|

시장보고서

상품코드

1848050

스페인의 체외(In-vitro) 진단 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Spain In-vitro Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

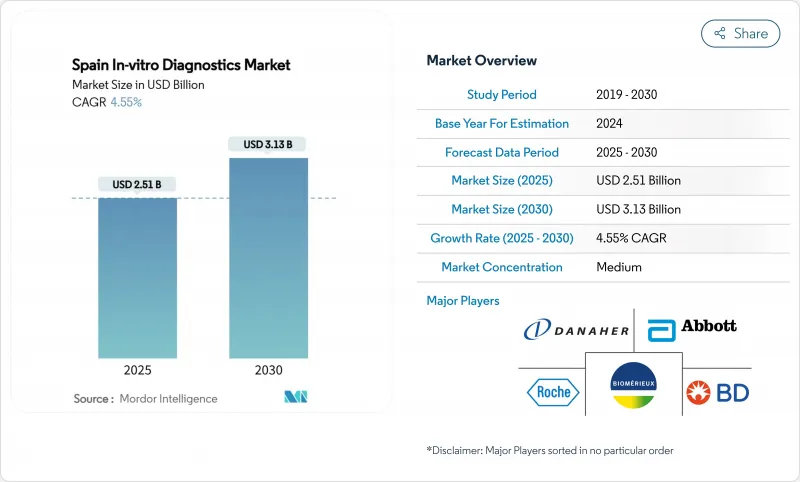

스페인의 체외(In-vitro) 진단 시장 규모는 2025년에 25억 1,000만 달러로 평가되었고, 2030년에 31억 3,000만 달러에 이를 것으로 예측되며, CAGR은 4.55%를 나타낼 전망입니다.

지속적인 성장 동력은 고령화 인구, 만성질환 발생률 증가, 그리고 국가 차원의 EU 체외진단규정(IVDR) 완전 이행에 기인합니다. 빈번한 신장·당뇨·고혈압 검진 수요가 검사량을 끌어올리는 가운데, 마드리드와 카탈루냐의 병원 그룹들은 AI 기반 분석기로 실험실을 현대화하며 검사 소요 시간을 단축하고 있습니다. 분자 검사 혁신 기업들은 유럽투자은행(EIB)의 자금 지원을 받고 있으며, 스페인의 디지털 헬스 전략은 IVDR 추적성 규정을 충족하는 연결형 기기에 예산을 집중시키고 있습니다. 동시에 17개 자치지역에 걸친 분산형 조달 체계는 공급업체들이 시약 지출을 임상 결과와 연계하는 가치 기반 계약을 체결하도록 유도하고 있습니다.

스페인의 체외(In-vitro) 진단 시장 동향 및 인사이트

만성 질환과 생활 습관병의 부담 증가

스페인 성인의 약 15.1%가 만성 신장 질환을 앓고 있으며, 인구 고령화로 이 수치는 계속 증가하고 있습니다. 당뇨병, 암, 심혈관 질환의 높은 유병률은 일차 진료 클리닉에서 더 이른 시점과 더 빈번한 검사를 촉진하고 있습니다. CARABELA-CKD 프로그램은 신장학 치료 경로를 표준화하고 스페인의 IVD 시장 전반에 걸쳐 크레아티닌, eGFR, 미세알부민 검사 수요를 높이고 있습니다. 갈리시아와 아스투리아스 지역의 실험실들은 신장 패널 검사가 매년 두 자릿수 증가세를 보인다고 보고하며, 이로 인해 시약 유통업체들은 재고 수준을 높여야 하는 상황입니다. 지역 보건 당국은 이제 병원 재정 지원 협약에 선별 검사 목표를 포함시키며, 구매량을 만성 질환 관리 지표와 연계하는 접근법을 취하고 있습니다. 이러한 요소들이 종합적으로 작용하여 일상적 및 전문적 검사의 꾸준한 기초 성장세를 뒷받침하고 있습니다.

분자 및 면역 진단의 급속한 기술 혁신

유럽투자은행(EIB)의 유니버설 DX에 대한 2천만 유로 대출은 대장암 조기 발견을 위한 액체 생검 개발을 가속화합니다. 스페인 스타트업들은 차세대 시퀀싱과 머신러닝 알고리즘을 결합해 한 번의 분석으로 다중 바이오마커를 프로파일링함으로써 검사당 비용을 낮춥니다. 발렌시아 대학병원들은 90분 내 결과를 제공하고 입원 격리 기간을 단축하는 다중 호흡기 패널을 검증했습니다. 면역진단 플랫폼은 이제 화학발광 검출과 자동 교정을 통합하여 갑상선 및 심장 마커의 민감도를 높입니다. IVDR이 추적성과 성능 벤치마킹을 강화함에 따라 현지 기업들은 클라우드 기반 품질 관리 대시보드를 도입하여 인증기관 감사에 직접 반영함으로써 규정 준수를 강화하고 경쟁 차별화를 강화하고 있습니다.

엄격히 진화하는 EU IVDR 규제 상황

스페인 실험실의 73%가 IVDR 적합성 파일 완성에 필요한 충분한 지침이 부족하다고 응답했습니다. 고위험 검사는 2025년 5월까지 새로운 성능 연구 및 시판 후 감시 규정을 충족해야 하지만, 인증기관 수용 능력은 여전히 부족합니다. 2024/1860 개정안은 일부 기한을 연장하는 동시에 공급망 추적 의무를 추가하여 행정 업무량을 증가시킵니다. 소규모 시약 제조업체들은 문서 작업에 R&D 예산을 전용하면서 제품 파이프라인 회전율을 저하시키고 있습니다. 각 자치구가 자체 조달 기준을 통해 EU 법률을 해석함에 따라 공급업체들은 전국적 출시를 복잡하게 만드는 다양한 지역별 체크리스트에 직면하고 있습니다.

부문 분석

2024년 스페인의 IVD 시장 규모에서 임상 화학 분야는 대사, 신장, 간 기능 패널의 핵심적 역할에 힘입어 28.5%를 차지했습니다. 일상 분석기는 높은 처리량과 비용 효율성을 달성하여 시약 수요를 안정화시킵니다. 그러나 병원들이 종양학 및 감염병 유전자 검사를 확대함에 따라 분자 진단 시장은 9.6%의 연평균 복합 성장률(CAGR)을 기록 중입니다. 스페인의 IVD 시장은 지역 항생제 내성 프로파일에 맞춤화된 증후군별 PCR 메뉴를 제공하는 Seegene과 Werfen의 합작 투자로 혜택을 보고 있습니다. 차세대 시퀀싱 비용이 하락함에 따라 지역 센터들은 EU 혁신 기금을 통해 자금 조달된 암 위험도 선별 프로그램을 시범 운영하며 성장을 공고히 하고 있습니다.

면역분석과 PCR 마커를 결합한 하이브리드 패널로의 전환은 기존 부문 경계를 모호하게 만든다. 실험실들은 비정상적인 화학 검사 결과 후 확인용 분자 검사를 실행하는 리플렉스 검사 프로토콜을 도입하여 부문 간 시약 소비를 증가시키고 있습니다. IVDR은 추적 가능한 로트 출시 데이터를 의무화하여 화학 및 분자 중간 소프트웨어의 통합을 촉진합니다. 이러한 발전은 분자진단의 전략적 중요성을 강화하는 동시에 임상 화학이 스페인의 IVD 시장에서 물량 주도권을 유지하도록 보장합니다.

2024년 스페인의 IVD 시장 점유율에서 시약 및 소모품이 71%를 차지했으며, 이는 높은 검사 빈도와 재고 보충 주기를 반영합니다. 실험실 정보 시스템과 연동된 자동화 재고 관리 모듈은 유통기한 관련 손실을 줄이지만, 치열한 입찰 가격 경쟁으로 마진은 여전히 낮습니다. 소프트웨어 및 서비스 부문(현재 매출의 10% 미만)은 디지털 병리학, 클라우드 미들웨어, AI 분석이 조달 우선순위로 부상하며 8.2%의 연평균 성장률(CAGR)로 다른 카테고리를 앞지를 전망입니다. 병원들은 장비 임대와 예측 유지보수 모듈을 묶은 구독 모델을 도입해 자본 지출을 운영비로 전환하고 있습니다.

기기 공급업체들은 이제 오픈 API를 내장해 타사 알고리즘이 분석기 데이터를 조회할 수 있도록 함으로써 플랫폼을 임상 의사 결정 허브로 전환하고 있습니다. 스페인의 디지털 헬스 전략은 HL7-FHIR 메시징을 선호하는 상호운용성 표준을 설정하여 공급업체들이 통합 인증을 추진하도록 유도합니다. 이에 따라 시약 제조사들은 소프트웨어 기업과 협력하여 품질 관리 대시보드를 패키징하고, 소모품 판매를 분석 성능 보증과 연계합니다. 하드웨어, 시약, 분석 기술 간의 이러한 융합은 스페인의 IVD 시장 전반에 걸쳐 종합적인 구매 결정을 촉진합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성 및 생활 습관병(당뇨병, 심혈관질환, 암)의 증가하는 부담

- 분자 및 면역 진단에 있어서의 급속한 기술 혁신

- 일차의료 및 가정 환경에서의 현장진단(Point-of-Care Testing) 확대

- 디지털 실험실 현대화를 위한 정부 및 EU 투자 프로그램

- 정밀의료와 동반진단의 채택 확대

- 시장 성장 억제요인

- 엄격하고 진화하는 EU IVDR 규제 환경

- 지역적 보험 적용 지연과 예산 제약

- 숙련된 실험실 인력 부족 및 교육 격차

- 규제 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 검사 유형별

- 임상 화학

- 면역 진단

- 분자진단학

- 혈액학

- 미생물 검사

- 응고 검사

- 현장진단(POC) 검사

- 제품별

- 기기 및 분석장치

- 시약 및 소모품

- 소프트웨어 & 서비스

- 사용성별

- 일회용 체외(In-vitro) 진단

- 재사용 가능한 체외(In-vitro) 진단

- 용도별

- 감염증

- 당뇨병

- 종양학(암)

- 심장병학

- 자가면역질환

- 기타 용도

- 최종 사용자별

- 병원 및 클리닉

- 진단 실험실

- 학술기관 및 연구기관

- 재택 케어/외래 POC 설정

- 기타 최종 사용자

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- Danaher Corporation(Beckman Coulter, Cepheid)

- F. Hoffmann-La Roche AG

- Siemens Healthineers AG

- Thermo Fisher Scientific Inc.

- bioMerieux SA

- Becton, Dickinson and Company

- Bio-Rad Laboratories Inc.

- QIAGEN NV

- Sysmex Corporation

- Werfen Group(Instrumentation Laboratory)

- Grifols SA

- Diasorin SpA

- Eurofins Scientific SE

- Illumina Inc.

- Hologic Inc.

- Nova Biomedical

- Sekisui Diagnostics

- Randox Laboratories

- Operon SA

- Fujifilm Wako

제7장 시장 기회와 전망

HBR 25.11.10The Spain IVD market size stands at USD 2.51 billion in 2025 and is forecast to reach USD 3.13 billion by 2030, expanding at a 4.55% CAGR.

Continued momentum is rooted in an aging population, higher chronic-disease incidence, and the country's full transition to the EU In Vitro Diagnostic Regulation (IVDR). Strong demand for frequent renal, diabetes, and hypertension screening is lifting test volumes, while hospital groups in Madrid and Catalonia are modernizing laboratories with AI-enabled analyzers that shorten turnaround times. Molecular assay innovators are benefiting from European Investment Bank financing, and Spain's Digital Health Strategy is steering budgets toward connected instruments that meet IVDR traceability rules. At the same time, decentralized procurement across 17 autonomous communities is nudging suppliers toward value-based contracts that link reagent spending to clinical outcomes.

Spain In-vitro Diagnostics Market Trends and Insights

Rising Burden of Chronic & Lifestyle Diseases

About 15.1% of Spanish adults live with chronic kidney disease, a figure that continues to climb with population aging. Higher prevalence of diabetes, cancer, and cardiovascular disorders is prompting earlier, more frequent testing in primary care clinics. The CARABELA-CKD program standardizes nephrology pathways and lifts demand for creatinine, eGFR, and micro-albumin tests across the Spain IVD market. Laboratories in Galicia and Asturias report double-digit yearly increases in renal panels, pushing reagent distributors to boost stock levels. Regional health authorities now bundle screening targets into hospital financing agreements, an approach that ties purchasing volumes to chronic-care metrics. Collectively, these factors underpin consistent baseline growth for routine and specialty assays.

Rapid Technological Innovation in Molecular & Immunodiagnostics

The European Investment Bank's EUR 20 million loan to Universal DX accelerates liquid-biopsy development for early colorectal-cancer detection. Spanish startups mix next-generation sequencing with machine-learning algorithms to profile multiple biomarkers in one run, lowering per-test costs. University hospitals in Valencia validate multiplex respiratory panels that deliver 90-minute results and reduce inpatient isolation days. Immunodiagnostic platforms now integrate chemiluminescent detection with automated calibration, raising sensitivity for thyroid and cardiac markers. As IVDR pushes traceability and performance benchmarking, local firms adopt cloud-based quality-control dashboards that feed directly into notified-body audits, strengthening compliance while sharpening competitive differentiation.

Stringent & Evolving EU IVDR Regulatory Landscape

Seventy-three percent of Spanish laboratories say they lack adequate guidance to complete IVDR conformity files. High-risk assays must meet new performance-study and post-market-surveillance rules by May 2025, yet notified-body capacity remains tight. The 2024/1860 amendment extends certain timelines but also adds supply-chain traceability duties, raising administrative workloads. Smaller reagent makers divert R&D budgets toward documentation, slowing product-pipeline turnover. Because each autonomous community interprets EU law through its own procurement filters, suppliers face variable local checklists that complicate national launches.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Point-of-Care Testing Across Primary & Home Settings

- Government & EU Investment Programs for Digital Lab Modernization

- Regional Reimbursement Delays & Budget Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clinical chemistry generated 28.5% of the Spain IVD market size in 2024, supported by its central role in metabolic, renal, and hepatic panels. Routine analyzers achieve high throughput and cost efficiency, which stabilizes reagent demand. However, molecular diagnostics is posting a 9.6% CAGR as hospitals expand oncology and infectious-disease gene testing. The Spain IVD market benefits from Seegene and Werfen's joint venture, which promises syndromic PCR menus tailored to local antimicrobial-resistance profiles. As next-generation sequencing costs fall, regional centers pilot cancer-risk screening programs financed through EU innovation funds, cementing growth.

A shift toward hybrid panels that combine immunoassay and PCR markers blurs traditional segment boundaries. Laboratories deploy reflex-testing protocols that trigger confirmatory molecular runs after abnormal chemistry results, raising cross-segment reagent consumption. IVDR mandates traceable lot-release data, encouraging integration of chemistry and molecular middleware. These developments reinforce molecular diagnostics' strategic importance while ensuring clinical chemistry retains volume leadership in the Spain IVD market.

Reagents & consumables represented 71% of the Spain IVD market share in 2024, reflecting high test frequency and replenishment cycles. Automated inventory modules tied to laboratory-information systems trim expiry-related wastage, yet tight tender pricing keeps margins thin. Software & services-currently under 10% of revenues-will outpace other categories at an 8.2% CAGR as digital pathology, cloud middleware, and AI analytics become procurement priorities. Hospitals adopt subscription models that bundle instrument leasing with predictive-maintenance modules, converting capital outlays into operating expenses.

Instrument vendors now embed open APIs so third-party algorithms can interrogate analyzer data, turning platforms into clinical-decision hubs. Spain's Digital Health Strategy sets interoperability standards that favor HL7-FHIR messaging, nudging suppliers to certify integrations. In turn, reagent makers collaborate with software firms to package quality-control dashboards, tying consumable sales to analytical-performance guarantees. This convergence between hardware, reagents, and analytics drives holistic purchasing decisions across the Spain IVD market.

The Spain In-Vitro Diagnostics Market Report is Segmented by Test Type (Clinical Chemistry, Molecular Diagnostics, and More), Product (Instruments & Analyzers, Reagents, and More), Usability (Disposable IVD Devices and Reusable IVD Devices), Application (Infectious Diseases, Oncology, Cardiology, and More), and End Users (Diagnostic Laboratories, Hospitals and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Abbott Laboratories

- Danaher Corporation (Beckman Coulter, Cepheid)

- Roche

- Siemens Healthineers

- Thermo Fisher Scientific

- bioMerieux

- Beckton Dickinson

- Bio-Rad Laboratories

- QIAGEN

- Sysmex

- Werfen Group (Instrumentation Laboratory)

- Grifols

- Diasorin S.p.A.

- Eurofins

- Illumina

- Hologic

- Nova Biomedical

- Sekisui Diagnostics

- Randox Laboratories

- Operon S.A.

- Fujifilm Wako

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Chronic & Lifestyle Diseases (Diabetes, CVD, Cancer)

- 4.2.2 Rapid Technological Innovation in Molecular & Immunodiagnostics

- 4.2.3 Expansion of Point-of-Care Testing Across Primary & Home Settings

- 4.2.4 Government & EU Investment Programs for Digital Lab Modernization

- 4.2.5 Growth of Precision Medicine & Companion Diagnostics Adoption

- 4.3 Market Restraints

- 4.3.1 Stringent & Evolving EU IVDR Regulatory Landscape

- 4.3.2 Regional Reimbursement Delays & Budget Constraints

- 4.3.3 Shortage of Skilled Laboratory Personnel & Training Gaps

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry Intensity

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Test Type

- 5.1.1 Clinical Chemistry

- 5.1.2 Immunodiagnostics

- 5.1.3 Molecular Diagnostics

- 5.1.4 Hematology

- 5.1.5 Microbiology

- 5.1.6 Coagulation

- 5.1.7 Point-of-Care (POC) Tests

- 5.2 By Product

- 5.2.1 Instruments & Analyzers

- 5.2.2 Reagents & Consumables

- 5.2.3 Software & Services

- 5.3 By Usability

- 5.3.1 Disposable IVD Devices

- 5.3.2 Reusable IVD Devices

- 5.4 By Application

- 5.4.1 Infectious Disease

- 5.4.2 Diabetes

- 5.4.3 Oncology (Cancer)

- 5.4.4 Cardiology

- 5.4.5 Autoimmune Disorders

- 5.4.6 Other Applications

- 5.5 By End-User

- 5.5.1 Hospitals & Clinics

- 5.5.2 Diagnostic Laboratories

- 5.5.3 Academic & Research Institutes

- 5.5.4 Home-Care / Ambulatory POC Settings

- 5.5.5 Other End-Users

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Danaher Corporation (Beckman Coulter, Cepheid)

- 6.3.3 F. Hoffmann-La Roche AG

- 6.3.4 Siemens Healthineers AG

- 6.3.5 Thermo Fisher Scientific Inc.

- 6.3.6 bioMerieux SA

- 6.3.7 Becton, Dickinson and Company

- 6.3.8 Bio-Rad Laboratories Inc.

- 6.3.9 QIAGEN N.V.

- 6.3.10 Sysmex Corporation

- 6.3.11 Werfen Group (Instrumentation Laboratory)

- 6.3.12 Grifols S.A.

- 6.3.13 Diasorin S.p.A.

- 6.3.14 Eurofins Scientific SE

- 6.3.15 Illumina Inc.

- 6.3.16 Hologic Inc.

- 6.3.17 Nova Biomedical

- 6.3.18 Sekisui Diagnostics

- 6.3.19 Randox Laboratories

- 6.3.20 Operon S.A.

- 6.3.21 Fujifilm Wako

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment