|

시장보고서

상품코드

1846236

항바이러스 치료제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Anti-Viral Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

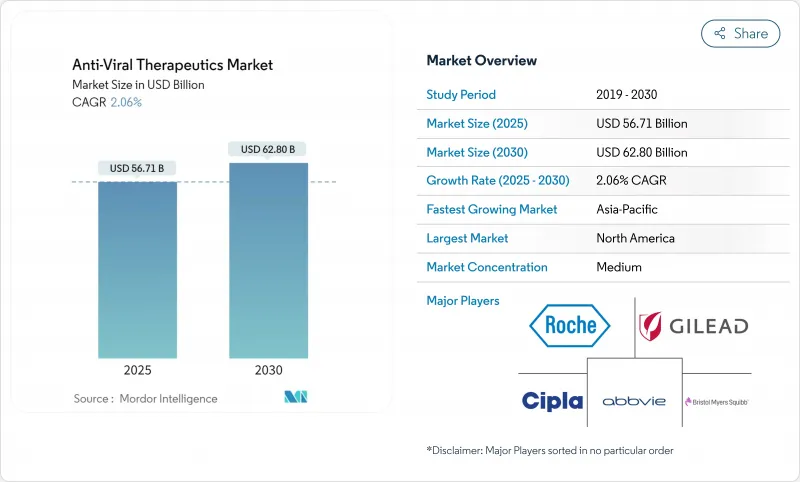

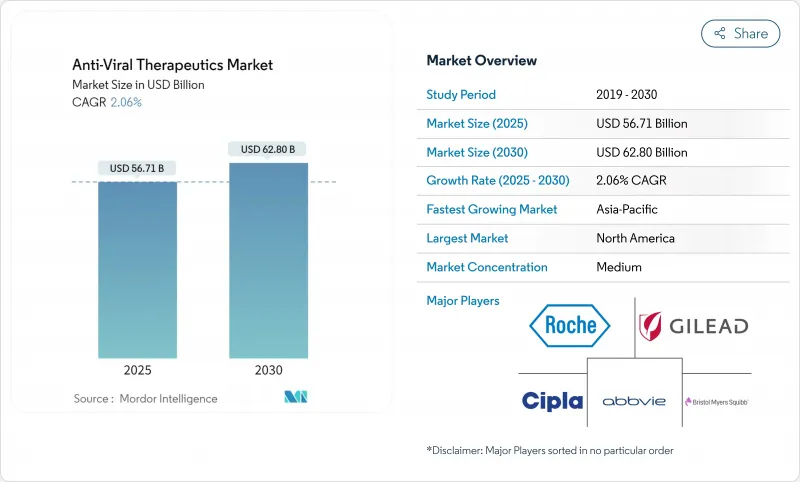

항바이러스 치료제 시장 규모는 2025년에 567억 1,000만 달러, 2030년에는 CAGR 2.06%로 628억 달러에 이를 것으로 예상됩니다.

장시간 작용형 제제, AI를 활용한 리드 화합물 탐색, 정부가 지원하는 광역 스펙트럼 프로그램 등이 현재 투자의 중심인 한편, 제1세대 항바이러스 치료제의 특허 만료이 두드림 성장을 억제하고 있습니다. 신흥경제국에서는 가격 규제가 강화되고 있어 치료제 개발 기업은 유리한 상환을 확보하기 위해 실제 임상에서의 증거 패키지를 우선하고 있습니다. 경쟁의 치열성은 규모가 큰 기업이 여전히 세계적인 유통을 지배하고 있기 때문에 완만하지만, 차별화된 생명공학 파이프라인이 프리미엄 파트너십을 이끌고 있습니다. 항바이러스 치료제 시장은 또한 콜드체인의 생산 능력 확대로 생물 제제와 장시간 작용형 주사제에 대한 액세스가 확대되어 공급망의 경직화에도 대응하고 있습니다.

세계의 항바이러스 치료제 시장 동향과 인사이트

장시간 작용 주사제 파이프라인 확대

연 2회 복용 레나카파비르는 2025년 항바이러스 치료제 시장에 진출하여 저자원 환경에서 중요한 장벽인 통원 횟수를 줄임으로써 어드히어런스에 대한 기대를 즉시 쇄신했습니다. 독자적인 나노크리스탈 캐리어는 최대 6개월 동안 약물 농도를 유지하고 바이러스 억제 지속성을 향상시키고 모니터링 비용을 절감합니다. 머크의월1회 경구 투여의 MK-8527은 이 실증에 근거해, 방출 캡슐의 개량이 주사제에 필적하는 편리성을 실현하는 다음의 파를 나타내는 것입니다. 의료 시스템의 능력 향상이 가장 중요한 것은 과도한 부담을 겪고 있는 클리닉이 매일 정제 투여 프로그램을 방해하는 지역입니다. 투약 누출의 감소는 치료 진행 비용의 감소로 이어지므로 지불자는 이러한 요법을 점점 선호하고 있습니다. 제조가 성숙함에 따라 1일 1회 투여의 경구약과 동등한 가격 설정이 될 것으로 예상되며, 현재 판매량의 중심이 되고 있는 얼리어댑터 시장뿐만 아니라 세계적인 보급이 가속될 것으로 기대됩니다.

HIV 병용 요법의 채용 급증

임상 현장에서는 3제 병용 요법에서 바이러스량이 검출되지 않는 상태를 유지하면서 누적 독성을 억제하는 2제 병용 요법이나 장시간 작용형 요법으로 이행하고 있습니다. 레나카파비르+이슬라트라빌과 같은 공동 제제는 내성에 대한 여러 기전에 의한 커버력을 확보하려고 하는 것으로, GSK-ViiV사의 VH499/VH184 프로그램은 신규의 표적 영역에서 동일한 전략을 답습한 것입니다. 규제당국은 어드히어런스의 향상이 하류의 공중위생상의 이익을 창출하기 때문에 이러한 합제에 우선심사로 보상하고 있습니다. 기존의 프로테아제 억제제로 제네릭 침식에 직면한 기존 제약 기업의 경우 차세대 합제는 방어 가능한 마진을 제공하여 브랜드 수명주기를 연장합니다. 항바이러스 치료제 시장은 환자 1인당 가치 향상으로 이익을 얻는 반면, 환자는 병존 질환을 앓고 나이가 들수록 정제 수가 줄어들고 약물 간 상호작용의 위험이 감소합니다.

AI를 활용한 Nucleos(t)ide 아날로그 설계

바이러스 중합효소의 구조로부터 학습한 머신러닝 모델은 결합 친화성과 대사 부채를 in silico로 예측함으로써 아날로그 최적화에 소요되는 시간을 줄여줍니다. Exscientia의 파이프라인은 AI가 어떻게 코로나바이러스, 인플루엔자, 파라믹소바이러스 패밀리에 걸쳐 효능을 보유하는 화합물을 확인하고 광역 스펙트럼 커버리지 추진을 지원하는 방법을 보여줍니다. 알고리즘에 의한 내성 예측은 병용 요법의 설계를 유도하여 조기 교차 내성의 가능성을 감소시킵니다. 그 결과, 규제 당국이나 지불자에게 좋은 인상을 주는 데이터 풍부한 자료가 됩니다. 계산기에 의한 초기 투자는 고액이지만, 사이클 타임의 단축과 임상 이탈률의 저하는 비용을 상쇄하는 것 이상의 효과가 있어, 항바이러스 치료제 업계 전체의 연구 개발 이익률을 향상시킵니다.

부문 분석

인플루엔자 항바이러스 치료제는 2024년 262억 달러를 초래해 항바이러스 치료제 시장 규모의 46.29%를 차지했습니다. 폴리머라제 산성(PA) 억제제 및 폴리머라제 염기성(PB2) 억제제의 파이프라인은 꾸준히 진행되고 있으며, 치료 옵션을 넓히고, 뉴라미니다제 내성에 대항할 수 있습니다. 한편, COVID-19/SARS-CoV-2 치료제는 유행성의 긴급성에서 유래하는 것이지만, 현재는 특히 면역 결핍 집단 사이에서 노출 후 예방이 지지되고 있기 때문에 2030년까지의 CAGR은 3.78%를 나타낼 전망입니다. B형 간염과 C형 간염의 성숙 부문은 치유 또는 기능적 치유 요법으로 치료 기간이 단축되기 때문에 두드러지지만, 아시아와 아프리카에서 질병 부담을 감안하면 여전히 큰 규모를 유지하고 있습니다. 헤르페스 치료에서 마이크로니들 패치와 내부 겔 제형은 우수한 병변 조절을 약속합니다. RSV와 CMV의 프로그램에서는 단일클론항체와 저분자 융합 억제제가 활용되어 소아 적응이 성장의 여지가 되고 있습니다.

항바이러스 치료제 시장은 단일 병원체 전략에서 숙주를 대상으로 하는 약물과 유행에 대비한 광역 스펙트럼 약물로 이동하고 있습니다. 이러한 프로그램은 공적 자금을 필요로 하지 않고 좁은 역학적 피크를 피할 수 있습니다. CMV 제형은 여전히 틈새 이식 집단을 지원하므로 높은 가격으로 판매되지만 수량은 제한적입니다. 미래경쟁 구도은 신속한 아웃 브레이크 대응 능력과 가족 간의 효능에 달려 있으며 바이러스 유형의 히에랄 키는 예측 기간 동안 대체 될 것으로 보입니다.

역전사효소 억제제는 HIV와 B형 간염 치료의 기간제로서 2024년 항바이러스 치료제 시장 점유율의 33.94%를 나타냈습니다. 화학적 개선의 적층은 내성 장벽과 신성 프로파일을 개선하여 제네릭 의약품의 침공에 대한 관련성을 유지하고 있습니다. 레나카파비르로 대표되는 캡시드 억제제는 CAGR로 카테고리를 선도하는 3.91%를 나타내며, 연 2회 투여에 의해 투여 빈도의 예상을 바꾸고 있습니다. 프로테아제 억제제는 계속 COVID-19의 급성기 관리에 필수적이며, 폴리머라제/뉴클레오시드 아날로그는 크로스바이러스의 신뢰성을 유지하고 있지만, 흡입 가능한 제제나 소아용 제제에 의한 차별화를 도모하고 있습니다.

RNAi와 안티센스 제형은 늦은 임상시험으로 옮겨가고 있지만, 단기적인 상업적 영향을 억제하는 전달 과제에 직면하고 있습니다. 광범위한 스펙트럼을 가진 저분자는 정부의 비축 계약을 획득했으며 예측할 수없는 대형 유행에 대한 헤지가되었습니다. 이러한 작용 메커니즘에 균형 잡힌 포트폴리오를 가진 기업은 내성 사이클과 가격 변동을 극복하는 데 가장 적합합니다. 향후 5년 동안 캡시드 기반 억제제 및 숙주 인자 억제제와 관련된 항바이러스 치료제 시장 규모는 임상 검증 및 제조 규모의 수렴에 따라 두 배가 될 수 있습니다.

지역 분석

북미는 2024년 매출액의 34.91%를 차지하고 FDA의 합리화된 지정과 프리미엄 항바이러스 치료제에 환불을 하는 지불자의 회의 깊이에 지지되었습니다. 미국을 중심으로 한 연구 개발 거점이 퍼스트 인 클래스의 약제를 신속하게 개발하고 전문 약국의 물류가 통합되어 전국에 신속한 유통이 가능합니다. 그러나 메디케어의 약가협상은 프리온보드 가격을 압박하고 실제 바이러스학적 결과에 의존하는 가치 기반 계약으로 기업을 향하게 하고 있습니다.

중국, 인도, 동남아시아가 국내 의약품 생산능력과 국민 모두 보험제도에 다액 투자를 하고 있기 때문에 아시아태평양의 CAGR은 가장 빠른 4.19%를 나타낼 전망입니다. 2024년 중국의 신약 승인 건수는 228건에 달하고, 규제 당국이 구미의 심사 속도에 맞출 의향을 나타내, 다국적 기업이 현지에서의 공동 개발 파트너십을 맺게 되었습니다. 인도에서는 비용 최적화된 생산 체제가 지역 수요에 대응하고, 일본의 고령화 사회는 재활성화 대상포진이나 RSV에 대한 항바이러스 치료제의 지속적인 사용을 지지하고 있습니다. 동시에, 콜드체인 프레임워크의 개선은 생물제제에 대한 접근을 확대하고, 지역의 항바이러스 치료제 시장을 더욱 확대합니다.

유럽은 안정적인 시장 가치를 유지하고 있지만 가격 협상은 엄격하고 의료 기술 평가를 사용하여 비용 효율적인 임계 값을 강제합니다. EMA의 중앙 집중화된 절차는 블록 동시 진입에 매력적이지만, 브렉짓 후 이중 신청은 복잡성을 증가시킵니다. 남유럽과 동유럽 국가들은 EU의 의료 재건 기금에 의해 지원되며, 백신과 항바이러스 치료제의 인지도가 높아짐에 따라 판매량이 증가할 수 있습니다. 전반적으로 지리적 다양화는 수익 위험을 분산하지만 컴플라이언스 비용을 높이기 위해 세계 규제를 활용하는 것이 섹터 리더의 핵심 역량입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 장시간 작용형 주사제 파이프라인의 확대

- HIV 병용 요법의 채용 급증

- COVID-19 주도의 항바이러스 연구개발의 파급

- AI를 활용한 핵산 아날로그 설계

- 광역 스펙트럼 약제에의 공적 자금 제공

- 항바이러스 치료제에 축발을 옮기는 mRNA 플랫폼

- 시장 성장 억제요인

- 항바이러스 치료제 내성 변이 증가

- 가격억제와 상환의 역풍

- 바이오 세이프티 그레이드의 제조 병목

- 저소득 지역의 콜드체인 격차

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 업계의 라이벌 관계

제5장 시장 규모·성장 예측

- 바이러스 유형별

- HIV/에이즈

- B형 간염

- C형 간염

- 인플루엔자

- 헤르페스(HSV)

- 호흡기 세포융합 바이러스(RSV)

- 거대세포 바이러스(CMV)

- 기타 및 신종 바이러스

- 약제 클래스별/작용 기전별

- 역전사효소 억제제(NRTI/NNRTI)

- 프로테아제 억제제

- 중합효소/뉴클레오시드 유사체 억제제

- RNAi 및 안티센스 치료제

- 광범위 스펙트럼 저분자 항바이러스 치료제

- 캡시드 억제제

- 기타

- 투여 경로별

- 경구

- 주사제(장기 작용형 포함)

- 국소

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Gilead Sciences Inc.

- GlaxoSmithKline plc(ViiV Healthcare)

- Merck & Co., Inc.

- F. Hoffmann-La Roche AG

- AbbVie Inc.

- Johnson & Johnson(Janssen)

- Bristol Myers Squibb Co.

- Pfizer Inc.

- Novartis AG

- AstraZeneca plc

- Cipla Ltd.

- Dr. Reddy's Laboratories

- Aurobindo Pharma Ltd.

- Lupin Ltd.

- Sun Pharmaceutical Inds.

- Shionogi & Co., Ltd.

- Takeda Pharmaceutical Co.

- Vir Biotechnology, Inc.

- Regeneron Pharmaceuticals

- Eli Lilly and Company

제7장 시장 기회와 전망

KTH 25.11.07The Anti-Viral Therapeutics market size is USD 56.71 billion in 2025 and is forecast to reach USD 62.80 billion by 2030 at a 2.06% CAGR, highlighting a stable but opportunity-rich arena where legacy small molecules meet high-value delivery innovations.

Long-acting formulations, AI-guided lead discovery, and government-backed broad-spectrum programs headline the current investment focus, while patent expiries on first-generation antivirals temper headline growth. Therapeutic developers are prioritizing real-world evidence packages to secure favorable reimbursement as price-control rules tighten in major economies. Competitive intensity remains moderate because scale players still dominate global distribution, yet differentiated biotech pipelines are attracting premium partnerships. The Anti-Viral Therapeutics market is also navigating supply-chain hardening, with cold-chain capacity expansions enabling wider access to biologics and long-acting injectables.

Global Anti-Viral Therapeutics Market Trends and Insights

Expanding Long-Acting Injectable Pipelines

Twice-yearly lenacapavir entered the Anti-Viral Therapeutics market in 2025 and immediately reframed adherence expectations by reducing clinic visits, a key barrier in low-resource settings. Proprietary nanocrystal carriers maintain drug levels for up to six months, improving viral suppression persistence and cutting monitoring costs. Building on this proof point, Merck's once-monthly oral MK-8527 flags a next wave where modified-release capsules rival injectables for convenience. Health-system capacity gains matter most in regions where over-burdened clinics hinder daily pill programs. Payers increasingly favor these regimens because fewer missed doses translate to lower progression-of-care costs. As manufacturing matures, pricing parity with daily orals is anticipated, accelerating global uptake beyond the early adopter markets that currently anchor volumes.

Surge in HIV Combination-Therapy Adoption

Clinical practice is pivoting from three-drug backbones toward dual or long-acting pairings that limit cumulative toxicity while sustaining undetectable viral loads . Co-formulations such as lenacapavir plus islatravir seek to lock in multi-mechanism coverage against resistance, and GSK-ViiV's VH499/VH184 program echoes the same strategy in a novel target space. Regulators are rewarding these fixed-dose combinations with priority reviews because the adherence upside generates downstream public-health benefits. For pharmaceutical incumbents that face generic erosion on older protease inhibitors, next-generation combos deliver a defendable margin and extend brand lifecycles. The Anti-Viral Therapeutics market benefits from higher per-patient values, while patients see fewer pills and reduced drug-drug interaction risk as they age with comorbidities.

AI-Enabled Nucleos(t)ide Analog Design

Machine-learning models trained on viral polymerase structures are cutting years from analog optimization by predicting binding affinity and metabolic liabilities in silico. Exscientia's pipeline showcases how AI-directed iterations can identify compounds that retain potency across coronavirus, influenza, and paramyxovirus families, supporting the push for broad-spectrum coverage. Algorithmic resistance forecasting guides combination-therapy design, reducing the likelihood of early cross-resistance. The result is a data-rich dossier that impresses regulators and payers alike. Although upfront computational investment is high, cycle-time savings and lower clinical attrition more than offset costs, boosting return on R&D across the Anti-Viral Therapeutics industry.

Other drivers and restraints analyzed in the detailed report include:

- COVID-19-Driven Antiviral R&D Spill-Over

- Rising Antiviral-Resistance Mutations

- Price-Control & Reimbursement Headwinds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Influenza antivirals delivered USD 26.2 billion in 2024, equal to 46.29% of the Anti-Viral Therapeutics market size, underscoring entrenched seasonal demand and clinical familiarity. Steady pipeline progress toward polymerase acidic (PA) and polymerase basic (PB2) inhibitors broadens therapeutic options and may counter neuraminidase resistance. Meanwhile, COVID-19/SARS-CoV-2 treatments, though originating from pandemic urgency, now post a 3.78% CAGR through 2030 as post-exposure prophylaxis gains favor, especially among immunocompromised cohorts. Mature hepatitis B and C segments plateau because cure or functional-cure regimens shorten treatment durations, yet remain sizeable given disease burden in Asia and Africa. Herpes therapies are benefiting from micro-needle patches and in-situ gel formulations that promise superior lesion control. RSV and CMV programs leverage monoclonal antibodies and small-molecule fusion inhibitors, with pediatric indications offering growth headroom.

The Anti-Viral Therapeutics market shifts from single-pathogen strategies to host-targeted or broad-spectrum agents poised for pandemic readiness. Such programs attract non-dilutive public funding and can bypass narrow epidemiological peaks. CMV assets still address niche transplant populations, leading to premium pricing but limited volumes. Future competitive landscapes will hinge on rapid outbreak response capacity and cross-family efficacy, redrawing the virus-type hierarchy over the forecast horizon.

Reverse transcriptase inhibitors retained a 33.94% Anti-Viral Therapeutics market share in 2024, propelled by backbone status in HIV and hepatitis B therapy. Incremental chemical tweaks improve resistance barriers and renal profiles, sustaining relevance against generic incursion. Capsid inhibitors, fronted by lenacapavir, show a category-leading 3.91% CAGR and are reshaping dose-frequency expectations through twice-yearly administration. Protease inhibitors remain vital in acute COVID-19 management, while polymerase/nucleoside analogs hold cross-viral credibility but seek differentiation via inhalable and pediatric formulations.

RNAi and antisense modalities press into late-phase trials, yet face delivery challenges that temper near-term commercial impact. Broad-spectrum small molecules court government stockpile contracts, providing a hedge against unpredictable outbreaks. Companies with balanced portfolios across these mechanistic classes are best placed to ride out resistance cycles and pricing volatility. Over the next five years, the Anti-Viral Therapeutics market size attached to capsid-based and host-factor inhibitors could double as clinical validation and manufacturing scale converge.

The Anti-Viral Therapeutics Market Report is Segmented by Virus Type (HIV & AIDS, Hepatitis B, Hepatitis C, and More), Drug Class (Reverse Transcriptase Inhibitors, Protease Inhibitors, Polymerase/Nucleoside Analog Inhibitors, and More), Route of Administration (Oral, Injectable, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America represented 34.91% of 2024 sales, buoyed by the FDA's streamlined designations and deep payer wallets that reimburse premium antivirals. US-centric R&D hubs fast-track first-in-class assets, and integrated specialty-pharmacy logistics ensure prompt nationwide distribution. However, Medicare's drug-price negotiations are set to pressure free-on-board prices, nudging firms toward value-based contracts that hinge on real-world virologic outcomes.

Asia-Pacific posts the fastest 4.19% CAGR as China, India, and Southeast Asia invest heavily in domestic pharmaceutical capacity and universal insurance schemes. China's 2024 tally of 228 novel drug approvals signals regulator intent to match Western review speeds, drawing multinationals into local co-development partnerships. India leverages cost-optimized production to supply regional demand, and Japanese aging demographics support sustained antivirals usage for reactivated herpes zoster and RSV. Simultaneously, improving cold-chain frameworks unlock broader biologics access, further expanding the regional Anti-Viral Therapeutics market.

Europe maintains steady value but negotiates harder on price, using health technology assessments to enforce cost-effectiveness thresholds. EMA's centralized procedure remains attractive for simultaneous bloc entry, yet post-Brexit dual filings add complexity. Southern and Eastern European nations, supported by EU healthcare restructuring funds, offer incremental volume upside as vaccine and antiviral awareness climbs. Collectively, geographic diversification spreads revenue risk but raises compliance costs, making global regulatory mastery a core competence for sector leaders.

- Gilead Sciences

- GlaxoSmithKline

- Merck

- Roche

- Abbvie

- Johnson & Johnson

- Bristol-Myers Squibb

- Pfizer

- Novartis

- AstraZeneca

- Cipla

- Dr. Reddy's Laboratories

- Aurobindo Pharma Ltd.

- Lupin

- Sun Pharmaceutical Inds.

- Shionogi & Co., Ltd.

- Takeda Pharmaceutical Co.

- Vir Biotechnology, Inc.

- Regeneron Pharmaceuticals

- Eli Lilly and Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding long-acting injectable pipelines

- 4.2.2 Surge in HIV combination-therapy adoption

- 4.2.3 COVID-19-driven antiviral R&D spill-over

- 4.2.4 AI-enabled nucleos(t)ide analog design

- 4.2.5 Public-sector funding for broad-spectrum agents

- 4.2.6 mRNA platforms pivoting to antivirals

- 4.3 Market Restraints

- 4.3.1 Rising antiviral-resistance mutations

- 4.3.2 Price-control & reimbursement headwinds

- 4.3.3 Biosafety-grade manufacturing bottlenecks

- 4.3.4 Cold-chain gaps in low-income regions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Virus Type

- 5.1.1 HIV & AIDS

- 5.1.2 Hepatitis B

- 5.1.3 Hepatitis C

- 5.1.4 Influenza

- 5.1.5 Herpes (HSV)

- 5.1.6 Respiratory Syncytial Virus (RSV)

- 5.1.7 Cytomegalovirus (CMV)

- 5.1.8 Other & Emerging Viruses

- 5.2 By Drug Class / Mechanism

- 5.2.1 Reverse Transcriptase Inhibitors (NRTI/NNRTI)

- 5.2.2 Protease Inhibitors

- 5.2.3 Polymerase / Nucleoside Analog Inhibitors

- 5.2.4 RNAi & Antisense Therapeutics

- 5.2.5 Broad-spectrum Small-molecule Antivirals

- 5.2.6 Capsid Inhibitors

- 5.2.7 Others

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Injectable (incl. Long-Acting)

- 5.3.3 Topical

- 5.3.4 Others

- 5.4 By Region

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Gilead Sciences Inc.

- 6.3.2 GlaxoSmithKline plc (ViiV Healthcare)

- 6.3.3 Merck & Co., Inc.

- 6.3.4 F. Hoffmann-La Roche AG

- 6.3.5 AbbVie Inc.

- 6.3.6 Johnson & Johnson (Janssen)

- 6.3.7 Bristol Myers Squibb Co.

- 6.3.8 Pfizer Inc.

- 6.3.9 Novartis AG

- 6.3.10 AstraZeneca plc

- 6.3.11 Cipla Ltd.

- 6.3.12 Dr. Reddy's Laboratories

- 6.3.13 Aurobindo Pharma Ltd.

- 6.3.14 Lupin Ltd.

- 6.3.15 Sun Pharmaceutical Inds.

- 6.3.16 Shionogi & Co., Ltd.

- 6.3.17 Takeda Pharmaceutical Co.

- 6.3.18 Vir Biotechnology, Inc.

- 6.3.19 Regeneron Pharmaceuticals

- 6.3.20 Eli Lilly and Company

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment