|

시장보고서

상품코드

1848083

스페인의 에스테틱 기기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Spain Aesthetic Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

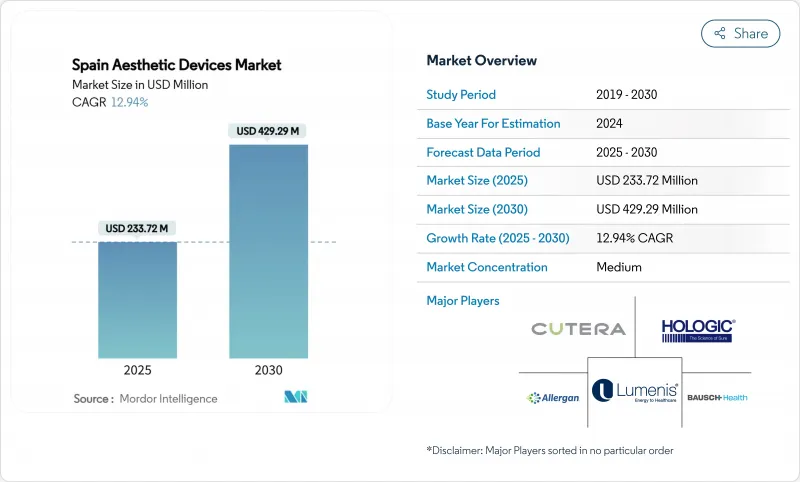

스페인의 에스테틱 기기 시장 규모는 2025년에 2억 3,372만 달러로 평가되었고, 예측기간(2025-2030년)의 CAGR은 12.94%를 나타낼 것으로 예측되며, 2030년에 4억 2,929만 달러에 달할 전망입니다.

정교한 최소 침습 시술에 대한 지속적인 수요가 이러한 추세를 견인하고 있으며, 국내에서 매년 시행되는 40만 건의 미용 시술이 이를 뒷받침하고 있습니다. 침습적 수술을 전문의 자격을 갖춘 성형외과 의사에게만 허용하는 최근 규제 강화로 인해 시술 건수가 고품질 시설에 집중되면서, 클리닉들은 규정을 준수하는 프리미엄 장비를 도입하도록 장려받고 있습니다. 에너지 기반 플랫폼, 인공지능 기반 영상 기술, 가정용 기술의 병행 발전은 사용자 기반을 확대하는 동시에 치료 결과를 개선하여 스페인의 에스테틱 기기 시장의 장기적 성장 전망을 강화하고 있습니다.

스페인의 에스테틱 기기 시장 동향 및 인사이트

고령화와 젊음에 대한 수요

스페인의 중간 연령은 계속해서 상승하고 있지만, 동시에 미용에 대한 관심도 높아지면서 45-65세 연령층이 비수술적 피부 탄력 개선 및 재생 시술을 선택하는 추세입니다. 가시화 기능이 있는 초점형 초음파와 같이 콜라겐 생성을 촉진하는 에너지 기반 방식은 눈에 띄면서도 은한 결과를 제공함으로써 이러한 선호도에 부합합니다. 마드리드와 바르셀로나의 품질 지향적 소비자들이 선호하는 정밀한 시술 전 평가 기능을 제공하는 3D 피부 매핑 시스템의 도입이 이를 더욱 강화하고 있습니다. 병원 및 대형 클리닉 그룹들은 이러한 시술을 교정적이라기보다 예방적 차원에서 마케팅하며 환자 생애 주기를 연장하고 있습니다. 인구학적 추세가 지속됨에 따라 스페인의 에스테틱 기기 시장의 기본 수요 기반도 유지될 전망입니다.

미용 시술을 위한 의료 관광 증가

스페인은 Real Decreto 81/2014를 통해 EU 국경 간 의료 지침에 가입함으로써 EU 내 환자들에 대한 보험금 지급 절차를 간소화하여 선택적 미용 시술을 위한 논리적인 목적지로 자리매김했습니다. 2024년 9월 시행된 미용 수술을 전문의 자격을 갖춘 성형외과 의사에게만 허용하는 규정은 역설적으로 엄격한 안전 감독을 시사함으로써 국가의 브랜드 이미지를 개선했습니다. 발렌시아와 말라가의 클리닉들은 이제 해안가의 매력을 활용해 외국인 방문객을 대상으로 HIFU 기반 바디 컨투어링 패키지에 숙박을 묶어 제공하고 있습니다. 높은 환자 만족도는 디지털 입소문을 촉진하여 시술량과 장비 교체 수요를 높이는 선순환 유입 사이클을 강화하고 있습니다.

미용 시술에 대한 제한된 보험 적용

공공 보험은 선택적 미용 시술을 제외하여 환자들이 고가의 치료비를 자비로 부담하도록 합니다. 미용 관련 소송의 평균 법원 밖 합의금은 33,000유로를 초과하여 관련 재정적 위험을 보여줍니다. 장비 감가상각 비용이 시술 가격에 포함되기 때문에, 클리닉은 수익성을 유지하기 위해 이용률을 높여야 하며, 이는 중산층의 접근성을 제한합니다. Ley 29/2006 법률의 법적 프레임워크는 안전성과 효능에 대한 엄격한 증명을 요구하여 제조사의 규정 준수 비용을 증가시키며, 이는 다시 소비자에게 전가됩니다. 소비자용 광선 치료 마스크와 휴대용 RF 기기가 확산되고 있지만, 주요 도시 외곽 지역에서는 여전히 많은 스페인인들이 전문 장비를 이용하기 어렵습니다.

부문 분석

2024년 스페인의 에스테틱 기기 시장 점유율에서 에너지 기반 장비는 59.64%를 차지했으며, 레이저, 고주파, 초음파 플랫폼이 다양한 적응증에 걸쳐 다용도로 입증되었습니다. 초음파 기반 시스템은 현재 안드로겐성 탈모증 치료에 검증된 두피 재생 프로토콜로 확장된 고강도 집속 초음파 시술에 힘입어 2030년까지 연평균 16.35%의 성장률을 기록할 것으로 전망됩니다.

레이저 제조사들은 색소 합병증 없이 지속적인 여드름 제거 효과를 제공하는 실시간 열화상 기능을 탑재한 1726nm 장비를 상용화 중입니다. 온도 제어형 RF 마이크로니들링 플랫폼은 임상 시험에서 86.7%의 환자 만족도를 기록하며, 레이저 기술이 진화하는 가운데서도 고주파의 경쟁력을 유지하고 있습니다. 필러와 같은 비에너지 대체품은 개선된 유변학 및 강화된 AEMPS 감독으로 시장 점유율을 유지하는 반면, 화학 필링은 비용 효율적인 보조 치료법으로 틈새 시장에서 부활하고 있습니다. 마이크로니들 롤러는 이제 Class IIa 규정에 따라 관리되며, 이로 인해 클리닉들은 더 안전한 카트리지 기반 시스템을 채택하고 있습니다. 이러한 트렌드들은 종합적으로 스페인의 에스테틱 기기 시장이 에너지 기반 플랫폼을 계속 선호하면서도 보조 치료 분야에서의 표적화된 혁신을 위한 여지를 남겨두도록 보장합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고령화 인구 및 젊어 보이는 외모에 대한 수요

- 미용 시술을 위한 의료 관광 증가

- 최소 침습적 치료의 인기 상승

- 에스테틱 기기의 기술 발전

- 미용 및 웰빙에 대한 문화적 강조

- 도시 중심부의 사설 미용 클리닉 확대

- 시장 성장 억제요인

- 미용 시술에 대한 제한된 보험 적용 범위

- 농촌 지역의 인증된 미용 전문가 부족

- 기기와 필러에 대한 EU의 엄격한 규제 감독

- 선택적 시술의 경제적 민감성

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(단위 : 달러)

- 기기 유형별

- 에너지 기반 기기

- 레이저 기반

- 광 기반(IPL)

- 고주파 기반

- 초음파 기반

- 저온 지방분해와 플라즈마 및 기반

- 비에너지 기반 기기

- 보툴리눔툭신(보톡스)

- 피부 필러&스레드

- 화학적 필링

- 미세 박피술

- 임플란트

- 메조테라피 및 기타

- 에너지 기반 기기

- 용도별

- 피부 재생 및 탄력 개선

- 바디 컨투어링 및 셀룰라이트 감소

- 탈모

- 문신 및 색소 침착 제거

- 유방

- 여드름 및 흉터 치료

- 기타 용도

- 최종 사용자별

- 병원

- 피부과 및 미용 클리닉

- 메디컬 및 스파

- 가정용

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- AbbVie(Allergan Aesthetics)

- Alma Lasers(Sisram Medical)

- Cutera Inc.

- Bausch Lomb(Solta Medical)

- Galderma SA

- Hologic Inc.(Cynosure)

- Lumenis

- Lutronic Corporation

- Candela Medical

- Venus Concept

- InMode Ltd.

- Fotona

- Sciton Inc.

- BTL Aesthetics

- Zimmer Aesthetics

- Apyx Medical

- WonTech

- Straumann Group(botiss aesthetics)

- Sinclair Pharma

- Laboratorios Leti

제7장 시장 기회와 전망

HBR 25.11.10The Spain Aesthetic Devices Market size is estimated at USD 233.72 million in 2025, and is expected to reach USD 429.29 million by 2030, at a CAGR of 12.94% during the forecast period (2025-2030).

Persistent demand for sophisticated, minimally invasive procedures anchors this trajectory, helped by 400,000 cosmetic interventions performed in the country every year. Recent regulatory tightening that limits invasive surgeries to board-certified plastic surgeons is concentrating procedure volumes in high-quality facilities, encouraging clinics to acquire compliant, premium equipment. Parallel advances in energy-based platforms, artificial intelligence-guided imaging, and home-use technologies are broadening the user base while improving treatment outcomes, reinforcing the long-term growth outlook for the Spain aesthetic devices market.

Spain Aesthetic Devices Market Trends and Insights

Aging Population & Youthful-Appearance Demand

Spain's median age continues to inch upward, yet cosmetic consciousness is rising in parallel, pushing the 45-65 cohort toward non-surgical tightening and resurfacing options. Energy-based modalities that stimulate collagen, such as micro-focused ultrasound with visualization, fit this preference by delivering visible yet discreet results. Uptake is further reinforced by 3D skin-mapping systems that provide precise pre-treatment assessments, a feature embraced by quality-oriented consumers in Madrid and Barcelona. Hospitals and large clinic groups continue to market these procedures as preventive rather than corrective, lengthening patient lifecycles. As demographic momentum endures, so does the baseline demand floor for the Spain aesthetic devices market.

Rising Medical Tourism in Cosmetic Procedures

Spain's accession to the EU cross-border healthcare directive through Real Decreto 81/2014 smooths reimbursement for intra-EU patients, making the country a logical destination for elective aesthetics. The September 2024 rule that confines cosmetic surgery to board-certified plastic surgeons has paradoxically improved the nation's brand by signaling strict safety oversight. Clinics in Valencia and Malaga now bundle accommodation with HIFU-based body-contouring packages, leveraging coastal appeal to foreign visitors. High patient satisfaction ratings feed digital word-of-mouth, reinforcing a virtuous inflow cycle that elevates procedure volumes and equipment replacement needs across the Spain aesthetic devices market.

Limited Insurance Coverage for Cosmetic Procedures

Public insurance excludes elective aesthetics, obliging patients to self-fund expensive treatments. Average out-of-court settlements for cosmetic-related claims exceed EUR 33,000, illustrating the financial stakes involved. Because device amortization costs are rolled into procedure pricing, clinics must keep utilization high to remain profitable, raising affordability barriers for middle-income groups. The legal framework under Ley 29/2006 mandates rigorous proof of safety and efficacy, driving up manufacturer compliance costs that, again, echo down to consumers. Although consumer-grade light-therapy masks and handheld RF tools are proliferating, professional equipment remains inaccessible to many Spaniards outside major cities.

Other drivers and restraints analyzed in the detailed report include:

- Growing Popularity of Minimally Invasive Treatments

- Technological Advances in Aesthetic Devices

- Shortage of Certified Aesthetic Professionals in Rural Areas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Energy-based equipment accounted for 59.64% of Spain aesthetic devices market share in 2024 as lasers, radiofrequency, and ultrasound platforms proved versatile across multiple indications. Ultrasound-based systems are forecast to log a 16.35% CAGR through 2030, propelled by high-intensity focused ultrasound procedures that now extend to scalp rejuvenation protocols validated for androgenetic alopecia treatment.

Laser manufacturers are commercializing 1726 nm devices with real-time thermal imaging that achieve durable acne clearance without pigmentary complications. Temperature-controlled RF microneedling platforms record 86.7% patient satisfaction in clinical trials, keeping radiofrequency relevant even as lasers evolve. Non-energy alternatives such as fillers maintain share through improved rheology and tighter AEMPS oversight, while chemical peels enjoy a niche revival as cost-effective adjuncts. Microneedle rollers now fall under Class IIa rules, prompting clinics to adopt safer cartridge-based systems. Collectively, these trends ensure that the Spain aesthetic devices market continues to favor energy platforms while leaving space for targeted innovation in adjunct categories.

The Spain Aesthetic Devices Market Report is Segmented by Device Type (Energy-Based Devices, Non-Energy-Based Devices), Application (Skin Resurfacing & Tightening, Body Contouring & Cellulite Reduction, Hair Removal, Tattoo & Pigmentation Removal, Breast Augmentation, Acne & Scar Treatment, Other Applications), End User (Hospitals, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- AbbVie (Allergan Aesthetics)

- Alma Lasers (Sisram Medical)

- Cutera

- Bausch + Lomb (Solta Medical)

- Galderma

- Hologic

- Lumenis

- Lutronic

- Candela Medical

- Venus Concept

- InMode Ltd.

- Fotona

- Sciton

- BTL

- Zimmer Aesthetics

- Apyx Medical

- WonTech

- Straumann Group (botiss aesthetics)

- Sinclair Pharma

- Laboratorios Leti

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population & Youthful Appearance Demand

- 4.2.2 Rising Medical Tourism in Cosmetic Procedures

- 4.2.3 Growing Popularity of Minimally-Invasive Treatments

- 4.2.4 Technological Advancements in Aesthetic Devices

- 4.2.5 Cultural Emphasis on Beauty & Wellness

- 4.2.6 Expanding Private Aesthetic Clinics in Urban Centers

- 4.3 Market Restraints

- 4.3.1 Limited Insurance Coverage for Cosmetic Procedures

- 4.3.2 Shortage of Certified Aesthetic Professionals in Rural Areas

- 4.3.3 Stringent EU Regulatory Oversight on Devices & Fillers

- 4.3.4 Economic Sensitivity of Elective Procedures

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Device Type

- 5.1.1 Energy-based Devices

- 5.1.1.1 Laser-based

- 5.1.1.2 Light-based (IPL)

- 5.1.1.3 Radio-frequency-based

- 5.1.1.4 Ultrasound-based

- 5.1.1.5 Cryolipolysis & Plasma-based

- 5.1.2 Non-energy-based Devices

- 5.1.2.1 Botulinum Toxin

- 5.1.2.2 Dermal Fillers & Threads

- 5.1.2.3 Chemical Peels

- 5.1.2.4 Microdermabrasion

- 5.1.2.5 Implants

- 5.1.2.6 Mesotherapy & Others

- 5.1.1 Energy-based Devices

- 5.2 By Application

- 5.2.1 Skin Resurfacing & Tightening

- 5.2.2 Body Contouring & Cellulite Reduction

- 5.2.3 Hair Removal

- 5.2.4 Tattoo & Pigmentation Removal

- 5.2.5 Breast Augmentation

- 5.2.6 Acne & Scar Treatment

- 5.2.7 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Dermatology & Cosmetic Clinics

- 5.3.3 Medical Spas

- 5.3.4 Home-use Settings

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie (Allergan Aesthetics)

- 6.3.2 Alma Lasers (Sisram Medical)

- 6.3.3 Cutera Inc.

- 6.3.4 Bausch + Lomb (Solta Medical)

- 6.3.5 Galderma SA

- 6.3.6 Hologic Inc. (Cynosure)

- 6.3.7 Lumenis

- 6.3.8 Lutronic Corporation

- 6.3.9 Candela Medical

- 6.3.10 Venus Concept

- 6.3.11 InMode Ltd.

- 6.3.12 Fotona

- 6.3.13 Sciton Inc.

- 6.3.14 BTL Aesthetics

- 6.3.15 Zimmer Aesthetics

- 6.3.16 Apyx Medical

- 6.3.17 WonTech

- 6.3.18 Straumann Group (botiss aesthetics)

- 6.3.19 Sinclair Pharma

- 6.3.20 Laboratorios Leti

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment