|

시장보고서

상품코드

1848059

커넥티드카 디바이스 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Connected Car Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

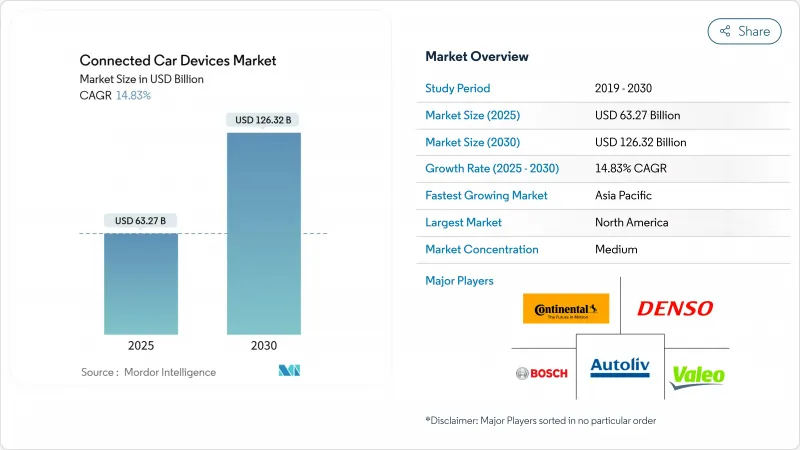

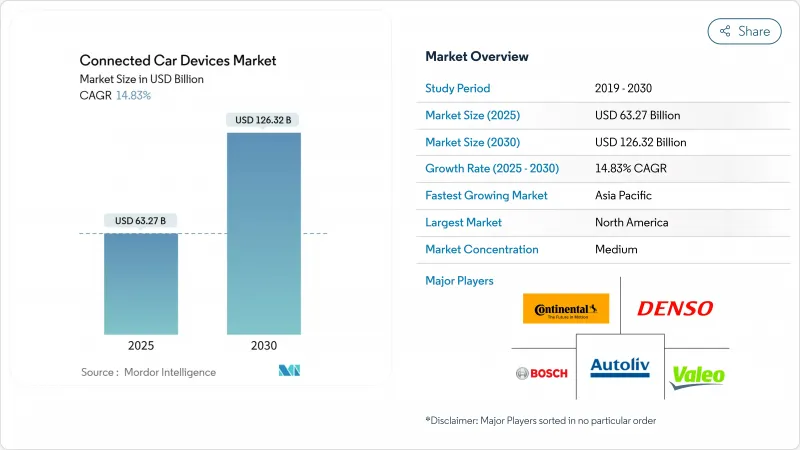

커넥티드카 디바이스 시장 규모는 2025년에 632억 7,000만 달러로 평가되었고, 예측기간(2025-2030년)의 CAGR은 14.83%를 나타낼 것으로 예측되며, 2030년에 1,263억 2,000만 달러로 성장할 전망입니다.

수요는 5G의 급속한 보급, 새로운 e-Call 및 ADAS 의무화, 그리고 원활한 연결성에 의존하는 소프트웨어 정의 차량으로의 전환에서 비롯됩니다. OEM들은 임베디드 모듈을 구독 서비스와 데이터 수익화의 핵심으로 간주하며, 연결형 서비스로 차량당 최대 1,600달러의 잠재적 수익을 창출할 수 있습니다. 성장은 셀룰러 차량-모든 것 간 통신(C-V2X) 표준의 확산과 안전 핵심 기능의 지연 시간을 줄이는 엣지 AI 칩셋에 의해 강화됩니다.

세계의 커넥티드카 디바이스 시장 동향 및 인사이트

신속한 5G 구축 및 통신사-OEM 파트너십

자동차 5G 연결은 2027년까지 활성화 수익 측면에서 기하급수적으로 성장할 것으로 예상됩니다. Cisco와 TELUS는 이미 자동화 플랫폼에서 150만 대 이상의 5G 차량을 공급하여 자율 주행 기능에 중요한 지연 시간을 거의 실시간 수준으로 단축했습니다. 현재 파트너십은 연결성, 엣지 컴퓨팅 및 개발자 도구를 통합된 제품으로 묶어 OEM이 새로운 서비스를 더 빠르게 출시할 수 있도록 합니다. 이러한 제휴는 통신사가 대역폭 공급자에서 전략적 기술 파트너로 전환함에 따라 공급업체 환경을 변화시킵니다. 그 결과 생성된 서비스 플랫폼은 프리미엄 인포테인먼트, 원격 진단, 고해상도 지도를 뒷받침하여 사용자당 평균 수익(ARPU) 증대를 지원합니다.

의무화된 전자식 긴급통화(eCall) 및 ADAS 규정

미국 고속도로교통안전청(NHTSA)은 2029년 9월까지 모든 경량 차량에 보행자 감지 기능이 탑재된 자동 긴급 제동 장치(AEB) 장착을 의무화하며, 연간 준수 비용 3억 5,400만 달러와 생애 주기 혜택 58억 2,000만 달러 이상의 효과를 예상합니다. 유럽은 일반 안전 규정(GSR) 하에 e-Call 및 일련의 운전자 보조 기능을 시행하는 반면, 중국은 베이징에 7,000개 이상의 5G-A 기지국을 구축하며 차량-도로-클라우드 연계 시범 사업을 확대하고 있습니다. 이러한 의무화는 일정 관련 불확실성을 제거하여 OEM이 연결 센서를 표준 장비로 통합하도록 촉진합니다. 공급업체는 예측 가능한 물량으로 이익을 얻고, 소비자는 사고율을 낮추는 보편적 안전 기능을 확보합니다.

사이버 보안 취약성 및 리콜

Pwn2Own Automotive 2024 대회에서 알파인(Alpine)의 Halo9 인포테인먼트 장치에 96% 성공률의 제로클릭(zero-click) 공격이 노출되며 원격 침해의 용이성이 부각되었습니다. 2023년 소프트웨어 관련 리콜은 3천만 대 이상의 차량에 영향을 미쳤으며, NIST에 등재된 CVE-2023-6248 결함은 대중적인 텔레매틱스 게이트웨이의 완전한 장치 장악을 가능케 합니다. 차량이 이동형 데이터 센터로 진화함에 따라 공격 표면이 확대되어 판매 후 패치 비용과 평판 손실이 증가하고 있습니다. 규제 기관은 설계 단계부터 보안(security-by-design)을 요구하며, 공급업체에게 하드웨어 신뢰 기반(root-of-trust), 안전한 무선 업데이트(OTA) 프레임워크, 지속적인 침투 테스트를 적용하도록 압박하고 있습니다.

부문 분석

2024년 커넥티드카 디바이스 시장 점유율의 63.27%를 OEM 설치가 차지했습니다. 공장 장착 하드웨어는 차량 진단, 전력 관리, 보증 프레임워크와 깊이 통합되기 때문입니다. 자동차 제조사는 e-Call 및 ADAS 규정 준수를 보장하고, 무선 업데이트를 간소화하며, 데이터에 대한 브랜드 통제력을 강화하기 위해 조립 과정에서 모듈을 내장합니다. 소프트웨어 정의 아키텍처에 대한 의존도가 높아짐에 따라 OEM이 원격 기능 활성화 및 예측 유지보수 같은 수익 창출 서비스와 연결성을 연계함에 따라 이 채널의 주도적 위상이 공고해지고 있습니다.

그러나 보험사와 차량 관리사가 기존 차량을 개조함에 따라 애프터마켓 공급업체도 연평균 15.74%의 성장률로 빠르게 확장 중입니다. 플러그 앤 플레이 방식의 동글과 하드와이어드 블랙박스는 행동 기반 보험료 산정 및 자산 추적의 기반이 되는 실시간 사용 데이터를 제공합니다. HARMAN의 즉시 업그레이드 키트는 설치 속도와 크로스 브랜드 호환성이 필요한 혼합 차량군에 맞춤화된 솔루션의 대표적인 사례다. OEM의 통제력은 여전히 강력하지만, 가격에 민감한 소유주와 상업 운영자들은 병행 애프터마켓을 지속적으로 주도하며 커넥티드카 디바이스 시장 내 경쟁적 다양성을 보장하고 있습니다.

차량 간 통신(V2V)은 도로변 장치 없이도 충돌 경고를 제공하기 때문에 2024년 커넥티드카 디바이스 시장 매출 점유율의 39.62%를 차지했습니다. 성숙한 표준과 입증된 안전성 향상 효과로 OEM들은 특히 5성급 안전 등급을 목표로 하는 대량 생산 모델에 V2V를 우선 도입하고 있습니다. 상업용 차량에서도 전방 충돌 경고 시스템이 가동 중단 시간과 보험 비용을 절감함에 따라 개조 설치가 확산되고 있습니다.

차량-전력망(V2G) 기능은 재생에너지 비중이 높은 전력망 안정화를 위해 에너지 유틸리티 기업과 자동차 제조사가 협력함에 따라 2030년까지 연평균 15.12% 성장률을 기록할 전망입니다. 양방향 충전기와 연결성을 결합하면 전기차가 저장된 전력을 네트워크로 역송전하여 소유주와 전력망 운영자에게 새로운 수익원을 창출합니다. 차량-인프라(V2I) 및 차량-보행자(V2P) 부문 성장은 스마트시티 투자에 따라 움직이지만, 이는 광범위한 공공 투자에 의존합니다. 시간이 지나면 통합 V2X 제품군이 모든 모드를 통합하겠지만, 생태계가 성숙해지는 동안 V2V는 핵심 기술로 남을 것입니다.

지역 분석

2024년 북미는 커넥티드카 디바이스 시장 점유율의 38.73%를 차지했습니다. 인프라 투자 및 일자리 법(IIJA)에 따른 연방 자금 지원과 ADAS, 고화질 인포테인먼트, 5G 핫스팟으로 가득한 프리미엄 SUV에 대한 소비자 수요가 확산을 주도하고 있습니다. 미국 교통부와 5G 자동차 협회(5G Automotive Association)의 지속적인 시범 운영은 C-V2X에 대한 신뢰도를 높이는 한편, 엄격한 사이버 보안 및 개인정보 보호 규정이 조달 사양을 형성하고 있습니다. 캐나다와 멕시코는 통합된 공급망의 혜택을 받아 지역 OEM 공장에서 커넥티드 모듈과 소프트웨어 스택을 표준화할 수 있습니다. 이러한 요소들은 북미 전역에서 건강한 교체 주기와 애프터세일즈 구독 서비스를 유지합니다.

아시아태평양 지역은 2030년까지 연평균 15.37%의 가장 빠른 성장률을 기록할 전망입니다. 중국의 차량-도로-클라우드 통합 청사진은 공공 및 민간 투자를 주도하며, 베이징 시만 해도 지능형 모빌리티를 위한 5G-A 기지국 7,000개 이상을 운영 중입니다. 국내 브랜드들은 혼잡한 전기차 시장에서 차별화를 위해 커넥티비티를 탑재하고 있으며, 지역 공급업체들은 이륜차 및 초소형차를 위한 비용 최적화된 텔레매틱스를 제공하고 있습니다. 일본과 한국은 반도체 제조 역량과 조기 5G 도입을 바탕으로 차세대 C-V2X 사이드링크 기능을 시험 중입니다. 인도는 안전 규제가 강화되고 스마트폰에 익숙한 구매자들이 상시 연결 인포테인먼트를 요구함에 따라 대량 시장으로 부상하고 있으나, 가격 민감도로 인해 유선 솔루션의 필요성은 여전히 존재합니다.

유럽은 의무적 e-Call 및 일반 안전 규정(GSR)과 같은 조화된 규제 하에 꾸준한 성장세를 유지합니다. 독일, 영국, 프랑스가 고급 트림 라인에 커넥티비티를 기본 적용하는 럭셔리 브랜드를 중심으로 도입을 주도하며 중형 브랜드들도 이를 따르고 있습니다. 에너지 효율 및 탄소 감축 목표는 EV 충전을 재생에너지 생산과 연계하는 V2G(차량-전력망) 시범 사업에 대한 관심을 촉진합니다. 엄격한 데이터 주권 법규는 클라우드 호스팅 선택에 영향을 미쳐 유럽 기반 공급업체에 우위를 제공합니다. 사이버 보안 인증을 위한 범유럽 표준이 개발 중이며, 이는 국경을 초월한 인증 절차를 간소화하고 커넥티드카 디바이스 시장을 더욱 활성화할 것으로 기대됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 분석가 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 5G의 급속한 보급 및 통신사-OEM 협력

- 미국, EU, 중국에서의 의무적 전자응급통화(e-Call) 및 ADAS 규정

- OEM의 구독 기반 수익 목표

- 차량 내 추론을 가능케 하는 엣지 AI 칩

- 사용량 기반 보험이 주도하는 애프터마켓 텔레매틱스

- 산업 간 앱 스토어 생태계

- 시장 성장 억제요인

- 사이버 보안 취약점 및 리콜

- 다중 대역 V2X 모듈의 높은 BOM 비용

- 데이터 클라우드 전송 비용이 OEM 서비스 마진을 잠식

- 반도체 공급망의 취약성

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 라이벌의 격렬함

제5장 시장 규모 및 성장 예측

- 최종 사용자별

- OEM

- 애프터마켓

- 통신 유형별

- V2V

- V2I

- V2P

- V2N

- V2G

- 제품 유형별

- 운전 지원 시스템(ADAS)

- 텔레매틱스

- 차재 인포테인먼트

- 사이버 보안 하드웨어

- 커넥티비티 기술별

- 내장형

- 통합형

- 테더

- DSRC

- C-V2X(4G/5G)

- 차량 추진 유형별

- 내연 엔진차

- 전기자동차

- 배터리 전기자동차

- 하이브리드 전기자동차

- 연료전지 전기자동차

- 플러그인 하이브리드 전기자동차

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- Continental AG

- Robert Bosch GmbH

- Denso Corporation

- ZF Friedrichshafen AG

- Harman International

- Valeo SA

- Magna International

- Panasonic Corp.

- Visteon Corp.

- Autoliv Inc.

- Infineon Technologies AG

- Autotalks Ltd.

- Qualcomm Inc.

- NXP Semiconductors

- NVIDIA Corp.

- Sierra Wireless

- Cisco Systems

- Huawei Technologies

- AT&T

- Verizon

- Vodafone Group

- Ericsson

- LG Electronics

- Telit

제7장 시장 기회와 전망

HBR 25.11.10The Connected Car Devices Market size is estimated at USD 63.27 billion in 2025, and is expected to reach USD 126.32 billion by 2030, at a CAGR of 14.83% during the forecast period (2025-2030).

Demand stems from rapid 5G roll-outs, new e-Call and ADAS mandates, and the shift toward software-defined vehicles that rely on seamless connectivity. OEMs view embedded modules as the backbone for subscription services and data monetization, with potential revenue of USD 1,600 per vehicle from connected offerings. Growth is bolstered by the spread of cellular vehicle-to-everything (C-V2X) standards and edge AI chipsets that lower latency for safety-critical functions.

Global Connected Car Devices Market Trends and Insights

Rapid 5G Roll-Out and Carrier-OEM Partnerships

Automotive 5G connections are forecast to grow exponentially in enablement revenues by 2027. Cisco and TELUS already provision more than 1.5 million 5G vehicles on automated platforms, cutting latency to near-real-time levels critical for autonomous features. Partnerships now bundle connectivity, edge computing, and developer tools into unified offerings that let OEMs launch new services faster. These alliances change the supplier landscape because carriers shift from bandwidth providers to strategic technology partners. The resulting service platforms underpin premium infotainment, remote diagnostics, and high-definition maps, supporting higher average revenue per user.

Mandatory E-Call and ADAS Regulations

The National Highway Traffic Safety Administration requires automatic emergency braking with pedestrian detection on all light vehicles by September 2029, carrying USD 354 million in annual compliance costs and lifetime benefits topping USD 5.82 billion. Europe enforces e-Call and a suite of driver-assistance functions under the General Safety Regulation, while China scales vehicle-road-cloud pilots with more than 7,000 5G-A base stations in Beijing. These mandates remove uncertainty around timelines, prompting OEMs to integrate connected sensors as standard equipment. Suppliers benefit from predictable volumes, and consumers gain universal safety features that lower accident rates.

Cyber-Security Vulnerabilities and Recalls

The Pwn2Own Automotive 2024 contest exposed a zero-click exploit in Alpine's Halo9 infotainment unit with a 96% success rate, highlighting the ease of remote compromise. Software-related recalls affected over 30 million vehicles in 2023, and the NIST-listed CVE-2023-6248 flaw enables full device takeover of popular telematics gateways. As vehicles become rolling data centres, their attack surface expands, raising the cost of post-sale patches and reputational damage. Regulators demand security-by-design, pushing suppliers to embed hardware root-of-trust, secure over-the-air frameworks, and continuous penetration testing.

Other drivers and restraints analyzed in the detailed report include:

- Subscription-Based Revenue Targets

- Edge AI Chips for In-Vehicle Inferencing

- High BOM Cost of Multi-Band V2X Modules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

OEM installations captured 63.27% of the connected car devices market share in 2024 because factory-fitted hardware integrates deeply with vehicle diagnostics, power management, and warranty frameworks. Automakers embed modules during assembly to ensure compliance with e-Call and ADAS mandates, streamline over-the-air upgrades, and bolster brand control over data. Growing reliance on software-defined architectures cements this channel's leadership as OEMs link connectivity to revenue-generating services such as remote feature activation and predictive maintenance.

However, aftermarket providers are expanding quickly, with a 15.74% CAGR, as insurers and fleet managers retrofit legacy assets. Plug-and-play dongles and hardwired black boxes supply real-time usage data that underpins behaviour-based premiums and asset tracking. HARMAN's ready-upgrade kits exemplify solutions tailored for mixed fleets needing installation speed and cross-brand compatibility. While OEM control remains strong, price-sensitive owners and commercial operators continue to drive a parallel aftermarket, ensuring competitive variety within the connected car devices market.

Vehicle-to-vehicle links represented 39.62% of the connected car devices market revenue share in 2024 because they deliver collision warnings without requiring roadside units. Mature standards and demonstrated safety gains encourage OEMs to adopt V2V first, particularly in high-volume models aiming for five-star safety ratings. Retrofits also proliferate in commercial fleets where forward-collision alerts cut downtime and insurance costs.

Vehicle-to-grid capability is projected to post a 15.12% CAGR to 2030 as energy utilities partner with automakers to stabilise renewable-heavy grids. Bidirectional chargers paired with connectivity let electric cars feed stored power back to the network, creating new revenue for owners and grid operators. Growth in vehicle-to-infrastructure and vehicle-to-pedestrian segments follows smart-city spending, yet these depend on broader public investment. Over time, integrated V2X suites will blend all modes, but V2V will remain the cornerstone while ecosystems mature around it.

The Connected Car Devices Market Report is Segmented by End-User Type (OEM and Aftermarket), Communication Type (V2V, V2I, and More), Product Type (Driver Assistance System (DAS), Telematics, and More), Connectivity Technology (Embedded, Integrated, and More), Vehicle Propulsion Type (IC Engine and Electric), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 38.73% of the connected car devices market share in 2024. Uptake is driven by federal funding under the Infrastructure Investment and Jobs Act and consumer appetite for premium SUVs brimming with ADAS, high-definition infotainment, and 5G hotspots. Ongoing pilots with the U.S. Department of Transportation and the 5G Automotive Association boost confidence in C-V2X, while tight cybersecurity and privacy rules shape procurement specifications. Canada and Mexico benefit from integrated supply chains, enabling regional OEM plants to standardise connected modules and software stacks. These factors sustain healthy replacement cycles and after-sales subscriptions across North America.

Asia-Pacific is on track for the fastest 15.37% CAGR to 2030. China's vehicle-road-cloud blueprint anchors public and private spending, with Beijing alone hosting more than 7,000 5G-A base stations for intelligent mobility. Domestic brands embed connectivity to differentiate in a crowded electric-vehicle arena, while regional suppliers deliver cost-optimised telematics for two-wheelers and microcars. Japan and South Korea leverage chip-making prowess and early 5G roll-outs to test next-generation C-V2X sidelink features. India emerges as a high-volume opportunity as safety norms tighten and smartphone-savvy buyers demand always-on infotainment, though price sensitivity keeps tethered solutions relevant.

Europe maintains steady momentum under harmonised regulations such as mandatory e-Call and the General Safety Regulation. Germany, the United Kingdom, and France lead adoption as luxury marques bundle connectivity into premium trim lines, and mid-range brands follow suit. Energy-efficiency and carbon-reduction goals drive interest in vehicle-to-grid pilots that align EV charging with renewable output. Strict data sovereignty laws influence cloud-hosting choices, giving European-based providers an edge. Pan-EU standards for cybersecurity certification are under development, promising to streamline cross-border homologation and further stimulate the connected car devices market.

- Continental AG

- Robert Bosch GmbH

- Denso Corporation

- ZF Friedrichshafen AG

- Harman International

- Valeo SA

- Magna International

- Panasonic Corp.

- Visteon Corp.

- Autoliv Inc.

- Infineon Technologies AG

- Autotalks Ltd.

- Qualcomm Inc.

- NXP Semiconductors

- NVIDIA Corp.

- Sierra Wireless

- Cisco Systems

- Huawei Technologies

- AT&T

- Verizon

- Vodafone Group

- Ericsson

- LG Electronics

- Telit

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid 5G Roll-Out and Carrier-OEM Partnerships

- 4.2.2 Mandatory E-Call and ADAS Regulations in US, EU, CN

- 4.2.3 Subscription-Based Revenue Targets by OEMs

- 4.2.4 Edge AI Chips Enabling In-Vehicle Inferencing

- 4.2.5 Usage-Based-Insurance Driving Aftermarket Telematics

- 4.2.6 Cross-Industry App-Store Ecosystems

- 4.3 Market Restraints

- 4.3.1 Cyber-Security Vulnerabilities and Recalls

- 4.3.2 High BOM Cost of Multi-Band V2X Modules

- 4.3.3 Data-Cloud Egress Fees Eroding OEM Service Margins

- 4.3.4 Semiconductor Supply-Chain Fragility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By End-User Type

- 5.1.1 OEM

- 5.1.2 Aftermarket

- 5.2 By Communication Type

- 5.2.1 V2V

- 5.2.2 V2I

- 5.2.3 V2P

- 5.2.4 V2N

- 5.2.5 V2G

- 5.3 By Product Type

- 5.3.1 Driver Assistance System (ADAS)

- 5.3.2 Telematics

- 5.3.3 In-Car Infotainment

- 5.3.4 Cyber-security Hardware

- 5.4 By Connectivity Technology

- 5.4.1 Embedded

- 5.4.2 Integrated

- 5.4.3 Tethered

- 5.4.4 DSRC

- 5.4.5 C-V2X (4G/5G)

- 5.5 By Vehicle Propulsion Type

- 5.5.1 Internal-Combustion Engine Vehicles

- 5.5.2 Electric Vehicles

- 5.5.2.1 Battery Electric Vehicle

- 5.5.2.2 Hybrid Electric Vehicle

- 5.5.2.3 Fuel-cell Electric Vehicle

- 5.5.2.4 Plug-in Hybrid Electric Vehicle

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 Robert Bosch GmbH

- 6.4.3 Denso Corporation

- 6.4.4 ZF Friedrichshafen AG

- 6.4.5 Harman International

- 6.4.6 Valeo SA

- 6.4.7 Magna International

- 6.4.8 Panasonic Corp.

- 6.4.9 Visteon Corp.

- 6.4.10 Autoliv Inc.

- 6.4.11 Infineon Technologies AG

- 6.4.12 Autotalks Ltd.

- 6.4.13 Qualcomm Inc.

- 6.4.14 NXP Semiconductors

- 6.4.15 NVIDIA Corp.

- 6.4.16 Sierra Wireless

- 6.4.17 Cisco Systems

- 6.4.18 Huawei Technologies

- 6.4.19 AT&T

- 6.4.20 Verizon

- 6.4.21 Vodafone Group

- 6.4.22 Ericsson

- 6.4.23 LG Electronics

- 6.4.24 Telit

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment