|

시장보고서

상품코드

1844720

산소 제거제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Oxygen Scavengers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

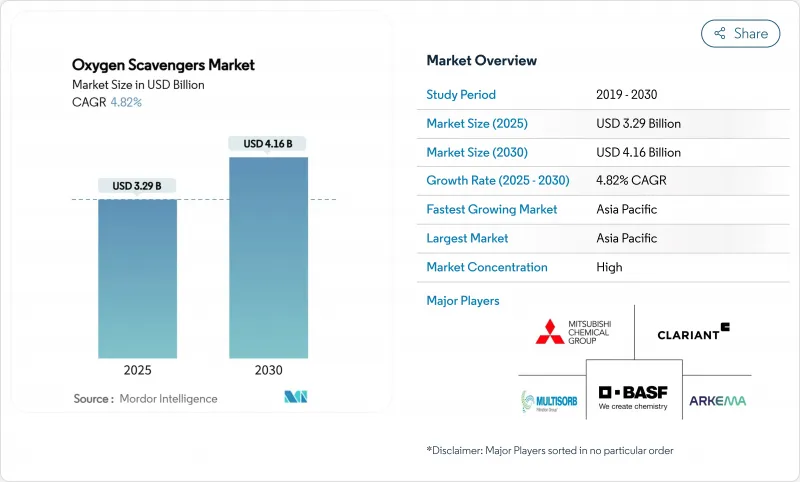

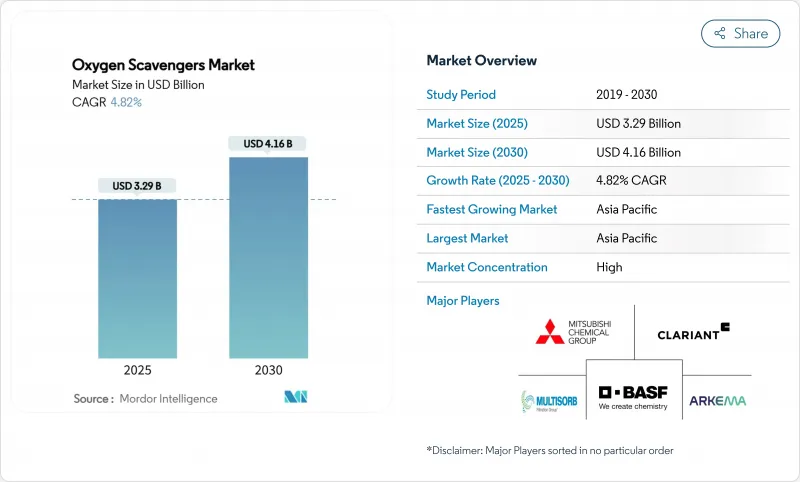

산소 제거제 시장 규모는 2025년에 32억 9,000만 달러로 평가되었고, 예측기간(2025-2030년)의 CAGR은 4.82%를 나타낼 것으로 예측되며 2030년에 41억 6,000만 달러에 이를 전망입니다.

수요는 기존 철분 분말에서 폴리머 통합 및 효소 기반 시스템으로 전환되며, 이는 브랜드 소유자가 더 엄격한 유통기한, 순도 및 재활용성 목표를 충족하는 데 기여합니다. 아시아태평양 지역은 다층 포장 필름의 핵심 생산 거점인 반면, 북미는 고부가가치 제약 응용 분야를 주도하며, 양 지역 모두 글로벌 공급업체의 원자재 조달 전략에 영향을 미칩니다. FDA의 인간 식품 프로그램 및 EU 규정 2025/40과 같은 규제들은 금속 이온 이동을 방지하는 비금속 제형으로의 전환을 가속화하고 있습니다. 최종 사용 분야 전반에 걸쳐, 전자상거래 붐은 브랜드 소유자들이 복잡한 주문 처리 네트워크를 통해 수주간에 걸친 운송 과정에서도 효과성을 유지하는 산소 관리 기술을 선택하도록 강제하며, 이는 산소 흡수제 시장의 중기 성장을 지속시키고 있습니다.

세계의 산소 제거제 시장 동향 및 인사이트

신선 즉석 및 냉장 포장 식품의 급속한 성장

편의 식품으로의 소비자 습관 변화는 육류, 수산물 및 델리 카테고리 전반에 걸쳐 능동적 산소 관리 기술의 적용 범위를 확대했습니다. 브랜드 소유자들은 열성형 트레이에 봉지 없는 산소 제거층을 통합하여 제품이 장기간 냉장 보관 및 소매 진열 중에도 색상 안정성을 유지하도록 합니다. 지역 슈퍼마켓 체인들은 폐기물 감소와 상품 진열 유연성 향상을 주요 이점으로 꼽으며, 저온에서 신속히 활성화되는 솔루션을 공동 포장업체에 요구하고 있습니다. 이에 장비 공급업체들은 밀봉 무결성을 해치지 않는 산소 흡수 수지가 사전 충전된 다층 필름을 수용하기 위해 고속 트레이 밀봉 라인을 개조하고 있습니다. 이러한 도입 동향은 미국과 독일에 위치한 필름 압출기 업체들의 꾸준한 주문 유입으로 이어져 산소 흡수제 시장의 기본 성장세를 강화하고 있습니다.

의약품 포장 내 잔류 산소에 대한 약전 기준 강화

최신 USP 및 EMA 가이드라인은 비경구 및 고형 제형 팩의 잔류 산소에 상한선을 설정하여 의약품 제조업체에 명시된 보존 기간 동안 0.5% 미만의 산소를 유지하는 장벽 시스템을 검증하도록 촉구하고 있습니다. 카라콘의 PharmaKeep 시리즈와 같은 폴리머 기반의 스캐빈저는 상대 습도 10-90%로 기능하여 금속 이온의 위험을 피하면서 의약품의 습도 감수성에 대응할 수 있습니다. 유럽의 규제도 비슷한 궤도를 따르고 있으며, 2025년 3월에 발효된 EU의 개정 식품 접촉 재료 규제는 의약품 포장 재료에 영향을 미치는 순도 요건과 전환 제한의 강화를 도입했습니다. 이러한 진보는 미량 산소가 단백질의 분해를 촉매할 수 있는 생물학적 제제와 수년간의 안정성 데이터를 필요로 하는 수분 반응성 저분자 치료제에서 두드러집니다.

금속 이온 오염과 관능적 변질 우려

철 기반 봉지는 미량의 이온을 방출하여 민감한 기능성 식품에서 산화 반응을 촉진하고 고급 차 및 커피에서 금속성 이취를 유발할 수 있습니다. 규제 감사관들은 이제 최악의 습도 조건 하에서의 이주 시험을 요구하여 일부 브랜드 소유자들이 고가 SKU에 대해 철 기반 시스템을 완전히 배제하도록 하고 있습니다. 폴리머 캡슐화 방법은 직접 접촉 위험을 낮추지만, 소규모 제조업체들이 감당하기 어려운 원자재 비용을 증가시킵니다. 이러한 상충 관계는 제약 및 특수 식품 채널에서 기존 봉지의 단기적 보급을 억제하여 산소 흡수제 시장의 일부 성장을 제한하고 있습니다.

부문 분석

금속 제형은 확립된 공급망, 빠른 흡수 동역학 및 낮은 단위 비용 덕분에 2024년 산소 흡수제 시장 점유율 57.89%를 유지했습니다. 이 부문의 규모 이점은 글로벌 육류 가산업체 및 스낵 생산업체와의 대량 계약으로 이어져, 입문용 용도 분야의 산소 흡수제 시장 규모를 견인하고 있습니다. 그러나 비금속 시스템은 8.60%의 연평균 복합 성장률(CAGR)로 모든 소재 그룹 중 가장 빠르게 성장하고 있습니다. 폴리머 통합 변형 제품은 최종 공정에서의 봉지 삽입 필요성을 제거하여 고속 충전 및 밀봉 라인의 전환 시간을 단축합니다. 효소 및 아스코르브산 제형은 금속 첨가제를 제한하는 할랄, 코셔 및 클린 라벨 브랜드를 위한 선택지를 더욱 확대합니다. 제약 감사에서 폴리머 시스템의 습도 제어 창고 호환성이 점점 더 강조되면서, 블리스터 필름 압출기 업체들이 아모소브(Amosorb) 및 파마키프(PharmaKeep) 농축액 채택을 촉진하고 있습니다. 나노 복합 촉매에 대한 지속적인 연구 개발은 특히 단위 가격이 주류 스낵 식품 예산과 일치할 경우, 2030년 이후 비금속 솔루션이 철 기반 제품의 우위를 잠식할 수 있음을 시사합니다. 이러한 역학 관계는 산소 흡수제 시장 내 소재 부문 다양성을 강화합니다.

2세대 화학 기술은 또한 재활용 의무와 부합하는데, 이는 박막 라미네이트 대신 단일 소재 PET 또는 PP 구조에 제거 능력을 내장하는 방식이기 때문입니다. 이는 EU 규정 2025/40 하의 순환 경제 목표를 지원하는 접근법입니다. 수지 공급업체들은 2030년까지 재활용 함량 30% 달성을 약속한 음료 브랜드의 요구를 충족시키며, 흐림 현상 증가를 최소화한 병-병 재활용 가능성을 입증했습니다. 한편 금속성 소분 포장제 제조업체들은 분말 입자 크기 최적화와 해상 운송 중 조기 활성화를 지연시키는 흡습성 완충제 첨가로 대응하고 있습니다. 따라서 소재 플랫폼 간 경쟁은 활성화 제어, 단위 경제성, 다운스트림 재활용 성능의 균형에 집중되며, 이 경쟁은 산소 흡수제 시장에서 변환업체와 글로벌 CPG 구매자 모두의 조달 결정을 좌우할 것입니다.

세계의 산소 제거제 시장 보고서는 업계를 유형별(금속 산소 제거제와 비금속 산소 제거제), 최종 사용자 업계별(식품 및 음료, 제약, 석유 및 가스, 전력 등), 지역별(북미, 남미, 유럽, 중동 및 아프리카)으로 분류하고 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

아시아태평양은 2024년 수요의 38.05%를 차지하고, 2030년까지의 CAGR은 7.50%로 예측됩니다. 이는 중국의 의약품 수출 기반의 확대와 인도의 유연한 필름 전환에 있어서 급속한 생산능력 증강에 뒷받침된 것입니다. 이 지역의 각국 정부는 콜드체인 물류에 대한 보조금을 지속적으로 지급하고 식품 폐기물 감축의 국가 목표를 설정하고 있으며 액티브 배리어 솔루션의 채택을 자극하고 있습니다. 이 지역은 원료 공급망이 확립되어 국내 시장과 수출 시장 모두에 대응하는 식품 가공 산업 수요가 증가하고 있다는 장점이 있습니다. 미쓰비시가스화학은 일본의 MGC 에이지레스와 태국의 에이지레스 등 자회사를 통해 이 지역에 강한 존재를 가지고 있으며, 산소 제거제의 생산과 유통을 지원하는 인프라가 확립되어 있음을 보여줍니다.

북미는 산소 제거제 시장에 있어서 성숙했지만 기술적으로 진행된 시장입니다. FDA의 엄격한 감독은 철저한 전환 시험을 의무화하고 있으며, 완전히 문서화된 폴리머 배합에 대한 수요가 증가하고 있습니다. 브랜드 소유자는 주 수준의 확장 생산자 책임 규칙에 따라 기계적 재활용 목표를 충족하는 솔루션을 선호합니다. 캐나다의 육류 가산업자는 아시아를 위한 수출 항해에 대응하기 위해 대용량의 가방과 자동 삽입 장치를 지정하여 안정적인 대체 수요를 유지하고 있습니다. 멕시코에서는 편의점 부문이 성장하고 지역 성장을 더욱 뒷받침하고 있지만 비용 압력으로 수동적 장벽과 능동적 장벽이 혼합되어 있습니다.

유럽은 북미의 규제 촉진요인을 반영하고 있지만, 추가 순환 경제의 야심을 거듭하고 있습니다. EU 규칙 2025/40은 2030년까지 모든 포장을 재활용할 수 있도록 의무화되었으며, 회수 기능을 통합한 단일 소재 구조에 대한 투자에 박차를 가하고 있습니다. 프랑스와 독일의 주요 음료 그룹은 비금속 첨가제를 포함한 PET 병용 프리폼을 시험적으로 제조하여 산소 보호와 보증금 리턴 시스템의 무결성을 도모하고 있습니다. 동유럽의 필름 압출업체는 구미공급자로부터 폴리머 콘센트레이트를 수입하게 되어 있어 기술 격차의 해소와 채택의 확산을 볼 수 있습니다. 중동 및 아프리카와 남미는 절대량으로는 후진을 숭배하고 있지만, 현대적인 식료품 소매업태의 확대에 따라 관심이 가속되고 있습니다. 이러한 신흥국 시장에서는 개발은행이 자금을 제공하는 실증 프로젝트가 활성산소 관리의 부패 저감 효과를 실증하고 있어 산소 제거제 시장에 대한 중기적인 수요 유입이 안정되어 있음을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 신선 즉석 및 냉장 포장 식사의 급속한 성장

- 의약품 포장 내 잔류 산소에 대한 약전 기준 강화

- 무균 콜드체인 식사 키트 물류 확대

- 나노 복합 폴리머 스캐빈저 상용화

- 장기간 운송 유통기한에 대한 전자상거래 수요

- 시장 성장 억제요인

- 금속 이온 오염 및 관능적 변질 우려

- 비용 효율적이고 고차단성 필름 대체재

- 변동성 높은 철광석 및 특수 촉매 가격 변동

- 밸류체인 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 유형별

- 금속 산소 제거제

- 비금속 산소 제거제

- 최종 사용자 산업별

- 식품 및 음료

- 의약품

- 석유 및 가스

- 전력

- 화학

- 펄프 및 제지

- 기타 최종 사용자 산업(수처리, 폐수처리 등)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 태국

- 인도네시아

- 베트남

- 말레이시아

- 필리핀

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 튀르키예

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 남아프리카

- 나이지리아

- 이집트

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- Accepta Water Treatment

- Arkema

- Avient Corporation

- BASF

- Clariant

- Desiccare Inc.

- Ecolab

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- Multisorb

- Solenis

- Veolia

제7장 시장 기회와 전망

HBR 25.11.07The Oxygen Scavengers Market size is estimated at USD 3.29 billion in 2025, and is expected to reach USD 4.16 billion by 2030, at a CAGR of 4.82% during the forecast period (2025-2030).

Demand pivots from conventional iron powders toward polymer-integrated and enzyme-based systems that help brand owners satisfy stricter shelf-life, purity and recyclability targets. Asia-Pacific represents the core production base for multilayer packaging films while North America drives high-value pharmaceutical applications, and both regions influence raw-material sourcing strategies for global suppliers. Regulations such as the FDA's Human Foods Program and EU Regulation 2025/40 are amplifying the shift toward non-metallic formulations that avoid metal-ion migration. Across end-uses, the e-commerce boom forces brand owners to choose oxygen management technologies that remain effective during weeks-long journeys through complex fulfilment networks, sustaining medium-term growth for the oxygen scavengers market.

Global Oxygen Scavengers Market Trends and Insights

Rapid Growth in Fresh-Ready & Chilled Packaged Meals

Shifts in consumer habits toward convenience foods have widened deployment of active oxygen management across meat, seafood and deli categories. Brand owners integrate sachet-free scavenging layers into thermoformed trays so products remain color-stable throughout extended chilled storage and retail display. Regional supermarket chains cite reduced waste and improved merchandising flexibility as key benefits, prompting co-packers to specify solutions that activate rapidly at low temperatures. Equipment suppliers are therefore adapting high-speed tray-sealing lines to accommodate multilayer films pre-loaded with scavenging resins that do not compromise seal integrity. This adoption dynamic feeds a steady order pipeline for film extruders located in the United States and Germany, reinforcing baseline growth for the oxygen scavengers market.

Stricter Pharmacopeia Limits on Residual Oxygen in Drug Packs

The latest USP and EMA guidelines cap residual oxygen in parenteral and solid-dose packs, urging drug makers to validate barrier systems that sustain <=0.5% oxygen throughout the stated shelf life. Polymer-based scavengers such as Colorcon's PharmaKeep series can function across 10-90% relative humidity, addressing drug-product moisture sensitivity while avoiding metal-ion risks. the European regulations are following similar trajectories, with the EU's revised food contact material regulations effective March 2025 introducing enhanced purity requirements and migration limits that affect pharmaceutical packaging materials .Contract development organizations embed such additives directly into polyolefin blisters, which simplifies line qualification versus separate sachets. These advances are most visible in biologics, where trace oxygen can catalyze protein degradation, and in moisture-reactive small-molecule therapies that require multi-year stability data.

Metal-Ion Contamination & Sensory-Taint Concerns

Iron-based sachets release trace ions that can catalyze oxidative reactions in sensitive nutraceuticals and lead to metallic off-notes in premium teas and coffees. Regulatory auditors now require migration testing under worst-case humidity, prompting some brand owners to exclude ferrous systems entirely for high-value SKUs. Polymer encapsulation methods lower direct contact risk, yet they raise raw-material costs that smaller manufacturers struggle to absorb. This trade-off tempers near-term penetration of traditional sachets in pharmaceutical and specialty-food channels, restraining a portion of the oxygen scavengers market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Aseptic Cold-Chain Meal-Kit Logistics

- Commercialization of Nanocomposite Polymer Scavengers

- Cost-Effective and High-Barrier Film Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metallic formulations retained 57.89% oxygen scavengers market share in 2024 thanks to established supply chains, rapid absorption kinetics and low unit cost. The segment's scale advantage translates into volume contracts with global meat processors and snack producers, anchoring the oxygen scavengers market size for entry-level applications. However, non-metallic systems are growing at an 8.60% CAGR, the fastest among all material groups. Polymer-integrated variants eliminate the need for end-of-line sachet insertion, which shortens changeover time on high-speed fill-and-seal lines. Enzyme and ascorbic-acid formulations further widen options for halal, kosher and clean-label brands that restrict metallic additives. Pharmaceutical audits increasingly cite polymer systems' compatibility with humidity-controlled warehouses, encouraging blister-film extruders to adopt Amosorb and PharmaKeep concentrates. Continuous R-&D around nanocomposite catalysts suggests non-metallic solutions could erode iron's lead beyond 2030, especially if unit prices align with mainstream snack food budgets. Collectively, these dynamics reinforce material-segment diversity within the oxygen scavengers market.

Second-generation chemistries also align with recycling mandates because they embed scavenging capacity in mono-material PET or PP structures rather than laminated foil, an approach that supports circular-economy targets under EU Regulation 2025/40. Resin suppliers have demonstrated bottle-to-bottle recyclability with minimal haze increase, satisfying beverage-brand commitments to 30% recycled content by 2030. Meanwhile, metallic sachet makers counter by optimizing powder particle size and adding moisture-absorbing buffers that delay premature activation during ocean transit. Competition across material platforms therefore centers on balancing activation control, unit economics and downstream recycling performance, a contest that will shape procurement decisions for both converters and global CPG buyers in the oxygen scavengers market.

The Global Oxygen Scavenger Market Reports Segments the Industry by Type (Metallic Oxygen Scavengers and Non-Metallic Oxygen Scavengers), End-User Industry (Food and Beverage, Pharmaceutical, Oil and Gas, Power and More), and Geography (Asia-Pacific, North America, South America, Europe, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 38.05% of 2024 demand and is projected to deliver a 7.50% CAGR to 2030, underpinned by China's expanding pharmaceutical export base and India's rapid capacity additions in flexible-film conversion. Governments across the region continue to subsidize cold-chain logistics and set national targets for food-waste reduction, stimulating adoption of active barrier solutions. The region benefits from established supply chains for raw materials and growing demand from food processing industries that serve both domestic and export markets. Mitsubishi Gas Chemical's strong presence in the region through subsidiaries like MGC AGELESS Co., Ltd. in Japan and AGLESS (THAILAND) CO., LTD. demonstrates the established infrastructure supporting oxygen scavenger production and distribution.

North America represents a mature but technically advanced arena for the oxygen scavengers market. Stringent FDA oversight mandates exhaustive migration testing and drives demand for fully documented polymer formulations. Brand owners prioritize solutions compatible with mechanical recycling targets under state-level extended producer responsibility rules. Canadian meat processors, dealing with export voyages toward Asia, specify high-capacity sachets and automated insertion equipment, sustaining steady replacement demand. Mexico's rising convenience-food sector further supports regional growth, although cost pressures favour a mix of passive and active barriers.

Europe mirrors North American regulatory drivers but layers additional circular-economy ambitions. EU Regulation 2025/40 will require all packaging to be recyclable by 2030, spurring investments in mono-material structures with embedded scavenging capability. Large beverage groups in France and Germany pilot PET bottle preforms containing non-metallic additives, aligning oxygen protection with deposit-return systems. Eastern European film extruders increasingly import polymer concentrates from Western suppliers, bridging technology gaps and spreading adoption. The Middle East & Africa and South America trail in absolute volume yet show accelerating interest as modern grocery retail formats expand. Across these emerging regions, demonstration projects funded by development banks illustrate the spoilage-reduction benefits of active oxygen management, pointing toward steady medium-term demand inflows for the oxygen scavengers market.

- Accepta Water Treatment

- Arkema

- Avient Corporation

- BASF

- Clariant

- Desiccare Inc.

- Ecolab

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- Multisorb

- Solenis

- Veolia

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Growth in Fresh-Ready and Chilled Packaged Meals

- 4.2.2 Stricter Pharmacopeia Limits on Residual Oxygen in Drug Packs

- 4.2.3 Expansion of Aseptic Cold-Chain Mealkit Logistics

- 4.2.4 Commercialisation of Nanocomposite Polymer Scavengers

- 4.2.5 E-commerce Demand for Longer Transit Shelf-Life

- 4.3 Market Restraints

- 4.3.1 Metal-Ion Contamination & Sensory-Taint Concerns

- 4.3.2 Cost-Fffective and High-Barrier Film Substitutes

- 4.3.3 Volatile Iron-Ore and Specialty Catalyst Price Swings

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Metallic Oxygen Scavengers

- 5.1.2 Non-metallic Oxygen Scavengers

- 5.2 By End-user Industry

- 5.2.1 Food and Beverage

- 5.2.2 Pharmaceutical

- 5.2.3 Oil and Gas

- 5.2.4 Power

- 5.2.5 Chemical

- 5.2.6 Pulp and Paper

- 5.2.7 Other End-user Industries (Water and Waste-Water Treatment, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Thailand

- 5.3.1.6 Indonesia

- 5.3.1.7 Vietnam

- 5.3.1.8 Malaysia

- 5.3.1.9 Philippines

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Turkey

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 South Africa

- 5.3.5.5 Nigeria

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Accepta Water Treatment

- 6.4.2 Arkema

- 6.4.3 Avient Corporation

- 6.4.4 BASF

- 6.4.5 Clariant

- 6.4.6 Desiccare Inc.

- 6.4.7 Ecolab

- 6.4.8 MITSUBISHI GAS CHEMICAL COMPANY, INC.

- 6.4.9 Multisorb

- 6.4.10 Solenis

- 6.4.11 Veolia

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment