|

시장보고서

상품코드

1848138

능동 이식형 의료기기 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Active Implantable Medical Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

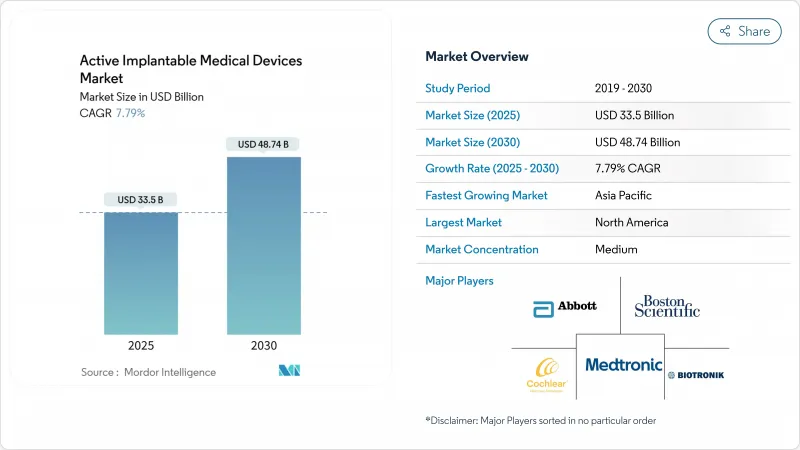

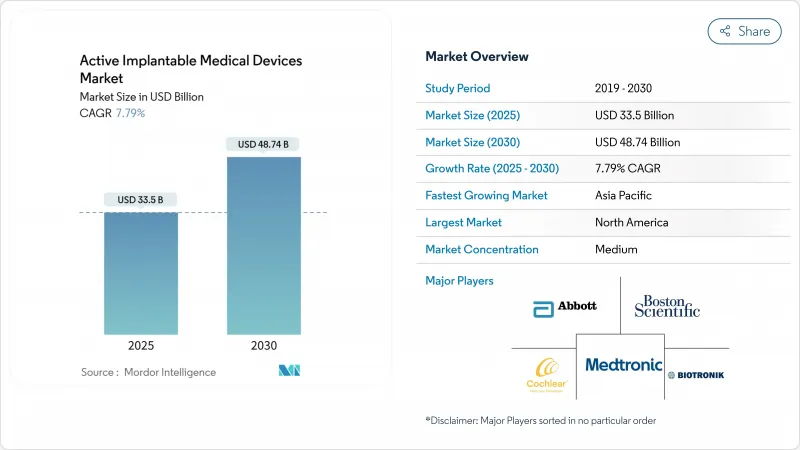

능동 이식형 의료기기 시장 규모는 2025년에 335억 달러로 추정되고, 2030년에는 487억 4,000만 달러에 달할 것으로 예측되며, CAGR 7.79%로 성장이 전망됩니다.

평균 수명 연장, 전자기기의 급속한 소형화, 상환 프레임워크의 확대에 의해 기술 채용 사이클이 단축되는 한편, 환자의 적격성이 확대되고 있습니다. AI를 활용한 원격 모니터링의 도입으로 심장 오류 경고를 최대 85% 줄이고, 임상의의 부담을 줄이며 장기적인 장비 사용에 대한 신뢰를 높였습니다. 이와 병행하여 EU 의료기기 규제(MDR)는 2027년 12월까지 클래스 III 임플란트의 이행 기한을 연장하여 강력한 품질 시스템을 갖춘 제조업체에 수요를 유도하고 있습니다. 2024년 공급 부족 후 반도체 공급망의 안정화로 리드리스 및 무선 아키텍처에 필수적인 서브센티미터 부품 생산이 회복되고 있습니다. 이러한 역학이 결합되어 능동 이식형 의료기기 시장은 2030년까지 꾸준한 확대 궤도를 그릴 수 있습니다.

세계의 능동 이식형 의료기기 시장 동향 및 인사이트

심장 질환, 신경 질환, 귀 질환의 유병률 상승

심부전은 세계에서 6,400만 명 이상에 영향을 주고 심방세동은 2030년까지 선진국 시장에서 1,790만 증례에 이를 것으로 예측되며, 이식형 제세동기 및 재동기 장치 수요가 높아지고 있습니다. 파킨슨병은 세계 약 1,000만 명의 환자가 앓고 있으며 실시간으로 치료법을 조정하는 적응형 뇌심부 자극 시스템의 채용에 박차를 가하고 있습니다. WHO는 2050년까지 7억 명의 사람들이 청력 상실을 겪을 것으로 예상하고 있으며, 이러한 동향은 완전 내장형 설계가 미용 장벽을 제거함에 따라 인공 내이의 사용을 가속화하고 있습니다. 병존 질환 프로파일도 보편화되고 있으며, 여러 장치의 임베딩을 촉진하고 능동 이식형 의료기기 시장의 지속적인 성장을 지원하고 있습니다.

급속한 소형화 및 MRI로 안전한 리드리스 설계 혁신

Abbot의 AVEIR 듀얼 챔버 시스템과 같은 장치는 경정맥 리드없이 방실 페이싱을 동기화합니다. MRI 프로토콜은 조건부에서 3 테슬라에서 완전한 무제한 스캔으로 진보되었으며, 장치 환자를 위한 오랜 영상 진단 장벽이 제거되었습니다. Precision Neuro Science의 레이어 7 피질 인터페이스는 1,024개의 얇은 전극을 갖추고 있으며, 현재 실현 가능한 미세 가공을 예시하고 있습니다. 치료 완료 후 용해되는 생체 재흡수 페이스메이커는 최초의 인간에서의 실현 가능성 시험을 완료하고 적출 수술이 불필요하게 되는 미래를 시사하고 있습니다. 이러한 진보는 감염 위험을 줄이고, 절차를 단순화하며, 환자 선택의 폭을 넓히고, 능동 이식형 의료기기 시장의 기세를 강화하고 있습니다.

신흥 시장에서 고가의 장비 및 기술 비용

많은 중저소득 지역에서는 임플란트의 가격이 여전히 가구연수를 상회하고 있으며, 보급은 도시의 부유층에 한정되어 있습니다. 이러한 경제권에서는 기본적인 진단을 받을 수 있는 주민의 비율은 불과 19%에 불과해 전신적인 의료격차가 부각되고 있습니다. 화폐 가격은 하드 캘린시에서 판매되는 의료기기의 수입 비용을 더욱 상승시키고, 단편적인 보험 적용으로 대부분의 지불이 자기부담이 됩니다. 인도와 브라질의 현지 제조 정책에는 세제 우대 조치가 있지만 고위험 임플란트 카테고리에는 전문 클린룸 제조 및 지적 재산 포트폴리오가 필요하며 국내 기업이 거의 보유하지 않습니다. 임플란트 치료에는 전기 생리학자와 이비인후과 외과의사가 필요하지만, 이들은 여전히 기간 병원에 집중되어 있기 때문에 트레이닝 부족이 장벽을 더욱 향상시키고 있습니다. 자금 조달 모델이 성숙할 때까지 비용은 많은 신흥 지역의 능동 이식형 의료기기 시장에 계속 캡처할 것으로 보입니다.

부문 분석

이식형 제세동기는 미국의 심부전 환자 약 600만 명의 심장 돌연사 예방에 있어서 구명적 역할에 의해 2024년의 능동 이식형 의료기기 시장 규모의 31.23%를 차지했습니다. 피하형 및 리드리스형은 감염 위험을 줄이고 MRI 액세스를 가능하게 하므로 안정적인 교환 주기를 유지할 수 있습니다. 심박 조율기는 듀얼 챔버 리드리스 설계를 통해 경정맥 리드 없이 복잡한 부정맥을 수정할 수 있게 되었기 때문에 관련성을 유지하고 있습니다. 보조 인공 심장은 자기 부상 펌프에 의해 혈전증이 감소하고 2년 생존율이 전세대에 비해 2배가 되었습니다.

이식형 보청기는 2030년까지 연평균 복합 성장률(CAGR)이 9.43%로 가장 빠른 성장률을 나타내며 완전 이식형 인공 내이가 중요한 임상시험에 들어가 외부 프로세서 없이 24시간 소리를 들을 수 있게 됩니다. 메드엘의 TICI 가용성 연구의 초기 데이터는 표준 모델과 동등한 음성 인식 능력과 더 높은 환자 만족도를 보여줍니다. 또한, 신경자극장치는 과잉자극을 89% 차단하는 클로즈드 루프 기능으로부터 혜택을 받고, 삽입형 루프 레코더와 약제 주입 펌프는 개별화된 만성 질환 관리로부터 혜택을 받습니다. 이러한 역학은 제품의 다양성을 높이고 능동 이식형 의료기기 시장 전망를 지원하고 있습니다.

심혈관 질환은 심부전 유병률의 상승과 전도계 페이싱 및 재동기의 적응 확대에 의해 2024년 능동 이식형 의료기기 시장 규모의 55.34%를 차지합니다. Abbot의 TriClip은 중등도 이상의 삼첨판 역류를 84% 감소시켜 Kansas City Cardiomyopathy Questionnaire 점수를 개선했습니다. 적응성 깊은 뇌 자극으로 인해 이전에는 난치성이었던 파킨슨병의 하위 유형에도 임상적 이익이 확대되었기 때문에 신경학적 용도는 견조하게 추이하고 있습니다.

난청 치료는 2030년까지 연평균 복합 성장률(CAGR) 10.67%로 성장할 전망이고, WHO가 7억 명의 난청 환자를 예측하고 있으며, 완전 임베디드 솔루션이 수년간 스티그마를 닦습니다. 만성 통증 관리는 복용량을 자동으로 조정하고 오피오이드에 대한 의존도를 줄이는 AI 구동 척수 자극 장치의 채택을 증가시킵니다. 폐쇄 루프 인슐린 전달과 같은 내분비 이용 사례는 능동 이식형 의료기기 시장에 새로운 볼륨을 주입할 수 있는 새로운 인접 영역을 보여줍니다.

지역 분석

북미는 2024년 매출의 38.54%를 차지하였고, 브레이크스루 디바이스의 메디케어 적용 및 학계, 산업계, 벤처 캐피탈을 연결하는 에코시스템의 밀도가 높은 것이 요인이 되고 있습니다. FDA의 브레이크스루 디바이스 패스웨이는 심장 및 신경 디바이스의 승인을 평균 150일 이내에 단축시켜 임상가의 신속한 도입을 가능하게 했습니다. 견고한 상환 제도와 확립된 소개 네트워크가 리드 리스페이싱과 적응형 DBS 시스템의 높은 기술을 지원하고 있습니다. 그러나 가치 기반 지불 이니셔티브는 장기적인 비용 상쇄를 증명하기 위해 공급업체에 압력을 가하고 있으며, 능동 이식형 의료기기 시장의 가격 구조를 재구성할 수 있는 위험 분담 계약의 도래를 알리고 있습니다.

아시아태평양은 중국의 VoBP 비용 재설정과 2017년 이후 270개의 혁신적인 임플란트 국가 의료 제품국의 승인 가속으로 2025-2030년 연평균 복합 성장률(CAGR) 8.76%로 성장합니다. 일본의 초고령화 사회는 작고 수명이 긴 기기에 대한 수요를 부추겼으며, 한국의 고급 제조 능력은 한국을 주요 수출 허브에 자리잡고 있습니다. 인도의 생산 연동형 장려금 제도는 세계 OEM을 현지 최종 조립에 끌어들여 물류 비용을 절감하고 보다 광범위한 지역 접근을 지원하고 있습니다. 이러한 변화는 아시아태평양의 능동 이식형 의료기기 시장에서 가중치를 높이고 세계 공급업체에 규모 효율성을 제공합니다.

유럽은 MDR 이행의 병목을 극복하고 인증 취득을 늦추면서도 결국에는 증거 표준의 조화를 도모하고 있습니다. 독일은 여전히 전기 생리학의 강국이며 프랑스의 디지털 건강 상환의 틀은 AI 연동 임플란트의 인센티브입니다. 브렉시트는 영국의 승인 경로를 병렬로 추가하여 두 지역 출시 계획을 복잡하게 합니다. 그럼에도 불구하고 대륙의 고령화 인구통계 및 국민 모두 보험제도는 여전히 안정적인 장비 수요를 보장하고 있습니다. 노티파이드 바디의 용량이 정상화되면 승인을 기다리는 신제품이 출시되어 능동 이식형 의료기기 시장에서 유럽의 지위가 강화될 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 심장, 신경, 이비과 질환의 유병률 상승

- 급속한 소형화와 MRI 대응 및 납 프리 설계의 혁신

- 고령화 사회에서의 임플란트 적응자의 확대

- OECD 국가와 중국 보험 상환 제도의 호조 확대

- AI를 활용한 원격 모니터링 알고리즘이 현실 세계의 성과 향상

- 획기적인 생체 흡수성 일렉트로닉스로 임플란트 적출 수술 불필요해짐

- 시장 성장 억제요인

- 신흥 시장에서의 의료기기 및 처치의 고비용

- 엄격한 사이버 보안 및 규제 상 장애물이 승인 장기화

- 초소형 부품의 반도체 공급 병목

- 리튬 요오드 화학에서 배터리 재료의 지속가능성에 대한 압력

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 페이스메이커

- 이식형 제세동기(ICD)

- 심실 보조 장치(VAD)

- 신경 자극 장치

- 척수 자극 장치

- 뇌심부 자극 장치

- 미주 신경 자극 장치

- 천골신경 자극 장치

- 이식형 보청기

- 인공 내이

- 골전도 보청 시스템

- 삽입형 루프 레코더

- 이식형 약제 주입 펌프

- 용도별

- 심혈관 질환

- 신경질환

- 난청

- 만성 통증 관리

- 내분비 및 대사(예 : 당뇨병)

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 전문의 및 이비인후과 클리닉

- 재택 케어의 설정

- 기술별

- MRI 대응 디바이스

- 종래의 디바이스

- 리드리스 및 무선 임플란트

- 충전식 및 생체 흡수성 파워 시스템

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Medtronic plc

- Abbott Laboratories

- Boston Scientific Corporation

- Cochlear Limited

- BIOTRONIK SE & Co. KG

- LivaNova PLC

- Nevro Corp

- Axonics Inc.

- Inspire Medical Systems

- Sonova(Advanced Bionics)

- MED-EL

- MicroPort CRM

- Terumo

- Abiomed

- Jarvik Heart Inc.

- Biotronik Neuro

- BlueWind Medical

- CVRx Inc.

- Shenzhen Mindray

- Lepu Medical

제7장 시장 기회 및 향후 전망

AJY 25.11.03The active implantable medical devices market size generated USD 33.50 billion in 2025 and is projected to reach USD 48.74 billion by 2030, translating to a 7.79% CAGR.

Rising life expectancy, rapid miniaturization of electronics, and expanding reimbursement frameworks are widening patient eligibility while shortening technology-adoption cycles. The uptake of AI-enabled remote monitoring has cut false cardiac alerts by up to 85%, easing clinician workload and increasing confidence in long-term device use. In parallel, the EU Medical Device Regulation (MDR) has extended transition deadlines to December 2027 for Class III implants, channeling demand toward manufacturers with strong quality systems. Stabilization of the semiconductor supply chain after 2024 shortages is restoring production of sub-centimeter components essential for leadless and wireless architectures. Together, these dynamics reinforce a steady scale-up trajectory for the Active implantable medical devices market through 2030.

Global Active Implantable Medical Devices Market Trends and Insights

Rising Prevalence of Cardio-, Neuro- & Otologic Disorders

Heart failure impacts more than 64 million people worldwide and atrial fibrillation is expected to reach 17.9 million cases in developed markets by 2030, intensifying demand for implantable cardioverter-defibrillators and resynchronization devices. Parkinson's disease affects around 10 million patients globally, spurring adoption of adaptive deep-brain stimulation systems that modulate therapy in real time. WHO forecasts that hearing loss will affect 700 million people by 2050, a trend accelerating cochlear-implant usage as fully implantable designs erase cosmetic barriers. Co-morbid disease profiles are also becoming more common, prompting multi-device implantation and underpinning sustained growth in the Active implantable medical devices market.

Rapid Miniaturization & MRI-Safe Leadless Design Innovations

Leadless pacemakers have shrunk to volumes below 1 cm3 while retaining 10-year battery life, and devices like Abbott's AVEIR dual-chamber system synchronize atrioventricular pacing without transvenous leads. MRI protocols have progressed from conditional to fully unrestricted scanning at 3 Tesla, removing long-standing imaging barriers for device patients. Precision Neuroscience's Layer 7 cortical interface, hosting 1,024 hair-thin electrodes, exemplifies the fine-scale fabrication now achievable. Bio-resorbable pacemakers that dissolve after therapy completion have completed first-in-human feasibility trials, hinting at a future where explant surgery becomes unnecessary. These advances lower infection risks, simplify procedures, and widen patient selection, strengthening momentum in the Active implantable medical devices market.

High Device & Procedure Cost in Emerging Markets

In many low- and middle-income regions, implant prices still exceed annual household income, limiting penetration to wealthy urban populations. Only 19% of residents in these economies have access even to basic diagnostics, highlighting systemic care gaps. Currency depreciation further inflates import costs for devices priced in hard currencies, while fragmented insurance coverage pushes most payments out of pocket. Local manufacturing policies in India and Brazil offer tax incentives, yet high-risk implant categories require specialized cleanroom production and intellectual property portfolios that few domestic firms possess. Training deficits compound the barrier, as implant procedures demand electrophysiologists and otologic surgeons who remain concentrated in flagship hospitals. Until financing models mature, cost will continue to cap the Active implantable medical devices market in numerous emerging territories.

Other drivers and restraints analyzed in the detailed report include:

- Ageing Population Expanding Implant-Eligible Pool

- Favourable Reimbursement Expansion in OECD & China

- Stringent Cybersecurity & Regulatory Hurdles Lengthen Approvals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Implantable cardioverter-defibrillators captured a 31.23% slice of the Active implantable medical devices market size in 2024 thanks to their life-saving role in sudden-cardiac-death prevention among roughly 6 million US heart-failure patients. Subcutaneous and leadless formats reduce infection risk and enable MRI access, sustaining steady replacement cycles. Pacemakers stay relevant because dual-chamber leadless designs now correct complex arrhythmias without transvenous leads. Ventricular assist devices profit from magnetically levitated pumps that cut thrombosis, doubling two-year survival compared with previous generations.

Implantable hearing devices post the fastest trajectory at a 9.43% CAGR through 2030 as totally implantable cochlear implants enter pivotal trials and promise round-the-clock sound without external processors. Early data from MED-EL's TICI feasibility study showed speech-recognition parity with standard models and higher patient satisfaction. Neurostimulators also benefit from closed-loop capabilities that cut overstimulation by 89%, while insertable loop recorders and drug-infusion pumps gain from personalized chronic-disease management. These dynamics collectively deepen product diversity and future-proof the Active implantable medical devices market.

Cardiovascular disorders retained 55.34% of the Active implantable medical devices market size in 2024 driven by escalating heart-failure prevalence and broadening indications for conduction-system pacing and resynchronization. Abbott's TriClip device reduced moderate-or-greater tricuspid regurgitation by 84% and improved Kansas City Cardiomyopathy Questionnaire scores, highlighting structural-heart opportunities. Neurological applications remain steady because adaptive deep-brain stimulation widens clinical benefit to previously refractory Parkinson's subtypes.

Hearing-loss treatment is growing at a 10.67% CAGR to 2030 as WHO projects 700 million affected individuals, and fully implantable solutions erase long-standing stigma. Chronic pain management sees rising adoption of AI-driven spinal cord stimulators that auto-calibrate dosing, reducing opioid reliance. Endocrine use cases, such as closed-loop insulin delivery, represent an emerging adjacency that could inject fresh volume into the Active implantable medical devices market.

The Active Implantable Medical Devices Market Report is Segmented by Product Type (Pacemakers, Implantable Cardioverter-Defibrillators (ICD), and More), Application (Cardiovascular Disorders, Neurological Disorders, and More), Technology (Conventional Devices, and More), (end User (Hospitals, and More), Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 38.54% of 2024 sales, fueled by Medicare coverage of breakthrough devices and a dense ecosystem linking academia, industry, and venture capital. The FDA Breakthrough Device pathway has compressed cardiac and neuro device approvals to under 150 days on average, allowing rapid clinician adoption. Robust reimbursement and established referral networks support high procedural volumes for leadless pacing and adaptive DBS systems. Yet value-based payment initiatives are pressuring suppliers to evidence longitudinal cost offsets, ushering in risk-sharing contracts that could reshape the Active implantable medical devices market's pricing structure.

Asia-Pacific is set to grow at 8.76% CAGR between 2025 and 2030 thanks to China's VoBP cost resets and accelerated National Medical Products Administration approvals of 270 innovative implants since 2017. Japan's super-aged society fuels demand for small, long-life devices, while South Korea's advanced fabrication capacity positions it as a leading export hub. India's Production Linked Incentive scheme is drawing global OEMs to set up local final assembly, trimming logistics costs and supporting broader regional access. These shifts elevate Asia-Pacific's weighting in the Active implantable medical devices market and create scale efficiencies for global suppliers.

Europe is navigating MDR transition bottlenecks that delay certification yet ultimately harmonize evidence standards. Germany remains a powerhouse in electrophysiology, and France's digital-health reimbursement framework incentivizes AI-linked implants. Brexit adds a parallel UK approval pathway, raising planning complexity for dual-region launches. Nonetheless, the continent's ageing demographic and universal coverage still assure steady device demand. Once notified-body capacity normalises, pent-up approvals could yield a release of new products and reinforce Europe's place within the Active implantable medical devices market.

- Medtronic

- Abbott Laboratories

- Boston Scientific

- Cochlear

- BIOTRONIK

- LivaNova

- Nevro

- Axonics Inc.

- Inspire Medical Systems

- Sonova (Advanced Bionics)

- MED-EL

- MicroPort CRM

- Terumo

- Abiomed

- Jarvik Heart

- Biotronik Neuro

- BlueWind Medical

- CVRx Inc.

- Mindray

- Lepu Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Cardio-, Neuro- & Otologic Disorders

- 4.2.2 Rapid Miniaturisation & MRI-Safe/Lead-Less Design Innovations

- 4.2.3 Ageing Population Expanding Implant-Eligible Pool

- 4.2.4 Favourable Reimbursement Expansion in OECD & China

- 4.2.5 AI-Enabled Remote Monitoring Algorithms Improving Real-World Outcomes

- 4.2.6 Breakthrough Bio-Resorbable Electronics Eliminating Explant Surgeries

- 4.3 Market Restraints

- 4.3.1 High Device & Procedure Cost in Emerging Markets

- 4.3.2 Stringent Cyber-Security / Regulatory Hurdles Lengthen Approvals

- 4.3.3 Semiconductor Supply Bottlenecks for Ultra-Miniature Components

- 4.3.4 Battery-Material Sustainability Pressures on Lithium-Iodine Chemistry

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Pacemakers

- 5.1.2 Implantable Cardioverter-Defibrillators (ICD)

- 5.1.3 Ventricular Assist Devices (VAD)

- 5.1.4 Neurostimulators

- 5.1.4.1 Spinal Cord Stimulators

- 5.1.4.2 Deep Brain Stimulators

- 5.1.4.3 Vagus Nerve Stimulators

- 5.1.4.4 Sacral Nerve Stimulators

- 5.1.5 Implantable Hearing Devices

- 5.1.5.1 Cochlear Implants

- 5.1.5.2 Bone-Anchored Hearing Systems

- 5.1.6 Insertable Loop Recorders

- 5.1.7 Implantable Drug-Infusion Pumps

- 5.2 By Application

- 5.2.1 Cardiovascular Disorders

- 5.2.2 Neurological Disorders

- 5.2.3 Hearing Loss

- 5.2.4 Chronic Pain Management

- 5.2.5 Endocrine & Metabolic (e.g., Diabetes)

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgery Centres

- 5.3.3 Specialty & ENT Clinics

- 5.3.4 Home-Care Settings

- 5.4 By Technology

- 5.4.1 MRI-Compatible Devices

- 5.4.2 Conventional Devices

- 5.4.3 Leadless / Wireless Implants

- 5.4.4 Rechargeable / Bio-resorbable Power Systems

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Medtronic plc

- 6.3.2 Abbott Laboratories

- 6.3.3 Boston Scientific Corporation

- 6.3.4 Cochlear Limited

- 6.3.5 BIOTRONIK SE & Co. KG

- 6.3.6 LivaNova PLC

- 6.3.7 Nevro Corp

- 6.3.8 Axonics Inc.

- 6.3.9 Inspire Medical Systems

- 6.3.10 Sonova (Advanced Bionics)

- 6.3.11 MED-EL

- 6.3.12 MicroPort CRM

- 6.3.13 Terumo

- 6.3.14 Abiomed

- 6.3.15 Jarvik Heart Inc.

- 6.3.16 Biotronik Neuro

- 6.3.17 BlueWind Medical

- 6.3.18 CVRx Inc.

- 6.3.19 Shenzhen Mindray

- 6.3.20 Lepu Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment