|

시장보고서

상품코드

1849844

유럽의 그린 데이터센터 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Europe Green Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

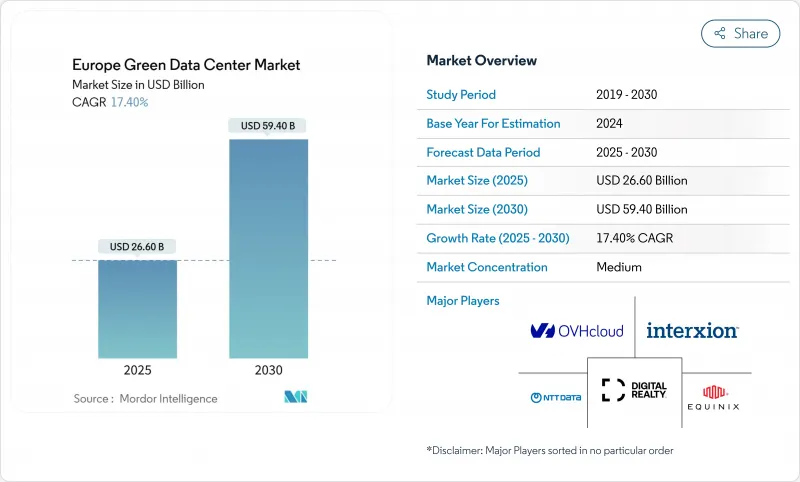

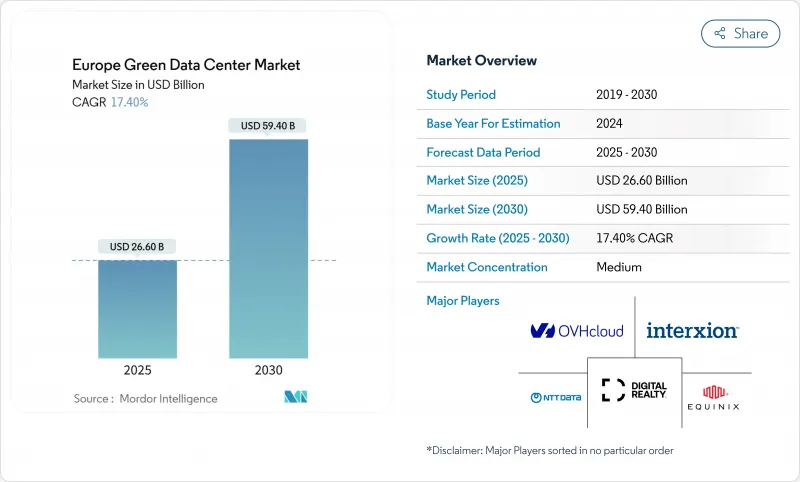

유럽의 그린 데이터센터 시장은 2025년에 266억 달러로 평가되었고, 2030년에 CAGR은 17.4%를 나타낼 것으로 예측되며, 594억 달러에 이를 전망입니다.

EU 그린딜에 따른 강화된 규제 목표, 차세대 AI 인프라에 대한 대규모 투자, 전사적 디지털 전환은 용량 확대와 지속가능성 혁신을 동시에 뒷받침하는 지속적인 수요 곡선을 공고히 하고 있습니다. 에너지 효율 지침이 500kW 이상 시설에 에너지 지표 보고 및 재생에너지 기준 충족을 요구함에 따라 운영사들은 초고효율 전력 및 냉각 기술에 자본을 집중하고 있습니다. 북유럽의 전력구매계약(PPA) 인센티브는 저탄소 전력을 보장하며 운영사가 물리적 한계에 근접한 전력사용효율(PUE) 비율을 달성할 수 있게 합니다. 한편 FLAP-D 허브는 전력망 지연에도 불구하고 상호연결 밀도 측면에서 여전히 매력적입니다. 모니터링, 수명주기 관리, 규정 준수 보고를 통합 제공하는 서비스 제공업체들은 하드웨어 중심 업체들보다 빠르게 성장하고 있으며, 이는 일회성 구축에서 지속적인 최적화로 전환되는 추세를 반영합니다. 범위 3 보고 지원과 고밀도 액체 냉각을 연계할 수 있는 공급업체가 가장 큰 상승 여력을 확보할 수 있을 것입니다.

유럽의 그린 데이터센터 시장 동향 및 인사이트

클라우드 및 빅데이터 워크로드 급증

2024년 유럽 데이터 센터 전력 소비의 8%를 차지한 AI 및 머신러닝 작업은 2028년까지 20%에 달할 전망으로, 공기보다 15-25배 빠르게 열을 제거하는 액체 냉각 기술의 급속한 도입을 촉진하고 있습니다. 마이크로소프트는 2026년까지 20,000 개 이상의 GPU를 수용하는 리즈의 AI 전용 캠퍼스에 25억 달러를 투자하기로 결정했으며, 이는 하이퍼스케일러들이 고밀도 랙을 중심으로 시설 아키텍처를 재구성하는 방식을 보여줍니다. 엣지에서 발생하는 소규모 추론 워크로드는 중앙 훈련 클러스터에 연결된 분산형 마이크로 사이트를 생성하여 지연 시간을 줄이면서 재생 에너지 목표를 유지하고 있습니다. 기업 클라우드 전략에는 이제 정량적 지속가능성 지표가 포함됩니다. 유럽 사업자의 38%가 2024년 AI 성장과 탄소 감축 약속을 균형 있게 추진하기 위해 친환경 시설에 투자했습니다. 액체 냉각 준비 설계와 랙 단위 열 재사용은 성능과 규정 준수 이점을 동시에 제공하여 단기 수요 형성에서 주도적 위치를 공고히 합니다.

EU 그린딜 및 Fit-for-55 의무

에너지 효율 지침은 500kW 이상 데이터센터에 연간 자원 지표 공개와 2030년까지 에너지 소비 11.7% 감축을 의무화합니다. 독일 에너지 효율법은 2026년 7월 이후 신축 시설에 PUE 1.2 상한선을 설정하고 2027년까지 100% 재생에너지 전력 사용을 의무화합니다. 2024년 9월 시행되는 범유럽 지속가능성 평가 프레임워크는 운영사가 성과를 벤치마킹하고 기업지속가능성보고지침(CSRD) 적용 기업의 구매 우선권을 확보할 수 있게 합니다. 규정 준수 비용이 제품 혁신을 촉진하고 있습니다. 이퀴닉스는 시설 PUE를 낮추면서 인근 주택을 난방하는 폐열 네트워크를 시범 운영 중입니다. 투명한 지표를 입증할 수 있는 운영사는 기업 RFP에서 경쟁 우위를 점하며, 자동 모니터링 및 수명주기 탄소 회계 플랫폼 도입이 가속화되고 있습니다.

액체 냉각 및 현장 재생에너지의 높은 자본 지출

직접 칩 냉각 및 침지 시스템은 수명 주기 비용 절감에도 불구하고 공기 냉각보다 20-40% 더 비싸 저비용 자본이 부족한 사업자의 투자 회수 기간을 연장합니다. 20kW를 초과하는 AI 랙은 이러한 업그레이드 필요성을 증폭시키지만, 개조 작업은 바닥 평면 재구성, 전기 설비 교체, 직원 재교육을 요구합니다. 현장 태양광 또는 배터리 설치는 6개월의 허가 기간을 거쳐야 하므로 일정이 복잡해지고 보유 비용이 증가합니다. 대규모 다국적 기업들은 지속가능성 연계 대출을 통해 비용을 완화하지만, 소규모 코로케이션 업체들은 자금 조달 혁신이나 파트너십 모델이 초기 부담을 상쇄할 때까지 마진 압박 위험에 직면합니다.

부문 분석

2024년 솔루션 매출은 161억 달러로 전체 지출의 60.54%를 차지했으며, 이는 운영사들이 지침 기반 PUE 기준을 충족하기 위해 효율적인 파워 트레인, 고밀도 서버, 첨단 냉각 시스템을 도입했기 때문입니다. 유럽 그린 데이터센터 서비스 시장 규모는 105억 달러를 기록했으며, 탄소 회계, 수명 주기 모니터링, 규제 자문에 대한 수요 급증을 반영하여 2030년까지 연평균 22.1% 성장률(CAGR)을 유지할 전망입니다. 전용 시스템 통합 관행은 리모델링 공간 내에서 액체 및 공기 냉각을 조화시켜 이전 시간을 단축하면서 자원 효율성을 높입니다. 데이터센터 인프라 관리(DCIM) 소프트웨어를 통한 지속적인 모니터링은 에너지 보고를 자동화하며, 이는 EU 그린딜 하의 투명성 감사에 필수적인 전제 조건입니다. 스코프 3 추적 의무가 심화됨에 따라 공급업체 감사 및 내재 탄소 평가에 중점을 둔 전문 서비스 포트폴리오가 점유율을 확대하며, 하드웨어 교체 주기를 보완하는 서비스 주도 성숙 단계를 재확인하고 있습니다.

하이퍼스케일러는 2024년 매출의 35.2%를 차지하며 24.4% CAGR로 성장 중입니다. 재무 건전성을 활용해 재생에너지 계약을 확보하고 대규모 액체 냉각 시험을 진행하고 있습니다. 유럽 그린 데이터센터 시장에서 하이퍼스케일 캠퍼스가 차지하는 규모는 2030년까지 250억 달러를 초과할 전망이며, 전력구매계약(PPA)에 포함된 지속가능성 조항이 장기적 경쟁력을 확보하는 기반이 됩니다. 콜로케이션 제공업체들은 중견 기업을 겨냥한 재생 에너지 크레딧과 폐열 재활용 방안을 묶어 차별화하고 있습니다. 기업 온프레미스 인프라 규모는 계속 축소되지만, 지연 시간에 민감한 워크로드를 보유한 기업들은 효율적인 냉각 장비를 갖춘 엣지 노드에 의존하는 하이브리드 모델을 유지합니다. 엣지 제공업체들은 인구 밀집 지역 근처에 250kW-1MW 모듈을 배치하며, 재순환 공기 이코노마이저와 모듈형 배터리 저장 장치를 통해 규제 준수를 보장합니다. 대형 하이퍼스케일러들은 건설 단계 탄소 감축을 홍보합니다. 예를 들어 AWS는 스웨덴에서 저탄소 강재를 채택해 내재 탄소 배출량을 최대 70%까지 줄여, 소규모 경쟁사들이 따라잡기 위해 노력하는 기준을 제시했습니다.

유럽의 그린 데이터 센터 시장 세분화는 서비스(시스템 통합, 모니터링 서비스, 전문 서비스, 기타 서비스), 솔루션(전원, 서버, 관리 소프트웨어 등), 사용자(코로케이션 공급자, 클라우드 서비스 공급자, 기업), 최종 사용자 업계(의료, 금융 서비스, 정부 기관 등)로 분류합니다. 시장 예측은 금액(달러)으로 제공됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 주류 드라이버

- 클라우드와 빅데이터 워크로드 급증

- EU 그린딜과 Fit-for-55의 의무

- FLAP-D 허브에서의 하이퍼스케일 및 엣지 확장

- 주목받지 않은 드라이버

- 초저 PUE 실현을 가능케 하는 북유럽 PPA

- 지역 난방 폐열 보조금

- 스코프 3 중시의 그린 SLA 수요

- 시장 성장 억제요인

- 주류의 제약

- 액체 냉각 및 현장 재생에너지의 높은 자본 지출(CAPEX)

- 전력 부족 허브에서의 전력망 연결 지연

- 주목받지 못하는 제약요인

- 탄소강과 콘크리트의 조사

- 지속 가능한 DC 엔지니어링의 인력 부족

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 거시 경제 동향이 시장에 미치는 영향 평가

제5장 시장 규모와 성장 예측

- 컴포넌트별

- 서비스별

- 시스템 통합

- 모니터링 서비스

- 전문 서비스

- 기타 서비스

- 솔루션별

- 전력

- 냉각

- 서버

- 네트워크 장비

- 관리 소프트웨어

- 기타 솔루션

- 서비스별

- 데이터센터 유형별

- 코로케이션 공급자

- 하이퍼스케일러/클라우드 서비스 제공업체

- 기업 및 엣지

- 티어 유형별

- 티어 1 및 티어 2

- 티어 3

- 티어 4

- 업계별

- 의료

- 금융 서비스

- 정부

- 통신 및 IT

- 제조업

- 미디어 및 엔터테인먼트

- 기타 업종

- 국가별

- 독일

- 영국

- 프랑스

- 네덜란드

- 아일랜드

- 노르웨이

- 스웨덴

- 덴마크

- 스페인

- 이탈리아

- 러시아

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Equinix Inc.

- Digital Realty Trust Inc.

- NTT Global Data Centers EMEA GmbH

- Schneider Electric SE

- Fujitsu Ltd.

- Cisco Systems Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Co.

- IBM Corporation

- Eaton Corporation plc

- Vertiv Holdings Co.

- OVH Groupe SAS

- Interxion Holding NV

- Vantage Data Centers LLC

- Bulk Infrastructure AS

- Green Mountain AS

- EcoDataCenter AB

- Stack Infrastructure Inc.

- Iron Mountain Inc.

- Deep Green Data Centres Ltd.

- Verne Global Ltd.

제7장 시장 기회와 장래의 전망

HBR 25.11.12The Europe green data center market generated USD 26.6 billion in 2025 and is forecast to reach USD 59.4 billion by 2030, advancing at a 17.4% CAGR.

Heightened regulatory ambition under the EU Green Deal, hyperscale investments in next-generation AI infrastructure, and enterprise-wide digitization are reinforcing a sustained demand curve that supports both capacity growth and sustainability innovation. Operators are steering capital toward ultra-efficient power and cooling technologies as the Energy Efficiency Directive requires facilities above 500 kW to report energy metrics and meet renewable-energy thresholds. Nordic incentives for power-purchase agreements (PPAs) ensure low-carbon electricity and enable operators to post power-usage-effectiveness (PUE) ratios close to the physical minimum, while FLAP-D hubs remain attractive for interconnection density despite grid backlogs. Service providers that bundle monitoring, lifecycle management, and compliance reporting are expanding faster than hardware-centric peers, reflecting the shift from one-off builds to continuous optimization. Vendors able to align Scope 3 reporting support with high-density liquid cooling stand to capture the strongest upside.

Europe Green Data Center Market Trends and Insights

Cloud & Big-Data Workload Surge

AI and machine-learning tasks consumed 8% of data-center electricity in Europe during 2024 and may hit 20% by 2028, prompting rapid adoption of liquid cooling that removes heat 15-25 times faster than air. Microsoft earmarked USD 2.5 billion for an AI-focused campus in Leeds hosting more than 20,000 GPUs by 2026, signalling how hyperscalers reshape facility architecture around high-density racks. Smaller inference workloads at the edge are spawning distributed micro-sites tethered to central training clusters, reducing latency while sustaining renewable-energy targets. Enterprise cloud strategies now include quantitative sustainability metrics; 38% of European operators invested in greener facilities in 2024 to balance AI growth with carbon-reduction pledges. Liquid-ready designs and rack-level heat reuse deliver both performance and compliance benefits that reinforce the driver's position in near-term demand formation.

EU Green Deal & Fit-for-55 Mandates

The Energy Efficiency Directive obliges data centers above 500 kW to publish annual resource metrics and to cut energy consumption by 11.7% by 2030. Germany's Energy Efficiency Act sets a PUE ceiling of 1.2 for new builds from July 2026 and a 100% renewable-electricity mandate by 2027. A pan-EU sustainability-rating framework entering force in September 2024 enables operators to benchmark performance and secure procurement preference from corporates bound by the Corporate Sustainability Reporting Directive. Compliance spending is unlocking product innovation: Equinix is piloting waste-heat networks that warm neighboring homes while lowering facility PUE. Operators able to evidence transparent metrics gain a competitive edge in enterprise RFPs, intensifying adoption of automated monitoring and lifecycle-carbon accounting platforms.

High CAPEX for Liquid-Cooling & On-site RE

Direct-to-chip and immersion systems cost 20-40% more than air cooling despite life-cycle savings, stretching payback timelines for operators lacking low-cost capital. AI racks topping 20 kW magnify the need for these upgrades, yet retrofit works demand floorplate reconfiguration, electrical refits, and staff reskilling. On-site solar or battery installations face six-month permitting windows, complicating schedules and raising holding costs. Larger multinationals mitigate expense through sustainability-linked loans, but smaller colocation players risk margin compression until financing innovation or partnership models neutralize upfront burdens.

Other drivers and restraints analyzed in the detailed report include:

- Hyperscale & Edge Build-outs in FLAP-D Hubs

- Nordic PPAs Enabling Ultra-Low PUE

- Grid-Connection Delays in Power-Scarce Hubs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions revenue reached USD 16.1 billion in 2024, equal to 60.54% of overall expenditure, as operators procured efficient power trains, high-density servers, and advanced cooling to satisfy Directive-driven PUE benchmarks. Europe green data center market size for services registered USD 10.5 billion and is on track for a 22.1% CAGR to 2030, reflecting surging demand for carbon accounting, lifecycle monitoring, and regulatory advisory. Dedicated system-integration practices align liquid and air cooling within retrofit footprints, compressing migration time while raising resource efficiency. Continuous monitoring via data-center-infrastructure-management (DCIM) software automates energy reporting, a mandatory prerequisite for transparency audits under the EU Green Deal. As Scope 3 tracking obligations deepen, professional-services portfolios focused on supplier audits and embodied-carbon assessments capture an incremental share, reaffirming a services-led maturity phase that complements hardware refresh cycles.

Hyperscalers held 35.2% of 2024 revenue and expand at 24.4% CAGR, capitalizing on balance-sheet strength to lock renewable contracts and trial liquid-cooling at scale. The Europe green data center market size attributed to hyperscale campuses is projected to exceed USD 25 billion by 2030, with sustainability clauses embedded in power-purchase agreements anchoring long-term competitiveness. Colocation providers differentiate by bundling renewable credits and waste-heat-reuse schemes that appeal to mid-sized enterprises. Enterprise on-premises footprints continue to shrink, yet firms with latency-sensitive workloads maintain hybrid models that lean on edge nodes outfitted with efficient cooling. Edge providers deploy 250 kW-1 MW modules near population centers, ensuring regulatory compliance through recycled-air economizers and modular battery storage. Larger hyperscalers publicize construction-phase carbon cuts, such as AWS adopting low-carbon steel in Sweden to trim embodied emissions by up to 70%, setting a bar smaller competitors strive to match.

Europe Green Data Center Market Report Segments the Industry Into Service (System Integration, Monitoring Services, Professional Services, Other Services), Solution (Power, Servers, Management Software, and More), User (Colocation Providers, Cloud Service Providers, Enterprises), and End-User Industry (Healthcare, Financial Services, Government, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Equinix Inc.

- Digital Realty Trust Inc.

- NTT Global Data Centers EMEA GmbH

- Schneider Electric SE

- Fujitsu Ltd.

- Cisco Systems Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Co.

- IBM Corporation

- Eaton Corporation plc

- Vertiv Holdings Co.

- OVH Groupe SAS

- Interxion Holding N.V.

- Vantage Data Centers LLC

- Bulk Infrastructure AS

- Green Mountain AS

- EcoDataCenter AB

- Stack Infrastructure Inc.

- Iron Mountain Inc.

- Deep Green Data Centres Ltd.

- Verne Global Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream Drivers

- 4.2.2 Cloud and Big-Data Workload Surge

- 4.2.3 EU Green Deal and Fit-for-55 Mandates

- 4.2.4 Hyperscale and Edge Build-outs in FLAP-D Hubs

- 4.2.5 Under-the-Radar Drivers

- 4.2.6 Nordic PPAs Enabling Ultra-Low PUE

- 4.2.7 District-Heating Waste-Heat Subsidies

- 4.2.8 Scope-3-Focused Green SLAs Demand

- 4.3 Market Restraints

- 4.3.1 Mainstream Restraints

- 4.3.2 High CAPEX for Liquid-Cooling and On-site RE

- 4.3.3 Grid-Connection Delays in Power-Scarce Hubs

- 4.3.4 Under-the-Radar Restraints

- 4.3.5 Embodied-Carbon Steel and Concrete Scrutiny

- 4.3.6 Sustainable-DC Engineering Talent Shortage

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Assessment of the impact of Macro Economic Trends on the Market

5 Market Size and Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 By Service

- 5.1.1.1 System Integration

- 5.1.1.2 Monitoring Services

- 5.1.1.3 Professional Services

- 5.1.1.4 Other Services

- 5.1.2 By Solution

- 5.1.2.1 Power

- 5.1.2.2 Cooling

- 5.1.2.3 Servers

- 5.1.2.4 Networking Equipment

- 5.1.2.5 Management Software

- 5.1.2.6 Other Solutions

- 5.1.1 By Service

- 5.2 By Data Center Type

- 5.2.1 Colocation Providers

- 5.2.2 Hyperscalers/Cloud Service Providers

- 5.2.3 Enterprise and Edge

- 5.3 By Tier Type

- 5.3.1 Tier 1 and 2

- 5.3.2 Tier 3

- 5.3.3 Tier 4

- 5.4 By Industry Vertical

- 5.4.1 Healthcare

- 5.4.2 Financial Services

- 5.4.3 Government

- 5.4.4 Telecom and IT

- 5.4.5 Manufacturing

- 5.4.6 Media and Entertainment

- 5.4.7 Other Verticals

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Netherlands

- 5.5.5 Ireland

- 5.5.6 Norway

- 5.5.7 Sweden

- 5.5.8 Denmark

- 5.5.9 Spain

- 5.5.10 Italy

- 5.5.11 Russia

- 5.5.12 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global?level Overview, Market?level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Equinix Inc.

- 6.4.2 Digital Realty Trust Inc.

- 6.4.3 NTT Global Data Centers EMEA GmbH

- 6.4.4 Schneider Electric SE

- 6.4.5 Fujitsu Ltd.

- 6.4.6 Cisco Systems Inc.

- 6.4.7 Dell Technologies Inc.

- 6.4.8 Hewlett Packard Enterprise Co.

- 6.4.9 IBM Corporation

- 6.4.10 Eaton Corporation plc

- 6.4.11 Vertiv Holdings Co.

- 6.4.12 OVH Groupe SAS

- 6.4.13 Interxion Holding N.V.

- 6.4.14 Vantage Data Centers LLC

- 6.4.15 Bulk Infrastructure AS

- 6.4.16 Green Mountain AS

- 6.4.17 EcoDataCenter AB

- 6.4.18 Stack Infrastructure Inc.

- 6.4.19 Iron Mountain Inc.

- 6.4.20 Deep Green Data Centres Ltd.

- 6.4.21 Verne Global Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment