|

시장보고서

상품코드

1846172

낙서 방지 코팅 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Anti-Graffiti Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

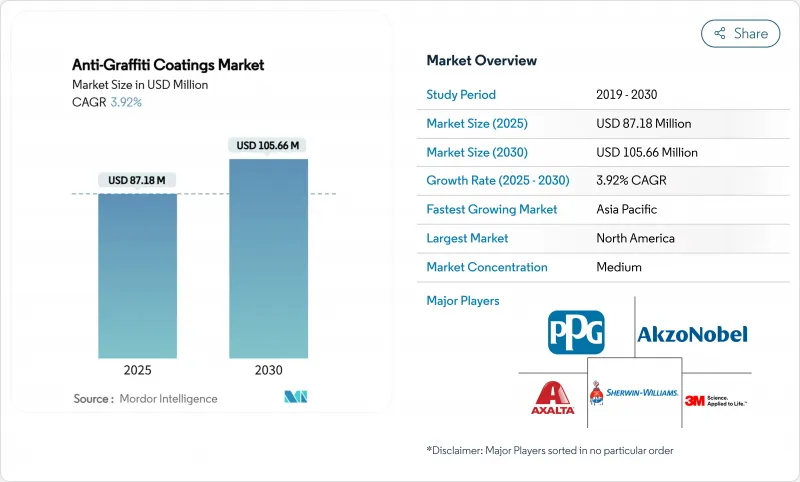

낙서 방지 코팅 시장 규모는 2025년에 8,718만 달러로 추정되고, 2030년에는 1억 566만 달러에 이를 것으로 예상되며, 예측 기간(2025-2030년)의 CAGR은 3.92%를 나타낼 전망입니다.

캘리포니아에서 프랑스, 호주에 이르기까지 퍼플루오로알킬 물질(PFAS)과 폴리플루오로알킬 물질(PFAS)의 점진적인 폐지가 확산됨에 따라 수성 및 실리콘이 풍부한 화학물질에 대한 결정적인 축족이 성장을 형성하고 있습니다. 지방자치단체의 낙서제거 예산 증가, 아시아태평양 인프라 파이프라인 활황, 휘발성 유기화합물(VOC)에 대한 규제 단속은 건설과 교통 자산에 걸쳐 내구성이 뛰어나고, 저배출 가스 제품에 대한 수요를 뒷받침하고 있습니다. 듀얼 펑션과 파우더 형식의 병렬 기술 혁신이 경쟁 기회를 확대하는 한편, 원재료 비용의 변동과 새로운 기재에의 접착의 과제가 단기적인 확대를 억제하고 있습니다.

세계의 낙서 방지 코팅 시장 동향과 인사이트

낙서 제거에 대한 지자체 지출 증가

각 도시는 정기적인 유지 보수의 배분을 초과하는 파괴 행위의 상승을 억제하기 위해 예산을 앞당깁니다. 포틀랜드의 긴급 조례 1099-2024는 2020년부터 2022년 사이에 낙서에 대한 불만이 586% 급증했으며, 웰링턴 시의회는 2025년까지 보호 프로그램에 757만 달러를 확보했습니다. 독일철도는 청소에 연간 800만 유로를 소비하고 있기 때문에 무용제의 세척 사이클을 반복해도 괜찮은 폴리실라잔 배리어를 채용하고 있습니다. 제거를 반복하는 것보다 예방 쪽이 저렴하다는 것이 판명되었기 때문에 지방 자치체의 조달에서는 도시의 미관을 유지해, 라이프 사이클 코스트를 최소한으로 억제하는 영구적인 저 VOC(휘발성 유기 화합물) 코팅이 점점 선호되고 있습니다. 이 교대는 공공 인프라와 교통에서 낙서 방지 코팅 시장의 꾸준한 수량 확보로 이어져 공급업체의 중기 수익 전망을 지원합니다.

공공 인프라 건설의 급속한 확대

아시아태평양의 건설 러시는 표면 보호 솔루션의 기준선 수요를 밀어 올리고 있습니다. 중국의 2024년 국가개발개혁위원회 로드맵은 국내 수요의 기폭제로 '고품질 인프라'를 강조했으며 철도, 교량, 스마트시티 프로젝트에서 낙서방지사양 개발을 가속화했습니다. 인도와 인도네시아의 병렬 스마트 모빌리티 복도는 미래의 유지 보수 비용을 억제하기 위해 영구 코팅을 조달 기준에 통합합니다. 미국 연방정부의 '바이클린' 이니셔티브에서도 비슷한 자금이 제공되어 저탄소 건축재료에 20억 달러 이상의 자금이 흘러 수성으로 휘발성 유기화합물(VOC)에 준거한 제품에 대한 기호가 기울어지고 있습니다. 신흥 허브 계약자는 확립된 청소 차량 없이 운영하는 경우가 많으며, 내구성 있는 코팅을 평생 비용을 줄이는 선행적인 안전 방법으로 간주하고, 낙서 방지 코팅 시장의 장기적인 보급을 뒷받침하고 있습니다.

휘발성 실록산과 불소 수지의 원재료 비용

실록산과 불소 수지의 가격 변동은 최종 사용자가 가격에 민감한 지금 생산자의 마진을 압박하고 있습니다. 이산화규소(SiO2)를 포함한 특정 규소화합물에 대한 규칙을 강화하는 유럽화학청의 제안은 공급망에 대한 경계를 강화하고 컴플라이언스 비용을 증가시킵니다. 생산자는 내구성을 보장하면서 실록산 부하를 줄이는 하이브리드 화학 물질을 시도파관만 재 설계 장애물과 인증 타임라인은 롤아웃을 지연시킵니다. 스팟 구매에 의존하는 소규모 배합 제조업체는 비용 전가의 현저한 위험에 직면하고 있으며, 낙서 방지 코팅 시장의 당면 생산량을 억제하고 있습니다.

부문 분석

비희생 시스템은 2024년에 낙서 방지 코팅 시장 점유율의 52.18%를 차지했고, 2030년까지의 CAGR은 4.48%를 나타낼 전망입니다. 고객은 라이프 사이클 비용을 줄이는 한 번 도포하고 헹굼 반복 세척의 내성을 선호합니다. 세미 희생형은 중간 정도의 재도장 간격으로 중간 정도의 예산을 만족하지만, 희생형 필름은 역사적 보존이나 내구성 폴리머를 사용할 수 없는 섬세한 기재에 대응합니다.

비희생층의 높은 초기 비용도, 재도장을 위한 교통역이나 공공시설의 폐쇄가 적으면 상쇄됩니다. 폴리우레탄-파우더 배리어의 사례 연구는 광택을 잃지 않고 1,000회 이상의 세척 사이클을 초과해도 워시오프 내성이 있음을 보여줍니다. 이러한 경제성은 프리미엄 틈새를 강화하고 낙서 방지 코팅 시장의 가치 집중을 지원합니다.

낙서 방지 코팅의 보고서는 유형(희생, 반 희생, 비 희생), 기술(수성, 솔벤트, 분체 코팅), 최종 사용자 산업(자동차, 운송, 건설 및 기타 최종 사용자 산업), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 2024년에 낙서 방지 코팅 시장 점유율의 39.25%를 유지했습니다. 포틀랜드의 긴급 조례 1099-2024와 유사한 도시는 보호 페인트를 연간 유지 보수 예산에 통합하여 예측 가능한 경상 수주로 이어지고 있습니다. 이 지역의 바이 클린 조항은 연방 자금을 저탄소, 수성층으로 향하게 하고, 적합한 공급업체를 우선 벤더에 밀어 올립니다. 캘리포니아의 대기질 관리지구(AQMD)는 비조막 도료에 100g/L의 휘발성 유기화합물(VOC) 상한을 설정하여 연구개발(R&D) 생산에 계속 박차를 가해 세계에 출하되는 제품 라인에 영향을 주고 있습니다.

2030년까지의 CAGR이 4.21%로 가장 급성장하고 있는 것은 아시아태평양이며, 이것은 중국의 인프라 정비 가속과 인도의 스마트 시티 100 도시 전개에 추진되고 있습니다. 지하철의 지주와 보도교에 예방 코팅을 지정하는 도시 평의회는 미래의 청소 노동력의 급증을 피하기 위한 것입니다. 일본과 한국과 같은 성숙시장은 환경정책 강화에 따라 기존 철도와 고속도로 자산을 낮은 VOC층에서 개수함으로써 흐름을 유지하고 있습니다.

유럽은 첨단 환경 규제 하에서 꾸준히 성장하고 있습니다. 프랑스의 과불소·폴리불소알킬물질(PFAS) 금지령과 유럽연합(EU)의 광범위한 규제(보류중)에 의해 수지의 선택사항이 바뀌어, 실리콘이나 바이오폴리머의 연구가 급피치로 진행되고 있습니다. 독일에서는 매년 2억 유로를 넘는 낙서 피해가 발생하고 있기 때문에 영구적인 장벽에 대한 재정적인 견해가 선명해지고 있으며, 지자체의 컨소시엄이 낙서 방지 조항을 담은 장기 유지 보수 계약을 맺도록 촉구하고 있습니다. 남미와 중동, 아프리카는 현재 규모가 작은 것, 상파울루와 리야드에서 급속한 지하철 개수를 통해 공간을 확보하고 있으며, 낙서 방지 코팅 시장을 다지역적인 확산에 자리잡고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 낙서 제거에 대한 지자체 지출 증가

- 공공 인프라 건설의 급속한 확대

- 휘발성 유기 화합물(VOC) 규제의 엄격화에 의해 수성 배합이 가속

- 스마트 시티용 스트리트 패니처에의 낙서 방지 분체 도료 채용

- 교통 시설에서 낙서 방지와 항균 표면의 융합

- 시장 성장 억제요인

- 휘발성 실록산 및 불소 수지 원료 비용

- 불소계 코팅에 영향을 미치는 퍼플루오로알킬 물질(PFAS) 및 폴리플루오로알킬 물질(PFAS)의 새로운 규제

- 고다공질 3D 프린팅 콘크리트 표면에의 접착 과제

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모·성장 예측

- 유형별

- 희생

- 반희생

- 비희생

- 기술별

- 수성

- 용제형

- 분체 도장

- 최종 사용자 산업별

- 자동차 및 수송

- 건설

- 기타 최종 사용자 산업(산업 장비, 유틸리티)

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- 3M

- AkzoNobel NV

- Axalta Coating Systems LLC

- BASF

- CSL Silicones Inc.

- Dulux

- Hempel A/S

- Hydron Protective Coatings Ltd

- IFS Coatings

- IGP Pulvertechnik AG

- Nano-Care Deutschland AG

- Nukote Coating Systems International

- PPG Industries Inc.

- Saint-Gobain

- Teknos Group

- The Sherwin-Williams Company

- Urban Hygiene Ltd

- WRMeadows, Inc.

- Wacker Chemie AG

제7장 시장 기회와 전망

KTH 25.11.07The Anti-Graffiti Coatings Market size is estimated at USD 87.18 Million in 2025, and is expected to reach USD 105.66 Million by 2030, at a CAGR of 3.92% during the forecast period (2025-2030).

Growth is shaped by a decisive pivot toward water-based and silicone-rich chemistries as Per- and polyfluoroalkyl substances (PFAS) phase-outs spread from California to France and Australia. Higher municipal graffiti-removal budgets, brisk infrastructure pipelines in Asia-Pacific, and regulatory crack-downs on Volatile Organic Compounds (VOCs) are sustaining demand for durable, low-emission products across construction and transit assets. Parallel innovation in dual-function and powder formats is broadening competitive opportunities while raw-material cost swings and adhesion challenges on novel substrates temper short-run expansion.

Global Anti-Graffiti Coatings Market Trends and Insights

Escalating Municipality Spending on Graffiti Removal

Cities are front-loading budgets to curb soaring vandalism costs that outpace routine maintenance allocations. Portland's Emergency Ordinance 1099-2024 follows a 586% jump in graffiti complaints between 2020 and 2022, while Wellington City Council ring-fenced USD 7.57 Million for protective programmes through 2025 . Deutsche Bahn's EUR 8 Million annual outlay on cleanup has pushed the rail operator toward polysilazane barriers that tolerate repeated solvent-free wash cycles. As prevention proves cheaper than serial removal, municipal procurement increasingly favours permanent, low-VOC (Volatile Organic Compound) coatings that preserve urban aesthetics and minimise life-cycle costs. This shift anchors steady volume off-take for the anti-graffiti coatings market in public infrastructure and transit assets, underpinning suppliers' medium-term revenue visibility.

Rapid Expansion of Public Infrastructure Construction

Asia-Pacific construction booms are boosting baseline demand for surface-protection solutions. China's 2024 National Development and Reform Commission roadmap highlights "high-quality infrastructure" as a domestic-demand catalyst, accelerating anti-graffiti specification in rail, bridge, and smart-city projects. Parallel smart-mobility corridors in India and Indonesia are embedding permanent coatings into procurement standards to curb future maintenance outlays. Similar funding flows from the United States' Federal Buy Clean initiative channel more than USD 2 Billion toward low-carbon building materials, tilting preferences to water-based, Volatile Organic Compound (VOC)-compliant offerings. Contractors in emerging hubs, often operating without established cleaning fleets, view durable coatings as an upfront safeguard that lowers whole-life costs, reinforcing long-run uptake across the anti-graffiti coatings market.

Volatile Siloxane and Fluoropolymer Raw-Material Costs

Siloxane and fluoropolymer pricing swings are squeezing producer margins at a time when end-users remain price sensitive. European Chemicals Agency proposals to tighten rules on certain silicon compounds, including Silicon Dioxide (SiO2), have heightened supply-chain caution and inflated compliance expenditures. Producers are experimenting with hybrid chemistries that trim siloxane loads while safeguarding durability, yet re-engineering hurdles and certification timelines slow roll-outs. Smaller formulators reliant on spot purchases face pronounced cost pass-through risks, restraining near-term output in the anti-graffiti coatings market.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Volatile Organic Compound (VOC) Norms Accelerating Water-borne Formulations

- Adoption of Anti-graffiti Powder Coatings for Smart-city Street Furniture

- Emerging Per- and polyfluoroalkyl substances (PFAS) Restrictions Affecting Fluorinated Coatings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Non-sacrificial systems held 52.18% of anti-graffiti coatings market share in 2024 and are expanding at a 4.48% CAGR to 2030. Customers favour their one-time application and rinse-repeat cleaning tolerance that shrink life-cycle spend. Semi-sacrificial formats satisfy mid-tier budgets with moderate recoat intervals, while sacrificial films cater to historic preservation or sensitive substrates that cannot host durable polymers.

Higher upfront expenditure on non-sacrificial layers is offset by fewer closures of transit stations or public buildings for re-painting. Case studies on polyurethane-powder barriers show wash-off resilience beyond 1,000 cleaning cycles without gloss loss. These economics reinforce the premium niche, anchoring value concentration within the anti-graffiti coatings market.

The Anti-Graffiti Coatings Report is Segmented by Type (Sacrificial, Semi-Sacrificial, and Non-Sacrificial), Technology (Water-Based, Solvent-Based, and Powder Coating), End-User Industry (Automotive and Transportation, Construction, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 39.25% of the Anti-Graffiti Coatings market share in 2024. Portland's Emergency Ordinance 1099-2024 and similar city mandates integrate protective coatings into annual maintenance budgets, translating to predictable recurrent orders. The region's Buy Clean clauses funnel federal funds toward low-carbon, water-based layers, pushing compliant suppliers up the preferred-vendor ladder. California's Air Quality Management District (AQMD) caps of 100 g/L Volatile Organic Compound (VOC) on non-sacrificial coatings continue to spur research and development (R&D) output, influencing product lines shipped worldwide.

Asia-Pacific is the fastest-expanding territory at 4.21% CAGR through 2030, propelled by China's infrastructure acceleration and India's 100-smart-city rollout. Urban councils specifying preventive coatings for metro pillars and pedestrian bridges aim to avoid future cleaning labour spikes. Mature markets such as Japan and South Korea sustain flow by retrofitting existing rail and highway assets with low-VOC layers in line with tightened environmental policies.

Europe grows steadily under the weight of progressive environmental regulation. France's Per- and polyfluoroalkyl substances (PFAS) embargo and the European Union (EU)'s pending wide-spectrum restriction are reshuffling resin choices and fast-tracking silicone and bio-polymer research. Germany's graffiti damage exceeding EUR 200 Million each year sharpens the financial case for permanent barriers, encouraging municipal consortiums to award long-term maintenance contracts featuring anti-graffiti clauses. South America and the Middle East & Africa, while smaller today, are carving space through rapid metro upgrades in Sao Paulo and Riyadh, positioning the anti-graffiti coatings market for multi-regional breadth.

- 3M

- AkzoNobel N.V.

- Axalta Coating Systems LLC

- BASF

- CSL Silicones Inc.

- Dulux

- Hempel A/S

- Hydron Protective Coatings Ltd

- IFS Coatings

- IGP Pulvertechnik AG

- Nano-Care Deutschland AG

- Nukote Coating Systems International

- PPG Industries Inc.

- Saint-Gobain

- Teknos Group

- The Sherwin-Williams Company

- Urban Hygiene Ltd

- W.R.Meadows, Inc.

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Municipality Spending on Graffiti Removal

- 4.2.2 Rapid Expansion of Public-infrastructure Construction

- 4.2.3 Stricter Volatile Organic Compound (VOC) Norms Accelerating Water-borne Formulations

- 4.2.4 Adoption of Anti-graffiti Powder Coatings for Smart-city Street Furniture

- 4.2.5 Convergence of Anti-graffiti & Antimicrobial Surfaces in Transit Assets

- 4.3 Market Restraints

- 4.3.1 Volatile Siloxane & Fluoropolymer Raw-material Costs

- 4.3.2 Emerging Per- and polyfluoroalkyl substances (PFAS) Restrictions Affecting Fluorinated Coatings

- 4.3.3 Adhesion Challenges on Highly Porous 3D-Printed Concrete Facades

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Sacrificial

- 5.1.2 Semi-Sacrificial

- 5.1.3 Non-Sacrificial

- 5.2 By Technology

- 5.2.1 Water-Based

- 5.2.2 Solvent-Based

- 5.2.3 Powder Coating

- 5.3 By End-User Industry

- 5.3.1 Automotive and Transportation

- 5.3.2 Construction

- 5.3.3 Other End-User Industries (Industrial Equipment, Utilities)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 AkzoNobel N.V.

- 6.4.3 Axalta Coating Systems LLC

- 6.4.4 BASF

- 6.4.5 CSL Silicones Inc.

- 6.4.6 Dulux

- 6.4.7 Hempel A/S

- 6.4.8 Hydron Protective Coatings Ltd

- 6.4.9 IFS Coatings

- 6.4.10 IGP Pulvertechnik AG

- 6.4.11 Nano-Care Deutschland AG

- 6.4.12 Nukote Coating Systems International

- 6.4.13 PPG Industries Inc.

- 6.4.14 Saint-Gobain

- 6.4.15 Teknos Group

- 6.4.16 The Sherwin-Williams Company

- 6.4.17 Urban Hygiene Ltd

- 6.4.18 W.R.Meadows, Inc.

- 6.4.19 Wacker Chemie AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

- 7.2 Introduction of Bio-based Technology Coatings