|

시장보고서

상품코드

1846257

자동차용 전력 모듈 패키징 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Power Module Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

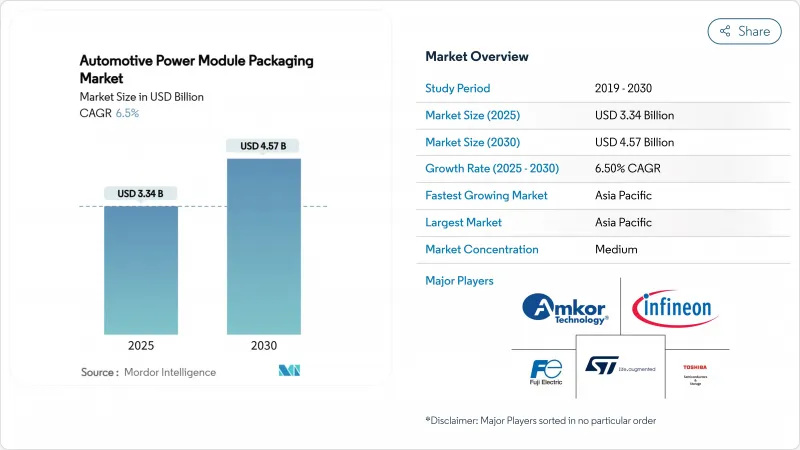

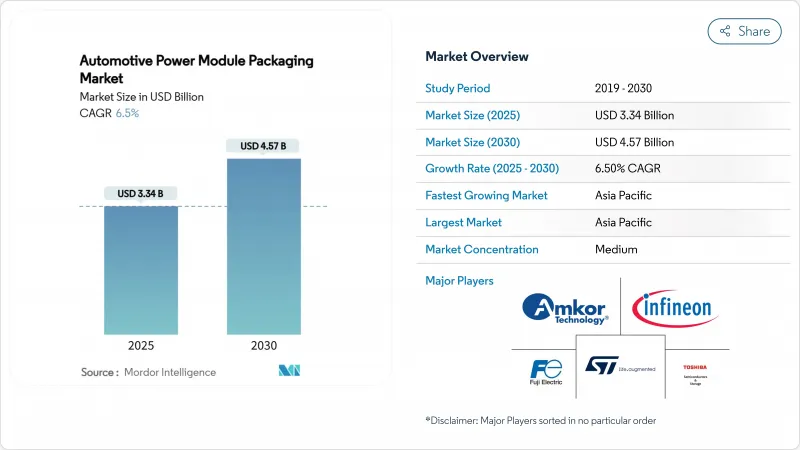

자동차용 전력 모듈 패키징 시장 규모는 2025년에 33억 4,000만 달러에 이르고, 2030년에는 CAGR 6.5%를 나타내 45억 7,000만 달러에 달할 것으로 예상됩니다.

자동차용 전력 모듈 패키징 시장이 확대되고 있는 이유는 자동차 제조업체가 전동화 프로그램을 가속화하고 고전압 아키텍처의 양산을 추진하고 와이드 밴드갭 디바이스에 대한 첨단 열 관리 솔루션을 요구하고 있기 때문입니다. 200mm SiC 웨이퍼 팹 투자 증가, 개발 사이클 단축 파트너십, 배기 가스 규제 강화 등 장기적인 수요를 강화하고 있습니다. 와이어 본드레스 인터커넥트, 양면 냉각, 은 소결을 자랑하는 공급업체는 트랙션 인버터, 자동차 충전기, DC-DC 컨버터 설계로 승리를 거두고 있습니다. 한편, SiC기판공급제약과 세분화된 인정규칙이 여전히 역풍이 되고 있습니다.

세계의 자동차용 전력 모듈 패키징 : 시장 동향 및 인사이트

EV와 HEV의 급속한 생산 확대

2024년 세계 배터리 전기자동차와 하이브리드 자동차의 생산량이 급증하고 자동차 용도는 이미 SiC 수요의 70% 이상을 차지했습니다. Tesla의 Cybertruck 파워 컨버터는 800V 플랫폼이 전압 스트레스를 두 배로 늘리고 열 관리의 필요성을 높이는 방법을 보여줍니다. ZF의 300kW eBeam 액슬을 포함한 상용차 프로그램은 고내구성 패키지의 대응 가능한 기반을 더욱 확장하고 있습니다.

SiC 및 GaN 광대역 갭 디바이스로 이동

4세대 SiC MOSFET은 200℃ 이상의 접합 온도를 유지하며 구리 클립, 은 소결 및 다이의 직접 냉각이 필요합니다. 인피니언은 2025년이 자동차용 GaN, 특히 차량용 충전기와 고주파 DC-DC 컨버터의 전환기가 될 것으로 예측했습니다. SiC 기판공급 병목은 200mm 웨이퍼로의 전환과 생산 능력을 안정화시키는 멀티 소스 계약에 초점을 맞추었습니다.

표준화된 인증 프로토콜 부족

파워 일렉트로닉스 공급업체는 AEC-Q100, AEC-Q101, AEC-Q200이 각 지역의 OEM에 따라 다른 해석을 했기 때문에 테스트 루프의 반복에 직면하여 시장 투입까지의 시간이 장기화되어 경상외 비용이 늘어났습니다. IECQ는 절차의 조화를 도모하기 위해 자동차 자격 인증 프로그램을 시작했지만 채용에 편차가있었습니다.

부문 분석

인텔리전트 전력 모듈은 2024년 매출의 38.1%를 차지했으며, 엔트리 레벨 EV와 하이브리드 차량을 위한 양적 선택이었습니다. SiC 전력 모듈은 비용이 많이 들지만 프리미엄 및 상용 플랫폼이 효율성을 선호했기 때문에 CAGR 예측은 15.4%를 달성했습니다. SiC 디바이스의 자동차용 전력 모듈 패키징 시장 규모는 2030년까지 추가로 7.5%의 점유율을 획득할 것으로 예측되고 있습니다. 로옴과 Valeo의 TRCDRIVE 팩은 SiC가 열적 타협 없이 인버터를 소형화할 수 있음을 보여주었습니다. 한편, GaN은 고주파 스위칭이 전류 제한을 능가하는 자동차 충전기에 침투했습니다. IGBT와 FET 모듈은 중거리 및 보조 부하에 계속 사용되었으며, 최근의 미쓰비시 전기 릴리스에서는 내습성을 향상시키면서 스위칭 손실을 15% 줄였습니다.

자동차용 전력 모듈 패키징 시장에서 OEM 제조업체는 비용, 효율성 및 가용성의 균형을 맞추면서 시장의 다양화가 계속되고 있습니다. 200mm 웨이퍼가 생산 규모에 도달하고 수직 통합 전략이 성숙하면 SiC 비용 저하가 예상됩니다. 따라서 설계 툴, 게이트 드라이버, 열적으로 최적화된 하우징을 번들하는 공급업체는 다년간의 플랫폼 상을 획득하기 위한 포지셔닝을 하고 있습니다. 고객이 턴키 모듈 서브시스템을 요구함에 따라, 집적 디바이스 제조업체와 조립 전문 기업 간의 경쟁 홈은 좁아질 것으로 보입니다.

2024년 점유율은 기존 400V 승용차 플랫폼을 중심으로 600V까지의 시스템이 44.3%를 유지했습니다. 그러나 601-1200V 대역은 급속 충전 시간을 단축하는 800V 토폴로지로의 변화를 반영하여 CAGR6.9%와 자동차용 전력 모듈 패키징 시장에서 가장 급속히 상승하고 있습니다. Aptiv는 견고한 패키징의 가치를 높이는 절연 문제와 연면 요구 사항을 설명했습니다. 1200V 이상의 모듈은 여전히 틈새 시장이며 헤비 듀티 및 인프라 역할을 목표로 합니다.

높은 전압 요구는 더 두꺼운 절연 젤, 낮은 인덕턴스 구리 클립 및 1.5kV 이상의 정격 프레스 피트 핀 개발을 강화했습니다. 인피니언 1200V CoolSiC MOSFET은 800V DC-DC 컨버터용으로 Forvia Hella에 채택되어 플랫폼 변화를 강조합니다. OEM이 차세대 고전압 도메인 컨트롤러를 표준화함에 따라 부분 방전 내구성과 현장 고장 분석을 보장하는 패키징 공급업체가 사양을 이길 것으로 보입니다.

자동차용 전력 모듈 패키징 시장은 모듈형(IPM, Sic 전력 모듈, Gan 전력 모듈, 기타), 전력 정격(최대 600V, 601-1200V, 기타), 패키징 기술(와이어 본드, 와이어 본드리스/파워 오버 레이, 기타), 추진력 유형(BEV, HEV, PHEV, FCEV), 차량 유형(승용차, 기타), 용도(트랙션 인버터, 온보드 충전기, DC-DC 컨버터, 보조/크라이메이트/EPS), 지역별로 구분됩니다.

지역 분석

아시아태평양은 2024년에 57.2%의 점유율을 유지했으며, 2030년까지 연평균 복합 성장률(CAGR)은 8.9%를 나타낼 전망입니다. 중국의 듀얼 크레딧 규칙과 규모의 우위성이 지역 생산 능력 회복력에 대응한 말레이시아 인피네온의 20억 달러의 200mm 팹을 포함한 주요 SiC 투자를 끌어들였습니다. 기판, 금속화 페이스트, 성형 컴파운드에 이르는 현지 공급망은 리드 타임을 단축하고 비용을 절감했습니다.

onsemi는 체코 공화국에 엔드 투 엔드 SiC 라인을 건설하기 위해 20억 달러를 투자하여 웨이퍼에서 모듈까지의 관리를 보장하고 수입 의존도를 낮추었습니다. 연방 정부의 제조세 공제도 미국 내 모듈 조립을 촉진했습니다.

유럽에서는 프리미엄 EV 브랜드와 엄격한 배기가스 규제에 중점을 두었습니다. 비테스코 테크놀로지스는 5억 7,600만 유로(6억 5,000만 달러)를 투자하여 오스트라바에서 첨단 전자 생산을 확대하여 지역의 전기화 기세에 자신감을 보였습니다. 지역 분산 이니셔티브가 통합되어 단일 지역의 위험을 줄이고 세계 품질 기준을 높이는 기술 이전을 촉진하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- EV와 HEV의 급속한 생산 확대

- SiC 및 GaN 와이드 밴드갭 디바이스로의 변화

- 보다 높은 전력 밀도의 모듈을 요구하는 자동차의 전동화

- 세계의 엄격한 배기가스 규제

- 와이어 본드레스/톱 사이드 냉각 패키지의 OEM 채용

- 전력 모듈을 통합한 셀 투 팩 아키텍처

- 시장 성장 억제요인

- 표준화된 인증 프로토콜의 부족

- SiC/GaN 기판의 고비용과 공급 제약

- 신흥의 800V 플랫폼에 있어서 열 관리의 한계

- SiC 공급 체인공급 능력 과잉 가능성

- 거시경제 요인의 영향

- 밸류체인 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 모듈 유형별

- 지능형 전력 모듈(IPM)

- SiC 전력 모듈

- GaN 전력 모듈

- IGBT 모듈

- FET 모듈

- 정격 전력

- 600V 이하

- 601-1200V

- 1200V 이상

- 패키징 기술별

- 와이어 본드

- 와이어 본드/파워 오버레이

- 프레스 피트/다이 다이렉트 프레스

- PCB 임베디드

- 추진 유형별

- 배터리 전기자동차(BEV)

- 하이브리드 자동차(HEV)

- 플러그인 하이브리드(PHEV)

- 연료전지 전기자동차(FCEV)

- 차량 유형별

- 승용차

- 소형 상용차

- 대형 상용차 및 버스

- 용도별

- 트랙션 인버터

- 차재 충전기

- DC-DC 컨버터

- 보조/공조/EPS

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 기타 남미

- 유럽

- 독일

- 프랑스

- 영국

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- Amkor Technology, Inc.

- Kulicke & Soffa Industries, Inc.

- Powertech Technology Inc.(PTI)

- Infineon Technologies AG

- STMicroelectronics NV

- Fuji Electric Co., Ltd.

- Toshiba Electronic Devices & Storage Corporation

- SEMIKRON Danfoss GmbH & Co. KG

- JCET Group Co., Ltd.

- StarPower Semiconductor Ltd.

- Mitsubishi Electric Corporation

- ROHM Co., Ltd.

- onsemi Corporation

- Nexperia BV

- Wolfspeed, Inc.

- Microchip Technology Inc.

- Littelfuse, Inc.(IXYS)

- Vitesco Technologies Group AG

- Vincotech GmbH

- CISSOID SA

- Hitachi Astemo, Ltd.

- Danfoss Silicon Power GmbH

- BYD Semiconductor Co., Ltd.

- Dynex Semiconductor Ltd.

- Shenzhen BASiC Semiconductor Ltd.

제7장 시장 기회와 전망

KTH 25.11.10The automotive power module packaging market size reached USD 3.34 billion in 2025 and is forecast to climb to USD 4.57 billion by 2030, reflecting a compound annual growth rate (CAGR) of 6.5%.

The automotive power module packaging market is expanding because automakers accelerated electrification programs, pushed higher voltage architectures into volume production, and demanded advanced thermal-management solutions for wide-bandgap devices. Rising investments in 200 mm SiC wafer fabs, partnerships that compress development cycles, and tighter emission standards collectively reinforce long-term demand. Suppliers that master wire-bondless interconnects, double-sided cooling, and silver sintering are securing design wins in traction inverters, on-board chargers, and DC-DC converters. Meanwhile, supply constraints for SiC substrates and fragmented qualification rules remain headwinds.

Global Automotive Power Module Packaging Market Trends and Insights

Rapid EV and HEV production growth

Global battery-electric and hybrid output climbed sharply in 2024, and automotive applications already accounted for more than 70% of SiC demand. Tesla's Cybertruck power converter illustrated how 800 V platforms double voltage stresses and intensify thermal management needs. Tier-1 suppliers such as BorgWarner reported 47% year-on-year eProduct sales growth, signaling that established drivetrain specialists are pivoting resources toward high-density modules.Commercial vehicle programs, including ZF's 300 kW eBeam axle, further widen the addressable base for ruggedized packaging.

Shift toward SiC and GaN wide-bandgap devices

Fourth-generation SiC MOSFETs now sustain junction temperatures above 200 °C, intensifying the need for copper clips, silver sintering, and direct die cooling. Infineon forecasts 2025 as an inflection year for automotive GaN, especially in on-board chargers and high-frequency DC-DC converters. Supply bottlenecks for SiC substrates sharpened focus on 200 mm wafer transitions and on multi-source agreements that stabilize capacity.

Lack of standardized qualification protocols

Power-electronics suppliers faced repeated test loops because AEC-Q100, AEC-Q101, and AEC-Q200 were interpreted differently by regional OEMs, prolonging time-to-market and inflating non-recurring expenses. IECQ launched its Automotive Qualification Programme to harmonize procedures, yet adoption remained uneven.

Other drivers and restraints analyzed in the detailed report include:

- Vehicle electrification demands higher power-density modules

- Stringent global emission regulations

- High cost and supply constraints of SiC/GaN substrates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Intelligent Power Modules held 38.1% of 2024 revenue and remained the volume choice for entry-level EVs and hybrids. SiC Power Modules, though costlier, achieved 15.4% CAGR forecasts as premium and commercial platforms prioritized efficiency. The automotive power module packaging market size for SiC devices is projected to capture an additional 7.5 percentage-point share by 2030. ROHM and Valeo's TRCDRIVE pack showed how SiC enables inverter downsizing without thermal compromise. Meanwhile, GaN penetrated on-board chargers where high-frequency switching outweighed current limits. IGBT and FET modules continue to serve mid-range and auxiliary loads, and recent Mitsubishi Electric releases reduced switching losses by 15% while extending moisture tolerance.

Market diversification persisted across the automotive power module packaging market as OEMs balanced cost, efficiency, and availability. SiC cost declines are expected once 200 mm wafers reach scale and vertical-integration strategies mature. Hence, suppliers that bundle design tools, gate drivers, and thermally optimized housings are positioning themselves to capture multi-year platform awards. The competitive split between integrated device makers and specialized assembly firms is likely to narrow as customers demand turnkey module sub-systems.

Systems up to 600 V retained a 44.3% share in 2024, anchored by existing 400 V passenger-car platforms. However, the 601-1200 V band is the automotive power module packaging market's fastest climber at 6.9% CAGR, mirroring the shift to 800 V topologies that cut fast-charging times. Aptiv outlined insulation challenges and creepage requirements that raise the value of robust packaging. Above-1200V modules remain niche, targeting heavy-duty and infrastructure roles.

Higher voltage demands intensified the development of thicker insulation gels, copper clips with lower inductance, and press-fit pins rated beyond 1.5 kV. Infineon's 1200 V CoolSiC MOSFETs were selected by Forvia Hella for 800 V DC-DC converters, underscoring the platform shift. Packaging suppliers that guarantee partial discharge endurance and field-failure analytics will win specifications as OEMs standardize on next-generation high-voltage domain controllers.

Automotive Power Module Packaging Market is Segmented by Module Type (IPM, Sic Power Module, Gan Power Module, and More), Power Rating (Up To 600V, 601-1200V, and More), Packaging Technology (Wire-Bond, Wire-bondless/Power Overlay, and More), Propulsion Type (BEV, HEV, PHEV, and FCEV), Vehicle Type (Passenger Cars, and More), Application (Traction Inverter, On-Board Charger, DC-DC Converter, Auxiliary/Climate/EPS), and Geography.

Geography Analysis

Asia-Pacific retained a 57.2% share in 2024 and posted the highest outlook at 8.9% CAGR to 2030. China's dual-credit rules and scale advantages drew major SiC investments, including Infineon's USD 2 billion 200 mm fab in Malaysia that addressed regional capacity resilience. Local supply chains spanning substrates, metallization pastes, and molding compounds shortened lead times and trimmed costs.

North American demand accelerated as domestic OEMs unveiled new 800 V pickups and SUVs. onsemi committed USD 2 billion to build an end-to-end SiC line in the Czech Republic, ensuring wafer-to-module control and reducing import dependency. Federal manufacturing tax credits also encouraged module assembly within the United States.

Europe focused on premium EV brands and strict emissions mandates. Vitesco Technologies invested EUR 576 million (USD 650 million) to expand advanced-electronics production in Ostrava, signaling confidence in regional electrification momentum. Collectively, regional diversification initiatives are diluting single-region risk and fostering technology transfers that elevate global quality benchmarks.

- Amkor Technology, Inc.

- Kulicke & Soffa Industries, Inc.

- Powertech Technology Inc. (PTI)

- Infineon Technologies AG

- STMicroelectronics N.V.

- Fuji Electric Co., Ltd.

- Toshiba Electronic Devices & Storage Corporation

- SEMIKRON Danfoss GmbH & Co. KG

- JCET Group Co., Ltd.

- StarPower Semiconductor Ltd.

- Mitsubishi Electric Corporation

- ROHM Co., Ltd.

- onsemi Corporation

- Nexperia B.V.

- Wolfspeed, Inc.

- Microchip Technology Inc.

- Littelfuse, Inc. (IXYS)

- Vitesco Technologies Group AG

- Vincotech GmbH

- CISSOID SA

- Hitachi Astemo, Ltd.

- Danfoss Silicon Power GmbH

- BYD Semiconductor Co., Ltd.

- Dynex Semiconductor Ltd.

- Shenzhen BASiC Semiconductor Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid EV and HEV production growth

- 4.2.2 Shift toward SiC and GaN wide-bandgap devices

- 4.2.3 Vehicle electrification demanding higher power-density modules

- 4.2.4 Stringent global emission regulations

- 4.2.5 OEM adoption of wire-bondless / top-side-cooling packages

- 4.2.6 Cell-to-pack architectures integrating power modules

- 4.3 Market Restraints

- 4.3.1 Lack of standardized qualification protocols

- 4.3.2 High cost and supply constraints of SiC / GaN substrates

- 4.3.3 Thermal-management limits in emerging 800 V platforms

- 4.3.4 Potential SiC supply-chain over-capacity

- 4.4 Impact of Macroeconomic Factors

- 4.5 Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Module Type

- 5.1.1 Intelligent Power Module (IPM)

- 5.1.2 SiC Power Module

- 5.1.3 GaN Power Module

- 5.1.4 IGBT Module

- 5.1.5 FET Module

- 5.2 By Power Rating

- 5.2.1 Up to 600 V

- 5.2.2 601 - 1200 V

- 5.2.3 Above 1200 V

- 5.3 By Packaging Technology

- 5.3.1 Wire-bond

- 5.3.2 Wire-bondless / Power Overlay

- 5.3.3 Press-fit / Direct Pressed-Die

- 5.3.4 PCB-embedded

- 5.4 By Propulsion Type

- 5.4.1 Battery-Electric Vehicle (BEV)

- 5.4.2 Hybrid Electric Vehicle (HEV)

- 5.4.3 Plug-in Hybrid (PHEV)

- 5.4.4 Fuel-Cell Electric Vehicle (FCEV)

- 5.5 By Vehicle Type

- 5.5.1 Passenger Cars

- 5.5.2 Light Commercial Vehicles

- 5.5.3 Heavy Commercial Vehicles and Buses

- 5.6 By Application

- 5.6.1 Traction Inverter

- 5.6.2 On-board Charger

- 5.6.3 DC-DC Converter

- 5.6.4 Auxiliary / Climate / EPS

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 France

- 5.7.3.3 United Kingdom

- 5.7.3.4 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Saudi Arabia

- 5.7.5.1.2 United Arab Emirates

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amkor Technology, Inc.

- 6.4.2 Kulicke & Soffa Industries, Inc.

- 6.4.3 Powertech Technology Inc. (PTI)

- 6.4.4 Infineon Technologies AG

- 6.4.5 STMicroelectronics N.V.

- 6.4.6 Fuji Electric Co., Ltd.

- 6.4.7 Toshiba Electronic Devices & Storage Corporation

- 6.4.8 SEMIKRON Danfoss GmbH & Co. KG

- 6.4.9 JCET Group Co., Ltd.

- 6.4.10 StarPower Semiconductor Ltd.

- 6.4.11 Mitsubishi Electric Corporation

- 6.4.12 ROHM Co., Ltd.

- 6.4.13 onsemi Corporation

- 6.4.14 Nexperia B.V.

- 6.4.15 Wolfspeed, Inc.

- 6.4.16 Microchip Technology Inc.

- 6.4.17 Littelfuse, Inc. (IXYS)

- 6.4.18 Vitesco Technologies Group AG

- 6.4.19 Vincotech GmbH

- 6.4.20 CISSOID SA

- 6.4.21 Hitachi Astemo, Ltd.

- 6.4.22 Danfoss Silicon Power GmbH

- 6.4.23 BYD Semiconductor Co., Ltd.

- 6.4.24 Dynex Semiconductor Ltd.

- 6.4.25 Shenzhen BASiC Semiconductor Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment