|

시장보고서

상품코드

1844710

플라스틱 접착제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Plastic Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

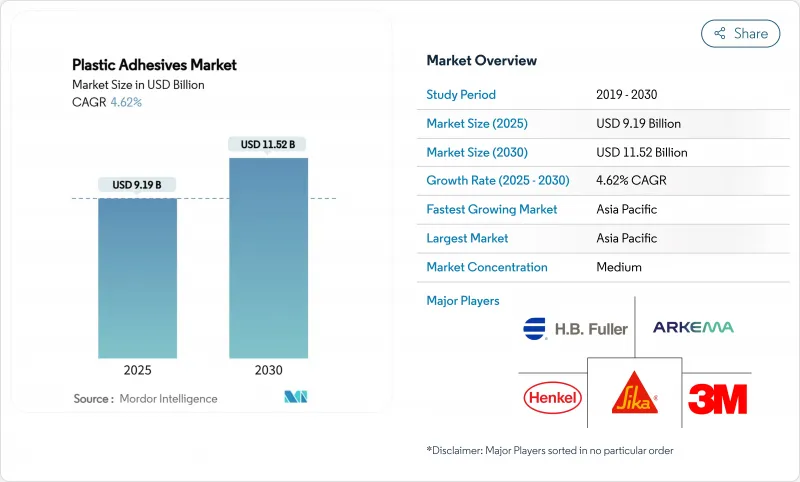

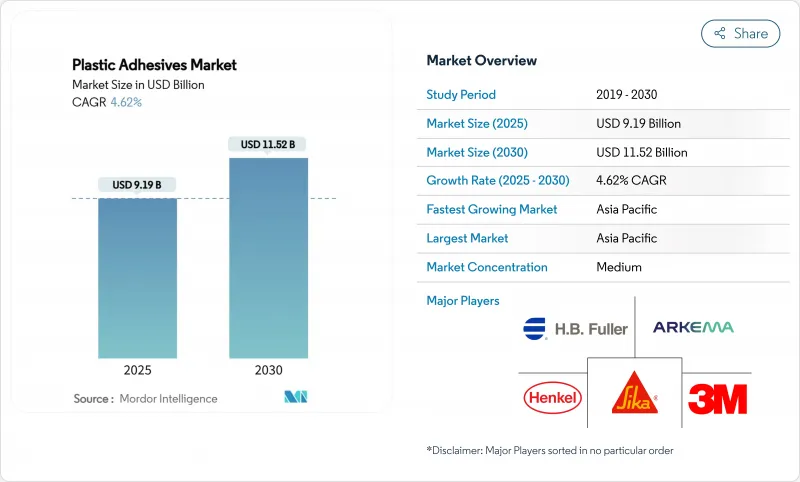

플라스틱 접착제 시장 규모는 2025년에 91억 9,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR은 4.62%로, 2030년에는 115억 2,000만 달러에 달할 것으로 예상됩니다.

플라스틱 접착제 시장은 범용 접착제에서 전기자동차 배터리 팩, 의료용 웨어러블 및 차세대 건축 패널에 해당하는 특수 화학 물질로 전환하고 있습니다. 경량 자동차에 대한 수요가 증가하고, 헬스케어에서 바이오 폴리우레탄 필름으로의 전환, VOC 규제의 강화로 자동차, 의료, 건축 분야에서의 응용 범위가 넓어지고 있습니다. 제조업체는 중국, 유럽연합(EU), 미국에서 진화하는 배출규제를 준수하는 수성 등급과 바이오 유래 등급을 출시하고 있으며, 플라스틱 접착제 시장이 지속가능성의 의무화에 의해 태어날 기회를 포착할 수 있도록 하고 있습니다. 제조업체 각사는 기술 격차의 시정, 원료 비용·리스크와의 밸런스, 새로운 지역으로의 진출을 도모하기 위해, 목표를 좁힌 M&A나 공동 개발 계약을 채용하고 있어 경쟁 세력은 여전히 유동적입니다.

세계의 플라스틱 접착제 시장 동향과 인사이트

자동차 업계에서 경량화 추진

자동차 제조업체는 과도한 무게를 제거하고 혼합 재료 설계를 강화하기 위해 기계식 패스너를 구조용 접착제로 대체하고 있습니다. 전형적인 2025년 전기자동차 SUV는 현재 접착제의 400 선형 피트 이상을 통합하고 20년 전에 30피트 미만에 비해 알루미늄, 탄소섬유 및 엔지니어링 플라스틱을 접합할 때 접착제가 수행하는 구조적 역할을 보여줍니다. 나고야 대학에서 개발한 충격 강화 엘라스토머와 에폭시의 하이브리드는 기존의 에폭시에 비해 22배의 충격 강도를 실현해, 충돌 안전성을 유지하면서 패널의 박형화와 에너지 흡수성이 높은 충돌 구조를 가능하게 했습니다. 대부분의 OEM이 항속거리 연장을 위해 차체의 경량화에 임하고 있기 때문에 플라스틱 접착제 시장은 2030년까지 자동차 소비량이 연율 2자리수로 증가할 것으로 예상하고 있습니다.

고성능 플라스틱으로 건설 변화

외관과 글레이징 시스템은 경량 복합 패널로 전환되어 긴 수명의 고탄성 접착제가 필요합니다. 시카 보호 글레이징용 접착제 시리즈는 지진 하중을 흡수하면서도 강성을 유지할 수 있기 때문에 허리케인급 커튼월에도 사용할 수 있습니다. 신흥경제국에서는 고층 빌딩의 개수, 아시아에서는 그린필드의 대규모 프로젝트로 내화성, 자외선 내구성, 신속한 시공의 균형을 맞춘 플라스틱 접착제가 필요합니다. 빠른 경화 PVC TrimWelder 제품은 30분 내에 80%의 처리 강도에 도달하므로 계약자는 법률 준수를 희생하지 않고 프로젝트 사이클을 가속화할 수 있습니다.

석유 원료 가격 변동

에폭시와 폴리우레탄의 베이스 수지 비용은 원유와 프로파일렌의 동향에 따라 달라집니다. 2025년 1월 독일 액상 에폭시 가격은 재고가 부족한 가운데 1.73% 상승했지만, 같은 달 하순에는 춘절을 앞두고 판매자가 잉여 재고를 처분했기 때문에 아시아 한월은 1.4% 하락했습니다. 미국에서는 폴리에틸렌이 5¢/lb 상승하여 포장용 점착제의 투입량을 더욱 밀어 올렸습니다. 코베스트로는 HB 풀러와 ISCC-PLUS 인증 바이오나프타 스트림을 통해 화석 원료의 변동을 완화하기 위한 인증 물질 수지 공급 계약을 체결했습니다.

부문 분석

에폭시 그레이드는 2024년 플라스틱 접착제 시장 규모의 32.45%를 차지하며 자동차의 바디 인 화이트 어셈블리와 철골 철근 콘크리트 패널의 구조 접합부를 지지했습니다. 높은 유리 전이 온도와 내화학성으로 인해 에폭시는 전단 하중과 온도 스파이크가 집중되는 장소에 적합합니다. 그러나 특수 시아노아크릴레이트, 아크릴, 하이브리드 우레탄은 OEM이 소형 전자기기의 신속한 접착을 추구하고 열에 민감한 기판용 콜드 큐어 대체품을 필요로 하기 때문에 가장 빠른 5.18%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 따라서 플라스틱 접착제 시장은 에폭시의 견고한 점유율과 속도와 유연성을 중시하는 신흥 틈새 화학물질의 균형을 맞추고 있습니다. HB 풀러의 사이버본드 라인과 같은 시아노아크릴레이트 패키지는 ISO 10993의 세포독성 요건을 충족하면서 의료기기의 미량 투여를 위해 점도를 조절할 수 있습니다. 바이오 유래의 환상 카보네이트로 만들어진 비이소시아네이트 폴리우레탄은 파일럿 라인의 규모를 확대하고 있으며, 플라스틱 접착제 시장에서 지속 가능한 수지에 축발이 퍼지고 있음을 보여줍니다.

제조업체는 표면 에너지가 낮은 폴리올레핀과 계면하는 접착 촉진제를 최적화하기 위한 연구개발을 거듭하여 프라이머 없이 보다 높은 박리 강도를 실현하는 것을 목표로 하고 있습니다. 실리콘 에폭시 하이브리드는 고온 일렉트로닉스 모듈의 기밀 밀봉을 유지하고, 배합 제조업체에 차별화를 도모하는 새로운 루트를 제공합니다. 환경 규제에 의해 비스페놀 A 유도체가 금지되는 가운데, 에폭시 수지 제조업체는 비스 F와 노볼락의 대체품의 상시를 가속시키고, EU에서 향후 예정되고 있는 내분비 난란 물질의 재검토에 대응하면서, 플라스틱 접착제 시장의 큰 점유율을 지키고 있습니다.

지역 분석

아시아태평양은 엔지니어링 플라스틱, 일렉트로닉스 및 양말의 주요 제조 기지이며, 플라스틱 접착제 시장의 최대 수익 기여 지역으로 자리매김하고 있습니다. 중국의 EV 생산, 인도의 고속도로와 주택 계획, ASEAN의 패키징 공장이 총체로 소비를 확대하고 있습니다. 인도의 스마트 시티 임무와 같은 정부의 이니셔티브는 폴리머 접착 패널과 파이프에 의존하는 유틸리티 지출을 자극하고 있습니다.

북미는 성숙해지고 있지만, 경량 복합재와 기밀성이 높은 건물 외벽을 촉진하는 엄격한 연비와 건축 에너지 규제에 의해 꾸준한 성장을 기록하고 있습니다. 미국 환경보호청에 의한 저GWP건재에의 작용은 지붕재나 단열보드에 있어서의 저스모그 접착제 수요를 가속화하고 있습니다. 플라스틱 접착제 시장은 미국·멕시코·캐나다 협정으로부터도 혜택을 받고 있으며, 이 협정은 자동차용 접착제의 지역 조달에 인센티브를 부여해, 관세 면제의 자격을 부여하고 있습니다.

유럽은 재활용 가능한 접착제의 기술 혁신을 촉진하기 위해 녹색 거래 프레임 워크를 활용합니다. 생산자는 사용 된 소비재를 분해하고 폐쇄 루프의 플라스틱 흐름을 허용하기 위해 처방을 적용합니다. 항공우주 응용 분야에서 더 엄격한 EN 16603-20-01 아웃 가스 기준은 플라스틱 접착제 시장에서 틈새 시장이지만 귀중한 층을 열고 우주 등급 접착제를 인증하기 위해 공급업체를 압박합니다.

중동 및 아프리카에서는 해수 담수화, 태양열 인프라, 고층 접객 확장 프로젝트를 개최하고 있습니다. 고급 호텔은 사막의 기온에 대응하는 실리콘 웨더 씰을 채용하여 성장을 지원합니다. 라틴아메리카에서는 멕시코와 브라질에서 건설이 회복되고 온쇼어 전자 장비 조립이 증가하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 연구 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 자동차 산업에 있어서의 차량의 경량화의 추진

- 고성능 플라스틱으로의 건설 변화

- 포장·E-Commerce 업계에서의 수요 증가

- 의료용 웨어러블용의 바이오 베이스의 폴리우레탄 필름

- 모듈식 전기자동차 배터리 팩용 열 관리 접착제

- 시장 성장 억제요인

- 석유 원료 가격의 변동

- 세계 VOC 및 유해물질 규제 강화

- 외관 패널의 소방법 업그레이드

- 밸류체인 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 수지 유형

- 에폭시

- 시아노아크릴레이트

- 우레탄

- 실리콘

- 기타 수지 유형(아크릴, 핫멜트 EVA 등)

- 기술

- 용제 기반

- 수성 기반

- 최종 사용자 산업

- 자동차

- 건축 및 건설

- 전기 및 전자

- 의료

- 포장

- 기타 최종 사용자 산업(재생에너지, 소비재 등)

- 지역

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- 3M

- Arkema

- Avery Dennison Corporation

- BASF

- Dow

- Dymax

- HB Fuller Company

- Henkel AG and Co. KGaA

- Huntsman International LLC

- INTERTRONICS

- Master Bond Inc.

- Panacol-Elosol GmbH

- Permabond LLC

- Pidilite Industries Ltd.

- Sika AG

- Toyochem Co. Ltd.

제7장 시장 기회와 전망

KTH 25.10.31The Plastic Adhesives Market size is estimated at USD 9.19 Billion in 2025, and is expected to reach USD 11.52 Billion by 2030, at a CAGR of 4.62% during the forecast period (2025-2030).

The plastic adhesives market is transitioning from general-purpose bonding agents toward specialized chemistries that address electric-vehicle battery packs, medical wearables, and next-generation construction panels. Rising demand for lightweight vehicles, the shift to bio-based polyurethane films in healthcare, and stricter VOC legislation are widening application scopes across automotive, medical, and building sectors. Producers are releasing water-based and bio-derived grades that comply with evolving emission ceilings in China, the European Union, and the United States, enabling the plastic adhesives market to capture opportunities created by sustainability mandates. Competitive dynamics remain fluid as manufacturers adopt targeted M&A and joint-development agreements to close technology gaps, balance feedstock cost risks, and reach new geographic pockets.

Global Plastic Adhesives Market Trends and Insights

Lightweight-vehicle push in automotive industry

Automakers are replacing mechanical fasteners with structural adhesives to eliminate excessive weight and strengthen mixed-material designs. A typical 2025 electric SUV now integrates more than 400 linear feet of adhesive compared with fewer than 30 feet two decades ago, illustrating the structural role adhesives play in joining aluminum, carbon fiber, and engineering plastics. Impact-toughened elastomer-epoxy hybrids developed at Nagoya University deliver 22-times higher impact strength than legacy epoxies, which allows thinner panels and energy-absorbing crash structures while maintaining crashworthiness. With most OEMs committing to lighter bodies for range extension, the plastic adhesives market expects automotive consumption to climb at double-digit annual rates through 2030.

Construction shift to high-performance plastics

Facade and glazing systems are moving toward lightweight composite panels that demand long-life, high-modulus bonding agents. Sika's protective glazing adhesive family can absorb seismic loads yet retain rigidity for hurricane-rated curtain walls. High-rise retrofits in developed economies and green-field megaprojects in Asia require plastic adhesives that balance fire resistance, UV durability, and fast installation. Fast-cure PVC TrimWelder products reach 80% handling strength in 30 minutes, enabling contractors to accelerate project cycles without sacrificing code compliance.

Petro-feedstock price volatility

Epoxy and polyurethane base-resin costs fluctuate with crude oil and propylene trends. German liquid epoxy prices rose 1.73% in January 2025 amid thin inventories, while Asian contracts slipped 1.4% later that month as sellers cleared surplus ahead of the Spring Festival. Polyethylene spikes of 5 ¢/lb in the United States further lifted packaging-grade adhesive inputs. Covestro signed a certified mass-balance supply agreement with H.B. Fuller to mitigate fossil feedstock swings through ISCC-PLUS-accredited bio-naphtha streams.

Other drivers and restraints analyzed in the detailed report include:

- Increasing demand from packaging and e-commerce industry

- Bio-based polyurethane films for medical wearables

- Tightening global VOC and hazard regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy grades accounted for 32.45% of the plastic adhesives market size in 2024, underpinning structural joints in automotive body-in-white assemblies and steel-reinforced concrete panels. The high glass-transition temperature and chemical resistance keep epoxies relevant where shear loads and temperature spikes converge. Specialty cyanoacrylates, acrylics, and hybrid urethanes, however, exhibit the fastest 5.18% CAGR, as OEMs pursue rapid bonding in miniature electronics and need cold-cure alternatives for heat-sensitive substrates. The plastic adhesives market therefore balances epoxy's entrenched share with emergent niche chemistries that emphasize speed and flexibility. Cyanoacrylate packages such as H.B. Fuller's Cyberbond line allow viscosity tailoring for medical device micro-dosing while meeting ISO 10993 cytotoxicity requirements. Non-isocyanate polyurethanes made from bio-derived cyclic carbonates are scaling pilot lines, signalling a broader pivot toward sustainable resins inside the plastic adhesives market.

Manufacturers layer R&D to optimise adhesion promoters that interface with low-surface-energy polyolefins, aiming to unlock higher peel strengths without primers. Silicone-epoxy hybrids maintain hermetic seals in high-temperature electronics modules, giving formulators another route to differentiate. As environmental bans curb bisphenol-A derivatives, epoxy suppliers accelerate the launch of bis-F and novolac alternatives, guarding their sizeable plastic adhesives market share while aligning with upcoming endocrine-disruptor reviews in the EU.

The Plastic Adhesives Market Report is Segmented by Resin Type (Epoxy, Cyanoacrylate, Urethane, Silicones, Other Resin Types), Technology (Solvent-Based, Water-Based), End-User Industry (Automotive, Building and Construction, Electrical and Electronics, Medical, Packaging, Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific remains the principal manufacturing hub for engineering plastics, electronics, and footwear, positioning the region as the largest revenue contributor to the plastic adhesives market. China's EV output, India's highway and housing programs, and ASEAN's packaging plants collectively amplify consumption. Government initiatives such as India's Smart City Mission continue to stimulate public-works spending that relies on polymer-bonded panels and pipes.

North America, while mature, registers steady gains through stringent fuel-economy and building-energy codes that promote lightweight composites and air-tight building envelopes. The United States Environmental Protection Agency's push toward low-GWP construction materials accelerates demand for low-smog adhesives in roofing and insulation boards. The plastic adhesives market also benefits from the United States-Mexico-Canada Agreement, which incentivises regional sourcing of automotive adhesives to qualify for tariff exemptions.

Europe leverages its Green Deal framework to catalyse recyclable adhesive innovation. Producers adapt formulas to disassemble end-of-life consumer goods and enable closed-loop plastic flows. Stricter EN 16603-20-01 outgassing criteria in aerospace applications pressurise suppliers to certify space-grade adhesives, opening a niche yet valuable tier within the plastic adhesives market.

The Middle East and Africa host expansion projects in desalination, solar infrastructure, and high-rise hospitality. Premium hotel builds specify silicone weather-seals rated for desert temperatures, supporting incremental growth. Latin America's construction rebound and on-shore electronics assembly in Mexico and Brazil add diverse demand layers, albeit from a smaller base than the three dominant regions.

- 3M

- Arkema

- Avery Dennison Corporation

- BASF

- Dow

- Dymax

- H.B. Fuller Company

- Henkel AG and Co. KGaA

- Huntsman International LLC

- INTERTRONICS

- Master Bond Inc.

- Panacol-Elosol GmbH

- Permabond LLC

- Pidilite Industries Ltd.

- Sika AG

- Toyochem Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Lightweight-vehicle push in automotive industry

- 4.2.2 Construction shift to high-performance plastics

- 4.2.3 Increasing demand from packaging and e-commerce industry

- 4.2.4 Bio-based polyurethane films for medical wearables

- 4.2.5 Thermal-management adhesives for modular electric vehicle battery packs

- 4.3 Market Restraints

- 4.3.1 Petro-feedstock price volatility

- 4.3.2 Tightening global VOC and hazard regulations

- 4.3.3 Fire-safety code upgrades for facade panels

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 Resin Type

- 5.1.1 Epoxy

- 5.1.2 Cyanoacrylate

- 5.1.3 Urethane

- 5.1.4 Silicones

- 5.1.5 Other Resin Types (Acrylic, Hot-Melt EVA, etc.)

- 5.2 Technology

- 5.2.1 Solvent-based

- 5.2.2 Water-based

- 5.3 End-user Industry

- 5.3.1 Automotive

- 5.3.2 Building and Construction

- 5.3.3 Electrical and Electronics

- 5.3.4 Medical

- 5.3.5 Packaging

- 5.3.6 Other End-user Industries (Renewable Energy, Consumer Goods, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corporation

- 6.4.4 BASF

- 6.4.5 Dow

- 6.4.6 Dymax

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG and Co. KGaA

- 6.4.9 Huntsman International LLC

- 6.4.10 INTERTRONICS

- 6.4.11 Master Bond Inc.

- 6.4.12 Panacol-Elosol GmbH

- 6.4.13 Permabond LLC

- 6.4.14 Pidilite Industries Ltd.

- 6.4.15 Sika AG

- 6.4.16 Toyochem Co. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment