|

시장보고서

상품코드

1849814

가상현실(VR) : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Virtual Reality (VR) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

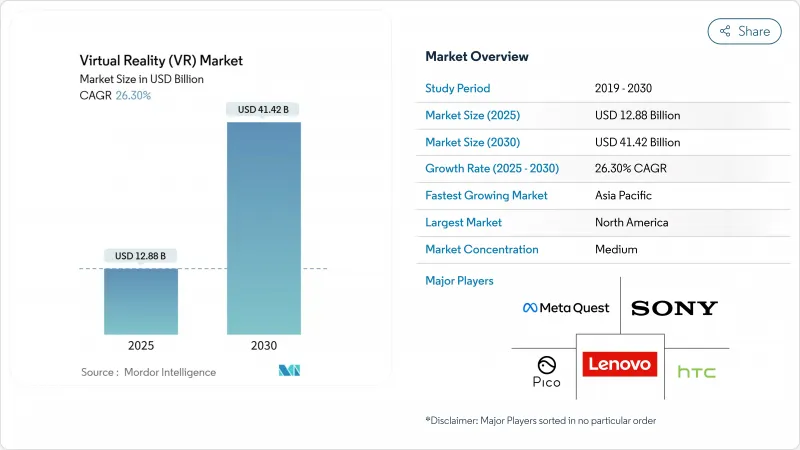

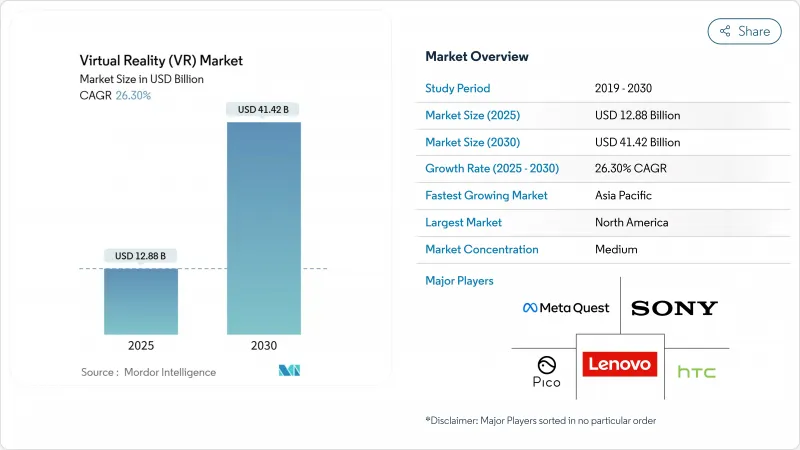

가상현실(VR) 시장 규모는 2025년에 128억 8,000만 달러로 추정되며, 2030년에는 CAGR 26.30%를 나타내 414억 2,000만 달러에 이를 것으로 예측됩니다.

몰입형 트레이닝 플랫폼의 급속한 기업 채용, 혼합 리얼리티 대응 프로세서의 이용 가능성의 상승, 5G 엣지 인프라의 성숙이 이 확대를 뒷받침하고 있습니다. 기업의 넷 제로 서약은 가상 퍼스트 이벤트에 대한 수요를 가속화하고 치료 용도의 규제 클리어런스는 엔터테인먼트를 넘어 기술의 범위를 넓혀줍니다. 하드웨어 기술 혁신은 여전히 필수적이지만, 기업이 재단사의 컨텐츠, 견고한 분석, 학습 관리 시스템과의 완벽한 통합을 우선시함에 따라 소프트웨어 및 서비스는 기세를 늘리고 있습니다.

세계의 가상현실(VR) 시장 동향과 인사이트

기업 전반에 걸친 VR 교육 도입 증가

각 기업은 시험적인 성공 후 본격적인 VR 트레이닝 프로그램을 전개하고 기존 방법에 비해 트레이닝 시간이 75% 단축되어 학습자의 자신감이 275% 향상된 것을 들고 있습니다. 보잉은 교육 시간을 75% 줄이고 델타 항공은 기술자의 숙련도 점검을 5,000% 향상시켰습니다. 손익분기점은 375명의 수강자로 달성되며, 수강자 수가 3,000명을 넘으면 비용효과가 52% 향상됩니다. 포춘 500사의 75% 이상이 현재 월마트 소매 시뮬레이션과 미국 육군 정신건강 모듈을 포함한 학습 전략에 VR을 통합하고 있으며, SOMPO와 같은 일본 보험사는 직장에서의 사고를 억제하기 위해 VR 위험 시뮬레이션을 도입하고 있습니다. 그 결과, 지식은 보다 견고하게 정착되어 현장에서의 퍼포먼스도 보다 안전하게 되어, 트레이닝은 가상현실(VR) 시장에의 주요 기업 진입구로서 확고한 지위를 구축하고 있습니다.

복합현실 대응 GPU 및 SoC의 주류화

퀄컴의 Snapdragon XR2 Gen 2와 같은 차세대 칩셋은 눈당 4.3K 해상도를 제공하고 공간 매핑을 위해 12대의 카메라를 구성하여 미드레인지 헤드셋에 플래그쉽 성능을 제공합니다. Apple의 Vision Pro는 2,300만 화소의 마이크로 OLED 패널을 구동하기 위해 듀얼 칩을 채택하여 처리 수요 곡선을 보여줍니다. 디스플레이 부품만으로도 단가에 530달러가 늘어나기 때문에 다이나믹 포베티드 렌더링과 시선 추적이 효율화에 필수적입니다. 삼성과 구글, 퀄컴의 3사 제휴는 이러한 실리콘의 진보를 주류상품화하고, 가격대를 단계적으로 인하하고, 가상현실(VR) 시장에 대한 접근을 확대할 것을 시사하고 있습니다.

사이버 술에 취한 장기적인 정원 우려

움직임과 빛의 불일치는 메스꺼움, 두통, 감각 장애를 일으켜 장기간의 세션을 망설입니다. 감각 불일치에 관한 조사에서는 시각과 전정의 불일치가 주된 원인이라고 지적되고 있으며, 디바이스의 흔들림이 복잡함을 늘리는 모바일 VR에서는 그 경향이 강해집니다. 의료용 헤드셋의 FDA 지침은 임상적 심각성을 강조하고 메스꺼움 경고를 두드러지도록 의무화합니다. 하드웨어 제조업체는 더 높은 리프레시 속도와 대기 시간 단축을 추구하고 있지만 생리적 한계는 여전히 존재합니다. 엔터프라이즈는 더 짧은 모듈로 위험을 줄이기 때문에 컨텐츠 설계 비용이 상승하고 당분간 가상현실(VR) 시장의 성장이 둔화됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 기업 전체에서의 VR 트레이닝 도입 증가

- 「복합 현실 대응」GPU와 SoC의 보급

- 5G/엣지를 활용한 VR 컨텐츠의 앤테더 스트리밍

- 기업의 넷 제로 서약이 「버추얼 퍼스트」이벤트를 추진

- VR 기반 정신건강요법의 규제 승인

- 컨트롤러 불필요한 인터랙션을 가능하게 하는 초음파 촉각

- 시장 성장 억제요인

- 사이버 세크니스와 장기적인 전정기능장애

- 아이박스의 열 축적에 의해 연속 사용이 제한

- 게임 이외의 AAA급 VR 컨텐츠 부족

- 시선 추적 분석의 데이터 프라이버시 컴플라이언스 비용

- 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 강도

- 거시경제 요인 평가

제5장 시장 규모와 성장 예측

- 제공별

- 하드웨어

- 소프트웨어

- 서비스

- 기기 형태별

- 유선 연결형 HMD

- 독립형 HMD

- 스크린리스 뷰어

- CAVE/몰입형 공간

- 몰입도별

- 비몰입형

- 반몰입형

- 완전 몰입형

- 최종 사용자 업계별

- 게임

- 미디어 및 엔터테인먼트

- 헬스케어

- 교육 및 훈련

- 군사 및 방위

- 소매 및 전자상거래

- 부동산 및 건축

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Meta Platforms(Meta Quest)

- Sony Corporation

- HTC Corporation

- Samsung Electronics Co. Ltd

- Apple Inc.

- Qualcomm Technologies Inc.

- Lenovo Group Ltd

- Pico Interactive Inc.

- Valve Corporation

- Varjo Technologies Oy

- Microsoft Corporation

- Magic Leap Inc.

- Vuzix Corporation

- FOVE Inc.

- DPVR(Lexiang Tech Co. Ltd)

- Unity Technologies Inc.

- Unreal Engine (Epic Games Inc.)

- Autodesk Inc.

- Dassault Systemes SE

- 3D Systems Corporation

제7장 시장 기회와 향후 전망

KTH 25.11.03The Virtual Reality market size is estimated at USD 12.88 billion in 2025 and is projected to reach USD 41.42 billion by 2030, advancing at a 26.30% CAGR.

Rapid enterprise adoption of immersive training platforms, rising availability of mixed-reality-ready processors, and maturing 5G edge infrastructure underpin this expansion. Corporate net-zero pledges accelerate demand for virtual-first events, while regulatory clearances for therapeutic applications extend the technology's reach beyond entertainment. Hardware innovation remains vital, yet software and services gain momentum as organizations prioritize tailored content, robust analytics, and seamless integration with learning-management systems.

Global Virtual Reality (VR) Market Trends and Insights

Rising Enterprise-Wide VR Training Adoption

Organizations roll out full-scale VR training programs after pilot success, citing a 75% reduction in training time and a 275% jump in learner confidence versus conventional methods. Boeing recorded a 75% cut in training hours, and Delta Air Lines raised technician proficiency checks by 5,000%. Break-even arrives at 375 learners and becomes 52% more cost-effective once cohorts exceed 3,000. Over 75% of Fortune 500 companies now embed VR in learning strategies, including Walmart's retail simulations and the U.S. Army's mental-health modules, while Japanese insurers such as SOMPO deploy VR hazard simulations to curb workplace incidents. The outcome is stronger knowledge retention and safer on-the-job performance, cementing training as the principal enterprise gateway into the Virtual Reality market.

Mainstreaming of Mixed-Reality-Ready GPUs and SoCs

Next-generation chipsets like Qualcomm's Snapdragon XR2+ Gen 2 deliver 4.3 K-per-eye resolution and orchestrate a dozen cameras for spatial mapping, bringing flagship performance to mid-range headsets. Apple's Vision Pro employs dual chips to drive 23 million-pixel micro-OLED panels, illustrating processing demand curves. Display components alone add USD 530 to unit costs, so dynamic foveated rendering and eye-tracking become essential for efficiency. Samsung's three-way alliance with Google and Qualcomm signals mainstream commercialisation of these silicon advances, progressively lowering price points and broadening access to the Virtual Reality market.

Cybersickness and Long-Term Vestibular Concerns

Motion-to-photon discrepancies trigger nausea, headache, and disorientation, discouraging extended sessions. Sensory-conflict research pinpoints combined visual-vestibular mismatch as the main cause, intensified in mobile VR where device sway adds complexity. FDA guidelines for medical-grade headsets mandate prominent nausea warnings, highlighting clinical gravity. Hardware makers pursue higher refresh rates and latency cuts, yet physiological limits persist. Enterprises mitigate risk through shorter modules, raising content design costs and dampening near-term Virtual Reality market growth.

Other drivers and restraints analyzed in the detailed report include:

- 5G/Edge-Powered Untethered Streaming of VR Content

- Corporate Net-Zero Pledges Driving Virtual-First Events

- Eye-Box Heat Build-Up Limiting Continuous Usage

For complete list of drivers and restraints, kindly check the Table Of Contents.

List of Companies Covered in this Report:

- Meta Platforms (Meta Quest)

- Sony Corporation

- HTC Corporation

- Samsung Electronics Co. Ltd

- Apple Inc.

- Qualcomm Technologies Inc.

- Lenovo Group Ltd

- Pico Interactive Inc.

- Valve Corporation

- Varjo Technologies Oy

- Microsoft Corporation

- Magic Leap Inc.

- Vuzix Corporation

- FOVE Inc.

- DPVR (Lexiang Tech Co. Ltd)

- Unity Technologies Inc.

- Unreal Engine (Epic Games Inc.)

- Autodesk Inc.

- Dassault Systemes SE

- 3D Systems Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising enterprise-wide VR training adoption

- 4.2.2 Mainstreaming of "mixed reality-ready" GPUs and SoCs

- 4.2.3 5G/Edge-powered untethered streaming of VR content

- 4.2.4 Corporate Net-Zero pledges driving 'virtual-first' events

- 4.2.5 Regulatory approvals for VR-based mental-health therapies

- 4.2.6 Ultrasound-haptics enabling controller-free interaction

- 4.3 Market Restraints

- 4.3.1 Cybersickness and long-term vestibular concerns

- 4.3.2 Eye-box heat build-up limiting continuous usage

- 4.3.3 Scarcity of AAA-grade VR content outside gaming

- 4.3.4 Data-privacy compliance costs for eye-tracking analytics

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Force Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Assessment of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Device Form Factor

- 5.2.1 Tethered HMD

- 5.2.2 Stand-alone HMD

- 5.2.3 Screenless Viewer

- 5.2.4 CAVE / Immersive Rooms

- 5.3 By Immersion Level

- 5.3.1 Non-Immersive

- 5.3.2 Semi-Immersive

- 5.3.3 Fully-Immersive

- 5.4 By End-User Industry

- 5.4.1 Gaming

- 5.4.2 Media and Entertainment

- 5.4.3 Healthcare

- 5.4.4 Education and Training

- 5.4.5 Military and Defense

- 5.4.6 Retail and eCommerce

- 5.4.7 Real Estate and Architecture

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Meta Platforms (Meta Quest)

- 6.4.2 Sony Corporation

- 6.4.3 HTC Corporation

- 6.4.4 Samsung Electronics Co. Ltd

- 6.4.5 Apple Inc.

- 6.4.6 Qualcomm Technologies Inc.

- 6.4.7 Lenovo Group Ltd

- 6.4.8 Pico Interactive Inc.

- 6.4.9 Valve Corporation

- 6.4.10 Varjo Technologies Oy

- 6.4.11 Microsoft Corporation

- 6.4.12 Magic Leap Inc.

- 6.4.13 Vuzix Corporation

- 6.4.14 FOVE Inc.

- 6.4.15 DPVR (Lexiang Tech Co. Ltd)

- 6.4.16 Unity Technologies Inc.

- 6.4.17 Unreal Engine (Epic Games Inc.)

- 6.4.18 Autodesk Inc.

- 6.4.19 Dassault Systemes SE

- 6.4.20 3D Systems Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment