|

시장보고서

상품코드

1849833

일반의약품(OTC) 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Over The Counter Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

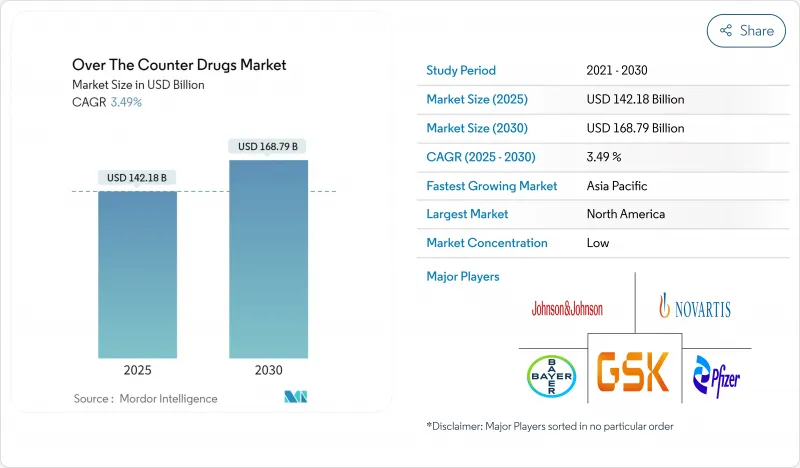

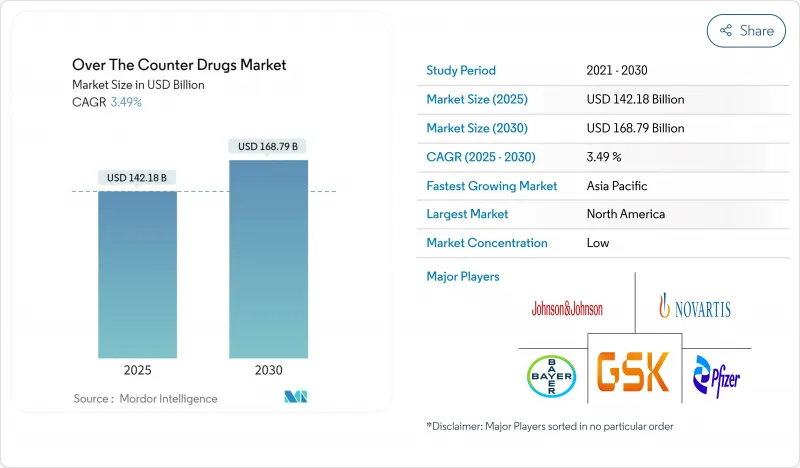

일반의약품(OTC) 시장은 2025년에 1,959억 6,000만 달러의 규모에 이르고, 2030년에는 CAGR 4.80%를 나타내 2,477억 4,000만 달러에 이를 것으로 예측됩니다.

이 동향은 1차 케어(1차 의료) 시스템의 부담을 경감해, 선반에서의 의사 결정을 간소화할 수 있는 기업에 보답하는 것입니다. 규제 당국은 한때 복잡한 분자를 처방전 전용 채널에 머물러 있던 규칙을 완화하고 있으며, 제조업체는 성숙한 브랜드의 만료 전략을 재검토하고 디지털 자체 선택 도구를 제품 시장에 통합하도록 촉구하고 있습니다. 또한, 구미, 씹을 수 있는 패치 등, 보다 일상적인 건강 습관에 가까운 제형에 대한 투자도 진행되고 있습니다. 아시아의 일부에서는 여전히 위조품 위험이 높기 때문에 브랜드 소유자는 신뢰성을 지키기 위해 추적 추적 기술과 커뮤니티 교육을 결합하고 있으며, 북미와 유럽의 소매 기업은 출입구 배달과 실시간 약사 지도를 융합시킨 옴니 채널 모델을 미세 조정하고 있습니다.

세계의 일반의약품(OTC) 시장 동향과 인사이트

셀프 케어와 예방 의료에 대한 소비자의 기호의 향상

화이자의 공개에 따르면, 소비자의 81%가 경미한 질병에 대한 최초 대응으로 OTC 제품을 이용하고 있습니다. 이 행동 변화는 일반적인 증상에 대한 의사의 진찰률을 감소시키기에 충분한 규모이며, 그 결과 처방의 습관도 변화하고 있습니다. 의사는 OTC의 사용을 스텝 테라피 프로토콜의 필수 요소로 삼아 처방에 의한 개입을 보다 긴급한 요구에 대해 삼가게 되었습니다. 흥미로운 부작용으로, 지불자는이 동향을 조용히 환영합니다. 왜냐하면 OTC 의약품이 1달러 사용될 때마다 개인부담이 발생하여 상환예산이 경감되기 때문입니다.

Rx에서 OTC로 전환 계속

미국 식품의약국(FDA)은 2025년 1월 비처방용 의약품 추가조건(ACNU) 규칙을 성문화하고 안전성 프로파일이 미묘하게 다른 제품이 OTC로 이행하는 문호를 열었습니다. 소비자 헬스케어 프로덕츠 협회(CHPA)는 700개 이상의 제품이 처방전의 벽을 넘어섰다고 지적합니다. 별로 인식되지 않지만, 라이프사이클 매니지먼트 팀이 Rx에서 OTC로의 이행을 특허연장 전술과 나란히 주류의 전략적 테코로 간주하고, 성숙한 분자를 재이용이나 재제제화하지 않고 상업적 추풍을 효과적으로 길게 하고 있다는 것입니다.

브랜드의 신뢰를 해치는 위조품과 규격 외품

National Association of Boards of Pharmacy는 온라인 약국 사이트의 96%가 컴플라이언스에 반하여 운영되고 있다고 추정합니다. 이러한 확산은 합법적인 브랜드 자산, 따라서 환자의 복용 보험을 손상시키는 병렬 시장을 조장합니다. 전략 수준에서 위조 위협은 규제 당국이 아직 의무화하지 않은 경우에도 공인 기업을 블록체인 기반 추적 및 추적 솔루션으로 향하게 합니다. 따라서 조기에 도입한 기업은 공급망의 무결성과 검증된 진정성에 기반한 마케팅 활용이라는 두 가지 이점을 확보할 수 있을 가능성이 있습니다.

부문 분석

기침, 감기, 인플루엔자 치료제는 2024년 23.1%로 최대 시장 점유율을 유지했지만 비타민 미네랄 보충제(VMS)의 2025-2030년 CAGR은 7.9%로 이 매트릭스에서는 가장 빠릅니다. 이 동향은 유행 후 면역 의식과 치료에서 예방에 이르기까지 광범위한 축발을 반영합니다. 특필해야할 것은 VMS의 브랜딩이 「수면의 질」이나 「스트레스 밸런스」라고 하는 기능적인 성과를 중심으로 하는 경향이 강해지고 있는 것으로, 기술적인 스펙이 아니고, 유저의 이점을 명시하기 위해서 하이테크 분야에서 오랜 세월 사용되어 온 정밀한 메시징 언어를 모방하고 있습니다.

제조체 각사는 스트레스 관리, 수면의 질, 인지 능력 등, 소비자의 새로운 관심사를 타겟으로 한 증상별 처방에 점점 힘을 들이게 되고 있어, 점점 혼잡한 마켓플레이스로 차별화된 포지셔닝을 만들어 내고 있습니다.

2024년에는 정제가 여전히 시장의 38.7%를 차지했지만 구미와 츄어블은 CAGR 9.8%를 나타낼 전망입니다. 과자의 형식이 건강 관리에 침투하는 것은 감각적 경험이 어떻게 기존 투약 형태에서 벗어날 수 있는지 이야기합니다. 제조업체는 현재 어린이뿐만 아니라 건강 지향적인 성인에게도 호소하기 때문에 젤라틴이없는 식물 기반 및 저당 프로파일에 투자하고 있습니다. 맛과 텍스처는 치료 효과와 소비자의 기호성 사이의 역사적인 분리를 없애고 테이블을 장식하는 제품 속성이되고 있습니다.

OTC 제제의 기술 혁신 파이프라인은 계속 확대되고 있으며, 경피흡수형 패치는 일관된 약물전달로 지지를 모으고, 구강내 붕괴형은 소아와 노인의 삼키는 장애에 대응하고 있습니다.

지역 분석

2024년 시장 점유율 상위는 34.8%로, 셀프 메디케이션을 조장하는 높은 자기 부담액, 견고한 약국 체인, Rx에서 OTC로의 전환에 유리한 규제 환경에 지지되었습니다. 2025년 1월부터 운영되는 FDA의 ACNU 프레임워크는 보다 복잡한 분자의 자기 선택을 유도하는 디지털 도구를 허용합니다. 이 역동적인 움직임은 기술 파트너를 의약품 상업화 전략의 핵심으로 밀어 올립니다.

CAGR 8.7%의 아시아태평양은 가처분 소득 증가와 중류 계급의 의욕 증가로 견인되어 2030년까지 가장 급성장하는 지역입니다. 중국의 국가약품감독관리국(국가의약품감독관리국)에는 5,000개 이상의 OTC 제품이 등록되어 있으며, 그중 800개 이상이 처방전에서 변경되었습니다. 경쟁이 치열해지면서 다국적 기업들은 패키지의 언어화 뿐만 아니라 지역의 임상 가이드라인에 따른 용량의 현지화를 진행하고 있습니다.

대부분의 사법 관할구는 온라인 판매를 허가하고 가격 통제를 앞두고 있지만, 조제의 감시를 지키기 위해 약국 이외의 소매를 제한하고 있는 곳도 많습니다. 세분화된 룰북은 제조업체가 국가별 SKU의 변형을 유지하도록 의무화하고 재고 복잡성을 증가시키지만 현지 건강 문제에 적응하는 마이크로 타겟 마케팅 클레임을 가능하게 합니다. 정교한 방법으로, 선적 전략을 채택하고 최종 패키징을 국가별로 할당할 때까지 지연시키는 민첩한 공급망이 유럽에서는 중요한 경쟁 우위가 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 셀프케어와 예방의료에 대한 소비자의 기호의 고조

- 복수의 치료 클래스에 걸친 처방약으로부터 일반의약품으로의 전환이 계속

- 디지털 및 옴니채널 약국 플랫폼의 보급

- 신흥 경제 국가에서 약국 및 의약품 소매 규제의 자유화

- 급속히 고령화하는 인구에 의해 만성 질환의 OTC 관리 수요 증가

- 팬데믹 후의 호흡기·면역 관련 제품에의 주력

- 시장 성장 억제요인

- 신흥 시장에서 브랜드 신뢰를 해치는 위조품 및 조악품

- 소매 경쟁의 격화와 프라이빗 브랜드의 확대에 의한 가격 하락

- 오용이나 유해 사건에 관한 안전성의 우려가 카테고리 확대 제한

- 규제 감시 및 추적 의무 강화로 컴플라이언스 비용 증가

- 공급망 분석

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 기침, 감기 및 독감

- 진통제

- 위장관

- 피부과

- 비타민, 미네랄 및 보충제(VMS)

- 체중 관리

- 안과

- 수면 보조제

- 구강 관리

- 금연 보조제

- 항히스타민제/알레르기

- 귀 관리

- 상처 관리

- 기타 제품

- 처방 유형별

- 정제

- 캡슐 및 소프트젤

- 액체 및 시럽

- 분말 및 과립

- 연고 및 크림

- 스프레이 및 흡입기

- 구미 및 씹을 먹는 제제

- 경피 패치

- 유통 채널별

- 병원 약국

- 체인 약국

- 독립 약국 및 드럭스토어

- 온라인 약국

- 기타 채널

- 연령층별

- 소아과(0-14세)

- 성인(15-64세)

- 노인(65세 이상)

- 원료별

- 화학 기반

- 허브 및 천연

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Kenvue Brands LLC

- Bayer AG

- Haleon Group

- Sanofi SA

- Reckitt Benckiser Group plc

- Pfizer Inc.

- Viatris Inc.

- Perrigo Company plc

- Takeda Pharmaceutical Co. Ltd.

- Boehringer Ingelheim International GmbH

- Sun Pharmaceutical Industries Ltd.

- Teva Pharmaceutical Industries Ltd.

- Glenmark Pharmaceuticals Ltd.

- Dr. Reddy's Laboratories Ltd.

- Piramal Enterprises Ltd.

- Church & Dwight Co. Inc.

- Procter & Gamble Co.

- Prestige Consumer Healthcare Inc.

- Hisamitsu Pharmaceutical Co. Inc.

- Lupin Ltd.

제7장 시장 기회와 향후 전망

KTH 25.11.03The over-the-counter (OTC) drugs market is worth USD 195.96 billion in 2025 and, on its present trajectory, is expected to reach USD 247.74 billion by 2030, reflecting a compound annual growth rate (CAGR) of 4.80%.

Steady expansion rests on consumers' increasing willingness to self-treat minor ailments, a trend that lightens the burden on primary-care systems and rewards companies able to simplify decision-making at the shelf. Regulatory agencies are continuing to relax rules that once kept complex molecules in prescription-only channels, inviting manufacturers to rethink end-of-life strategies for mature brands and to weave digital self-selection tools into product launches. Investment is also tilting toward dosage formats that feel more like daily wellness rituals, gummies, chewables, and patches, because taste and convenience now sit alongside efficacy when shoppers weigh options. With counterfeit risk still high in parts of Asia, brand owners are pairing track-and-trace technology with community education to protect trust, while retailers in North America and Europe fine-tune omnichannel models that merge doorstep delivery with real-time pharmacist guidance.

Global Over The Counter Drugs Market Trends and Insights

Rising Consumer Preference For Self-Care And Preventive Health

81% of consumers now turn to an OTC product as the first response to minor ailments, according to Pfizer disclosures. The behavioral shift is large enough to reduce physician footfall for common conditions, which in turn changes prescribing habits: physicians increasingly frame OTC use as an essential component of step-therapy protocols to reserve prescription interventions for higher-acuity needs. An interesting derivative effect is that payers quietly welcome the trend, because every OTC dollar spent introduces a private out-of-pocket contribution that relieves reimbursement budgets, a dynamic that rebalances cost pressures without new legislation.

Continued Rx-to-OTC Switches

The United States Food and Drug Administration (FDA) codified the Additional Conditions for Nonprescription Use (ACNU) rule in January 2025, opening the gate for products with nuanced safety profiles to migrate into OTC status. More than 700 individual products have crossed the prescription wall, notes the Consumer Healthcare Products Association (CHPA). An under-appreciated consequence is that life-cycle management teams now view Rx-to-OTC migration as a mainstream strategic lever alongside patent-extension tactics, effectively lengthening commercial tailwinds for mature molecules without repurposing or reformulating them.

Counterfeit and Substandard Products Undermining Brand Trust

The National Association of Boards of Pharmacy estimates that 96% of online pharmacy sites operate out of compliance. This proliferation fuels a parallel market that erodes legitimate brand equity and, by extension, patient adherence. At a strategic level, the counterfeit threat propels legitimate players toward blockchain-based track-and-trace solutions, even when regulators have not yet mandated them. Early adopters may therefore secure a two-fold benefit: supply-chain integrity and marketing leverage built on verified authenticity.

Other drivers and restraints analyzed in the detailed report include:

- Digital and Omnichannel Pharmacy Proliferation

- Liberalization of Pharmacy and Drug-retail Regulations in Developing Economies

- Price Erosion from Intensifying Retail Competition and Private-label Expansion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cough, cold, and flu remedies retain the largest slice of market share at 23.1% in 2024, yet vitamins, minerals, and supplements (VMS) clock a 7.9% CAGR for 2025-2030, the fastest within the matrix. The trend reflects post-pandemic immunity consciousness and a broader pivot from treatment to prevention. A notable inference is that VMS branding increasingly centers on functional outcomes such as "sleep quality" or "stress balance," mimicking the precision-messaging language long used in the tech sector to articulate user benefits rather than technical specs.

Manufacturers are increasingly focusing on condition-specific formulations that target emerging consumer concerns such as stress management, sleep quality, and cognitive performance, creating differentiated positioning in an increasingly crowded marketplace.

Tablets still account for 38.7% of the market in 2024, but gummies and chewables expand at 9.8% CAGR. The adhesion of confectionery formats to healthcare illustrates how sensory experience can dislodge entrenched dosage forms. Manufacturers now invest in gelatin-free plant bases and reduced sugar profiles to appeal to health-conscious adults, not just children. This pivot underlines a strategic insight: taste and texture are becoming table-stakes product attributes, erasing the historical divide between therapeutic efficacy and consumer indulgence.

The innovation pipeline for OTC formulations continues to expand, with transdermal patches gaining traction for consistent drug delivery and orally disintegrating formats addressing swallowing difficulties in pediatric and geriatric populations.

The Over the Counter Drugs Market is Segmented by Product Type (Cough, Cold, and Flu, Analgesics, and More), Formulation Type (Tablets, Capsules and More), Distribution Channel (Hospital Pharmacies, Retail Chain Pharmacies, and More), Age Group (Pediatrics (0-14 Yrs), and More), Source (Chemical-Based and Herbal & Natural) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Market share leadership at 34.8% in 2024 is underpinned by high out-of-pocket costs that foster self-medication, robust pharmacy chains, and a favorable regulatory climate for Rx-to-OTC switches. The FDA's ACNU framework, operational since January 2025, allows digital tools to guide self-selection for more complex molecules, a policy shift that effectively converts software into a regulatory compliance mechanism. This dynamic nudges tech partners into the core of drug-commercialization strategies.

At an 8.7% CAGR, Asia-Pacific represents the fastest-growing regional chunk through 2030, driven by rising disposable income and growing middle-class aspirations. China's National Medical Products Administration lists more than 5,000 registered OTC products, including over 800 switches from prescription status. The sharpening competitive stakes spur multinational firms to localize not just packaging language but also dose strengths aligned with regional clinical guidelines-an adaptation that historically lagged behind marketing localization.

Most jurisdictions permit online sales and refrain from price controls, yet many still restrict non-pharmacy retail to safeguard dispensing oversight. The fragmented rulebook obliges manufacturers to maintain country-specific SKU variants, which inflates inventory complexity but allows micro-targeted marketing claims attuned to local health concerns. A sophisticated takeaway emerges: agile supply chains that use postponement strategies, delaying final packaging until country allocation, is now a material competitive advantage in Europe.

- Kenvue Brands LLC

- Bayer

- Haleon Group

- Sanofi

- Reckitt Benckiser Group

- Pfizer

- Viatris

- Perrigo Company

- Takeda Pharmaceuticals

- Boehringer Ingelheim

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

- Glenmark Pharmaceuticals

- Dr. Reddy's Laboratories

- Piramal Enterprises Ltd.

- Church & Dwight

- Procter & Gamble

- Prestige Consumer Healthcare

- Hisamitsu Pharmaceutical

- Lupin

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Consumer Preference for Self-Care and Preventive Health

- 4.2.2 Continued Rx-to-OTC Switches Across Multiple Therapeutic Classes

- 4.2.3 Proliferation of Digital & Omnichannel Pharmacy Platforms

- 4.2.4 Liberalization of Pharmacy & Drug Retail Regulations in Developing Economies

- 4.2.5 Rapidly Ageing Population Elevating Demand for Chronic OTC Management

- 4.2.6 Post-Pandemic Focus on Respiratory & Immunity Products

- 4.3 Market Restraints

- 4.3.1 Counterfeit & Substandard Products Undermining Brand Trust in Emerging Markets

- 4.3.2 Price Erosion from Intensifying Retail Competition & Private-Label Expansion

- 4.3.3 Safety Concerns over Misuse and Adverse Events Limiting Category Expansion

- 4.3.4 Tightening Regulatory Surveillance and Track-and-Trace Mandates Increasing Compliance Costs

- 4.4 Supply-Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Cough, Cold & Flu

- 5.1.2 Analgesics

- 5.1.3 Gastrointestinal

- 5.1.4 Dermatology

- 5.1.5 Vitamins, Minerals & Supplements (VMS)

- 5.1.6 Weight Management

- 5.1.7 Ophthalmic

- 5.1.8 Sleep Aids

- 5.1.9 Oral Care

- 5.1.10 Smoking Cessation

- 5.1.11 Antihistamines / Allergy

- 5.1.12 Ear Care

- 5.1.13 Wound Care

- 5.1.14 Other Products

- 5.2 By Formulation Type

- 5.2.1 Tablets

- 5.2.2 Capsules & Softgels

- 5.2.3 Liquids & Syrups

- 5.2.4 Powders & Granules

- 5.2.5 Ointments & Creams

- 5.2.6 Sprays & Inhalers

- 5.2.7 Gummies & Chewables

- 5.2.8 Transdermal Patches

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Chain Pharmacies

- 5.3.3 Independent Pharmacies & Drugstores

- 5.3.4 Online Pharmacies

- 5.3.5 Other Channels

- 5.4 By Age Group

- 5.4.1 Pediatrics (0-14 yrs)

- 5.4.2 Adults (15-64 yrs)

- 5.4.3 Geriatrics (65+ yrs)

- 5.5 By Source

- 5.5.1 Chemical-based

- 5.5.2 Herbal & Natural

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Kenvue Brands LLC

- 6.3.2 Bayer AG

- 6.3.3 Haleon Group

- 6.3.4 Sanofi S.A.

- 6.3.5 Reckitt Benckiser Group plc

- 6.3.6 Pfizer Inc.

- 6.3.7 Viatris Inc.

- 6.3.8 Perrigo Company plc

- 6.3.9 Takeda Pharmaceutical Co. Ltd.

- 6.3.10 Boehringer Ingelheim International GmbH

- 6.3.11 Sun Pharmaceutical Industries Ltd.

- 6.3.12 Teva Pharmaceutical Industries Ltd.

- 6.3.13 Glenmark Pharmaceuticals Ltd.

- 6.3.14 Dr. Reddy's Laboratories Ltd.

- 6.3.15 Piramal Enterprises Ltd.

- 6.3.16 Church & Dwight Co. Inc.

- 6.3.17 Procter & Gamble Co.

- 6.3.18 Prestige Consumer Healthcare Inc.

- 6.3.19 Hisamitsu Pharmaceutical Co. Inc.

- 6.3.20 Lupin Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment