(UHMWPE), 폴리벤조이미다졸(PBI), 폴리(p-페닐렌-2,6-벤조비스옥사졸)(PBO), 탄화규소(SiC), 현무암)

- 탄소섬유

- 최종 사용자 산업별

- 항공우주 및 방위

- 자동차

- 스포츠 용품

- 대체 에너지

- 전자 및 통신

- 건설 및 인프라

- 기타 최종 사용자 산업(헬스케어 및 의료기기 등)

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- Avient Corporation

- Bally Ribbon Mills

- China Jushi Co., Ltd.

- DuPont

- Hexcel Corporation

- Honeywell International Inc.

- Huvis Corp

- Kolon Industries, Inc.

- Kureha Corporation

- Mitsubishi Chemical Carbon Fiber and Composites, Inc.

- Owens Corning

- PBI Performance Products, Inc.

- Sarla Performance Fibers Limited

- Solvay

- Teijin Limited

- Toray Industries Inc.

- Toyobo Co., Ltd.

- TOYOBO MC Corporation

- Weihai Guangwei Group Co., Ltd.

- WL Gore & Associates

- Yantai Tayho Advanced Materials Co., Ltd.

제7장 시장 기회와 전망

HBR 25.11.03The High-Performance Fibers Market size is estimated at USD 17.91 billion in 2025, and is expected to reach USD 26.45 billion by 2030, at a CAGR of 8.11% during the forecast period (2025-2030).

Uptake is accelerating as carbon, aramid, glass, and specialty fibers move from niche aerospace uses to mainstream roles in renewable-energy hardware, zero-emission vehicles, and data-rich telecom networks. Commercial wind-turbine blades that now exceed 100 m lengths, Type-IV hydrogen pressure vessels, and 5G fiber-optic cabling all require materials with exceptional strength-to-weight ratios and thermal stability. Aggressive capacity additions in China have pressured average selling prices, yet rising volumes and new applications continue to lift revenue. Policymakers' decarbonization mandates, combined with supply-chain localization initiatives in North America and Europe, further anchor long-term growth.

Global High-Performance Fibers Market Trends and Insights

Surging Demand for Lightweight Offshore-Wind Blades

Turbine blades topping 100 m now consume far greater volumes of carbon fiber than earlier models, and automated fiber placement is lowering production costs, allowing wind to surpass aerospace as the single largest volume outlet for some manufacturers. Hybrids that combine carbon and glass are being adopted to balance stiffness, corrosion resistance, and lightning-strike protection. Chinese and European blade makers with captive fiber lines gain cost advantages during rapid capacity build-outs in the North Sea and East China Sea.

High Demand from Aerospace and Defense Industry

Modernization of fighter fleets, uncrewed aerial systems, and space-launch vehicles keeps defense budgets invested in ultra-high-modulus carbon and ceramic fibers. Commercial aviation recovery has renewed orders for composite-rich wide-body platforms, while "more-electric" aircraft architectures introduce electromagnetic-shielding requirements that favor hybrid carbon-aramid lay-ups.

Volatile Polyacrylonitrile (PAN)-Precursor Supply Chain

Polyacrylonitrile price swings of 30-40% in 2024 curtailed margins for independent spinners lacking backward integration. Toray and domestic Chinese majors that control precursor capacity insulated themselves from spikes, while several Western producers postponed expansion plans pending more stable feedstock visibility. Bio-based acrylonitrile pilot projects in the United States could diversify inputs, yet commercial output remains years away.

Other drivers and restraints analyzed in the detailed report include:

- Commercial Rollout of Type-IV Hydrogen Pressure Vessels

- 5G Fiber-Optic Cabling Shift to Aramid Yarn

- Limited Recycling Infrastructure for Multi-Material Composites

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Carbon fiber captured 43.18% of the high-performance fibers market share in 2024 and is forecast to climb at a 9.08% CAGR to 2030, underpinned by automotive lightweighting mandates and renewable-energy infrastructure roll-outs. Asia-based producers such as Zhongfu Shenying are injecting fresh capacity-USD 866 million for 30,000 t/y in Jiangsu-to penetrate cost-sensitive industrial segments. Aramid continues to dominate ballistic and telecom applications; Teijin's industrial-scale recycling plant in the Netherlands now reprocesses aramid yarn into new fiber, lowering lifecycle emissions. Glass fiber remains the low-cost mainstay for construction and standard automotive panels, while polyphenylene sulfide (PPS) enjoys double-digit growth as electric-vehicle battery packs require thermal and chemical resilience. UHMWPE and ceramic fibers fill niche roles in cryogenic storage and hypersonic platforms, respectively.

Rapid cost erosion across industrial-grade carbon is reshaping procurement strategies. Automakers are locking multiyear contracts to assure supply, while wind OEMs negotiate tolling arrangements that exchange volume commitments for price ceilings. Material formulators are coupling carbon tow with low-viscosity epoxy resins to meet high-throughput blade production targets. Concurrently, the high-performance fibers market is witnessing growing venture investment in lignin-derived carbon to ease PAN dependence and improve environmental credentials. Although still pre-commercial, pilot lines have produced 35+ Msi modulus fibers suitable for sporting-goods laminates, signaling potential to disrupt incumbent supply chains later in the decade.

The Global High Performance Fibers Market is Segmented by Type (Carbon Fiber, Aramid Fiber, Glass Fiber, Polyphenylene Sulfide (PPS), and More), End-User Industry (Aerospace and Defense, Automotive, Sporting Goods, Alternative Energy, Electronics & Telecommunications, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Value (USD).

Geography Analysis

Asia-Pacific dominates with 40.25% of the high-performance fibers market share in 2024, propelled by China's renewable-energy deployment and aggressive vehicle-electrification timelines. Beijing's Five-Year Plan backs >100 GW/year of offshore-wind additions, doubling fiber usage in large-diameter blades. Domestic producers have broken Western monopoly on T1000-class carbon, enabling local OEMs to meet defense and aerospace specifications for advanced fighter jets. Japan's Toray and Teijin continue to command premium niches, while South Korea channels PPS and glass fiber into battery housings and electronic substrates.

North America, supported by the Inflation Reduction Act and Buy-American policies, is prioritizing domestic carbon-fiber output. New lines in Washington State, Alabama, and Quebec will add >15,000 t/y by 2027, mitigating reliance on Asian precursors and aligning with national-security objectives for fighter programs and space launchers. Mexico's growing EV assembly capacity is pulling aramid and glass imports south of the border, prompting regional converters to co-locate near final assembly hubs.

Europe's market evolution emphasizes sustainability and circular economy principles, with regulatory frameworks that increasingly favor bio-based and recyclable fiber solutions over conventional materials. The region's wind energy sector drives significant carbon fiber demand, while automotive applications focus on lightweight solutions that support emission reduction targets . German automakers validate thermoplastic carbon architectures that allow easier re-melt, while Nordic energy developers test bio-based epoxy matrices in offshore prototypes. Regional growth lags Asia's pace yet commands higher average selling prices due to stringent quality and environmental standards. Emerging demand in South America and the Middle East remains opportunistic, tied to infrastructure and renewable-energy megaprojects but tempered by currency volatility and skills shortages.

- Avient Corporation

- Bally Ribbon Mills

- China Jushi Co., Ltd.

- DuPont

- Hexcel Corporation

- Honeywell International Inc.

- Huvis Corp

- Kolon Industries, Inc.

- Kureha Corporation

- Mitsubishi Chemical Carbon Fiber and Composites, Inc.

- Owens Corning

- PBI Performance Products, Inc.

- Sarla Performance Fibers Limited

- Solvay

- Teijin Limited

- Toray Industries Inc.

- Toyobo Co., Ltd.

- TOYOBO MC Corporation

- Weihai Guangwei Group Co., Ltd.

- W. L. Gore & Associates

- Yantai Tayho Advanced Materials Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Lightweight Offshore-Wind Blades

- 4.2.2 High Demand from Aerodpace and Defense Industry

- 4.2.3 Commercial Rollout of Type-IV Hydrogen Pressure Vessels

- 4.2.4 5G fiber-optic Cabling Shift to Aramid Yarn

- 4.2.5 High Demand for Sporting and Protective Products

- 4.3 Market Restraints

- 4.3.1 Volatile Polyacrylonitrile (PAN)-Precursor Supply Chain

- 4.3.2 Limited Recycling Infrastructure for Multi-Material Composites

- 4.3.3 Chinese Over-Capacity Driving Price Compression

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Carbon Fiber

- 5.1.1.1 Composite Materials

- 5.1.1.1.1 Carbon Fiber Reinforced Polymer (CFRP)

- 5.1.1.1.2 Reinforced Carbon Carbon (RCC)

- 5.1.1.2 Textiles

- 5.1.1.3 Microelectrodes

- 5.1.1.4 Catalysis

- 5.1.2 Aramid Fiber

- 5.1.2.1 Meta-Aramid

- 5.1.2.2 Para-Aramid

- 5.1.3 Glass Fiber

- 5.1.4 Polyphenylene Sulfide (PPS)

- 5.1.5 Other Types (Ultra-High Molecular Weight Polyethylene (UHMWPE), Polybenzimidazole (PBI), Poly(p-phenylene-2,6-benzobisoxazole)(PBO), Silicon Carbide (SiC), Basalt)

- 5.1.1 Carbon Fiber

- 5.2 By End-user Industry

- 5.2.1 Aerospace & Defense

- 5.2.2 Automotive

- 5.2.3 Sporting Goods

- 5.2.4 Alternative Energy

- 5.2.5 Electronics & Telecommunications

- 5.2.6 Construction & Infrastructure

- 5.2.7 Other End User Industries (Healthcare & Medical Devices, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Avient Corporation

- 6.4.2 Bally Ribbon Mills

- 6.4.3 China Jushi Co., Ltd.

- 6.4.4 DuPont

- 6.4.5 Hexcel Corporation

- 6.4.6 Honeywell International Inc.

- 6.4.7 Huvis Corp

- 6.4.8 Kolon Industries, Inc.

- 6.4.9 Kureha Corporation

- 6.4.10 Mitsubishi Chemical Carbon Fiber and Composites, Inc.

- 6.4.11 Owens Corning

- 6.4.12 PBI Performance Products, Inc.

- 6.4.13 Sarla Performance Fibers Limited

- 6.4.14 Solvay

- 6.4.15 Teijin Limited

- 6.4.16 Toray Industries Inc.

- 6.4.17 Toyobo Co., Ltd.

- 6.4.18 TOYOBO MC Corporation

- 6.4.19 Weihai Guangwei Group Co., Ltd.

- 6.4.20 W. L. Gore & Associates

- 6.4.21 Yantai Tayho Advanced Materials Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Emerging of Nanofibers and Ceramic Fibers