|

시장보고서

상품코드

1848311

전기영동 시약 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Electrophoresis Reagents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

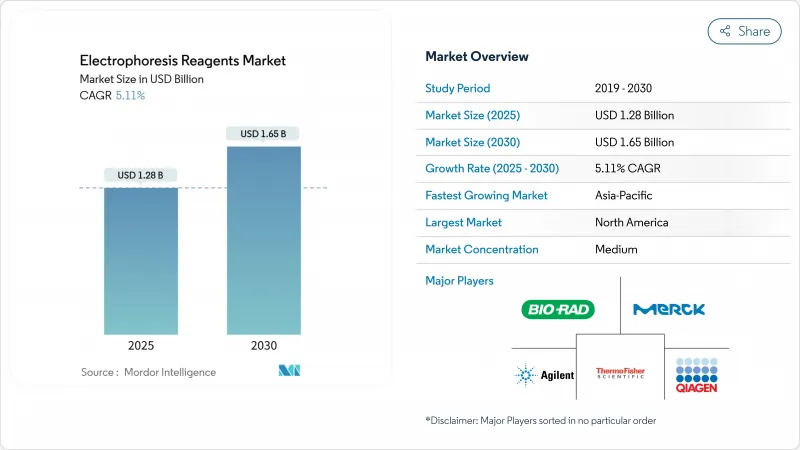

전기영동 시약 시장 규모는 2025년에 12억 8,000만 달러로 추정되고, 2030년에는 16억 5,000만 달러에 이를 것으로 예측되며, CAGR 5.11%로 성장할 전망입니다.

현재 정밀의료로의 장기적인 변화, 규제 감독의 엄격화, 연방 정부 연구비의 지속적인 투입이 수요를 견인하고 있습니다. 미국 식품의약품국의 2024년 5월 임상검사실 개발 시험 규칙은 20년간 5억 6,600만-35억 6,000만 달러의 컴플라이언스 부담을 도입하고 기존 시약 공급업체인 fda.gov 에 유리한 품질 임계값을 높였습니다. 아시아태평양은 최근 벤처 대출 연조에도 불구하고 지역 연구 기지가 확대되고 세계적인 성장 균형을 되찾는 태세가 갖추어져 있습니다. 보다 환경친화적인 염료 채용 증가, AI 대응 겔 분석 통합, 자동화가 진행된 모세관 시스템은 전기영동 시약 시장의 구조적 수요 촉진요인을 더욱 강화합니다.

세계의 전기영동 시약 시장 동향 및 인사이트

유전체 및 단백질체학 조사에 대한 자금 제공 증가

미국 국립위생연구소(National Institutes of Health)는 건강과 질병을 위한 멀티오믹스 컨소시엄(Multi-Omics for Health and Disease Consortium)에 2024년에 5,030만 달러를 할당하고, 신뢰성 높은 바이오마커 검증을 위해 전기영동 시약을 필요로 하는 통합 분석 플랫폼 공적 자금의 확대로 공급업체는 단일 소모품이 아니라 종합적이고 워크플로우에 맞는 제품군을 제공할 수밖에 없었습니다. 민간 기업의 공동 투자는 제약 스폰서가 창약 프로그램에 공적 인프라를 활용함으로써 이러한 추풍을 확대합니다. 현재 2023년 국립 인간 유전체 연구소의 예산의 30%가 컴퓨테셔널 유전체학에 소비되고 있으며, 데이터 집약적인 연구가 알고리즘 파이프라인을 위한 재현가능한 정량적 출력을 생성할 수 있는 고처리량 전기영동 시스템에 얼마나 유리한지를 명확하게 보여주고 있습니다. 이러한 자금제공 모델은 다년간의 연구조성금에 의한 구매로 이어지므로 전기영동 시약 시장 전체 수요 가시성을 높일 것입니다.

만성 질환 증가

고령화 사회로의 세계적인 변화는 진단의 복잡성을 높이고 초기 질병 상태에서 미묘한 단백질체학의 변화를 감지할 수 있는 고해상도 분리 기술을 지원합니다. 모세관 전기영동은 바이오 의약품의 규제 당국 신청에 중요한 요건인 치료 단백질의 전하 변동 분석을 지원합니다. 종양학에서 순환 종양 DNA의 전기영동 분리는 조직 기반 진단을 대체하는 저침습성 액체 생검 분석을 가능하게 하여 환자 1인당 검사 빈도를 증가시킵니다. 신흥국 시장의 예방의료 모델은 단발적인 진단 이벤트를 정기적인 시약 수요로 변환하여 역학적 동향을 그대로 전기영동 시약 시장의 시약량 증가에 반영합니다.

시간이 많이 걸리는 워크플로우 및 수동 겔 준비

폴리아크릴아미드 겔의 캐스트, 샘플의 로드, 런 후의 염색에는 최대 8시간을 필요로 하며, 하이 스루풋 환경에서는 인건비가 가장 큰 변동비가 됩니다. 바이오 래드의 Stain-Free 겔은 염색 공정을 생략하지만, 비싼 가격 설정과 새로운 장비의 필요성이 예산에 제약이 있는 실험실 채용을 막고 있습니다. 숙련된 기술자의 세계 부족은 워크플로우의 병목 현상을 심화시키고, 조달 팀은 총 소유 비용을 조사하고 대체 기술을 검토하도록 촉구하고 있습니다.

부문 분석

젤은 2024년 전기영동 시약 시장의 43.56%를 차지했으며, DNA, RNA, 단백질 용도 분야의 거의 모든 분리 워크플로우를 지원합니다. 아가로오스는 저비용으로 주조가 용이하기 때문에 핵산 분석의 스테디셀러이며, 폴리아크릴아미드는 고분해능의 단백질 작업을 지원하고 있습니다. 염료 매출은 작지만, 에티듐-브로마이드의 대체품이 규제 당국의 지지를 얻어 전기영동 시약 시장을 재형성함에 따라 CAGR 7.88%로 상승합니다. 2024년에 발표된 96-웰 폴리아크릴아미드 프로토타입은 트랜스퍼 호환이 가능한 수평 동시 전기영동을 입증하여 미래의 다중 샘플 메인스트림을 제공할 것을 제안합니다. Tris/아세테이트/EDTA와 같은 완충액 시스템은 성능과 비용 안정성이 독자적인 개선으로 인한 증가 이익을 능가하기 때문에 여전히 업계 표준으로 자리잡고 있습니다. 동시에 Biotium의 One-Step Lumitein 시리즈와 같은 새로운 염료 플랫폼은 겔 매트릭스에 직접 염색을 통합하고 세척 단계를 제거하고 프로토콜을 단축합니다.

지역 분석

북미는 2024년 전기영동 시약 시장 매출의 40.11%를 차지했으며, 강력한 NIH 자금과 밀집된 의약품 제조 거점에 지지를 받고 있습니다. 1,540만 달러의 NIH-NSF RNA 연구 프로그램은 거시 경제의 변동에 관계없이 시약 소비를 유지하는 공적 자금 메커니즘을 보여줍니다. Thermofisher의 2029년까지의 20억 달러의 국내 투자는 세액 공제와 리쇼어링 인센티브를 예측한 온쇼어 제조 및 연구개발 능력 확대에 대한 공급업체의 헌신을 강조합니다. 유럽은 성숙하면서도 규제가 많은 지역임에 변함이 없으며, 기업 지속가능성 듀 딜리전스 지령은 유해화학물질의 대체를 가속화하여 보다 환경친화적인 제제 수요를 촉진합니다. 칼 로스의 재생 용제와 바이오 에탄올의 제품 라인인 'SOLVAGREEN'은 유럽의 벤더가 포트폴리오를 규제 공약에 맞추는 방법을 보여줍니다.

아시아태평양은 2030년까지 CAGR 6.45%로 성장이 예측되어 가장 급성장이 전망되는 서브 시장입니다. 2021년 이후 벤처파이낸스가 22% 감소했음에도 불구하고 정부의 생명과학 예산이 증가하고 바이오의약품 생산 능력이 확대되고 있는 것이 그 요인입니다. 중국의 국내 설비 보조금과 인도의 생산 연동형 인센티브는 자본 지출을 지역 공급업체에 추가로 기울이지만 지적 재산과 공급망 안보에 대한 우려는 다국적 기업들에게 합작 투자와 현지 제조 지점의 추구를 촉구합니다. QIAGEN의 리야드 기지 설립과 사우디아라비아 보건부와의 각서는 중동 정부가 분자진단 생태계를 구축하기 위해 전략적 파트너십을 어떻게 활용하고 있는지를 밝혔습니다. 아프리카와 남미는 여전히 공헌도가 낮습니다. 기증자와 정부의 보건 프로그램을 목표로 하는 것은 부드러운 성장 궤도를 그리는 것이 아니라 일시적인 시약의 급증을 일으키고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 유전체 프로테옴 조사에 대한 자금 제공 확대

- 만성질환 유병률 상승

- 하이 스루풋 전기 영동에서 기술의 진보

- 맞춤형 의료의 도입 확대

- 포인트 오브 케어 분자 검사용 랩 온칩 시약 키트

- 보다 환경친화적이고 독성이 없는 염료 및 완충제로의 전환(ESG 주도)

- 시장 성장 억제요인

- 시간이 걸리는 워크플로우와 수동 겔 준비

- 대체 분리 기술의 가용성

- 아크릴 아미드 원료 부족으로 시약 가격 상승

- 에티듐 브로마이드계 염료의 엄격한 폐기 규칙

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품별

- 겔

- 아가로스 겔

- 폴리아크릴아미드겔

- 전분 젤

- 염료

- 에티듐 브로마이드(EtBr)

- 브로모페놀 블루

- SYBR 염료

- 기타 염료

- 버퍼

- 트리스/아세트산/EDTA

- 트리스/붕산/EDTA

- 기타 버퍼

- 기타 제품

- 겔

- 기술별

- 겔 전기영동

- 모세관 전기영동

- 최종 사용자별

- 학술연구기관

- 제약 및 바이오테크놀러지 기업

- 임상 및 진단 실험실

- 기타 최종 사용자

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Agilent Technologies Inc.

- Analytik Jena GmbH

- BioAtlas

- Bio-Rad Laboratories Inc.

- Cleaver Scientific Ltd.

- Cytiva(Danaher)

- Greiner Bio-One GmbH

- Helena Laboratories Corp.

- Hoefer Inc.(Harvard Bioscience)

- Labnet International Inc.

- Lonza Group AG

- Merck KGaA/Sigma-Aldrich

- New England Biolabs Inc.

- NIPPON Genetics Co., Ltd.

- PerkinElmer Inc.

- Promega Corporation

- Qiagen NV

- Randox Laboratories Ltd.

- Sebia Group

- SERVA Electrophoresis GmbH

- Takara Bio Inc.

- Thermo Fisher Scientific Inc.

제7장 시장 기회 및 향후 전망

AJY 25.11.03The electrophoresis reagents market size is valued at USD 1.28 billion in 2025 and is forecast to reach USD 1.65 billion by 2030, advancing at a 5.11% CAGR.

Demand is now driven by long-term shifts toward precision medicine, stricter regulatory oversight, and sustained federal research funding. The United States Food and Drug Administration's May 2024 laboratory-developed-test rule introduced a USD 566 million-USD 3.56 billion compliance burden over two decades, elevating quality thresholds that favor established reagent suppliers fda.gov. Asia-Pacific is poised to rebalance global growth as regional research hubs expand despite recent venture-financing softness. Rising adoption of greener stains, integration of AI-enabled gel analytics, and automation-heavy capillary systems further reinforce structural demand drivers for the electrophoresis reagents market.

Global Electrophoresis Reagents Market Trends and Insights

Increasing Funding for Genomic & Proteomic Research

The National Institutes of Health allocated USD 50.3 million in 2024 to its Multi-Omics for Health and Disease Consortium, signaling a sustained preference for integrated analytical platforms that require electrophoresis reagents for reliable biomarker validation. Expanded public funding compels suppliers to offer comprehensive, workflow-compatible product suites instead of stand-alone consumables. Private-sector co-investment magnifies these tailwinds, as pharmaceutical sponsors leverage public infrastructure for drug-discovery programs. Computational genomics now consumes 30% of the National Human Genome Research Institute's FY2023 budget, underscoring how data-intensive research favors high-throughput electrophoresis systems capable of generating reproducible quantitative outputs for algorithmic pipelines. Together, these funding models lengthen demand visibility across the electrophoresis reagents market by anchoring purchases to multiyear research grants.

Rising Prevalence of Chronic Diseases

The global shift toward aging populations elevates diagnostic complexity, favoring high-resolution separation techniques that can detect subtle proteomic variations in early disease states. Capillary electrophoresis supports charge-variant analysis of therapeutic proteins, a critical requirement in regulatory submissions for biopharmaceuticals. In oncology, electrophoretic separation of circulating tumor DNA enables minimally invasive liquid-biopsy assays that replace tissue-based diagnostics, thereby increasing test frequency per patient episode. Preventive-care models in developed markets convert one-off diagnostic events into recurring reagent demand, translating epidemiological trends directly into higher reagent volumes for the electrophoresis reagents market.

Time-consuming workflows & manual gel preparation

Casting polyacrylamide gels, loading samples, and post-run staining can require up to 8 hours, making labor the most significant variable cost in high-throughput environments. Bio-Rad's Stain-Free gels remove the staining step, but premium pricing and new-equipment needs deter adoption in budget-constrained labs. Global shortages of skilled technicians intensify workflow bottlenecks, prompting procurement teams to scrutinize total-cost-of-ownership and consider alternative technologies.

Other drivers and restraints analyzed in the detailed report include:

- Growing adoption of personalized medicine

- Lab-on-a-chip reagent kits for point-of-care molecular testing

- Availability of alternative separation technologies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gels accounted for 43.56% of the electrophoresis reagents market in 2024, underpinning virtually every separation workflow across DNA, RNA, and protein applications. Agarose remains a staple for nucleic-acid analysis thanks to low cost and straightforward casting, whereas polyacrylamide supports high-resolution protein work. Dye sales, though smaller, are set to climb at a 7.88% CAGR as ethidium-bromide replacements gain regulatory traction, reshaping the electrophoresis reagents market. Suppliers are differentiating gels through throughput-oriented formats; a 96-well polyacrylamide prototype published in 2024 demonstrated simultaneous horizontal electrophoresis with transfer compatibility, hinting at future multi-sample mainstream offerings. Buffer systems such as Tris/Acetate/EDTA remain entrenched industry standards because performance and cost stability outweigh incremental gains from proprietary modifications. Concurrently, newer dye platforms like Biotium's One-Step Lumitein series integrate staining directly into gel matrices, removing wash steps and shortening protocols-a direct response to labor-shortage challenges.

The Electrophoresis Reagents Market Report is Segmented by Product (Gel, Dyes, Buffers, and Other Products), Technique (Gel Electrophoresis and Capillary Electrophoresis), End User (Academic & Research Institutions, Pharmaceutical & Biotechnology Companies, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 40.11% of 2024 revenue for the electrophoresis reagents market, anchored by robust NIH funding and a dense pharmaceutical manufacturing base. The USD 15.4 million NIH-NSF RNA research program exemplifies the public-funding mechanism that sustains reagent consumption irrespective of macroeconomic volatility. Thermo Fisher's USD 2 billion domestic investment through 2029 underscores supplier commitment to on-shore manufacturing and R&D capacity expansion in anticipation of tax credits and reshoring incentives. Europe remains a mature yet regulation-intensive region; the Corporate Sustainability Due Diligence Directive accelerates substitution of hazardous chemicals, driving demand for greener formulations. Carl Roth's SOLVAGREEN line of recycled solvents and bioethanol illustrates how European vendors align portfolios with regulatory commitments.

Asia-Pacific is the fastest-growing sub-market with a 6.45% projected CAGR to 2030, fueled by rising government life-science budgets and expanding biopharmaceutical capacity despite a 22% venture-finance decline since 2021. China's domestic-equipment subsidies and India's production-linked incentives further tilt capital spending toward regional suppliers, though intellectual-property and supply-chain security concerns encourage multinationals to pursue joint ventures or local manufacturing branches. QIAGEN's establishment of a Riyadh hub and its memorandum with the Saudi Ministry of Health reveal how Middle East governments leverage strategic partnerships to build molecular-diagnostics ecosystems. Africa and South America remain smaller contributors; targeted donor and government health programs create episodic reagent spikes rather than smooth growth trajectories.

- Agilent Technologies

- Analytik Jena GmbH

- BioAtlas

- Bio-Rad Laboratories

- Cleaver Scientific Ltd.

- Cytiva

- Greiner Bio-One GmbH

- Helena Laboratories Corp.

- Hoefer Inc. (Harvard Bioscience)

- Labnet International Inc.

- Lonza Group

- Merck KGaA / Sigma-Aldrich

- New England Biolabs

- NIPPON Genetics Co., Ltd.

- PerkinElmer

- Promega

- QIAGEN

- Randox Laboratories

- Sebia

- SERVA Electrophoresis

- Takara Bio

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Funding for Genomic & Proteomic Research

- 4.2.2 Rising Prevalence of Chronic Diseases

- 4.2.3 Technological Advances in High-Throughput Electrophoresis

- 4.2.4 Growing Adoption of Personalized Medicine

- 4.2.5 Lab-On-A-Chip Reagent Kits for Point-Of-Care Molecular Testing

- 4.2.6 Shift Toward Greener, Non-Toxic Dyes & Buffers (ESG-Driven)

- 4.3 Market Restraints

- 4.3.1 Time-Consuming Workflows & Manual Gel Preparation

- 4.3.2 Availability of Alternative Separation Technologies

- 4.3.3 Acrylamide Feedstock Shortages Inflating Reagent Costs

- 4.3.4 Strict Disposal Rules for Ethidium-Bromide-Based Stains

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Gels

- 5.1.1.1 Agarose Gels

- 5.1.1.2 Polyacrylamide Gels

- 5.1.1.3 Starch Gels

- 5.1.2 Dyes

- 5.1.2.1 Ethidium Bromide (EtBr)

- 5.1.2.2 Bromophenol Blue

- 5.1.2.3 SYBR Dyes

- 5.1.2.4 Other Dyes

- 5.1.3 Buffers

- 5.1.3.1 Tris/Acetate/EDTA

- 5.1.3.2 Tris/Borate/EDTA

- 5.1.3.3 Other Buffers

- 5.1.4 Other Products

- 5.1.1 Gels

- 5.2 By Technique

- 5.2.1 Gel Electrophoresis

- 5.2.2 Capillary Electrophoresis

- 5.3 By End User

- 5.3.1 Academic & Research Institutions

- 5.3.2 Pharmaceutical & Biotechnology Companies

- 5.3.3 Clinical & Diagnostic Laboratories

- 5.3.4 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Agilent Technologies Inc.

- 6.3.2 Analytik Jena GmbH

- 6.3.3 BioAtlas

- 6.3.4 Bio-Rad Laboratories Inc.

- 6.3.5 Cleaver Scientific Ltd.

- 6.3.6 Cytiva (Danaher)

- 6.3.7 Greiner Bio-One GmbH

- 6.3.8 Helena Laboratories Corp.

- 6.3.9 Hoefer Inc. (Harvard Bioscience)

- 6.3.10 Labnet International Inc.

- 6.3.11 Lonza Group AG

- 6.3.12 Merck KGaA / Sigma-Aldrich

- 6.3.13 New England Biolabs Inc.

- 6.3.14 NIPPON Genetics Co., Ltd.

- 6.3.15 PerkinElmer Inc.

- 6.3.16 Promega Corporation

- 6.3.17 Qiagen N.V.

- 6.3.18 Randox Laboratories Ltd.

- 6.3.19 Sebia Group

- 6.3.20 SERVA Electrophoresis GmbH

- 6.3.21 Takara Bio Inc.

- 6.3.22 Thermo Fisher Scientific Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment