|

시장보고서

상품코드

1849861

WiGig(와이기그) : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)WiGig - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

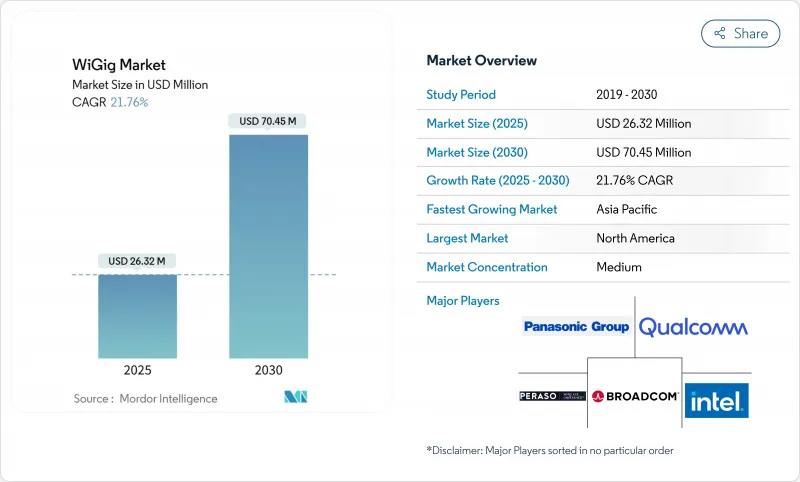

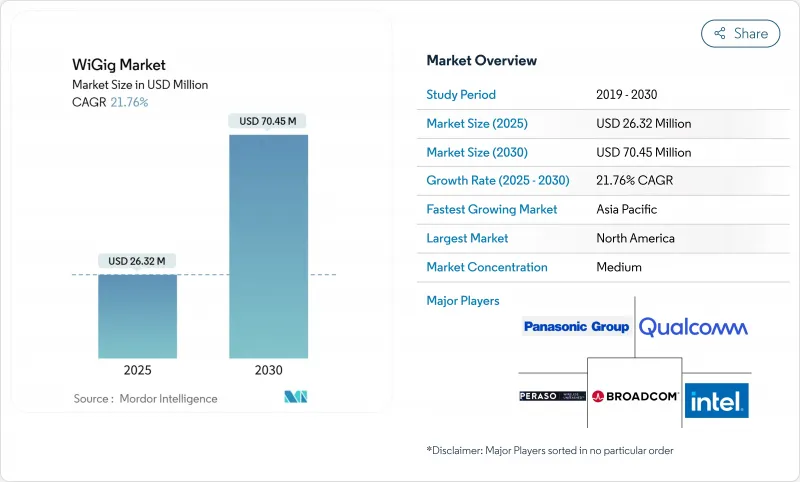

WiGig(와이기그) 시장 규모는 2025년에 263억 2,000만 달러로 평가되었고, 2030년에 704억 5,000만 달러로 확대될 것으로 예측되며, 이 기간의 CAGR은 21.76%를 나타낼 전망입니다.

상업적 추동력이 틈새 무선 도킹 허브에서 Wi-Fi 7 트라이밴드 액세스 포인트, 프리미엄 노트북, 초기 6G 백홀 시험으로의 광범위한 통합으로 전환되고 있습니다. 4K/8K 비디오, AR/VR 워크로드, 엣지 AI 트래픽에 대한 수요가 2.4GHz 및 5/6GHz 대역의 용량을 한계까지 끌어올리면서, 지연 시간에 민감한 애플리케이션에는 60GHz 대역의 처리량이 필수불가결해졌습니다. 동시에 반도체 업체들은 전력 소모를 줄이면서 폼 팩터를 축소하는 시스템 온 칩(SoC) 솔루션을 통해 설계 주기를 간소화하고 있으며, 이는 스마트폰과 초박형 노트북의 필수 조건입니다. 마지막으로 갈륨 공급과 관련된 지정학적 압박과 지역별 전력 제한 규정의 차이는 OEM 업체들이 제2 공급업체를 확보하고 규제 당국에 60GHz 프레임워크의 조화를 촉구하도록 유도하고 있으며, 이는 정책과 기술이 WiGig 시장 궤적을 형성할 것임을 시사합니다.

세계의 WiGig 시장 동향 및 인사이트

4K/8K 및 XR 스트리밍 수요 급증

초고화질 콘텐츠는 스트림당 25-100 Mbps의 지속적인 대역폭을 요구하며, 현재 가정은 4K, 8K, AR 작업을 동시에 실행합니다. 2.4GHz 및 5/6GHz 대역의 트래픽이 간섭과 제한된 연속 채널 폭에 직면하는 상황에서 60GHz 대역은 여유 공간을 제공합니다. 북미와 일본에서는 유료 TV 사업자들이 이미 기존 Wi-Fi의 한계를 시험하는 8K 스포츠 중계를 번들로 제공하고 있습니다. 이에 따라 장치 OEM 업체들은 프리미엄 TV, 콘솔, 헤드셋이 유선 연결 없이도 10ms 미만의 지연 시간을 유지할 수 있도록 멀티기가비트 라디오를 내장하고 있습니다. XR 헤드셋이 기업 교육 및 소비자 게임 분야에서 확대됨에 따라 안정적인 무선 전송 속도가 구매 기준으로 부상하며, 이는 직접적으로 WiGig의 잠재 시장 규모를 확대하고 있습니다.

Wi-Fi 7 AP에 60GHz 트라이밴드 무선 통합

액세스포인트 공급업체들은 2.4GHz, 5/6GHz, 60GHz를 단일 플랫폼으로 통합하는 Wi-Fi 7 칩셋을 출시 중입니다. 멀티링크 운영은 세션을 실시간으로 전환하여 근거리 장치는 60GHz로 이동하는 동시에 원거리 클라이언트는 저주파 대역에 잔류할 수 있게 합니다. 이 아키텍처는 고밀도 캠퍼스의 케이블링 비용을 절감하고, 대역 전환을 최적화하는 네트워크 분석 도구로부터 추가 소프트웨어 수익을 창출합니다. 10Gbps 광섬유 업링크를 구축하는 유럽 클라우드 사무실들은 트라이밴드 WiGig를 피크 시간대 혼잡 대비 수단으로 활용하며, 인프라 통합이 WiGig를 사치스러운 추가 기능에서 필수 기본 항목으로 전환하는 방식을 보여줍니다.

제한된 범위와 엄격한 직선 시야

60GHz 대역에서는 산소 흡수 및 벽 감쇠로 인해 링크 거리가 약 10미터로 제한되므로, 모든 회의실이나 공장 셀에 액세스 포인트를 설치해야 합니다. 유리 파티션조차도 처리량을 절반으로 줄일 수 있으며, 이동하는 사람들은 빔 추적 알고리즘이 필요한 페이딩을 유발합니다. 자율주행차 현장 테스트에서 작은 장애물이 프레넬 영역을 차단할 때 패킷 손실 급증이 관찰되어, WiGig 도입 시 정밀한 현장 조사가 필요함을 입증합니다. 이러한 제약으로 인해 해당 기술은 고밀도 장소나 고정 설치 환경으로 제한되며, 이는 소비자 시장에서의 광범위한 채택을 저해하고 대중 시장 가정용 라우터에서의 WiGig 시장 전망을 축소시킵니다.

부문 분석

2024년 디스플레이 장치가 WiGig 시장의 46.0%를 차지하며, 무선 모니터, 도킹 스테이션, AR/VR 헤드셋이 여전히 단기 수익의 핵심임을 입증했습니다. 이 하위 부문은 깔끔한 게이밍 공간을 원하는 가정과 핫데싱 레이아웃으로 전환하는 사무실의 수요로 혜택을 받습니다. 듀얼 4K 화면과 SSD급 주변장치를 지원하는 무선 허브는 이미 프리미엄 기업용 번들에 포함되어 있으며, 이는 신규 구축 시 USB-C 케이블링보다 WiGig가 ‘한 번 설계, 다중 배포’ 효율성을 제공함을 보여줍니다. AR/VR 헤드셋 제조사들은 메스꺼움을 유발하는 지연 현상을 피하기 위해 60GHz를 활용하며, 향후 출시될 혼합현실 장치들이 단위 판매량을 더욱 끌어올릴 전망입니다. TV와 프로젝터는 거실 전체에 압축되지 않은 8K 스트리밍을 위해 WiGig를 통합하지만, 단일 벽면만으로도 수신에 장애가 발생할 수 있어 채택이 더딘 상황입니다.

네트워크 인프라 장비는 28.40%의 연평균 성장률(CAGR)로 가장 빠르게 성장하는 분야로, 기업 리프레시 주기에 맞춰 출시되는 Wi-Fi 7 트라이밴드 액세스 포인트가 이 추세를 주도하고 있습니다. 공장 내 엣지 컴퓨팅 노드는 이제 광케이블 매설을 우회하기 위해 60GHz 백홀을 활용하여 설치 리드타임을 최대 70%까지 단축합니다. 도시 키오스크 업체들은 광섬유 공사 허가 절차로 인해 수개월이 추가되는 도심 밀집 지역의 팝업형 광대역 서비스에 60GHz 무선 기술을 실험 중입니다. 초기 측정 결과 시야가 확보된 경우 링크 가용성이 99% 이상으로 나타나, 백홀이 WiGig 시장의 고수익 인접 사업이 될 수 있음을 입증했습니다.

시스템 온 칩(SoC) 설계는 2024년 WiGig 시장의 58.0% 점유율을 차지했으며, 2030년까지 연평균 23.0% 성장할 것으로 전망됩니다. 통합 다이(die)는 베이스밴드, RF 프런트엔드, 전력 관리를 통합하여 기판 공간을 최대 30% 절감하고 스마트폰 배터리 수명을 연장합니다. 파운드리 업체들이 3nm 미만 노드를 완성함에 따라 60GHz 블록 추가의 증분 비용이 감소하여 중급 장치에서의 적용률이 가속화되고 있습니다. 퀄컴의 최신 플랫폼은 WiGig, 6GHz Wi-Fi, 블루투스 LE 오디오, 5G 라디오를 하나의 기판에 통합하여 공급업체 인증 주기를 분기에서 주로 단축시켰습니다.

기존 보드에 드롭인 모듈이 필요하거나 산업용 장치에 견고한 패키지가 요구되는 경우, 개별 집적 회로 구현 방식이 여전히 유효합니다. 예를 들어 의료 영상 카트는 전체 메인보드 재설계 없이 60GHz 카드를 개조할 수 있습니다. 인텔의 18A 로드맵은 단일 칩 아키텍처와 타일 기반 아키텍처를 모두 목표로 하여 OEM이 고성능 CPU 코어와 특수 라디오 타일을 혼합할 수 있게 함으로써, 제조 기술 발전이 다양한 부품 목록 경로를 지속 가능하게 한다는 점을 강조합니다. SoC의 편의성과 개별 부품의 유연성 간 상호작용은 혁신 위험을 균형 있게 조정하여 WiGig 시장의 지속적인 확장을 뒷받침할 것입니다.

WiGig 시장 보고서는 제품(디스플레이 장치, 네트워크 인프라 장치 등), 기술(시스템 온 칩(SoC), 집적 회로(IC)), 주파수 대역(57-66GHz, 66-71GHz, 기타), 용도(게임 및 멀티미디어, 기업용 무선 도킹 등), 최종 사용자 산업(가전공학, 기업 및 데이터센터, 자동차 및 운송 등), 지역별로 분류됩니다.

지역 분석

북미는 2024년 WiGig 시장의 34.20%를 차지했으며, 이는 조기 기업 도입, CHIPS 법안 지원 반도체 투자, 그리고 대부분의 지역보다 높은 EIRP를 허용하는 FCC 규정 덕분입니다. 뉴욕의 금융 서비스 기업들은 부동산 밀도를 극대화하기 위해 무선 도킹을 도입하고 있으며, 서부 해안의 기술 캠퍼스들은 애자일 작업 공간에 60GHz 링크를 활용하고 있습니다. 캐나다는 은행 및 미디어 분야에서 미국의 패턴을 반영하는 반면, 멕시코의 마킬라도라 회랑은 수출 제조 경쟁력을 높이기 위해 WiGig 기반 AGV 차량을 시범 운영 중입니다.

아시아태평양 지역은 2030년까지 연평균 23.50% 성장률로 성장 동력입니다. 일본의 네트워킹 OEM 업체들은 WiGig 라디오를 내장한 트라이밴드 Wi-Fi 7 액세스 포인트를 최초로 인증했으며, 도쿄의 초기 지자체 도입은 대규모 행사에 앞서 경기장 중앙 통로를 대상으로 합니다. 중국 가전 대기업들은 과열된 국내 시장에서 차별화를 위해 TV와 노트북에 60GHz 기능을 탑재하고 있으나, 수출 통관 시 갈륨 공급망 관련 지정학적 역풍에 직면할 수 있습니다. 한국은 프리미엄 스마트폰에 WiGig를 번들로 제공하며 고밀도 5G 백본을 활용한 트라이밴드 오프로드에 주력하고, 싱가포르는 금융지구 스마트 가로등에 60GHz 링크 시범 운영을 통해 지역 전체의 디지털 전환 추진력을 강조하고 있습니다.

유럽은 진척도가 제각각입니다. 독일과 영국은 결정론적 무선 기술을 기반으로 한 스마트 공장 개조에서 선도적이지만, 남유럽의 자본 지출 둔화로 지역 보급률은 세계 평균을 밑돕니다. ETSI 표준이 기술적 매개변수를 조화시키지만, EU 국가별 전력 제한 차이로 인한 추가 인증 작업이 출시를 지연시킵니다. 중동 및 아프리카는 초기 단계에 머물고 있습니다. 두바이의 핀테크 허브는 거래장 내 WiGig 적용을 검토 중이며, 남아프리카 광산에서는 실시간 시추 분석을 위한 60GHz 링크를 시험 중입니다. 그러나 자본 지출 제약과 지형적 어려움으로 단기 도입은 제한적이며, 지역 GDP와 연결성 이니셔티브가 진전됨에 따라 WiGig 시장에는 상당한 성장 여지가 남아 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 4K/8K 및 XR 스트리밍 수요의 급증

- Wi-Fi 7 AP에 WiGig 트라이밴드 라디오 통합

- WiGig 지원 노트북 및 스마트폰 부착률 상승

- 초고속 무선 도킹에 대한 기업 요구

- 60GHz 백플레인 링크를 채택하는 엣지-AI 서버

- 60GHz를 활용한 기내 연결성 시범 운영

- 시장 성장 억제요인

- 한정된 범위와 엄격한 시선

- Wi-Fi 6E/7 및 5G 밀리미터파(mmWave)에 의한 대체 위험

- 휴대용 60GHz 무선 장치의 열 설계 한계

- 분산된 60GHz EIRP 규정

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 투자분석

제5장 시장 규모와 성장 예측

- 제품별

- 디스플레이 장치

- 무선 도킹 스테이션

- AR/VR 헤드셋

- TV와 프로젝터

- 네트워크 인프라 장치

- 액세스 포인트와 라우터

- 백홀 무선

- 기타

- 디스플레이 장치

- 기술별

- 시스템 온 칩(SoC)

- 집적 회로(IC)

- 주파수 대역별

- 57-66GHz(IEEE 802.11ad)

- 66-71GHz

- 71-86GHz(IEEE 802.11ay 본딩)

- 용도별

- 게임 및 멀티미디어

- 기업용 무선 도킹

- 네트워크와 데이터 전송

- 차량 내 인포테인먼트

- 스마트 제조 및 IIoT

- 최종 사용자 업계별

- 소비자 가존

- 기업 및 데이터센터

- 자동차 및 운송

- 공업 및 제조업

- 항공우주 및 방위

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Qualcomm Technologies Inc.

- Intel Corporation

- Broadcom Inc.

- Cisco Systems Inc.

- Panasonic Holdings Corp.

- Peraso Technologies Inc.

- Blu Wireless Technology Ltd.

- Tensorcom Inc.

- Fujikura Ltd.

- Sivers Semiconductors AB

- Dell Technologies Inc.

- Lenovo Group Ltd.

- HP Development Company LP

- Samsung Electronics Co. Ltd.

- MediaTek Inc.

- Marvell Technology Inc.

- NXP Semiconductors NV

- Analog Devices Inc.

- Keysight Technologies Inc.

- LitePoint(Teradyne Inc.)

- NEC Corporation

- Qualcomm Atheros(subsidiary)

제7장 시장 기회와 장래의 전망

HBR 25.11.12The WiGig market size is valued at USD 26.32 billion in 2025 and is forecast to expand to USD 70.45 billion by 2030, translating into a 21.76% CAGR over the period.

Commercial momentum is shifting from niche wireless-docking hubs toward broad integration in Wi-Fi 7 tri-band access points, premium laptops, and early 6G backhaul trials. Demand for 4K/8K video, AR/VR workloads, and edge-AI traffic is stretching the capacity of the 2.4 GHz and 5/6 GHz bands, making 60 GHz throughput indispensable for latency-sensitive applications. At the same time, semiconductor vendors are simplifying design cycles through system-on-chip solutions that cut power draw while shrinking form factors, a prerequisite for smartphones and ultra-thin notebooks. Finally, geopolitical pressures around gallium supply and diverging regional power-limit rules are prompting OEMs to qualify second-source suppliers and lobby regulators for harmonized 60 GHz frameworks, indicating that policy as well as technology will shape the WiGig market trajectory.

Global WiGig Market Trends and Insights

Surge in 4K/8K and XR streaming demand

Ultra-high-definition content requires sustained 25-100 Mbps per stream, and households now run simultaneous 4K, 8K, and AR tasks. The 60 GHz layer supplies headroom where 2.4 GHz and 5/6 GHz traffic face interference and limited contiguous channel widths. In North America and Japan, pay-TV operators already bundle 8K sports feeds that push legacy Wi-Fi to its limits. Device OEMs therefore embed multi-gigabit radios so that premium televisions, consoles, and headsets can maintain sub-10 ms latencies without tethered links. As XR headsets scale in enterprise training and consumer gaming, dependable untethered throughput becomes a purchasing criterion, directly raising the addressable WiGig market.

Integration of 60 GHz tri-band radios in Wi-Fi 7 APs

Access-point vendors are shipping Wi-Fi 7 chipsets that aggregate 2.4 GHz, 5/6 GHz, and 60 GHz into a single platform. Multi-link operation hands sessions back and forth in real time, letting short-range devices jump to 60 GHz while distant clients remain on lower bands. This architecture reduces cabling costs for dense campuses and unlocks incremental software revenue from network-analytics tools that optimize band steering. European cloud offices deploying 10 Gbps fiber uplinks view tri-band Wi-Gig as a hedge against peak-hour congestion, underscoring how infrastructure integration converts WiGig from a luxury add-on into a baseline checklist item.

Limited range and strict line-of-sight

At 60 GHz, oxygen absorption and wall attenuation curb links to roughly 10 meters, so access points must be installed in every conference room or factory cell. Even glass partitions can halve throughput, and moving people create fading that requires beam-tracking algorithms. Field tests on autonomous vehicles show packet-loss spikes when small obstacles break Fresnel zones, reinforcing that WiGig rollouts need precise site surveys. Such constraints restrict the technology to high-density venues or fixed setups, limiting broader consumer adoption and trimming WiGig market expectations in mass-market home routers.

Other drivers and restraints analyzed in the detailed report include:

- Rising attach-rate of WiGig-enabled laptops and smartphones

- Enterprise need for ultra-fast wireless docking

- Substitution risk from Wi-Fi 6E/7 and 5G mmWave

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Display devices commanded 46.0% of the WiGig market in 2024, demonstrating how wireless monitors, docking stations, and AR/VR headsets still anchor near-term revenue. The sub-segment benefits from households seeking clutter-free gaming corners and offices migrating to hot-desking layouts. Wireless hubs that host dual 4K screens and SSD-grade peripherals already appear in premium enterprise bundles, showing that design-once, deploy-many efficiencies favor WiGig over USB-C cabling for new builds. AR/VR headset makers rely on 60 GHz to avoid nausea-inducing latency, and upcoming mixed-reality rollouts will further lift unit volumes. Televisions and projectors integrate WiGig for uncompressed 8K streams across a living room, but adoption lags because a single wall can impair reception.

Network infrastructure devices are the fastest-growing slice at 28.40% CAGR, a trajectory driven by Wi-Fi 7 tri-band access points shipping into corporate refresh cycles. Edge-compute nodes inside factories now leverage 60 GHz backhaul to sidestep fiber trenching, reducing installation lead-times by up to 70%. Municipal kiosk vendors experiment with 60 GHz radios for pop-up broadband in dense downtown corridors where digging permits add months to fiber projects. Early metrics show link availability above 99% when clear line-of-sight is maintained, validating that backhaul can be a high-margin adjacency for the WiGig market.

System-on-chip designs held 58.0% share of the WiGig market in 2024 and are projected to grow at 23.0% CAGR through 2030. Unified dies integrate baseband, RF front-end, and power management, cutting board space by up to 30% and extending smartphone battery life. As foundries perfect sub-3 nm nodes, the incremental cost of adding a 60 GHz block falls, accelerating attach rates in mid-tier devices. Qualcomm's latest platforms pack WiGig, 6 GHz Wi-Fi, Bluetooth LE Audio, and 5G radios into one substrate, reducing vendor qualification cycles from quarters to weeks.

Discrete integrated-circuit implementations remain relevant where legacy boards need drop-in modules or where industrial gear demands ruggedized packages. Medical imaging carts, for instance, retrofit 60 GHz cards without redesigning the entire motherboard. Intel's 18A roadmap targets both monolithic and tile-based architectures so that OEMs can mix high-performance CPU cores with specialized radio tiles, underscoring how manufacturing advances keep multiple bill-of-materials paths viable. The interplay between SoC convenience and discrete flexibility should balance innovation risk, supporting continued WiGig market expansion.

The WiGig Market Report is Segmented by Product (Display Devices, Network Infrastructure Devices, and More), Technology (System-On-Chip (SoC) and Integrated Circuit (IC)), Frequency Band (57-66 GHz, 66-71 GHz, and More), Application (Gaming and Multimedia, Enterprise Wireless Docking, and More), End-User Industry (Consumer Electronics, Enterprise and Datacenter, Automotive and Transportation, and More), and Geography.

Geography Analysis

North America accounted for 34.20% of the WiGig market in 2024, owing to early enterprise adoption, CHIPS-Act-funded semiconductor investments, and FCC rules that allow higher EIRP than most regions. Financial-services firms in New York deploy wireless docking to maximize real-estate density, and West-Coast tech campuses use 60 GHz links in agile work pods. Canada mirrors U.S. patterns in banking and media verticals, while Mexico's maquiladora corridor pilots WiGig-based AGV fleets to raise export manufacturing competitiveness.

Asia Pacific is the growth engine with a 23.50% CAGR to 2030. Japan's networking OEMs were the first to certify tri-band Wi-Fi 7 access points that embed WiGig radios; early municipal deployments in Tokyo target stadium concourses ahead of large-scale events.China's consumer-electronics giants build 60 GHz capability into televisions and laptops to differentiate in crowded domestic channels, although export clearance may face geopolitical headwinds tied to gallium supply chains. South Korea bundles WiGig in premium smartphones, leveraging its dense 5G backbone for tri-band offload, while Singapore pilots 60 GHz links in financial district smart lamp-posts, underscoring region-wide digital-transformation momentum.

Europe exhibits heterogeneous progress. Germany and the United Kingdom lead with smart-factory retrofits that rely on deterministic wireless, but Southern Europe's slower capital-spending pulls regional penetration below global averages. ETSI standards harmonize technical parameters, yet power-limit disparities across EU nations raise extra certification work that delays rollouts. The Middle East and Africa remain nascent; Dubai's fintech hubs evaluate WiGig for trading floors, and South-Africa mines test 60 GHz links for real-time drilling analytics. However, capex constraints and terrain challenges temper near-term uptake, leaving considerable headroom for the WiGig market as regional GDP and connectivity initiatives advance.

- Qualcomm Technologies Inc.

- Intel Corporation

- Broadcom Inc.

- Cisco Systems Inc.

- Panasonic Holdings Corp.

- Peraso Technologies Inc.

- Blu Wireless Technology Ltd.

- Tensorcom Inc.

- Fujikura Ltd.

- Sivers Semiconductors AB

- Dell Technologies Inc.

- Lenovo Group Ltd.

- HP Development Company LP

- Samsung Electronics Co. Ltd.

- MediaTek Inc.

- Marvell Technology Inc.

- NXP Semiconductors N.V.

- Analog Devices Inc.

- Keysight Technologies Inc.

- LitePoint (Teradyne Inc.)

- NEC Corporation

- Qualcomm Atheros (subsidiary)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in 4K/8K and XR streaming demand

- 4.2.2 Integration of WiGig tri-band radios in Wi-Fi 7 APs

- 4.2.3 Rising attach-rate of WiGig-enabled laptops and smartphones

- 4.2.4 Enterprise need for ultra-fast wireless docking

- 4.2.5 Edge-AI servers adopting 60 GHz back-plane links

- 4.2.6 In-flight cabin connectivity pilots at 60 GHz

- 4.3 Market Restraints

- 4.3.1 Limited range and strict line-of-sight

- 4.3.2 Substitution risk from Wi-Fi 6E/7 and 5G mmWave

- 4.3.3 Thermal design limits in handheld 60 GHz radios

- 4.3.4 Fragmented 60 GHz EIRP regulations

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 Display Devices

- 5.1.1.1 Wireless Docking Stations

- 5.1.1.2 AR/VR Headsets

- 5.1.1.3 Televisions and Projectors

- 5.1.2 Network Infrastructure Devices

- 5.1.2.1 Access Points and Routers

- 5.1.2.2 Backhaul Radios

- 5.1.3 Others

- 5.1.1 Display Devices

- 5.2 By Technology

- 5.2.1 System-on-Chip (SoC)

- 5.2.2 Integrated Circuit (IC)

- 5.3 By Frequency Band

- 5.3.1 57-66 GHz (IEEE 802.11ad)

- 5.3.2 66-71 GHz

- 5.3.3 71-86 GHz (IEEE 802.11ay bonded)

- 5.4 By Application

- 5.4.1 Gaming and Multimedia

- 5.4.2 Enterprise Wireless Docking

- 5.4.3 Networking and Data Transfer

- 5.4.4 In-vehicle Infotainment

- 5.4.5 Smart Manufacturing / IIoT

- 5.5 By End-user Industry

- 5.5.1 Consumer Electronics

- 5.5.2 Enterprise and Datacenter

- 5.5.3 Automotive and Transportation

- 5.5.4 Industrial and Manufacturing

- 5.5.5 Aerospace and Defense

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Qualcomm Technologies Inc.

- 6.4.2 Intel Corporation

- 6.4.3 Broadcom Inc.

- 6.4.4 Cisco Systems Inc.

- 6.4.5 Panasonic Holdings Corp.

- 6.4.6 Peraso Technologies Inc.

- 6.4.7 Blu Wireless Technology Ltd.

- 6.4.8 Tensorcom Inc.

- 6.4.9 Fujikura Ltd.

- 6.4.10 Sivers Semiconductors AB

- 6.4.11 Dell Technologies Inc.

- 6.4.12 Lenovo Group Ltd.

- 6.4.13 HP Development Company LP

- 6.4.14 Samsung Electronics Co. Ltd.

- 6.4.15 MediaTek Inc.

- 6.4.16 Marvell Technology Inc.

- 6.4.17 NXP Semiconductors N.V.

- 6.4.18 Analog Devices Inc.

- 6.4.19 Keysight Technologies Inc.

- 6.4.20 LitePoint (Teradyne Inc.)

- 6.4.21 NEC Corporation

- 6.4.22 Qualcomm Atheros (subsidiary)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment