|

시장보고서

상품코드

1849868

지리공간 분석 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Geospatial Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

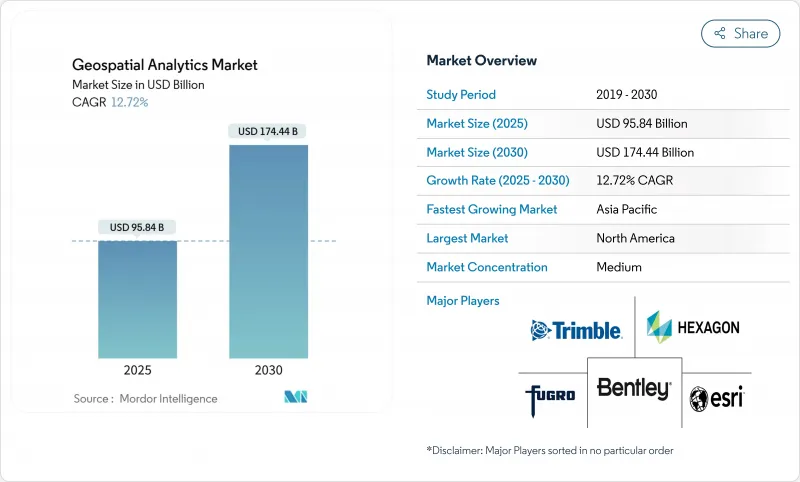

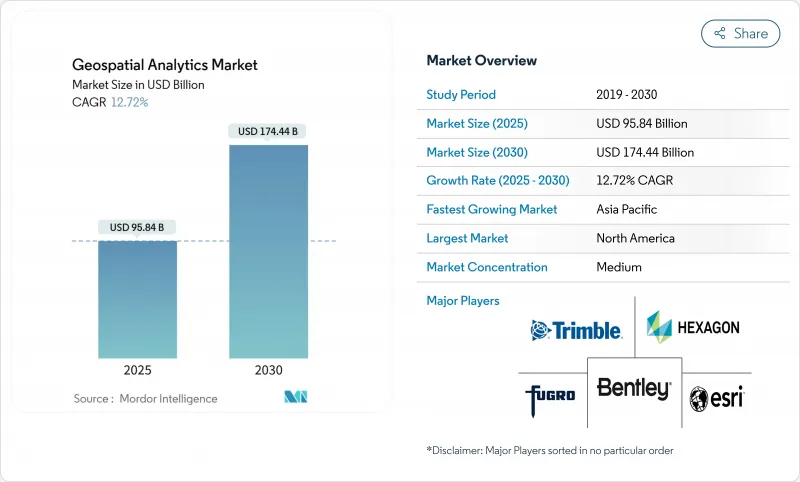

지리공간 분석 시장의 2025년 시장 규모는 958억 4,000만 달러로, 2030년에는 1,744억 4,000만 달러에 이를 것으로 예측되며, CAGR은 12.72%를 나타낼 전망입니다.

위치 기반 인사이트에 대한 수요 증가, 위성 별자리의 급속한 출시, 스마트 시티 투자로 이 분야는 디지털 전환의 필수 기둥으로 자리매김하고 있습니다. 기업은 인공지능이 특징 추출과 예측 모델링을 자동화함에 따라 공간 인텔리전스를 활용하여 업무 효율성을 높이고, 위험을 줄이고, 전략적 의사결정을 간소화합니다. 디지털 트윈에 대한 정부의 자극책, 5G의 전개, 센서 데이터를 로컬로 처리하는 엣지 컴퓨팅의 능력은 채용을 더욱 추진합니다. 한편, 개인정보보호규제의 강화나 하드웨어공급체인에 의한 압력은 성장을 억제하고 있지만, 전체적인 상승기조는 감속하고 있지 않습니다.

세계의 지리공간 분석 시장 동향과 인사이트

스마트 시티 프로그램 채용

도시의 디지털 트윈 이니셔티브는 지자체가 교통, 에너지 및 유틸리티를 실시간으로 시각화할 것을 요구하고 지리공간 분석 시장 수요를 가속화합니다. 일본 프로젝트 PLATEAU는 방재 및 토지 이용 계획을 지원하기 위해 200개 이상의 도시의 3D 모델을 제공합니다. 중국의 디지털 인프라 의무화는 표준화된 공간 프레임워크를 지방정부에 통합하여 지속적인 플랫폼 구매를 촉진하고 있습니다. 영국의 공공 부문 지리공간 협정은 지하 자산 맵핑을 위해 10억 파운드를 확보하여 공사 파업 및 유지보수 지연을 최소화합니다. 또한 유럽의 지방자치단체는 디지털 트윈을 사용하여 탄소 중립성의 진행 상황을 추적하고 지속가능성 목표와 위치 인텔리전스 간의 연관성을 강화하고 있습니다. 이러한 프로그램은 수년에 걸친 구매주기를 유지하며, 지자체 업무의 깊이에 공간 분석을 통합합니다.

5G 위치 정보 서비스 통합

5G 서브미터 단위의 위치 정확도와 밀리초 단위의 지연은 동적 교통 오케스트레이션부터 무인 항공기의 자율 라우팅에 이르기까지 실시간 지리 공간 용도를 해제합니다. 기지국에 설치된 엣지 컴퓨팅은 이미지와 센서 피드를 로컬로 처리하여 의료 및 방어에서 데이터 주권 규칙을 준수합니다. 소매업체는 쇼핑객 내비게이션에 실내 위치 추적을 채택하고 공장은 GPS 없이 자산 추적을 최적화합니다. 5G와 AI의 시너지 효과로 감지부터 결정까지의 사이클이 단축되어 상시 ON으로 컨텍스트를 의식한 공간 서비스에 대한 기대가 높아집니다.

높은 비용과 운영의 복잡성

기업이 고정밀 LiDAR에 예산을 나눌 때의 진입 장벽은 여전히 높고, 스캐너 1대당 최고 15만 달러, 연간 소프트웨어 라이선스는 5만 달러에 육박합니다. 위성, 무인 항공기, 레거시 GIS 아카이브를 통합하려면 희귀 기술이 필요합니다. 지리공간 데이터 사이언스자의 급여는 20-30% 할인입니다. 기업은 좌표계를 조정하고 포맷을 조화시키기 위해 프로젝트 시간의 대부분을 소비하고 시간 대 가치를 지연시킵니다. 구독은 자본 투자를 줄이는 반면 분석을 가동하면 운영이 급증합니다. 교육 프로그램과 인증은 매년 직원 1인당 1만-2만 5,000달러를 추가하여 중소기업 예산을 압박합니다.

부문 분석

서비스가 CAGR 12.9%를 나타낼 것으로 예측되지만, 이는 조직이 점점 복잡한 공간 솔루션을 채택하게 되어 스킬 갭이 확대되고 있음을 반영합니다. 소프트웨어는 2024년 지리공간 분석 시장 점유율 42.7%를 유지했지만, 구매자는 현재 배포를 가속화하기 위해 컨설팅 및 관리 서비스를 선호합니다. 하드웨어 매출은 센서의 가격 하락과 위성의 확대에 의해 견조하게 추이하고 있지만, 코모디티화가 진행됨에 따라 성장은 둔화하고 있습니다.

Managed Analytics의 사용이 증가하고 있다는 것은 라이선스 소유에서 성과 기반 계약으로의 전환을 나타냅니다. CARTO와 Indigo Ag의 협업은 농업 비즈니스가 데이터 융합 및 대시보드 전달을 아웃소싱함으로써 직원을 작물 과학의 혁신을 위해 해방하는 방법을 보여줍니다. 아웃소싱 모델은 또한 공간 리스크 스코어링이 필수적이지만 비중핵 업무인 보험과 부동산의 인력 부족을 완화합니다. 그 결과 서비스 부문은 지리공간 분석 시장 전체의 장기 경상 수익의 기둥이 되었습니다.

2024년 지리공간 분석 시장 규모의 35.7%는 지표면 해석으로 홍수 예측과 인프라 입지를 지원했습니다. 한편 경영진은 직관적인 비주얼을 요구하게 되어 CAGR 14.8%로 지오비주얼라이제이션을 추진하고 있습니다. 네트워크 분석도 기세를 유지하고 있으며, 유틸리티 라우팅 및 마지막 마일 배송 최적화를 지원합니다.

에코 애널리틱스 보행자 동선 대시보드는 3D 비주얼과 히트맵이 도심 상점 계획을 가속화하는 방법을 보여줍니다. 증강현실의 오버레이는 구역의 승인과 자본 사업의 자금 조달을 위해 이해 관계자의 동의를 촉구합니다. 인공지능이 테마 맵을 자동 생성하기 때문에 지오비쥬얼라이제이션은 비GIS 전문가의 진입 장벽을 낮추고 대응 가능한 지리공간 분석 시장을 확대합니다.

지리공간 분석 시장은 구성 요소별(소프트웨어, 서비스, 하드웨어), 분석 유형별(서피스 분석, 네트워크 분석 등), 배포 모델별(On-Premise, 클라우드), 최종 사용자 가상별(정부, 방위, 인텔리전스 등), 지역별로 분류됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 2024년 지리공간 분석 시장의 24.7%를 차지하며, 성숙한 위성 인프라, 광범위한 5G 전개, 지속적인 국방 지출에 지원되었습니다. 미국 국방부의 1,000기 감시 위성 계획은 신선한 이미지 스트림을 주입하고 분석 플랫폼 업그레이드에 박차를 가합니다. 캐나다의 지리공간 오픈 데이터 구상이나 멕시코의 도시 모빌리티 시험도 미국이 수익의 대부분을 차지한다고 해도 지역적인 수요를 증가시킵니다. 국가 지리 공간 정보국(National Geospatial-Intelligence Agency)의 Luno 상업 분석 계약과 같은 연방 정부 프로그램은 일관된 조달 흐름을 강화합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR) 14.5%를 나타낼 것으로 예측되며 스마트시티 보조금, 교통회랑 정비, 민간투자 증가가 그 추진력이 됩니다. 중국의 원격 감지 시장은 베이징이 하이퍼 스펙트럼과 레이더 페이로드에 자금을 제공함으로써 2033년까지 4배로 확대될 수 있습니다. 일본의 Project PLATEAU와 인도의 National Spatial Data Infrastructure는 표준화된 플랫폼에 대한 공공 부문의 의욕을 더욱 증명합니다. 인도네시아, 베트남, 필리핀의 급속한 도시화로 인해 홍수 리스크 모델링, 교통 오케스트레이션, 지형 전자화에 대한 지자체 지출이 증가하고 이 지역의 지리공간 분석 시장이 심화됩니다.

유럽에서는 오픈 데이터 정책과 녹색 전환에 대한 자금 지원을 통해 꾸준한 성장을 이루고 있습니다. 영국은 10억 파운드의 지리공간 전략을 통해 국가 자산 대장과 디지털 트윈의 전개를 지원합니다. 독일은 인더스트리 4.0 로드맵에 위치 정보 분석을 통합하고 프랑스는 우크라이나와 공동 첩보 능력으로 협력하여 방위 시장의 인계를 강조하고 있습니다. 북유럽은 탄소수지와 정밀농업에 공간 툴을 활용하여 솔루션 수출을 간소화하는 국경을 넘은 상호운용성 기준을 육성하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 스마트 시티 프로그램 도입

- 5G 대응 위치 정보 서비스의 통합

- IoT 유래의 공간 데이터의 보급

- 소형 위성 콘스텔레이션에 의한 고재방 화상 촬영

- 슈퍼 로컬 ESG 및 기후 위험 분석 수요

- 자율 운용을 위한 실시간 지오펜싱

- 시장 성장 억제요인

- 고비용과 운영의 복잡성

- 법적 및 프라이버시상의 장애물

- AI 구동형 공간 모델에서의 데이터 바이어스

- 이기종 표준 간의 상호 운용성

- 공급망 분석

- 기술 전망

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 시장의 거시 경제 요인 평가

제5장 시장 규모와 성장 예측

- 구성 요소별

- 소프트웨어

- 서비스

- 하드웨어

- 분석 유형별

- 표면 분석

- 네트워크 분석

- 지리 시각화

- 기타

- 배포 모델별

- On-Premise

- 클라우드

- 최종 사용자별

- 정부

- 국방 및 정보

- 농업

- 천연자원

- 유틸리티 및 통신

- 운송 및 물류

- 헬스케어 및 생명과학

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 동남아시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Esri Inc.

- Hexagon AB

- Trimble Inc.

- Maxar Technologies Inc.

- Bentley Systems Inc.

- Fugro NV

- L3Harris Technologies Inc.

- Airbus Defence and Space

- MDA Ltd.

- Atkins PLC(SNC-Lavalin)

- Intermap Technologies

- Oracle Corporation

- SAP SE(HANA Spatial)

- Google LLC(Google Maps Platform)

- Amazon Web Services(Location Service)

- Microsoft Corporation(Azure Maps)

- HERE Technologies

- TomTom NV

- CARTO

- Precisely(MapInfo)

제7장 시장 기회와 향후 전망

KTH 25.11.03The geospatial analytics market is valued at USD 95.84 billion in 2025 and is forecast to reach USD 174.44 billion by 2030, advancing at a 12.72% CAGR.

Rising demand for location-based insights, rapid satellite constellation launches, and smart-city investments position the discipline as an essential pillar of digital transformation. Enterprises use spatial intelligence to unlock operational efficiency, mitigate risk, and streamline strategic decisions as artificial intelligence automates feature extraction and predictive modeling. Government stimulus for digital twins, the rollout of 5G, and edge computing's ability to process sensor data locally further propel adoption. Meanwhile, heightened privacy regulation and hardware supply-chain pressures temper growth but have not slowed the overall upward trajectory.

Global Geospatial Analytics Market Trends and Insights

Adoption of Smart-City Programs

Urban digital-twin initiatives accelerate demand for the geospatial analytics market as municipalities seek real-time visibility across transportation, energy, and utilities. Japan's Project PLATEAU delivers 3D models for 200+ cities to support disaster prevention and land-use planning. China's digital infrastructure mandate embeds standardized spatial frameworks in local governments, driving continuous platform purchases. The United Kingdom's Public Sector Geospatial Agreement unlocks GBP 1 billion for underground asset mapping, minimizing construction strikes and maintenance delays. European councils also use digital twins to track carbon-neutrality progress, tightening the link between sustainability targets and location intelligence. Together, these programs sustain multi-year buying cycles and embed spatial analytics deep inside municipal operations.

Integration of 5G-Enabled Location Services

5G's sub-meter positioning accuracy and millisecond latency unlock real-time geospatial applications from dynamic traffic orchestration to autonomous drone routing. Ericsson's Istres deployment shows how dedicated network slices guarantee bandwidth for mission-critical mapping workloads.Edge computing co-located at base stations processes imagery and sensor feeds locally, ensuring compliance with data-sovereignty rules in healthcare and defense. Retailers adopt indoor positioning for shopper navigation, while factories optimize asset tracking without GPS. The synergy between 5G and AI shortens detection-to-decision cycles, raising expectations for always-on, context-aware spatial services.

High Costs and Operational Complexity

Entry barriers remain steep as enterprises budget for high-precision LiDAR-costing up to USD 150,000 per scanner-and annual software licenses approaching USD 50,000. Integrating satellite, drone, and legacy GIS archives demands rare skill sets; geospatial data scientists command 20-30% salary premiums. Firms spend most project hours cleansing coordinate systems and harmonizing formats, delaying time-to-value. Subscriptions reduce capex yet rapidly inflate opex when analytics run at full cadence. Training programs and certifications add USD 10,000-25,000 per employee each year, straining SME budgets.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of IoT-Derived Spatial Data

- Smallsat Constellations Enabling High-Revisit Imagery

- Legal and Privacy Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services are forecast to grow at a 12.9% CAGR, reflecting a widening skills gap as organizations adopt increasingly complex spatial solutions. Software maintained 42.7% geospatial analytics market share in 2024, but buyers now prioritize consulting and managed offerings to accelerate rollouts. Hardware revenue rises steadily through sensor price erosion and satellite expansion, although growth tempers as commoditization sets in.

Rising uptake of managed analytics illustrates the shift from license ownership toward outcome-based engagements. CARTO's collaboration with Indigo Ag shows how agribusinesses outsource data-fusion and dashboard delivery, freeing staff for crop-science innovation. Outsourcing models also mitigate talent shortages in insurance and real estate, where spatial risk scoring is vital yet non-core. As a result, the services segment anchors long-term recurring revenue streams across the geospatial analytics market.

Surface analysis accounted for 35.7% of the geospatial analytics market size in 2024, underpinning flood forecasting and infrastructure siting. Executive teams, however, increasingly demand intuitive visuals, propelling geovisualization at a 14.8% CAGR. Network analysis retains momentum, supporting utility routing and last-mile delivery optimization.

Echo Analytics' pedestrian-traffic dashboards illustrate how 3D visuals and heat maps accelerate city-center retail planning. Augmented-reality overlays foster stakeholder buy-in for zoning approvals and capital works funding. As artificial intelligence auto-generates thematic maps, geovisualization lowers the entry barrier for non-GIS professionals, enlarging the addressable geospatial analytics market.

Geospatial Analytics Market is Segmented by Component (Software, Services, and Hardware), Analysis Type (Surface Analysis, Network Analysis, and More), Deployment Model (On-Premises and Cloud), End-User Vertical (Government, Defense and Intelligence and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controlled 24.7% of the geospatial analytics market in 2024, supported by mature satellite infrastructure, extensive 5G rollout, and sustained defense spending. The U.S. Department of Defense's plan for 1,000 surveillance satellites will inject fresh imagery streams, spurring upgrades in analytic platforms. Canada's geospatial open-data initiatives and Mexico's urban-mobility pilots add incremental regional demand, though the United States dominates revenue. Federal programs such as the National Geospatial-Intelligence Agency's Luno commercial analytics contracts reinforce consistent procurement flows.

Asia-Pacific is forecast to register a 14.5% CAGR through 2030, propelled by smart-city grants, transport-corridor build-outs, and rising private-sector investment. China's remote-sensing market could quadruple by 2033 as Beijing funds hyperspectral and radar payloads. Japan's Project PLATEAU and India's National Spatial Data Infrastructure further validate public-sector appetite for standardized platforms. Rapid urbanization across Indonesia, Vietnam, and the Philippines drives municipal spending on flood-risk modeling, traffic orchestration, and land-tax digitization, deepening the regional geospatial analytics market.

Europe posts steady growth aided by open-data policies and green-transition funding. The United Kingdom's GBP 1 billion geospatial strategy underpins national asset registers and digital twin rollouts. Germany embeds location analytics in Industry 4.0 roadmaps, while France cooperates with Ukraine on joint intelligence capabilities, highlighting defense-market pull. Northern Europe leverages spatial tools for carbon budgeting and precision farming, fostering cross-border interoperability standards that simplify solution exports.

- Esri Inc.

- Hexagon AB

- Trimble Inc.

- Maxar Technologies Inc.

- Bentley Systems Inc.

- Fugro NV

- L3Harris Technologies Inc.

- Airbus Defence and Space

- MDA Ltd.

- Atkins PLC (SNC-Lavalin)

- Intermap Technologies

- Oracle Corporation

- SAP SE (HANA Spatial)

- Google LLC (Google Maps Platform)

- Amazon Web Services (Location Service)

- Microsoft Corporation (Azure Maps)

- HERE Technologies

- TomTom NV

- CARTO

- Precisely (MapInfo)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of Smart-City Programs

- 4.2.2 Integration of 5G-enabled Location Services

- 4.2.3 Proliferation of IoT-derived Spatial Data

- 4.2.4 Smallsat Constellations Enabling High-Revisit Imagery

- 4.2.5 Hyper-local ESG and Climate-Risk Analytics Demand

- 4.2.6 Real-time Geofencing for Autonomous Operations

- 4.3 Market Restraints

- 4.3.1 High Costs and Operational Complexity

- 4.3.2 Legal and Privacy Hurdles

- 4.3.3 Data-bias in AI-driven Spatial Models

- 4.3.4 Interoperability Across Heterogeneous Standards

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.3 Hardware

- 5.2 By Analysis Type

- 5.2.1 Surface Analysis

- 5.2.2 Network Analysis

- 5.2.3 Geovisualization

- 5.2.4 Others

- 5.3 By Deployment Model

- 5.3.1 On-Premises

- 5.3.2 Cloud

- 5.4 By End-user Vertical

- 5.4.1 Government

- 5.4.2 Defense and Intelligence

- 5.4.3 Agriculture

- 5.4.4 Natural Resources

- 5.4.5 Utility and Communication

- 5.4.6 Transportation and Logistics

- 5.4.7 Healthcare and Life Sciences

- 5.4.8 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Middle-East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 Esri Inc.

- 6.4.2 Hexagon AB

- 6.4.3 Trimble Inc.

- 6.4.4 Maxar Technologies Inc.

- 6.4.5 Bentley Systems Inc.

- 6.4.6 Fugro NV

- 6.4.7 L3Harris Technologies Inc.

- 6.4.8 Airbus Defence and Space

- 6.4.9 MDA Ltd.

- 6.4.10 Atkins PLC (SNC-Lavalin)

- 6.4.11 Intermap Technologies

- 6.4.12 Oracle Corporation

- 6.4.13 SAP SE (HANA Spatial)

- 6.4.14 Google LLC (Google Maps Platform)

- 6.4.15 Amazon Web Services (Location Service)

- 6.4.16 Microsoft Corporation (Azure Maps)

- 6.4.17 HERE Technologies

- 6.4.18 TomTom NV

- 6.4.19 CARTO

- 6.4.20 Precisely (MapInfo)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment