|

시장보고서

상품코드

1848325

접선유동여과 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Tangential Flow Filtration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

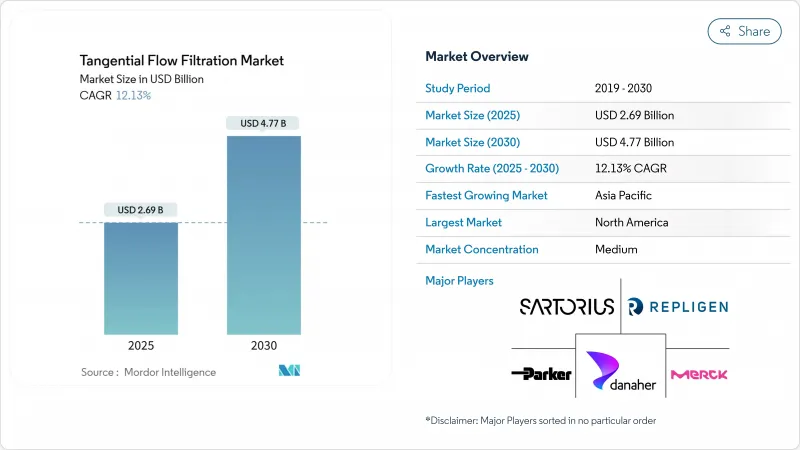

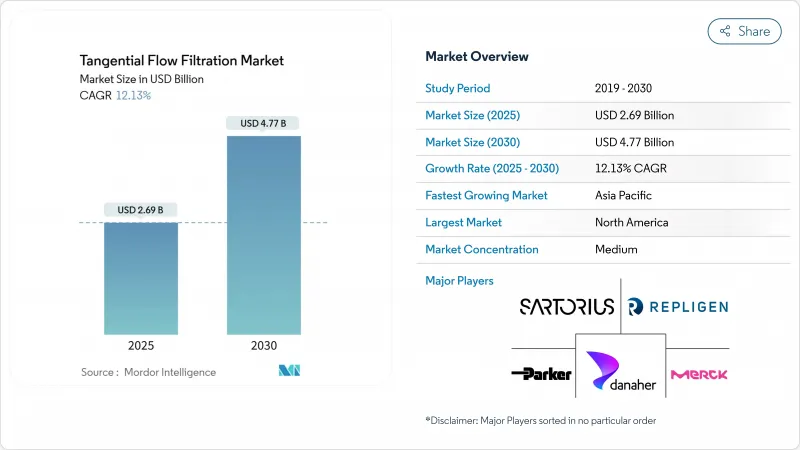

접선유동여과 시장 규모는 2025년에 26억 9,000만 달러로 추정되고, 2030년에는 47억 7,000만 달러에 이를 것으로 예측되며, CAGR 12.13%로 확대될 전망입니다.

공정 강화형 연속 바이오 제조 라인에 대한 지속적인 투자, 유전자 치료 플랜트의 급속한 스케일업, 일회용 장치로의 가속적 시프트가 이 두 자리수의 확대를 지원하고 있습니다. 아시아의 개발 수탁기관은 대규모의 그린 필드 플랜트를 가동하고 있는 한편, 북미와 유럽의 기존 제조업체는 클린 룸의 공간을 확장하지 않고 처리 능력을 높이기 위해서, 레거시 시설을 개수하고 있습니다. 인라인 분석과 여과 스키드의 지속적인 통합은 공정 개발 사이클을 단축하고, 고장률을 낮추며, 최종 사용자를 완전히 통합된 시스템 패키지로 밀어 올립니다. 동시에 공급업체는 GMP 등급 멤브레인 공급망 마찰 및 플라스틱 폐기물에 대한 규제 강화를 통해 재료 혁신 및 재활용 프로그램에 주력하고 있습니다.

세계의 접선유동여과 시장 동향 및 인사이트

일회용 시스템이 교환 시간 단축

접선유동여과의 일회용 시스템은 지금까지 다품종 생산 시설에 한정되어 있던 4-8시간의 세정 밸리데이션 윈도우를 없애, 개발 단계의 생산성을 27% 향상시켰습니다. 기존의 단일클론항체 공장 뿐만이 아니라, 세포 치료 및 유전자 치료에도 채용되게 되었습니다. 무균성이 보장되고 검증 파일이 보다 슬림해지기 때문에 규제 당국은 점점 더 일회용 어셈블리에 대한 지도를 강화하고 있으며, 이는 최근의 FDA 시설 사찰 동향에도 반영되고 있습니다. 그러나 지속가능성에 대한 논의는 격화되고 있습니다. 라이프사이클 평가가 구매 결정에 반영됨에 따라 공급업체는 생분해성 멤브레인 및 폐쇄 루프 플라스틱 재생 방식의 개발에 박차를 가하고 있습니다.

연속 바이오프로세스 채택 확대

연속 바이오프로세스는 접선유동여과를 수주간 정상 생산을 유지하는 상시 온라인 오퍼레이션으로 재지정하여 전형적인 설비 점유 면적을 50-70% 삭감하는 동시에 로트 간의 품질 편차를 억제합니다. 1억 개/mL 이상의 관류 배양에는 견고한 세포 보유 모듈이 필요합니다. 이것은 체류 시간의 단축이 벡터의 분해를 억제하기 때문에 유전자 치료 제조업체에 강하게 지지되고 있는 기능입니다. 디지털 트윈 모델링은 삼성 바이올로그스의 파일럿 라인에서 입증된 것처럼 플럭스, 전단, 막관통압을 실시간으로 미세 조정할 수 있게 되었습니다.

전단에 민감한 양식의 플럭스 속도 제한

바이러스 벡터와 같은 복잡한 생물학적 제제는 높은 전단력을 견딜 수 없기 때문에 조작자는 단클론 항체의 표준보다 50-75% 낮은 처리량 수준에서 필터를 운전할 수밖에 없습니다. 스트레스 포인트를 줄이는 표면 개질막을 사용하더라도 코어 물리학은 캡시드 파열의 위험 없이 흐름을 가속하는 능력을 제한하므로 사이클 시간이 길어지고 장비 용량이 압박됩니다.

부문 분석

2024년의 접선유동여과 시장 점유율은 시스템이 46.34%를 차지하였고, 펌프, 컨트롤러, 실시간 센서를 하나의 검증 엔벨로프로 결합한 턴키 어셈블리에 대한 사용자의 기호를 반영하고 있습니다. 다국적 기업은 데이터 무결성과 자동화의 의무화에 맞추어 설치된 스키드를 정기적으로 업그레이드하고 있기 때문에 수요는 계속 견조합니다. 이와 병행하여, 멤브레인 필터에 할당된 접선유동여과 시장 규모는 일회용 프로그램이 캠페인마다 새로운 카세트를 필요로 하기 때문에 2030년까지 14.67%의 연평균 복합 성장률(CAGR)로 상승하고 있습니다. 일회용 멤브레인 필터는 교차 오염 위험이 허용되지 않으며 교환 속도에 가치가 있는 유전자 치료실에서 특히 급속히 확대되고 있습니다.

사전 컨디셔너, 유동 경로 센서, 일회용 전도성 프로브와 같은 액세서리는 가장 작은 금액의 부문이지만 한 자릿수 중반의 꾸준한 성장을 기록합니다. 공급업체는 이러한 추가 기능을 서비스 계약과 번들로 하여 하드웨어 이외의 수익을 확대하고 있습니다. 리플리겐이 최근 출시한 SoloVPE Plus 시스템은 농도 테스트를 70% 단축하고 자동화된 필터 제어 루프로 피드백하는 통합 분석 추진을 보여줍니다. 하드웨어와 애널리틱스의 이러한 융합은 사용자에게 배치 실패의 위험을 줄이면서 공급업체에게 높은 마진을 제공합니다.

한외여과는 고전적인 생물제제의 완충액 교환과 농축 공정에 정착되어 있기 때문에 2024년에는 57.53%의 매출을 유지했습니다. 그럼에도 불구하고 정밀 여과는 2030년까지 연평균 복합 성장률(CAGR) 14.83%로 확대될 것으로 예측되며, 이는 세포 보유의 엄격한 컷오프에 의존하는 고세포 밀도의 관류 배양에 뒷받침되고 있습니다. 그러므로 정밀 여과 모듈에 할당된 접선 유동 여과 시장 규모는 매크로 규모의 수치보다 빠르게 성장하고 있으며, 파편 제거를 위해 정확한 기공 분포를 필요로 하는 바이러스 벡터 시설에 의해 자극되고 있습니다.

폴리머 화학에서의 획기적인 개선, 특히 폴리에테르 설폰 블렌드와 재생 셀룰로오스 코팅은 장시간 관류 운전 중 플럭스 안정성 및 내파울링성을 향상시킵니다. 또한 새로운 생물학적 제제의 전단 감수성의 특징인 높은 역삼투액 선택성과 낮은 막 투과압을 조합한 그라디언트 포어 구조에도 혁신적인 아키텍처가 나타났습니다. 역삼투와 나노 여과는 여전히 틈새 시장이며, 주로 유틸리티 용수의 연마를 다루고 있으며, 그 점유율이 예측 기간 동안 크게 늘어나지 않을 것 같습니다.

지역 분석

북미는 고급 연구개발 클러스터, 명확한 FDA 검증 패스웨이, 백신, 항체, 바이러스 벡터 전반에 걸친 풍부한 도입 능력에 힘입어 접선유동여과 시장의 2024년 매출의 39.62%를 창출했습니다. Thermofisher Scientific에 의한 Solventam 정화 사업의 41억 달러 인수와 같은 합병은 이 지역이 기술 통합의 중력의 중심지 역할을 한다는 것을 뒷받침합니다. 그러나 인재 부족과 원재료의 리드 타임의 상승이 계속되고 있기 때문에 공급망을 2대륙으로 나누는 것을 검토하고 있는 제조업체도 있습니다.

아시아태평양의 2030년까지의 CAGR은 13.56%로 세계에서 가장 빠르게 확대될 전망입니다. 삼성 바이오로직스의 60억 달러의 '플랜트 5' 건설과 롯데 바이오로직스의 33억 달러의 그린필드 복합시설을 비롯한 여러 주요 프로젝트는 대용량 여과 스키드에 대한 현지 수요를 높이고 있습니다. WuXi Biologics 및 Chime Biologics와 같은 중국 CDMO도 마찬가지로 바이러스 벡터 제품군의 규모를 확대하고 주문 잔액을 더욱 늘리고 있습니다. 유리한 세제 우대 조치, 상대적으로 낮은 인건비, 고분자 수지의 운송 경로의 단축 등이 이 지역의 경쟁력을 높이고 있지만, 지재와 규제의 조정이라는 과제가 남아 있기 때문에 일부의 다국적 스폰서의 수입은 완만합니다.

유럽은 견고한 의약품 기반과 물 재사용과 생분해성 필터 엘리먼트를 장려하는 엄격한 환경 법령에 의해 한 자릿수 중반의 안정된 성장을 누리고 있습니다. 브렉지트(EU 이탈) 관련 국경을 넘은 마찰과 에너지 가격 상승은 조업 비용을 끌어올리지만 동시에 소비전력 1킬로와트 당 더 많은 제품을 짜내는 연속처리 케이스를 뒷받침하고 있습니다. 중동 및 아프리카와 남미는 이제 막 시작되었지만 성장을 기대할 수 있는 지역입니다. 두 지역 모두 정부의 생명 과학 보조금 프로그램의 혜택을 받고 있지만 성숙한 시장에서 볼 수있는 공급업체와 인력 생태계가 아직 갖추어지지 않았습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 일회용 시스템으로 전환 시간 대폭 단축

- 상용 바이오프로세스의 채용 확대

- 유전자 치료 벡터용 하이 스루풋 스크리닝 카세트

- 바이오의약품에 있어서 고세포 밀도 관류로의 이행

- 신흥아시아에서 CAPEX 저위 CDMO 건설

- ESG 주도의 물 재활용 의무

- 시장 성장 억제요인

- 전단 감수성 모달리티는 플럭스율을 제한

- GMP 등급 중공사 공급 부족

- 프로세스 자동화 도입에 있어서 학습 곡선 리스크

- 일회용 플라스틱에 관한 수출 관리 규칙

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 시스템

- 일회용 접선유동여과 시스템

- 재사용 가능한 접선유동여과 시스템

- 멤브레인 필터

- 폴리에테르술폰

- 재생 셀룰로오스

- 기타 막

- 액세서리

- 시스템

- 기술별

- 한외여과

- 정밀여과

- 역삼투 및 나노 여과

- 용도별

- 백신과 mAb

- 세포 및 유전자 치료 벡터

- 혈장 유래 단백질

- 기타 용도

- 최종 사용자별

- 바이오 의약품 제조업체

- 계약 개발 제조 조직(CDMO)

- 기타 최종 사용자

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Danaher Corporation

- Merck KGaA

- Sartorius AG

- Repligen Corp.

- Parker Hannifin Corporation

- Alfa Laval

- Andritz Group

- Meissner Filtration

- Sterlitech Corp.

- Solaris Biotechnology

- Thermo Fisher Scientific

- 3M Company

- Cytiva

- GE HealthCare

- Asahi Kasei

- Koch Membrane Systems

- Donaldson Company

- Miltenyi Biotec

- Graver Technologies

- Cobetter Filtration

제7장 시장 기회 및 장래 전망

AJY 25.11.03The tangential flow filtration market size reached USD 2.69 billion in 2025 and is on course to attain USD 4.77 billion by 2030, advancing at a 12.13% CAGR.

Sustained investment in process-intensified, continuous biomanufacturing lines, the rapid scale-up of gene therapy plants, and an accelerated shift toward single-use equipment all underpin this double-digit expansion. Contract development organizations in Asia are commissioning large-footprint greenfield plants, while incumbent North American and European producers are retrofitting legacy facilities to boost throughput without expanding cleanroom space. Ongoing integration of inline analytics with filtration skids shortens process-development cycles and lowers failure rates, pushing end users to favor fully integrated system packages. At the same time, supply-chain friction in GMP-grade membranes and tightening rules on plastic waste are sharpening vendor focus on material innovation and recycling programs.

Global Tangential Flow Filtration Market Trends and Insights

Single-Use Systems Slash Change-Over Time

Single-use tangential flow filtration systems eliminate the 4-8-hour cleaning validation windows that previously limited multiproduct facilities, delivering a documented 27% uplift in development-stage productivity. Adoption has broadened beyond traditional monoclonal antibody plants to cell and gene therapy suites, where dedicated run campaigns heighten contamination concerns. Regulators increasingly guide toward disposable assemblies because sterility assurance is inherent and validation files are slimmer, a position mirrored across recent FDA facility inspection trends. Yet the sustainability conversation is intensifying; life-cycle assessments now inform purchasing decisions, spurring suppliers to advance biodegradable membranes and closed-loop plastic reclamation schemes.

Growing Adoption of Continuous Bioprocessing

Continuous bioprocessing repositions tangential flow filtration as a permanently online operation that maintains steady-state production for weeks, cutting the typical facility footprint by 50-70% while tightening quality variance among lots. Perfusion cultures running above 100 million cells/mL require robust cell-retention modules, a capability strongly favored by gene therapy producers because shorter residence times curb vector degradation. Digital-twin modeling now fine-tunes flux, shear, and trans-membrane pressure in real time, as demonstrated by Samsung Biologics' pilot lines.

Shear-Sensitive Modalities Limit Flux Rates

Complex biologics such as viral vectors cannot tolerate high shear, forcing operators to run filters at throughput levels that are 50-75% lower than monoclonal antibody norms. Even with surface-modified membranes that reduce stress points, core physics restrict the ability to accelerate flows without risking capsid rupture, thus prolonging cycle times and squeezing facility capacity.

Other drivers and restraints analyzed in the detailed report include:

- High-Throughput Screening Cassettes for Gene-Therapy Vectors

- Biopharma Shift to High-Cell-Density Perfusion

- Scarcity of GMP-Grade Hollow-Fiber Supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Systems accounted for a 46.34% tangential flow filtration market share in 2024, reflecting user preference for turnkey assemblies that couple pumps, controllers, and real-time sensors under a single validation envelope. Demand remains resilient because multinationals routinely upgrade installed skids to align with tightening data-integrity and automation mandates. In parallel, the tangential flow filtration market size allocated to membrane filters is climbing at a 14.67% CAGR to 2030 as single-use programs require fresh cassettes for each campaign. Disposable membrane uptake is particularly sharp in gene therapy suites, where cross-contamination risk is less acceptable and changeover speed carries premium value.

Accessories such as pre-conditioners, flow-path sensors, and disposable conductivity probes are the smallest dollar segment yet record steady, mid-single-digit growth. Suppliers bundle these add-ons with service agreements, expanding revenue beyond hardware. Repligen's recently launched SoloVPE Plus system exemplifies the push toward integrated analytics, shortening concentration tests by 70% and feeding back to automated filter-control loops. This convergence of hardware and analytics delivers higher margins to vendors while reducing batch-failure risk for users.

Ultrafiltration retained 57.53% revenue in 2024 given its entrenchment in buffer-exchange and concentration steps for classical biologics. Nevertheless, microfiltration is projected to expand at a 14.83% CAGR through 2030, propelled by high-cell-density perfusion cultures that depend on tight cell-retention cutoffs. The tangential flow filtration market size apportioned to microfiltration modules is therefore growing faster than the macroscale figure, stimulated by viral vector facilities that demand precise pore distribution for debris removal.

Breakthroughs in polymer chemistry, specifically polyethersulfone blends and regenerated-cellulose coatings, are boosting flux stability and fouling resistance during long perfusion runs. Innovations are also surfacing in gradient-pore architectures that pair high retentate selectivity with low trans-membrane pressure, features that align with the shear-sensitivity of new biologic entities. Reverse osmosis and nanofiltration remain niche, handling mainly utility water polishing, and their share is unlikely to budge materially across the forecast window.

The Tangential Flow Filtration Market Report is Segmented by Product Type (Systems, Membrane Filters, and Accessories), Technology (Ultrafiltration, Microfiltration, and Reverse Osmosis/ Nanofiltration), Application (Vaccines & MAbs), End-User (Biopharma Manufacturers, and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 39.62% of 2024 revenue in the tangential flow filtration market, supported by advanced R&D clusters, a well-defined FDA validation pathway, and deep installed capacity across vaccines, antibodies, and viral vectors. Mergers such as Thermo Fisher Scientific's USD 4.1 billion purchase of Solventum's purification business underscore the region's role as the gravitational center for technology consolidation. Persistent talent shortages and raw-material lead-time spikes, however, are prompting some producers to weigh dual-continental supply chains.

Asia-Pacific is on track to post a 13.56% CAGR through 2030, translating into the fastest regional expansion worldwide. Several headline projects, including Samsung Biologics' USD 6 billion "Plant 5" build and Lotte Biologics' USD 3.3 billion greenfield complex, are raising local demand for high-capacity filtration skids. Chinese CDMOs such as WuXi Biologics and Chime Biologics are similarly scaling viral-vector suites, further inflating order books. Favorable tax incentives, comparatively low labor costs, and short shipping lanes for polymer resins amplify the region's competitiveness, although lingering IP and regulatory alignment challenges moderate uptake among some multinational sponsors.

Europe enjoys steady mid-single-digit growth owing to a robust pharmaceutical base and strict environmental statutes that encourage water-reuse and biodegradable filter elements. Brexit-related cross-border friction and high energy prices inflate operating costs but simultaneously bolster the case for continuous processing that squeezes more product out per kilowatt consumed. Middle East & Africa and South America are nascent yet viewable growth pockets; both benefit from government life-science funding programs but still lack the dense supplier and talent ecosystems found in mature markets.

- Danaher

- Merck

- Sartorius

- Repligen Corp.

- Parker Hannifin

- Alfa Laval

- Andritz Group

- Meissner Filtration

- Sterlitech Corp.

- Solaris Biotechnology

- Thermo Fisher Scientific

- 3M

- Cytiva

- GE Healthcare

- Asahi Kasei

- Koch Membrane Systems

- Donaldson Company

- Miltenyi Biotec

- Graver Technologies

- Cobetter Filtration

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Single-Use Systems Slash Change-Over Time

- 4.2.2 Growing Adoption of Continuous Bioprocessing

- 4.2.3 High-Throughput Screening Cassettes for Gene-Therapy Vectors

- 4.2.4 Biopharma Shift to High-Cell-Density Perfusion

- 4.2.5 CAPEX-Light CDMO Build-Outs in Emerging Asia

- 4.2.6 ESG-Driven Water-Recycling Mandates

- 4.3 Market Restraints

- 4.3.1 Shear-Sensitive Modalities Limit Flux Rates

- 4.3.2 Scarcity Of GMP-Grade Hollow-Fiber Supply

- 4.3.3 Learning-Curve Risk in Process-Automation Adoption

- 4.3.4 Export-Control Rules on Single-Use Plastics

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Systems

- 5.1.1.1 Single-use Tangential Flow Filtration Systems

- 5.1.1.2 Re-usable Tangential Flow Filtration Systems

- 5.1.2 Membrane Filters

- 5.1.2.1 Polyethersulfone

- 5.1.2.2 Regenerated Cellulose

- 5.1.2.3 Other Membranes

- 5.1.3 Accessories

- 5.1.1 Systems

- 5.2 By Technology

- 5.2.1 Ultrafiltration

- 5.2.2 Microfiltration

- 5.2.3 Reverse Osmosis / Nanofiltration

- 5.3 By Application

- 5.3.1 Vaccines & mAbs

- 5.3.2 Cell & Gene-Therapy Vectors

- 5.3.3 Plasma-derived Proteins

- 5.3.4 Other Applications

- 5.4 By End-User

- 5.4.1 Biopharma Manufacturers

- 5.4.2 Contract Development & Manufacturing Organisations (CDMOs)

- 5.4.3 Other End-Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Danaher Corporation

- 6.3.2 Merck KGaA

- 6.3.3 Sartorius AG

- 6.3.4 Repligen Corp.

- 6.3.5 Parker Hannifin Corporation

- 6.3.6 Alfa Laval

- 6.3.7 Andritz Group

- 6.3.8 Meissner Filtration

- 6.3.9 Sterlitech Corp.

- 6.3.10 Solaris Biotechnology

- 6.3.11 Thermo Fisher Scientific

- 6.3.12 3M Company

- 6.3.13 Cytiva

- 6.3.14 GE HealthCare

- 6.3.15 Asahi Kasei

- 6.3.16 Koch Membrane Systems

- 6.3.17 Donaldson Company

- 6.3.18 Miltenyi Biotec

- 6.3.19 Graver Technologies

- 6.3.20 Cobetter Filtration

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment