|

시장보고서

상품코드

1848342

전기 영동 장비 및 소모품 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Electrophoresis Equipment And Supplies - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

전기 영동 장비 및 소모품 시장 규모는 2025년에 22억 2,000만 달러, 2030년에는 28억 2,000만 달러에 이를 것으로 예측되며, 이 기간의 CAGR은 4.86%를 나타낼 전망입니다.

이 성장 궤도는 폭발적이기보다는 오히려 꾸준한 것으로, 경쟁 기술이 급증하는 가운데, 바이오 의약품의 연구 개발, 임상 진단, 규제된 품질 관리 검사가 전기 영동 분리에 의존하고 있는 성숙한 상황을 반영하고 있습니다. 개인화된 의료 프로그램에서는 현재 높은 처리량의 분자 특성 분석이 필요하므로 설비 투자는 탄력성을 유지하고 소모품의 교환 사이클은 견조하게 추이하고 있습니다. 동시에, 생물제제의 제조 기지에서는 단일클론항체의 인프로세스 및 릴리스 시험을 위한 모세관 시스템의 표준화가 진행되고 있으며, 하드웨어, 시약, 분석 소프트웨어를 번들한 통합 플랫폼에 대한 수요가 유지되고 있습니다. 액체 크로마토그래피 질량분석기로부터의 경쟁 압력은 여전히 큰 역풍이지만, 시약의 지속적인 수익, 레거시 공급업체의 설치 기반 이점 및 이 기술의 확립된 규제 경로가 결합되어 전기 영동 장비 및 소모품 시장의 일관된 확장을 지원합니다.

세계의 전기 영동 장비 및 소모품 시장 동향과 인사이트

맞춤형 의료 및 유전체 진단 채택 확대

모세관 전기영동은 PCR 워크플로우와 원활하게 결합하여 낭포성 섬유증 및 헌팅턴병과 같은 질환의 기초가 되는 유전자 변이의 신속한 자동 검출을 실현합니다. Clinical Chemistry and Laboratory Medicine 잡지에 게재된 성능 벤치마크에 따르면 전기영동은 최소한의 작업 시간으로 변화당 수백 샘플을 스크리닝할 수 있는 것으로 확인되어 병원 실험실의 운영 비용을 절감할 수 있습니다. 포인트 오브 케어용 마이크로플루이딕스 장치는 현재 이 능력을 침대 측에 제공하고 컴팩트한 카트리지는 5분 미만으로 분리를 완료하며, 이 방법이 정밀 치료 프로토콜과 관련된다는 것을 강조하고 있습니다.

세계 학술 및 위탁 연구 인프라 확대

인도, 중국, 인도네시아, 나이지리아에서는 정부 자금에 의한 연구소의 증설이 이루어지고 전기영동은 기초적인 교육 및 연구 툴로 자리매김하고 있습니다. 분자생물학 프로그램에 입학자 급증은 기본적인 수평 및 수직 젤 단위와 입문 수준 모세관 시스템의 대량 조달을 일으켰습니다. 계약 연구 기관(CRO)은 전기 영동 분석을 멀티오믹스 서비스 라인에 통합함으로써 이 기세를 전진시켜 지역 허브 전체에서 안정된 소모품의 풀스루를 확보하고 있습니다.

고급 전기 영동 시스템의 높은 자본 비용과 운영 비용

최신 모세관 유전자 분석기의 가격은 7만 5,000-15만 달러입니다. 고분자 매트릭스 및 모세관을 포함한 소모품은 일상적인 사용으로 3년 이내에 최초의 하드웨어 지출을 초과할 수 있습니다. 제안된 분석 수입품에 대한 관세 스케줄은 생명과학 분야 전체의 영업예산에 630억 달러를 올리게 되고, 소규모 연구소는 리프레시 계획을 연기하지 않을 수 없게 됩니다. 고순도 버퍼에서 공급망의 중단은 비용 구조의 부서짐을 돋보이게 하고 자원에 제약이 있는 지역에서는 가격이 채용의 주요 장벽이 됩니다.

부문 분석

시약 및 소모품의 전기 영동 장비 및 소모품 시장 규모는 2024년에 10억 3,000만 달러로 평가되었는데 전체 매출의 46.43%에 해당합니다. 농축 완충액, 프리캐스트 겔, 형광 염색제, 분자량 사다리는 한 번 사용하거나 재사용이 제한되므로 보충 사이클이 보장되고 자본 지출 정체에 대한 수익 쿠션이 됩니다. 시스템 매출은 여전히 순환적이지만, 소프트웨어 및 이미징 제품군은 실험실이 기존 젤 상자를 AI 지원 문서화 모듈로 개조함으로써 연간 6.54%로 증가할 것으로 예측됩니다. 에든버러 대학의 GelGenie 엔진은 픽셀 수준의 정밀도로 미약한 밴드를 분석하고 컴플라이언스 가능 보고서를 자동으로 생성함으로써 이러한 전환을 보여줍니다.

마이크로플루이딕스 카트리지의 발전은 칩 기반 소모품과 벤치탑 분석기의 새로운 하이브리드 카테고리를 열어 줍니다. 랩 온 어 칩은 한 번의 검사로 나노리터 단위의 용량을 소비하므로 시약 구매량은 90%나 줄어들지만 칩의 총 매출은 증가하기 때문에 벤더는 마진 프로파일을 안정시키기 위해 이 트레이드오프를 활용하고 있습니다. 차세대 장비 내의 스마트 유지보수 대시보드는 버퍼 및 모세관의 자동 재주문화를 촉진하여 전기 영동 장비 및 소모품 시장을 지원하는 소모품 우선 비즈니스 모델을 강화합니다.

유전체학 워크플로우는 NGS와 qPCR에 앞서 DNA 샘플 준비, RNA 무결성 검사, 단편 분석 프로토콜을 배경으로 2024년 전기 영동 장비 및 소모품 시장 점유율의 55.43%를 차지했습니다. 그러나 2030년까지 연평균 복합 성장률(CAGR)이 가장 높을 것으로 예상되는 것은 임상 진단의 7.02%이며, 단백질 치료제의 CE-SDS 밸리데이션과 병원 실험실에서의 도입을 간소화하는 FDA 클래스 I 면제가 뒷받침하고 있습니다. 단백질체학는 전하 변동 모니터링을 위한 모세관 등 전점 수렴에 축발을 계속 두고 있으며, 10 실험실을 대상으로 한 업계 라운드 로빈 연구에서는 pI 값의 상대 표준 편차가 5% 미만이 되어 엄격한 릴리스 기준을 충족했습니다.

전기영동은 신속한 턴어라운드, 제한된 시료의 조리, 명확한 육안 확인이 필요한 최전선 선별 작업에 적합합니다. 임상실이 외래로 이동함에 따라 이 기술의 실적가 작고 소모품이 자기 완결형이기 때문에 관리되는 유틸리티가 필요한 질량 분석기보다 물류면에서 유리합니다.

지역 분석

북미는 바이오파마 클러스터가 밀집되어 FDA의 명확한 지침이 있어 겔 및 모세관 시스템 FDA.GOV의 설치 기반이 충실하기 때문에 2024년 세계 매출의 42.45%를 차지했습니다. 대체 수요의 핵심은 GMP 컴플라이언스를 간소화하는 전자 배치 기록을 통합한 완전 자동화 하드웨어입니다. 과학 수입품에 대한 관세의 불확실성으로 인해 틈새 부품의 취득 비용이 증가할 수 있지만 소모품 흐름을 혼란시킬 가능성은 낮습니다.

아시아태평양은 CAGR 5.67%로 예측되며 가장 빠르게 성장하는 지역입니다. 중국의 14차 5개년 계획에서는 대학 수준의 생화학 연구실에 엄청난 자금이 할당되고, 인도의 생산 연동형 장려 프로그램은 분석 기기를 대상으로 하고 있으며, 대학 네트워크 전체에 조달의 파도가 밀려들고 있습니다. 일본과 한국은 바이오시밀러 개발을 위한 고급 모세관 시스템을 지속적으로 지지하고 안정적인 고가치 수요를 강화하고 있습니다.

유럽은 생명 공학 신흥 기업 증가와 공중 보건 시스템의 비용 억제 균형을 유지하면서 균형 성장을 유지합니다. EU 장비 규제의 조화로 인해 지역 전체 출시가 간소화되지만 지속가능성에 대한 지침은 공급업체가 소모품의 플라스틱 폐기물을 최소화하도록 요구합니다. 브라질과 사우디아라비아의 보건부는 헤모글로빈증 신생아 스크리닝에 전기 영동을 통한 확인을 의무화하여 향후 플랫폼 업그레이드에 대한 발판을 구축하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 바이오의약품 연구개발비 가속

- 맞춤형 의료와 유전체 진단의 도입 확대

- 세계 학술연구 및 계약조사 인프라 확대

- 바이오의약품 제조에 있어서의 하이 스루풋 품질 관리 수요 증가

- 신흥 경제국의 분자 생물학 교육 프로그램에 대한 정부 자금 증가

- 전기영동과 마이크로플루이딕스공학 및 자동화 플랫폼의 융합

- 시장 성장 억제요인

- 고급 전기 영동 시스템의 높은 자본 비용과 운영 비용

- LC-MS 등의 대체 분리 기술과의 경쟁

- 개발도상지역에서 복잡한 데이터 분석을 위한 숙련노동력 부족

- 중요한 고순도 시약 및 소모품 공급의 취약성

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 강도

제5장 시장 규모와 성장 예측

- 제품별

- 시스템

- 겔 전기 영동 시스템

- 모세관 전기 영동 시스템

- 미세유체 전기 영동 시스템

- 시약 및 소모품

- 겔 및 완충액

- 염색제 및 염료

- 막 및 블로팅 매체

- 분자량 표준 및 래더

- 소프트웨어 및 이미징 솔루션

- 겔 문서화 및 분석 소프트웨어

- CE 데이터 분석 플랫폼

- AI 기반 자동화 제품군

- 시스템

- 용도별

- 유전체학(DNA/RNA 분석)

- 단백질체학(단백질 특성 분석)

- 임상 진단

- 품질 관리 및 공정 검증

- 워크플로우 단계별

- 시료 준비 및 로딩

- 분리 및 분획

- 시각화, 이미징 및 데이터 분석

- 최종 사용자별

- 학술 및 연구 기관

- 병원 및 진단센터

- 제약 및 바이오테크놀러지 기업

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Agilent Technologies Inc.

- Bio-Rad Laboratories Inc.

- Thermo Fisher Scientific Inc.

- Danaher(Cytiva & Beckman Coulter)

- Merck KGaA(Millipore Sigma)

- GE Healthcare

- PerkinElmer Inc.

- QIAGEN NV

- Lonza Group Ltd.

- Shimadzu Corporation

- Sebia Group

- SCIEX

- Helena Laboratories

- Cleaver Scientific Ltd.

- Analytik Jena AG

- Lumex Instruments

- Consort NV

- Bio-Techne(ProteinSimple)

- Hitachi High-Tech Corp.

- Creative Diagnostics

제7장 시장 기회와 향후 전망

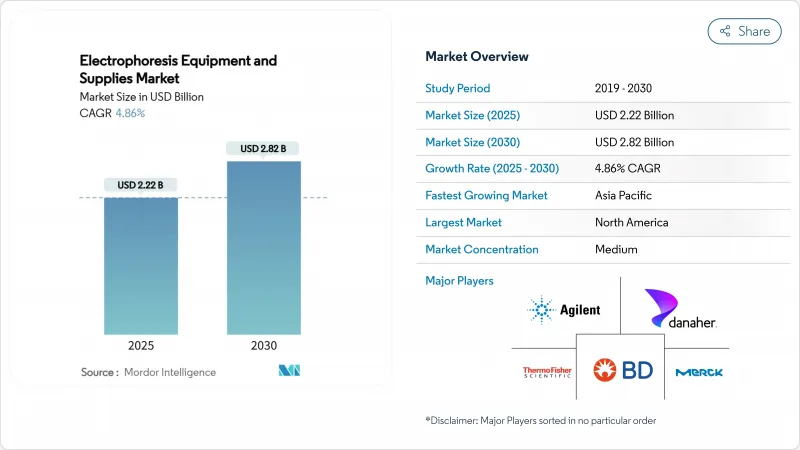

KTH 25.11.03The electrophoresis equipment and supplies market size stands at USD 2.22 billion in 2025 and is forecast to reach USD 2.82 billion by 2030, reflecting a 4.86% CAGR over the period.

This growth trajectory is steady rather than explosive, mirroring a maturing landscape in which biopharmaceutical R&D, clinical diagnostics, and regulated quality-control testing continue to rely on electrophoretic separation even as competing technologies proliferate. Personalized medicine programs now require high-throughput molecular characterization, which keeps capital equipment investments resilient and drives a robust consumables replacement cycle. At the same time, biologics manufacturing hubs are standardizing capillary systems for in-process and release testing of monoclonal antibodies, sustaining demand for integrated platforms that bundle hardware, reagents, and analysis software. Competitive pressure from liquid chromatography-mass spectrometry remains a real headwind, yet recurring reagent revenue, the installed base advantage of legacy suppliers, and the technology's established regulatory pathway combine to support consistent expansion of the electrophoresis equipment and supplies market.

Global Electrophoresis Equipment And Supplies Market Trends and Insights

Growing Adoption of Personalized Medicine and Genomic Diagnostics

Capillary electrophoresis couples seamlessly with PCR workflows to deliver rapid, automated detection of gene variants underlying disorders such as cystic fibrosis and Huntington's disease. Performance benchmarks published in Clinical Chemistry and Laboratory Medicine confirm that electrophoresis can screen hundreds of samples per shift with minimal hands-on time, which reduces operational costs for hospital labs. Point-of-care microfluidic devices now bring this capability to bedside settings, where compact cartridges complete separations in less than five minutes, underscoring the modality's relevance to precision-care protocols.

Expansion of Academic and Contract Research Infrastructure Worldwide

Government-funded laboratory build-outs across India, China, Indonesia, and Nigeria position electrophoresis as a foundational teaching and research tool. Enrollment surges in molecular-biology programs have triggered bulk procurements of basic horizontal and vertical gel units as well as entry-level capillary systems. Contract research organizations (CROs) carry this momentum forward by integrating electrophoretic assays into multi-omic service lines, ensuring steady consumables pull-through across regional hubs.

High Capital and Operating Costs of Advanced Electrophoresis Systems

State-of-the-art capillary genetic analyzers list between USD 75,000 and USD 150,000. Consumables, including polymer matrices and capillaries, can outstrip the initial hardware outlay within three years of routine use. Proposed tariff schedules on analytical imports would add USD 63 billion to operating budgets across life-science sectors, prompting smaller laboratories to postpone refresh plans. Supply chain interruptions in high-purity buffers underscore the fragility of the cost structure, making price a primary adoption barrier in resource-constrained geographies.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for High-Throughput Quality Control in Biologics Manufacturing

- Convergence with Microfluidics and Automation Platforms

- Competition from Alternative Separation Technologies Such as LC-MS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electrophoresis equipment and supplies market size for reagents and consumables was USD 1.03 billion in 2024, equating to 46.43% of overall revenue. Buffer concentrates, pre-cast gels, fluorescent stains, and molecular weight ladders are single-use or limited-reuse items, guaranteeing a replenishment cycle that cushions revenue against capital-spending lulls. Systems sales remain cyclical but software and imaging suites are forecast to compound at 6.54% annually as laboratories retrofit legacy gel boxes with AI-enabled documentation modules. The University of Edinburgh GelGenie engine exemplifies this transition by parsing faint bands with pixel-level accuracy and automatically generating compliance-ready reports.

Advances in microfluidic cartridges carve out a new hybrid category of chip-based consumables plus bench-top analyzers. Each lab-on-a-chip run consumes nanoliter volumes, reducing reagent purchases by as much as 90%, but drives higher chip revenue in aggregate, a trade-off vendors leverage to stabilize margin profiles. Smart-maintenance dashboards inside next-generation instruments prompt automatic re-ordering of buffers and capillaries, reinforcing the consumables-first business model that underpins the electrophoresis equipment and supplies market.

Genomics workflows controlled 55.43% of electrophoresis equipment and supplies market share in 2024 on the back of DNA sample preparation, RNA integrity checks, and fragment analysis protocols that precede NGS or qPCR. Yet the highest CAGR through 2030 belongs to clinical diagnostics at 7.02%, buoyed by CE-SDS validation for protein therapeutics and the FDA Class I exemption that simplifies implementation in hospital labs. Proteomics continues to pivot toward capillary isoelectric focusing for charge-variant monitoring, where industry round-robin studies across ten labs yielded relative standard deviations under 5% on pI values, meeting stringent release criteria.

Electrophoresis remains well suited to frontline screening tasks that need quick turnaround, limited sample triage, and definitive visual confirmation. As clinical labs migrate to outpatient settings, the technology's modest footprint and self-contained consumables give it a logistical edge over mass spectrometers that demand controlled utilities.

The Electrophoresis Equipment and Supplies Market Report is Segmented by Product (Systems, Reagents & Consumables, and Software & Imaging Solutions), Application (Genomics, and More), Workflow Stage (Sample Preparation, Separation, and Visualization), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 42.45% of global revenue in 2024 thanks to its dense biopharma cluster, clear FDA guidance, and deep installed base of gel and capillary systems FDA.GOV. Replacement demand centers on fully automated hardware that integrates electronic batch records to streamline GMP compliance. Tariff uncertainty on scientific imports could raise acquisition costs for niche components but is unlikely to disrupt consumables flows, which are predominantly regionally manufactured.

Asia-Pacific is the fastest-advancing territory with a projected 5.67% CAGR. China's 14th Five-Year Plan earmarks substantial funding for college-level biochemistry labs, while India's production-linked incentive program covers analytical instruments, triggering procurement waves across university networks. Japan and South Korea continue to favor premium capillary systems for biosimilar development, reinforcing steady high-value demand.

Europe maintains equilibrium growth, balancing rising biotech start-ups with cost-containment in public health systems. EU device regulation harmonization simplifies pan-regional launches, but sustainability directives push vendors to minimize plastic waste in consumables. Latin America and MEA remain nascent yet promising: national health ministries in Brazil and Saudi Arabia now require electrophoresis confirmation for hemoglobinopathy newborn screening, establishing a foothold for future platform upgrades.

- Agilent Technologies

- Bio-Rad Laboratories

- Thermo Fisher Scientific

- Danaher (Cytiva & Beckman Coulter)

- Merck

- GE Healthcare

- PerkinElmer

- QIAGEN

- Lonza Group Ltd.

- Shimadzu

- Sebia

- SCIEX

- Helena Laboratories

- Cleaver Scientific Ltd.

- Analytik Jena

- Lumex Instruments

- Consort NV

- Bio-Techne (ProteinSimple)

- Hitachi High-Tech Corp.

- Creative Diagnostics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Biopharmaceutical Research and Development Expenditure

- 4.2.2 Growing Adoption of Personalized Medicine and Genomic Diagnostics

- 4.2.3 Expansion of Academic and Contract Research Infrastructure Worldwide

- 4.2.4 Rising Demand for High-Throughput Quality Control in Biologics Manufacturing

- 4.2.5 Increasing Government Funding for Molecular Biology Education Programs In Emerging Economies

- 4.2.6 Convergence of Electrophoresis With Microfluidics and Automation Platforms

- 4.3 Market Restraints

- 4.3.1 High Capital and Operating Costs of Advanced Electrophoresis Systems

- 4.3.2 Competition from Alternative Separation Technologies Such as LC-MS

- 4.3.3 Limited Skilled Workforce for Complex Data Interpretation in Developing Regions

- 4.3.4 Vulnerabilities in Supply Of Critical High-Purity Reagents and Consumables

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Systems

- 5.1.1.1 Gel Electrophoresis Systems

- 5.1.1.2 Capillary Electrophoresis Systems

- 5.1.1.3 Microfluidic Electrophoresis Systems

- 5.1.2 Reagents & Consumables

- 5.1.2.1 Gels & Buffers

- 5.1.2.2 Stains & Dyes

- 5.1.2.3 Membranes & Blotting Media

- 5.1.2.4 Molecular Weight Standards & Ladders

- 5.1.3 Software & Imaging Solutions

- 5.1.3.1 Gel Documentation & Analysis Software

- 5.1.3.2 CE Data Analysis Platforms

- 5.1.3.3 AI-Driven Automation Suites

- 5.1.1 Systems

- 5.2 By Application

- 5.2.1 Genomics (DNA/RNA Analysis)

- 5.2.2 Proteomics (Protein Characterization)

- 5.2.3 Clinical Diagnostics

- 5.2.4 Quality Control & Process Validation

- 5.3 By Workflow Stage

- 5.3.1 Sample Preparation & Loading

- 5.3.2 Separation & Fractionation

- 5.3.3 Visualization, Imaging & Data Analysis

- 5.4 By End-User

- 5.4.1 Academic & Research Institutes

- 5.4.2 Hospitals & Diagnostic Centers

- 5.4.3 Pharmaceutical & Biotechnology Companies

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Agilent Technologies Inc.

- 6.3.2 Bio-Rad Laboratories Inc.

- 6.3.3 Thermo Fisher Scientific Inc.

- 6.3.4 Danaher (Cytiva & Beckman Coulter)

- 6.3.5 Merck KGaA (Millipore Sigma)

- 6.3.6 GE Healthcare

- 6.3.7 PerkinElmer Inc.

- 6.3.8 QIAGEN N.V.

- 6.3.9 Lonza Group Ltd.

- 6.3.10 Shimadzu Corporation

- 6.3.11 Sebia Group

- 6.3.12 SCIEX

- 6.3.13 Helena Laboratories

- 6.3.14 Cleaver Scientific Ltd.

- 6.3.15 Analytik Jena AG

- 6.3.16 Lumex Instruments

- 6.3.17 Consort NV

- 6.3.18 Bio-Techne (ProteinSimple)

- 6.3.19 Hitachi High-Tech Corp.

- 6.3.20 Creative Diagnostics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment