|

시장보고서

상품코드

1848043

이비인후과 기기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)ENT Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

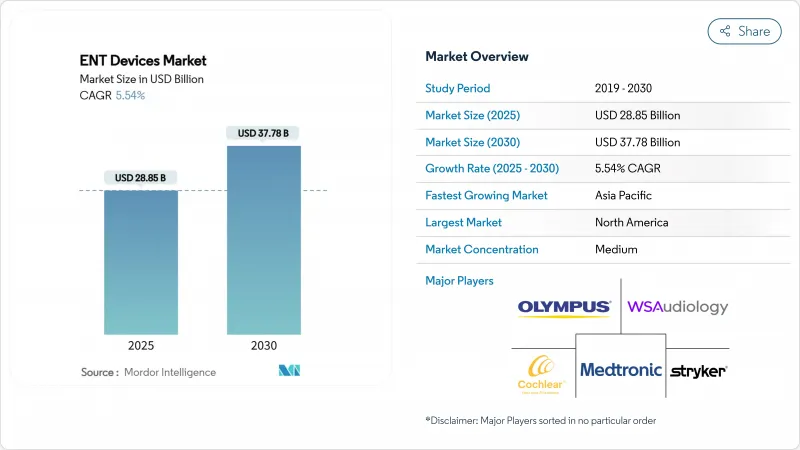

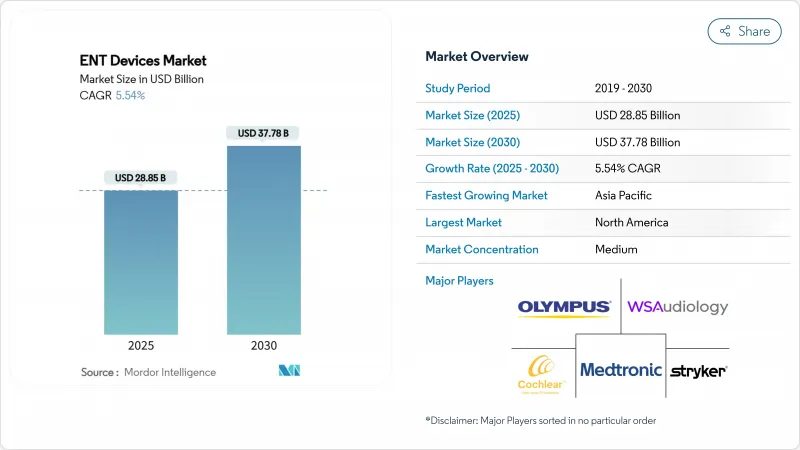

이비인후과 기기 시장 규모는 2025년에 288억 5,000만 달러로 평가되었고, CAGR은 5.54%를 나타낼 것으로 예측되며 2030년에 377억 8,000만 달러로 성장할 전망입니다.

왕성한 수요는 노화 관련 청각 및 비부비동 질환 환자층 확대, 병원 및 외래센터 전반의 안정적인 시술량, 일상적인 이비인후과 기기에 인공지능의 급속한 도입에서 비롯됩니다. 실제 청취 환경에 맞춰 조정되는 AI 지원 보청기, 조직 미세구조를 드러내는 하이퍼스펙트럼 내시경, 수술 후 회복을 가속화하는 풍선 비강 확장 키트는 종합적으로 임상적 기대를 높이고 교체 구매를 촉진합니다. 원격 프로그래밍이 가능한 스마트폰 연동 장비로 대표되는 가정 기반 치료의 병행적 발전은 환자 접근성을 확대하고 이비인후과 기기 시장 내 반복적 수익 모델을 지원합니다. 아시아태평양 지역의 인프라 확충, 일반의약품 보청기를 포함하는 북미의 보험 적용 범위 확대, 수술실 시간을 단축하는 수술 중심 혁신 기술이 물량 증가를 더욱 공고히 합니다.

세계의 이비인후과 기기 시장 동향 및 인사이트

이비인후과 질환의 유병률 상승

고령화 인구와 악화되는 도시 대기질로 인해 만성 비부비동염, 중이염, 감각신경성 난청의 발생률이 증가하고 있습니다. 병원 기록에 따르면 대도시 클리닉에서는 조기 진료를 받는 반면, 농촌 지역 환자들은 여전히 진행된 병변으로 내원하여 더 침습적인 치료가 필요한 경우가 많습니다. 이 같은 역학은 이비인후과 기기 시장 전반에 걸쳐 영상 내시경, 풍선 확장 키트, 프로그래밍 가능 보청기에 대한 기본 수요를 유지합니다. 따라서 공중보건 기관들은 조기 검진을 최우선 과제로 삼고 있으며, 이는 진단 장비 도입을 촉진하고 소모품의 후속 판매를 자극합니다.

이비인후과 기기의 기술 발전

디지털 신호 처리기, 좁은 빔 마이크, 4D 모션 센서가 이제 프리미엄 보청기에 내장되어 실시간 환경 분류 및 소음 억제를 가능하게 하여 음성 인식 능력을 향상시킵니다. 수술실에서는 하이퍼스펙트럼 영상 촬영이 가능한 경성 내시경이 혈류 공급된 점막과 악성 종양을 구분하여 절제 경계를 개선하고 출혈을 제한합니다. 이러한 혁신은 이비인후과 기기 시장을 기술 주도형 분야로 공고히 합니다. 제조사들은 소프트웨어 업데이트, 클라우드 기반 피팅 포털, 기존 수술 장비에 장착 가능한 모듈형 부품 등을 통해 차별화를 꾀합니다.

고비용 장비

완전 이식형 인공와우 시스템은 종종 25,000달러 이상으로 책정되어 보험 미가입 성인 다수에게 부담스러운 금액입니다. 국가 건강보험 제도가 있는 국가에서도 보험급여 상한선이 물가 상승률을 따라가지 못해 대기 목록이 지속됩니다. 결과적으로 임상적 적격 환자 중 극소수만 이식 수술을 받으며, 이는 이비인후과 기기 시장 내 규모 확장을 저해합니다. 능동형 중이 장비를 보철물로 재분류하려는 입법 제안은 메디케어 자금 지원을 확보하고 점진적으로 접근성 격차를 좁힐 수 있습니다.

부문 분석

보청기 부문은 2024년 매출의 32%를 차지하며 이비인후과 기기 시장 규모에서 가장 큰 비중을 차지했습니다. 클라우드 연동 펌웨어 업데이트, 리튬이온 충전식 배터리, AI 기반 장면 인식 기술로 교체 주기가 약 4년으로 유지되어 꾸준한 수요를 뒷받침합니다. 프리미엄 등급에서는 통합 건강 센서가 심장 리듬과 걸음 수를 추적하여 증폭 기능 이상의 가치를 제공합니다. 소비자 가전 업체들이 스마트폰 옆에 자가 장착형 모델을 배치하는 전략도 판매에 기여하는데, 이는 병원 맞춤 프리미엄 라인을 잠식하지 않으면서 유통 채널 노출을 확대하는 접근법입니다.

이식형 장비는 시장 규모는 작았으나 9.2%의 연평균 성장률 전망으로 가장 높은 성장 모멘텀을 보였다. 완전 이식형 인공와우 시스템 같은 혁신은 외부 프로세서를 제거해 미적 매력과 수영 편의성을 높입니다. 외과의들은 인공와우 손상을 줄이고 프로그래밍 시간을 단축하는 자기 유도 전극 배열을 선호합니다. 장기적 치료 성과가 우수해 보험사 수용도가 높아지면서 이비인후과 기기 시장의 다년간 성장이 촉진되고 있습니다. 진단 장비는 여전히 상당한 점유율을 유지하며, 휴대용 광간섭단층촬영(OCT) 이경은 이제 일차 진료 현장에서 중이 삼출액을 확인할 수 있어 조기 개입이 확대되고 있습니다. 수술 장비 도입은 최소 침습적 추세를 따르며, 특히 신속한 회전을 원하는 외래 센터에서 널리 사용되는 풍선 부비동 키트가 대표적입니다.

지역 분석

북미는 2024년 38%의 매출 점유율로 이비인후과 기기 시장을 주도했습니다. 광범위한 보험 적용 범위, 노련한 원격 청각학 네트워크, 활기찬 연구 생태계가 도입 주기를 가속화하고 있습니다. 보청기 소프트웨어가 탑재된 소비자용 이어버드의 FDA 승인은 규제 유연성을 강조하며, 소매업체들이 청각학 관련 제품 진열대를 확장할 수 있는 발판을 마련해 줍니다. 병원 그룹들은 스펙트럼 이미징 내시경 및 재수술 준비형 임플란트 제품군에 투자하여 의뢰 환자 유입을 유지함으로써 지역 지출 모멘텀을 강화하고 있습니다.

유럽은 여전히 주요 기여 지역입니다. 공공 지불 시스템이 대부분의 임플란트 비용을 보상하지만, 엄격한 증거 요건으로 인해 신기술의 초기 도입이 지연되고 있습니다. 지역 제조업체들은 환경 지침에 부합하기 위해 소형화와 친환경 포장을 강조하고 있습니다. 국경을 초월한 임상 컨소시엄은 데이터를 공유하여 수술 지침을 개선하고, 이비인후과 기기 시장을 통해 전 세계적으로 확산되는 장비 재설계에 정보를 제공합니다.

아시아태평양 지역은 7.2%의 연평균 성장률(CAGR) 전망으로 가장 빠르게 성장하는 시장입니다. 중국에서는 정부 지원 보험이 이제 골전도 보청기 솔루션을 보장하며, 인도의 아유슈만 바라트 프로그램은 지역 병원에서 부비동 수술을 지원합니다. 국내 공급업체들은 내구성과 경제성을 균형 있게 갖춘 중급 제품군을 확대해 도시-농촌 간 접근 격차를 좁히고 있습니다. 한국과 싱가포르의 스타트업들은 로봇 기술을 활용해 좁은 비강 내부를 탐색하며 라이선싱 계약을 통해 지적재산을 수출하고 있습니다. 중동 및 아프리카는 점진적으로 발전 중이지만, 걸프 국가들의 교육 병원 체계를 통해 첨단 장비 도입과 지역 외과의사 양성의 혜택을 받고 있습니다. 남미는 브라질이 이비인후과 센터를 현대화하는 반면 인접국들은 자금 제약에 직면하는 등 진전이 혼재된 양상입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 이비인후과 질환의 유병률 상승

- 이비인후과 기기의 기술 발전

- 최소 침습 수술의 채택 증가

- 인식 제고 캠페인 및 건강 프로그램 확대

- 원격의료 채택 증가

- 시장 성장 억제요인

- 장비의 고비용

- 장비 살균 및 유지보수 문제

- 신흥 시장에서 보청기 사용에 대한 사회적 낙인

- 공급망 분석

- 기술적 전망

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측

- 제품별

- 진단 장비

- 내시경(경성, 연성)

- 청력검사장비(OAE, 팀파노메트리)

- 외과 수술용 장비

- 전동 수술 기구

- 풍선 부비강 확장 시스템

- CO 레이저 & 다이오드 레이저

- 이비인후과 용품 및 소모품(스텐트, 이어 튜브)

- 보청기

- BTE

- ITE/ITC

- RIC

- OTC 보청기

- 이식형 보청기

- 인공 내이

- 뼈 보청기(BAHA)

- 영상 유도 수술 네비게이션 시스템

- 기타 제품

- 진단 장비

- 연령층별

- 소아(0-17세)

- 성인(18-64세)

- 고령자(65세 이상)

- 최종 사용자별

- 병원

- 이비인후과 클리닉

- 외래수술센터(ASC)

- 재택치료

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Cochlear Ltd.

- Sonova Holding AG

- Demant A/S

- GN Store Nord A/S

- WS Audiology

- Medtronic PLC

- Stryker Corporation

- Smith Nephew PLC

- Olympus Corporation

- Fujifilm Holdings Corp.

- Starkey Laboratories Inc.

- Coloplast(Atos Medical AB)

- InHealth Technologies

- Richard Wolf GmbH

- Nurotron Biotechnology Co. Ltd.

- Baxter International(Hill-Rom)

- Acclarent Inc.(J&J)

- Boston Scientific Corp.

- Smiths Medical

제7장 시장 기회와 전망

HBR 25.11.10The ENT devices market size reached USD 28.85 billion in 2025 and is forecast to climb to USD 37.78 billion by 2030, reflecting a 5.54% CAGR.

Robust demand stems from the expanding pool of age-related auditory and sinonasal disorders, steady procedure volumes across hospitals and ambulatory centers, and the rapid infusion of artificial intelligence into routine ENT tools. AI-enabled hearing aids that adjust to real-world listening environments, hyperspectral endoscopes that reveal tissue microstructures, and balloon sinus dilation kits that speed post-operative recovery collectively raise clinical expectations and spur replacement purchases. Parallel gains in home-based care, exemplified by smartphone-linked devices that permit remote programming, widen patient access and support recurring revenue models inside the ENT devices market. Volume growth is further anchored by Asia-Pacific's infrastructure build-out, North America's reimbursements that now cover over-the-counter aids, and surgically focused innovations that shorten operating-room time.

Global ENT Devices Market Trends and Insights

Rising Prevalence of ENT Disorders

Aging populations and deteriorating urban air quality have raised the incidence of chronic rhinosinusitis, otitis media, and sensorineural hearing loss. Hospital registries confirm earlier presentation in metropolitan clinics, while rural patients still arrive with advanced pathologies that often require more invasive interventions. Across the ENT devices market, this epidemiology sustains baseline demand for imaging scopes, balloon dilation kits, and programmable hearing aids. Public health agencies therefore prioritize early screening, which in turn elevates diagnostic instrument placements and stimulates follow-on sales of consumables.

Technological Advancements in ENT Devices

Digital signal processors, narrow-beam microphones, and 4D motion sensors now embed inside premium hearing aids, allowing real-time environmental classification and noise suppression that improve speech recognition. In operating theaters, rigid endoscopes capable of hyperspectral imaging distinguish perfused mucosa from malignancies, enhancing resection margins while limiting bleeding. These breakthroughs reinforce the ENT devices market as a technology-driven arena: manufacturers differentiate through software updates, cloud-based fitting portals, and module-ready components that clip into existing surgical stacks.

High Cost of Devices

Fully implanted cochlear systems often list above USD 25,000, a figure beyond the reach of many uninsured adults. Even in countries with national health plans, wait lists persist when reimbursement caps lag inflation. Consequently, only a fraction of clinically eligible patients receive implants, dampening volume expansion inside the ENT devices market. Legislative proposals to reclassify active middle-ear devices as prosthetics aim to unlock Medicare funding and could gradually narrow affordability gaps.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Minimally Invasive Procedures

- Rising Awareness Campaigns and Health Programs

- Device Sterilization and Maintenance Challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The hearing-aid segment generated the largest slice of the ENT devices market size with 32% revenue in 2024. Cloud-linked firmware updates, lithium-ion rechargeable batteries, and AI-guided scene detection keep replacement cycles near four years, supporting steady unit demand. At the premium tier, integrated health sensors track cardiac rhythm and step counts, expanding device value beyond amplification. Sales also benefit from consumer electronics entrants who position self-fit models next to smartphones, an approach that widens channel exposure without cannibalizing clinic-fitted premium lines.

Implantable devices accounted for a smaller base yet posted the highest forward momentum with a 9.2% CAGR outlook. Innovations such as totally implanted cochlear systems remove external processors, boosting cosmetic appeal and swimming convenience. Surgeons appreciate magnet-guided electrode arrays that reduce cochlear trauma and shorten programming sessions. Favorable long-term outcomes foster payer acceptance, propelling multi-year growth inside the ENT devices market. Diagnostic instruments retain significant share; portable optical-coherence-tomography otoscopes now reveal middle-ear effusions at primary-care desks, broadening early intervention. Surgical device uptake follows the minimally invasive trend, especially balloon sinus kits that occupy ambulatory centers seeking rapid turnover.

The ENT Devices Market Report is Segmented by Product (Diagnostic Devices, Surgical Devices, Hearing Aids, Implantable Devices, Image-Guided Surgery Navigation Systems, and More), Age Group (Pediatric, Adult, and Geriatric), End User (Hospitals, ENT Clinics, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the ENT devices market with 38% revenue share in 2024. Extensive insurance coverage, veteran tele-audiology networks, and a vibrant research ecosystem accelerate adoption cycles. FDA authorization of consumer earbuds equipped with hearing-aid software underscores regulatory agility and primes retailers for expanded audiology aisles. Hospital groups invest in spectral-imaging endoscopes and revision-ready implant suites to retain referral flows, reinforcing regional spending momentum.

Europe remains a substantive contributor. Public payer systems reimburse most implant costs, though stringent evidence requirements slow initial roll-outs of novel technologies. Regional manufacturers emphasize miniaturization and eco-friendly packaging to align with environmental directives. Cross-border clinical consortia pool data, refining surgical guidelines and informing device redesigns that travel globally through the ENT devices market.

Asia-Pacific represents the fastest-growing arena with a 7.2% CAGR outlook. Government-backed insurance in China now covers bone-anchored hearing solutions, while India's Ayushman Bharat program subsidizes sinus surgeries at district hospitals. Domestic suppliers scale mid-tier offerings that balance durability with affordability, narrowing urban-rural access gaps. Start-ups in Korea and Singapore leverage robotics to navigate narrow nasal cavities, exporting intellectual property through licensing deals. Middle East and Africa move gradually yet benefit from teaching-hospital frameworks in Gulf states that import advanced suites and train regional surgeons. South America shows mixed progress as Brazil modernizes otology centers while neighboring countries grapple with funding constraints.

- Cochlear

- Sonova

- Demant

- GN Store Nord

- WS Audiology

- Medtronic

- Stryker

- Smith+Nephew PLC

- Olympus

- Fujifilm Holdings Corp.

- Starkey Laboratories

- Coloplast (Atos Medical AB)

- InHealth Technologies

- Richard Wolf

- Nurotron Biotechnology

- Baxter International (Hill-Rom)

- Acclarent Inc. (J&J)

- Boston Scientific

- Smiths Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of ENT Disorders

- 4.2.2 Technological Advancements in the ENT Devices

- 4.2.3 Rising Adoption of Minimally Invasive Procedures

- 4.2.4 Rising Awareness Campaigns and Health Programs

- 4.2.5 Rising Adoption of Telemedicine

- 4.3 Market Restraints

- 4.3.1 High Cost of Devices

- 4.3.2 Device Sterilization and Maintenance Challenges

- 4.3.3 Social Stigma Around Hearing-Aid Use in Emerging Markets

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Diagnostic Devices

- 5.1.1.1 Endoscopes (Rigid, Flexible)

- 5.1.1.2 Hearing Screening Devices (OAE, Tympanometry)

- 5.1.2 Surgical Devices

- 5.1.2.1 Powered Surgical Instruments

- 5.1.2.2 Balloon Sinus Dilation Systems

- 5.1.2.3 CO? & Diode Lasers

- 5.1.2.4 ENT Supplies & Consumables (Stents, Ear Tubes)

- 5.1.3 Hearing Aids

- 5.1.3.1 Behind-the-Ear (BTE)

- 5.1.3.2 In-the-Ear / In-the-Canal (ITE/ITC)

- 5.1.3.3 Receiver-in-Canal (RIC)

- 5.1.3.4 Over-the-Counter (OTC) Hearing Aids

- 5.1.4 Implantable Devices

- 5.1.4.1 Cochlear Implants

- 5.1.4.2 Bone-Anchored Hearing Aids (BAHA)

- 5.1.5 Image-Guided Surgery Navigation Systems

- 5.1.6 Other Products

- 5.1.1 Diagnostic Devices

- 5.2 By Age Group

- 5.2.1 Pediatric (0-17 Years)

- 5.2.2 Adult (18-64 Years)

- 5.2.3 Geriatric (65+ Years)

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 ENT Clinics

- 5.3.3 Ambulatory Surgical Centers (ASCs)

- 5.3.4 Home-care

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Cochlear Ltd.

- 6.3.2 Sonova Holding AG

- 6.3.3 Demant A/S

- 6.3.4 GN Store Nord A/S

- 6.3.5 WS Audiology

- 6.3.6 Medtronic PLC

- 6.3.7 Stryker Corporation

- 6.3.8 Smith+Nephew PLC

- 6.3.9 Olympus Corporation

- 6.3.10 Fujifilm Holdings Corp.

- 6.3.11 Starkey Laboratories Inc.

- 6.3.12 Coloplast (Atos Medical AB)

- 6.3.13 InHealth Technologies

- 6.3.14 Richard Wolf GmbH

- 6.3.15 Nurotron Biotechnology Co. Ltd.

- 6.3.16 Baxter International (Hill-Rom)

- 6.3.17 Acclarent Inc. (J&J)

- 6.3.18 Boston Scientific Corp.

- 6.3.19 Smiths Medical

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment