|

시장보고서

상품코드

1844714

탄소섬유 강화 열가소성(CFRTP) 복합재료 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Carbon Fiber Reinforced Thermoplastic (CFRTP) Composite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

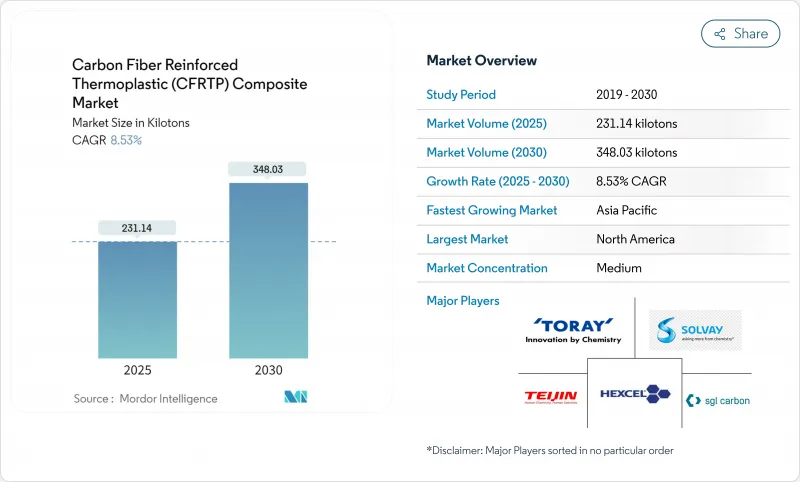

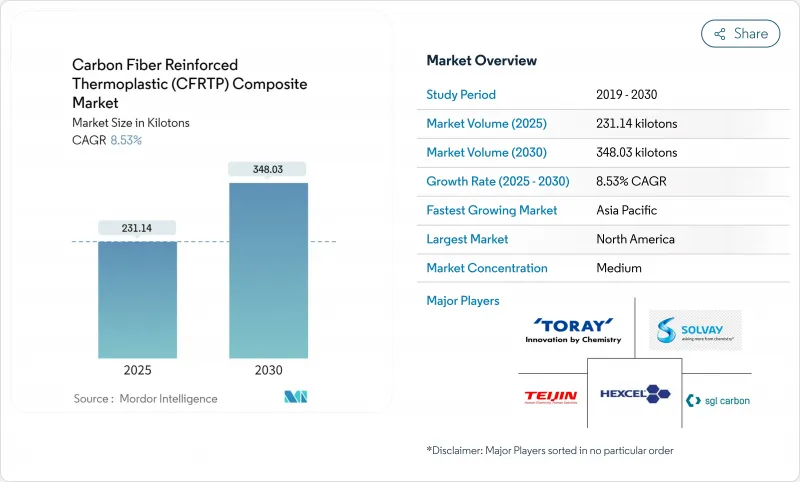

탄소섬유 강화 열가소성(CFRTP) 복합재료 시장 규모는 2025년에 231.14킬로톤으로 평가되었고, 예측기간(2025-2030년)의 CAGR은 8.53%를 나타낼 것으로 예측되며 2030년에 348.03킬로톤에 이를 전망입니다.

견고한 성장은 항공우주 등급의 강도 대비 중량 비율을 완전한 재활용성과 결합하는 소재의 능력을 반영하며, 운송, 에너지, 건설 분야의 탈탄소화 목표와 부합합니다. 전기차 생산 증가, 상업용 항공기 생산량 회복, 그리고 빠르게 진행되는 수소 저장 프로그램이 핵심 수요 축을 형성합니다. 동시에 에너지 효율적인 섬유 생산 및 적층 제조 분야의 혁신은 진입 장벽을 낮추는 한편, 지역별 재활용 의무화는 공급업체에게 새로운 수익원을 제공합니다. 통합된 기존 업체들이 지역별 생산 능력 확장과 전문 재활용 업체들에 맞서 시장 점유율을 방위함에 따라 경쟁 강도가 높아지고 있습니다.

세계의 탄소섬유 강화 열가소성(CFRTP) 복합재료 시장 동향 및 인사이트

경량 EV 구조에 대한 수요 급증

자동차 제조사들은 주행 거리 연장 및 충전 시간 단축을 위해 배터리 케이스, 차체 패널, 섀시 부재에 탄소섬유 열가소성 플라스틱 사용을 확대하고 있습니다. 이 소재의 가역적 용융 특성은 수명 종료 후 재활용을 지원하여 현재 중국과 유럽연합에서 시행 중인 순환경제 규정을 충족시킵니다. 손상된 부품을 교체하지 않고 재가열 및 재성형할 수 있어 수리가 용이해져 차량 운영사에게 이점이 발생합니다. 테슬라가 휴머노이드 로봇에 탄소섬유 복합재료를 적용한 사례는 차량을 넘어선 다용도성을 입증하며, 다양한 모빌리티 플랫폼으로의 확산 가능성을 시사합니다. 2024년 중국은 6만 9,000톤의 탄소섬유를 소비하며 아시아 수요 기반이 확대되고 있음을 보여주었습니다.

상업용 항공기 생산 가속화

항공기 본체 OEM 업체들은 737 MAX와 787 드림라이너의 생산량 목표 증가에 대응하기 위해 공급망을 재구축 중이며, 연료 소모를 줄이는 2차 구조용 복합재료 수요를 유지하고 있습니다. 헥셀은 2025년 1분기 실적 보고서에서 매출 감소에도 불구하고 경량 열가소성 솔루션에 대한 투자를 재확인했습니다. 전기 항공기로의 전환은 열가소성 수지 채택을 촉진합니다. 매트릭스가 배선을 절연하고 방빙 히터를 통합하기 때문입니다. 유럽의 열가소성 복합재료 연구 센터(TPRC) 주도 프로젝트는 대용량 부품 인증을 가속화하여 설계부터 비행까지의 기간을 단축합니다. 금속에 비해 우수한 피로 저항성은 정비 주기를 연장하며, 이는 코로나19 이후 항공사가 특히 중요하게 여기는 장점입니다.

높은 초기 투자 및 제조 비용

오토클레이브, 압축 프레스, 자동 섬유 배치 셀은 라인당 3천만 달러(약 300억 원)를 초과할 수 있어 진입 장벽을 높이고 가격 민감 부문에서의 채택 속도를 늦춘다. SGL 카본은 2024년 탄소섬유 부문의 매출이 35.2% 감소했다고 보고하며, 수요 변동으로 고정비 자산 활용률이 저조한 점을 원인으로 꼽았다. 리머릭 대학에서 시연한 플라즈마 + 마이크로파 가열 기술은 에너지를 최대 70% 절감하지만, 상용화까지는 수년이 더 소요될 전망입니다. 원료 섬유는 여전히 알루미늄이나 강철보다 비싸 복합재료가 경제형 차량에 적용되기 어렵다. 경제성은 양산으로 공구 비용을 상각할 때만 개선되므로, OEM 업체들은 하류 수요가 확정될 때까지 주저합니다.

부문 분석

PAN 기반 등급은 2024년 생산량의 78.12%를 차지하며 확고한 생산 라인과 항공우주 산업에서의 전통을 입증했습니다. 높은 인장 탄성률은 설계자가 안전 여유를 충족시키면서 구조적 무게를 줄일 수 있게 합니다. 기존 업체들이 연속 생산 라인을 개조하여 처리량을 높임에 따라 PAN 기반 등급의 탄소섬유 강화 열가소성 복합재료 시장 규모는 안정적인 연평균 7.9% 성장률(CAGR)로 확대될 전망입니다. 비용 효율적인 재가열 사이클은 스크랩률을 개선하여 공장 경제성을 높입니다.

재활용 섬유를 포함한 기타 원자재는 최종 사용자가 순환형 조달 목표를 채택함에 따라 원자재 중 가장 높은 연평균 9.71% 성장률을 기록하고 있습니다. 재활용 섬유는 현재 신규 섬유의 인장 강도 93.6%를 유지하여 2차 하중 경로 적용 범위가 확대되고 있습니다. Syensqo와 Trillium이 연구 중인 바이오 기반 아크릴로니트릴은 장기적으로 친환경 원료로의 전환을 예고합니다. 특수 피치 기반 등급은 금속과 유사한 전도성으로 배터리 팩의 열 관리에 활용됩니다. 물량은 적으나 프리미엄 가격 정책이 공급 제약을 상쇄하여 마진을 매력적으로 유지합니다.

PEEK는 250°C 연속 사용 온도와 화학적 불활성 덕분에 2024년 시장 점유율 34.51%를 확보했으며 연평균 성장률(CAGR) 9.82%로 성장을 주도하고 있습니다. 탄소섬유 강화 열가소성 복합재료 시장 점유율 우위는 가연성 및 연기 독성 규제가 엄격한 분야, 특히 제트 엔진과 해양 플랫폼에서 더욱 강화됩니다. 의료 기기 사용은 수익을 다각화하여 부문 간 위험을 분산시킵니다.

비용 중심 부문은 최고 온도를 가격과 교환하는 PU, PES 또는 PEI에 의존합니다. 이러한 수지는 작동 부하가 중간 수준인 내장 패널 및 소비자 전자제품에 공급됩니다. 탐색 중인 바이오 기반 PEI는 기계적 특성을 포기하지 않으면서 지속가능성 차별화 요소를 추가할 수 있습니다. 수지 제형사는 또한 전도성을 향상시키기 위해 나노 필러를 혼합하여 항공우주 시스템의 통합 제빙 층을 촉진합니다.

탄소섬유 강화 열가소성 복합재료 시장 보고서는 원재료(PAN 기반, 피치 기반 등), 수지(PEEK, PU 등), 제조 공정(압축 성형, AFP/테이프 레이잉 등), 최종 사용자 산업(항공우주 및 방위, 자동차 등), 지역(아시아태평양, 북미 등)별로 세분화됩니다. 시장 전망은 물량(킬로톤) 기준으로 제공됩니다.

지역별 분석

북미는 2024년 36.19% 점유율을 기록했으며, 이는 미국의 항공우주 및 방위 산업 단지를 기반으로 하고 캐나다의 MRO 허브가 뒷받침한 결과입니다. 토레이, 헥셀, 솔베이의 현지 진출은 리드 타임을 단축시켜 지정학적 위험으로부터 프로그램을 보호합니다. 인플레이션 감축법(IRA)에 따른 정부 보조금은 국내 수소 탱크 생산을 장려하여 다운스트림 수요를 확대하고 있습니다.

아시아태평양 지역은 2030년까지 9.21%의 가장 빠른 연평균 성장률(CAGR)을 기록할 전망입니다. 중국은 전기차 생산을 확대하며 현재 여러 킬로톤 규모의 탄소섬유 생산 라인을 보유해 기존 수입 의존도를 낮추고 있습니다. 일본의 선도 기업인 토레이와 테이진은 지역 풍력 및 해양 프로젝트 수요를 충족하기 위해 생산 능력을 두 배로 늘렸다. 한국은 전자 기술 노하우를 활용해 전자기 간섭(EMI) 차폐 복합재료를 5G 인프라에 통합하고 있습니다.

유럽은 강력한 수요와 새로운 규제 역풍이 공존합니다. 독일의 자동차 기반은 여전히 최대 부문 소비처이지만, 다가오는 재활용성 규제로 열가소성 대체가 가속화됩니다. 네덜란드의 열가소성 복합재료 연구 센터는 OEM과 공급업체 간 R&D 동맹을 주도합니다. 북유럽의 풍력 투자와 프랑스 항공우주 클러스터가 일반 산업 수요 부진을 상쇄합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 경량 EV 구조 수요 급증

- 상업용 항공기 생산 가속화

- 전 세계적 배출 및 재활용 의무 강화

- 건설 분야에서의 사용 증가

- 수소 압력 용기 프로그램의 급속한 확대

- 시장 성장 억제요인

- 높은 초기 투자 및 제조 비용

- 제한된 대규모 열성형 프레스 생산 능력

- 항공우주 분야에서 공급망의 무기화 위험

- 밸류체인 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측(수량)

- 원재료별

- 폴리아크릴로니트릴(PAN) 기반 탄소섬유 강화 복합재료(CFRTP)

- 피치 기반 탄소섬유 강화 복합재료(CFRTP)

- 기타 원료(재생 탄소섬유 등)

- 수지별

- 폴리에테르에테르케톤(PEEK)

- 폴리우레탄(PU)

- 폴리에테르 술폰(PES)

- 폴리에테르이미드(PEI)

- 기타(폴리아미드, 폴리카보네이트 등)

- 제조 공정별

- 압축 및 스탬프 성형

- AFP/테이프 레이잉

- 사출성형과 오버몰드

- 적층 조형(탄소섬유 함유 필라멘트)

- 최종 사용자 산업별

- 항공우주 및 방위

- 자동차

- 건설

- 전기 및 전자

- 풍력 터빈

- 해양

- 스포츠 장비

- 기타 최종 사용자 산업(헬스케어 등)

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- Arkema

- ARRIS Composites, Inc.

- Avient Corporation

- BASF

- Celanese Corporation

- DuPont

- Gurit Services AG, Zurich

- Hexcel Corporation

- Markforged

- Mitsubishi Chemical Corporation

- Quickstep

- SABIC

- SGL Carbon

- Syensqo

- Teijin Limited

- Toray Industries Inc.

- Victrex plc

제7장 시장 기회와 전망

HBR 25.11.07The Carbon Fiber Reinforced Thermoplastic Composite Market size is estimated at 231.14 kilotons in 2025, and is expected to reach 348.03 kilotons by 2030, at a CAGR of 8.53% during the forecast period (2025-2030).

Robust growth reflects the material's ability to pair aerospace-grade strength-to-weight ratios with full recyclability, aligning with decarbonization targets across transportation, energy, and construction. Rising electric-vehicle production, a rebound in commercial aircraft build rates, and fast-moving hydrogen storage programs form the core demand pillars. At the same time, breakthroughs in energy-efficient fiber production and additive manufacturing lower entry barriers, while regional recycling mandates open fresh revenue pools for suppliers. Competitive intensity is building as integrated incumbents defend share against regional capacity buildouts and specialist recyclers.

Global Carbon Fiber Reinforced Thermoplastic (CFRTP) Composite Market Trends and Insights

Surging Demand for Lightweight EV Structures

Automakers increase carbon fiber thermoplastic use in battery enclosures, body panels, and chassis members to extend driving range and cut charging time. The material's reversible melt behavior supports end-of-life recycling, satisfying circular-economy rules now unfolding in China and the European Union. Fleet operators benefit from easier repair because damaged parts can be reheated and reshaped instead of replaced. Tesla's application of carbon fiber composites in its humanoid robot underscores versatility beyond vehicles, suggesting spillover into multiple mobility platforms. China consumed 69,000 metric tons of carbon fiber in 2024, evidence of a deepening Asian demand base.

Accelerating Commercial Aircraft Production Ramp-ups

Airframe OEMs are rebuilding supply chains to meet higher 737 MAX and 787 Dreamliner output targets, sustaining composite demand for secondary structures that cut fuel burn. Hexcel reaffirmed investment in lightweight thermoplastic solutions in its Q1 2025 earnings report, despite lower top-line sales. The shift to more-electric aircraft fosters thermoplastic adoption because the matrix insulates wiring and integrates anti-icing heaters. European initiatives under the ThermoPlastic Composites Research Center (TPRC) accelerate certification of large-volume parts, shortening design-to-flight timelines. Superior fatigue resistance over metals lengthens service intervals, an advantage keenly valued by airlines after COVID-19 disruptions.

High Initial Investment and Manufacturing Cost

Autoclaves, compression presses, and automated fiber placement cells can top USD 30 million per line, curbing entry and slowing adoption in price-sensitive segments. SGL Carbon reported a 35.2% sales drop in its Carbon Fibers unit in 2024, citing demand swings that leave high fixed-cost assets under-utilized. Plasma + microwave heating demonstrated at the University of Limerick cuts energy up to 70%, yet commercial readiness remains several years out. Raw fiber remains costlier than aluminum or steel, keeping composites out of economy-class vehicles. Economics improve only when volumes amortize tooling, thus OEMs hesitate until downstream demand is locked.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Global Emission and Recyclability Mandates

- Rapid Scale-up of Hydrogen Pressure-Vessel Programs

- Limited Large-scale Thermoforming Press Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PAN-based grades delivered 78.12% of 2024 volume, underlining their entrenched production lines and aerospace heritage. High tensile modulus lets designers trim structural weight while meeting safety margins. The carbon fiber reinforced thermoplastic composite market size for PAN-based grades is projected to expand at a stable 7.9% CAGR as incumbents retrofit continuous lines for higher throughput. Cost-effective reheat cycles improve scrap rates, enhancing plant economics.

Other Raw Materials, including recycled fiber, register a 9.71% CAGR-the highest within raw materials-as end-users adopt circular procurement goals. Recycled fiber now retains 93.6% of virgin tensile strength, widening suitability for secondary load paths. Bio-sourced acrylonitrile under study by Syensqo and Trillium signals a longer-term pivot to greener feedstocks. Niche pitch-based grades serve thermal management in battery packs because of metal-like conductivity. Though volume small, premium pricing balances supply constraint, keeping margins attractive.

PEEK secured 34.51% 2024 share and leads growth at 9.82% CAGR thanks to 250 °C continuous-use temperature and chemical inertness. The carbon fiber reinforced thermoplastic composite market share advantage strengthens where flammability and smoke toxicity rules are strict, notably in jet engines and offshore platforms. Medical device usage diversifies revenue, spreading risk across sectors.

Cost-focused segments rely on PU, PES, or PEI which trade peak temperature for price. These resins feed interior panels and consumer electronics where operating loads are moderate. Bio-based PEI under exploration could add a sustainability differentiator without forfeiting mechanical properties. Resin formulators also blend nano-fillers to enhance conductivity, fostering integrated de-icing layers in aerospace systems.

The Carbon Fiber Reinforced Thermoplastic Composite Market Report is Segmented by Raw Material (PAN-Based, Pitch-Based, and More), Resin (PEEK, PU, and More), Manufacturing Process (Compression Molding, AFP/Tape Laying, and More), End-User Industry (Aerospace and Defense, Automotive, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Volume (Kilotons).

Geography Analysis

North America held 36.19% share in 2024, anchored by the United States' aerospace and defence complex and supported by Canada's MRO hubs. Local presence of Toray, Hexcel, and Solvay shortens lead times, safeguarding programs against geopolitical risk. Government grants under the Inflation Reduction Act encourage domestic hydrogen tank production, widening downstream pull.

Asia-Pacific posts the fastest 9.21% CAGR to 2030. China scales electric-vehicle output and now hosts multiple kiloton-scale carbon fiber lines, reducing earlier import dependence. Japanese pioneers Toray and Teijin double capacity to serve regional wind and marine projects. South Korea leverages electronics know-how to integrate EMI-shielding composites into 5G infrastructure.

Europe mixes strong demand with new regulatory headwinds. Germany's auto base remains the largest segment consumer, but looming recyclability rules fast-track thermoplastic substitution. The ThermoPlastic Composites Research Center in the Netherlands anchors R&D alliances across OEMs and suppliers. Nordic wind investments and French aerospace clusters offset softness in general industrial demand.

- Arkema

- ARRIS Composites, Inc.

- Avient Corporation

- BASF

- Celanese Corporation

- DuPont

- Gurit Services AG, Zurich

- Hexcel Corporation

- Markforged

- Mitsubishi Chemical Corporation

- Quickstep

- SABIC

- SGL Carbon

- Syensqo

- Teijin Limited

- Toray Industries Inc.

- Victrex plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for lightweight EV structures

- 4.2.2 Accelerating commercial aircraft production ramp-ups

- 4.2.3 Stringent global emission and recyclability mandates

- 4.2.4 Incresaing usage in the construction sector

- 4.2.5 Rapid scale-up of hydrogen pressure-vessel programs

- 4.3 Market Restraints

- 4.3.1 High initial investment and manufacturing cost

- 4.3.2 Limited large-scale thermoforming press capacity

- 4.3.3 Supply-chain weaponisation risk in aerospace

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Raw Material

- 5.1.1 Polyacrylonitrile (PAN)-based Carbon Fiber Reinforced Composites (CFRTP)

- 5.1.2 Pitch-based Carbon Fiber Reinforced Composites (CFRTP)

- 5.1.3 Other Raw Materials (Recycled Carbon Fibers, etc.)

- 5.2 By Resin

- 5.2.1 Polyether Ether Ketone (PEEK)

- 5.2.2 Polyurethane (PU)

- 5.2.3 PolyetherSulfone (PES)

- 5.2.4 Polyetherimide (PEI)

- 5.2.5 Others (Polyamide, Polycarbonate, etc.)

- 5.3 By Manufacturing Process

- 5.3.1 Compression and Stamp Moulding

- 5.3.2 Automated Fibre Placement / Tape Laying

- 5.3.3 Injection and Over-Moulding

- 5.3.4 Additive Manufacturing (Carbon Fiber-filled filaments)

- 5.4 By End-user Industry

- 5.4.1 Aerospace and Defence

- 5.4.2 Automotive

- 5.4.3 Construction

- 5.4.4 Electrical and Electronics

- 5.4.5 Wind Turbines

- 5.4.6 Marine

- 5.4.7 Sporting Equipments

- 5.4.8 Other End-user Industries (Healthcare, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Arkema

- 6.4.2 ARRIS Composites, Inc.

- 6.4.3 Avient Corporation

- 6.4.4 BASF

- 6.4.5 Celanese Corporation

- 6.4.6 DuPont

- 6.4.7 Gurit Services AG, Zurich

- 6.4.8 Hexcel Corporation

- 6.4.9 Markforged

- 6.4.10 Mitsubishi Chemical Corporation

- 6.4.11 Quickstep

- 6.4.12 SABIC

- 6.4.13 SGL Carbon

- 6.4.14 Syensqo

- 6.4.15 Teijin Limited

- 6.4.16 Toray Industries Inc.

- 6.4.17 Victrex plc

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment