|

시장보고서

상품코드

1849902

엔터프라이즈 방화벽 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Enterprise Firewall - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

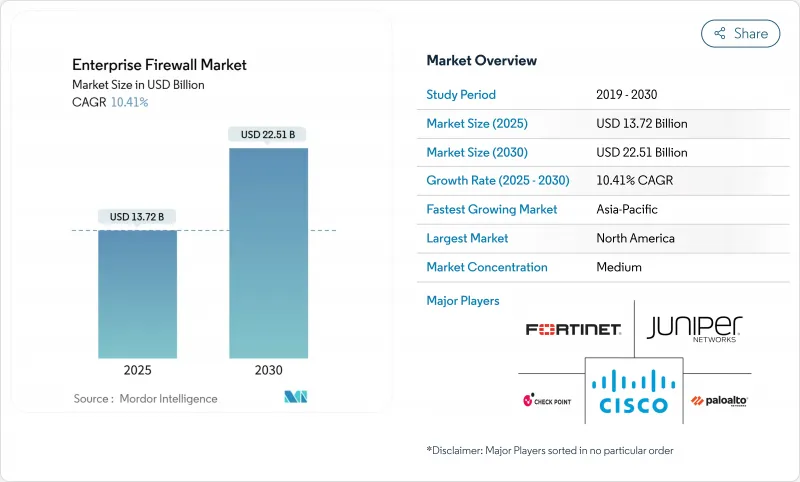

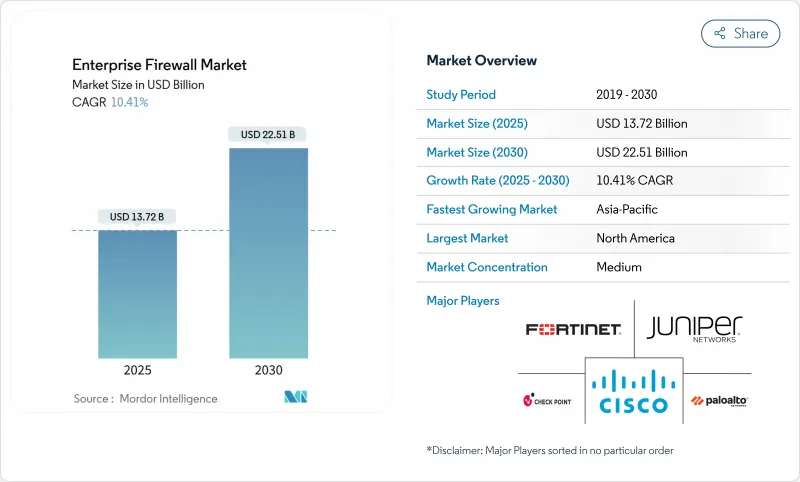

엔터프라이즈 방화벽 시장 규모는 2025년에 137억 2,000만 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR은 10.41%를 나타낼 것으로 예측되며, 2030년에는 225억 1,000만 달러로 성장할 전망입니다.

인공지능 기반의 다중 벡터 공격 증가, 클라우드 워크로드의 급속한 확장, 제로 트러스트 의무화는 실시간으로 남북 및 동서 트래픽을 검사하는 적응형 위협 인텔리전스 방화벽으로 조달 우선순위를 재편하고 있습니다. 하이브리드 근무 모델은 긴급성을 더하며, 구매자들이 하드웨어 오버헤드를 줄이면서 원격 사용자를 보호하기 위해 서비스형 방화벽(Firewall-as-a-Service)으로 이동하도록 촉진합니다. 공급업체들은 네트워크 및 보안 기능을 통합한 통합 플랫폼으로 대응하는 한편, PCI DSS 및 DORA와 같은 규정 준수 프레임워크는 지속적인 정책 시행 및 감사 보고에 대한 수요를 증가시킵니다. 반도체 비용 상승과 기술 인력 부족은 단기적인 하드웨어 출시를 제약하지만, 플랫폼화가 가속화되면서 구독 수익은 마진을 탄력적으로 유지합니다.

세계의 엔터프라이즈 방화벽 시장 동향 및 인사이트

향상된 다중 벡터 공격

공격자들은 이제 합법적 소프트웨어와 AI를 무기화하여 단일 캠페인으로 엔드포인트, 클라우드 워크로드, 측면 경로를 침투하며 정적 규칙 세트의 무력화를 초래합니다. 팔로알토 네트웍스는 2024년 발생한 사고의 86%가 직접적인 비즈니스 중단을 초래했다고 관찰하며, 기업들이 분산된 센서 전반에 걸쳐 실시간 인텔리전스를 상호 연관시키는 차세대 방화벽을 도입하도록 촉구하고 있습니다. 한 글로벌 통신사는 도메인 컨트롤러 외부에서 200개 이상의 특권 세션을 발견하여 동서 방향(east-west) 사각지대를 부각시켰습니다. 벤더들은 머신러닝 기반 검사 기능을 내장해 행동 이상을 탐지함으로써 기업이 수 밀리초 내에 의심스러운 트래픽을 격리하고 체류 시간을 단축할 수 있도록 지원합니다.

하이브리드 및 원격 근무 아키텍처의 빠른 채택

분산된 인력은 가정 네트워크와 관리되지 않는 기기에 의존하여 위협 표면을 데이터센터 경계를 훨씬 넘어 확장시킵니다. 조직들은 단일 클라우드 적용 지점에서 신원, 기기 상태, 방화벽 제어를 통합하는 보안 액세스 서비스 엣지(SASE) 모델로 전환하고 있습니다. 마이크로소프트는 암호화된 VPN 터널이 기존 검사를 회피하는 경우가 많다고 지적하며, 많은 기업이 사용자가 어디에서 연결하든 일관된 정책을 적용하기 위해 서비스형 방화벽(Firewall-as-a-Service)으로 이전하고 있습니다. 벨 캐나다와 팔로알토 네트웍스의 협력 사례는 통신사들이 원격 팀을 위한 관리형 연결에 AI 기반 방화벽을 적용하는 방식을 보여줍니다.

중소기업의 예산 제약

많은 소규모 기업은 전담 보안 인력이 부족하고 제한된 자본을 핵심 운영에 할당해야 하는 압박을 받아 고급 방화벽 도입이 지연됩니다. 사이버 보험사들은 관리형 보안 서비스를 도입한 계약자에게 보험료 할인을 제공하지만, 선불 구독 비용은 여전히 가격에 민감한 지역의 구매자를 주저하게 만듭니다. 공급업체들은 자동화된 정책 템플릿과 사용량 기반 과금을 포함한 입문용 클라우드 방화벽으로 대응하여 구매 장벽을 낮추고 있습니다.

부문 분석

온프레미스 어플라이언스는 예측 가능한 처리량과 에어갭 설계에 대한 규제적 안정성을 바탕으로 2024년 기업용 방화벽 시장 점유율의 47.22%를 유지했습니다. 프로토콜 마이그레이션 불확실성으로 인해 교체 주기가 연장되고 있음에도 불구하고, 매출 기준으로는 이 부문이 기업용 방화벽 시장 규모에서 가장 큰 비중을 차지했습니다. 데이터센터에서 지연 시간에 민감한 워크로드를 운영하는 기업들은 고속 TLS 검사를 위한 가속기를 내장한 전용 하드웨어를 계속 선호합니다.

클라우드 네이티브 방화벽 서비스(Firewall-as-a-Service)는 2030년까지 연평균 14.04% 성장률을 보이며, 중앙 집중식 정책, 탄력적 확장성, 사용량 기반 비용 구조를 제공하여 멀티클라우드 및 원격 근무 전략을 채택하는 기업들의 공감을 얻고 있습니다. 이 모델은 공급업체가 포털을 통해 지속적인 감사 로그를 제공함으로써 규정 준수 증거를 단순화합니다. 가상 어플라이언스는 양쪽 영역 사이에 위치하여 기업이 하드웨어를 배송하지 않고도 프라이빗 클라우드와 엣지 위치 전반에 규칙 세트를 복제할 수 있게 하여 제로 트러스트 전환 중 지사 전개를 용이하게 합니다. 이러한 혼합 접근 방식은 구매자들이 이제 단일 아키텍처에 의존하기보다 방화벽 폼 팩터를 워크로드 위치에 맞춰 선택한다는 점을 강조합니다.

하드웨어 어플라이언스는 2024년 매출의 48.31%를 차지하며, 결정론적 성능, 하드웨어 암호화 오프로드, 감사 팀을 만족시키는 변조 방지 설계에 대한 지속적인 수요를 반영했습니다. 기업용 방화벽 시장 규모에서 이 비중은 꾸준히 성장할 것으로 예상되나, 구매자들이 어플라이언스의 잠재력을 극대화하는 라이프사이클 서비스로 예산을 전환함에 따라 점유율은 감소할 전망입니다.

관리형 및 전문 서비스는 13.9%의 연평균 성장률(CAGR)로 확대될 것으로 전망됩니다. 지속적인 튜닝, 위협 정보 통합, 규정 준수 보고가 많은 내부 팀의 역량을 초과하기 때문입니다. 서비스 제산업체들은 DORA, HIPAA 및 산업별 표준을 위한 플레이북을 패키지화하여 고객의 평균 대응 시간 단축과 규제 기관 요구 충족을 지원합니다. 벤더들은 관리 콘솔에 AI 기반 코파일럿을 점점 더 많이 내장하고 있지만, 이상 현상을 맥락화하고 정책을 진화하는 비즈니스 목표에 맞추기 위해서는 여전히 인간 전문가의 역할이 필수적입니다.

엔터프라이즈 방화벽 시장은 전개 유형(온프레미스 어플라이언스, 클라우드 네이티브 방화벽 서비스(Firewall-as-a-Service), 하이브리드/가상 어플라이언스), 구성 요소(하드웨어 어플라이언스, 가상 어플라이언스/소프트웨어, 관리형/전문 서비스), 엔터프라이즈 규모(중소 및 영업, 중견 기업, 대기업), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), 헬스케어/생명 과학, 기타), 지역

지역 분석

북미는 2024년 매출의 35.4%를 차지하며 선두를 달렸는데, 이는 엄격한 연방 규정과 높은 침해 복구 비용이 선제적 구매를 촉진했기 때문입니다. 해당 지역 기업들은 제로 트러스트 아키텍처를 표준화하고 운영 단편화를 줄이기 위해 통합 플랫폼을 점점 더 선택하고 있습니다. 벨 캐나다가 팔로알토 네트웍스와 제휴한 사례는 통신사들이 AI 기반 방화벽과 연결성을 번들로 제공하여 분산된 인력을 지원하는 방식을 보여줍니다.

아시아태평양 지역은 2030년까지 연평균 12.7%의 성장률(CAGR)을 기록할 전망으로, 지역 중 가장 빠른 성장세를 보일 것입니다. 인도, 인도네시아, 일본 정부는 시민 데이터의 현지 검사를 촉구하며 국가별 클라우드에 배포 가능한 방화벽 구매를 장려하고 있습니다. 중국 내국 기업들은 암호화 규정 준수 및 중국어 위협 정보를 처리하는 인라인 머신러닝 모듈 공급으로 시장 점유율을 확대 중입니다. 다국적 클라우드 제산업체들은 글로벌 원격 측정 범위를 유지하면서 주권 조항을 충족하기 위해 지역 SOC 운영사와 협력하고 있습니다.

유럽은 GDPR과 향후 시행될 DORA 프레임워크에 대한 꾸준한 추진력을 유지하고 있으며, 이는 입증 가능한 세분화와 사고 보고를 요구합니다. 소닉월의 신규 유럽 SOC는 거주지 법률에 부합하는 현지 데이터 처리 및 신속 대응을 제공하기 위한 벤더 투자의 모범 사례입니다. 독일과 영국은 산업 스파이 방위에 집중하는 반면, 프랑스와 스페인은 멀티클라우드 확장을 위한 테넌트별 정책 격리가 가능한 클라우드 방화벽에 투자하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 다중 벡터 사이버 공격의 고도화

- 하이브리드/원격 근무 아키텍처의 급속한 도입

- 제로 트러스트와 세분화에 관한 규제 의무

- 동서 방향 보안이 필요한 클라우드 워크로드 확산

- 적응형 방화벽을 요구하는 AI 기반 다형성 악성코드

- 신흥 경제국에서의 주권적 트래픽 검사 조항

- 시장 성장 억제요인

- 중소기업의 예산 제약

- 복잡한 정책 관리를 위한 기술 부족

- IPv6 전환으로 인한 하드웨어 교체 주기 지연

- 데이터 거주지 요구사항에 따른 지역별 클라우드 SOC로의 전환

- 업계 밸류체인 분석

- 규제 상황

- 기술의 전망

- 업계의 매력 - Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 거시 경제 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측

- 전개 유형별

- 온프레미스 어플라이언스

- 클라우드 네이티브 서비스형 방화벽(Firewall-as-a-Service)

- 하이브리드/가상 어플라이언스

- 컴포넌트별

- 하드웨어 어플라이언스

- 가상 어플라이언스/소프트웨어

- 관리형 서비스와 전문 서비스

- 기업 규모별

- 중소기업(종업원 100명 미만)

- 중규모 기업(100-999명)

- 대기업(1,000명 이상)

- 최종 사용자 업계별

- BFSI

- 헬스케어 및 생명과학

- 제조업과 산업

- 정부 및 방위

- 소매업 및 전자상거래

- 통신 및 미디어

- 교육 및 조사

- 에너지 및 유틸리티

- 기타 최종 사용자 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 싱가포르

- 말레이시아

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Fortinet, Inc.

- Palo Alto Networks, Inc.

- Check Point Software Technologies Ltd.

- Cisco Systems, Inc.

- Juniper Networks, Inc.

- Sophos Ltd.

- WatchGuard Technologies, Inc.

- SonicWALL LLC

- Forcepoint LLC

- Barracuda Networks, Inc.

- Hillstone Networks Co., Ltd.

- Stormshield SAS

- AhnLab, Inc.

- Clavister AB

- Untangle, Inc.

- GajShield Infotech(India) Pvt. Ltd.

- F-Secure Corp.

- OPNsense(Deciso BV)

- Gateworks Corp.

- Sangfor Technologies Inc.

- Huawei Technologies Co., Ltd.

- Hillstone Networks

- Array Networks, Inc.

- Stonesoft Oy(a McAfee company)

- Netgate(ESF)

제7장 시장 기회와 미래 동향

- 화이트 스페이스와 미충족 요구 평가

The Enterprise Firewall Market size is estimated at USD 13.72 billion in 2025, and is expected to reach USD 22.51 billion by 2030, at a CAGR of 10.41% during the forecast period (2025-2030).

Rising AI-driven, multi-vector attacks, rapid cloud workload expansion, and zero-trust mandates are reshaping procurement priorities toward adaptive threat-intelligence firewalls that inspect north-south and east-west traffic in real time. Hybrid work models add urgency, pushing buyers toward Firewall-as-a-Service to protect remote users while reducing hardware overhead. Vendors respond with unified platforms that blend network and security functions, while compliance frameworks such as PCI DSS and DORA increase demand for continuous policy enforcement and audit reporting. Semiconductor cost inflation and skills shortages constrain short-term hardware rollouts, yet subscription revenues keep margins resilient as platformization gains pace.

Global Enterprise Firewall Market Trends and Insights

Escalating Sophistication of Multi-Vector Attacks

Attackers now weaponize legitimate software and AI to breach endpoints, cloud workloads, and lateral pathways in one campaign, leaving static rule sets ineffective. Palo Alto Networks observed that 86% of incidents in 2024 caused direct business disruption, prompting enterprises to deploy next-generation firewalls that correlate real-time intelligence across distributed sensors. A global telecom uncovered more than 200 privileged sessions sitting outside domain controllers, underscoring east-west blind spots. Vendors embed machine-learning inspection to flag behavioral anomalies, enabling enterprises to quarantine suspicious traffic within milliseconds and cut dwell time.

Rapid Adoption of Hybrid and Remote Work Architectures

Decentralized workforces rely on home networks and unmanaged devices, expanding the threat surface far beyond data-center perimeters. Organizations shift toward secure access service edge models that fuse identity, device health, and firewall controls inside a single cloud point of enforcement. Microsoft notes that encrypted VPN tunnels often evade traditional inspection, so many firms migrate to Firewall-as-a-Service for uniform policy wherever users connect. Partnerships such as Bell Canada with Palo Alto Networks highlight how carriers wrap AI-powered firewalls around managed connectivity for remote teams.

Budget Constraints Among SMBs

Many small firms lack full-time security personnel and face pressure to allocate limited capital to core operations, slowing the adoption of advanced firewalls. Cyber-insurance carriers now offer premium reductions to policyholders that deploy managed security services, but up-front subscription costs still deter buyers in price-sensitive regions. Vendors respond with entry-level cloud firewalls that include automated policy templates and usage-based billing, lowering procurement hurdles.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Mandates for Zero-Trust and Segmentation

- Cloud Workload Proliferation Requiring East-West Security

- Skills Shortage to Manage Complex Policies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premise appliances retained 47.22% of the 2024 enterprise firewall market share on the back of predictable throughput and regulatory comfort with air-gapped designs. In revenue terms, the segment accounted for the largest slice of the enterprise firewall market size, even as refresh cycles extend because of protocol migration uncertainty. Enterprises running latency-sensitive workloads in data centers continue to favor purpose-built hardware that embeds accelerators for high-speed TLS inspection.

Cloud-native Firewall-as-a-Service, advancing at a 14.04% CAGR through 2030, brings centralized policy, elastic scale, and pay-as-you-grow economics that resonate with firms embracing multicloud and remote work strategies. The model also simplifies compliance evidence because providers surface continuous audit logs via portals. Virtual appliances sit between both worlds, letting enterprises replicate rule sets across private clouds and edge locations without shipping hardware, which eases branch rollouts during zero-trust transitions. The blended approach underlines how buyers now map firewall form factor to workload locality rather than defaulting to a single architecture.

Hardware appliances captured 48.31% of 2024 revenues, reflecting persistent demand for deterministic performance, hardware encryption offload, and tamper-resistant designs that satisfy audit teams. This slice of the enterprise firewall market size is expected to grow steadily, yet its proportion declines as buyers shift budget toward lifecycle services that unlock the appliance's full potential.

Managed and professional services are forecast to expand at 13.9% CAGR because continuous tuning, threat-feed integration, and compliance reporting outstrip many in-house teams' bandwidth. Service providers bundle playbooks for DORA, HIPAA, and sector-specific standards, helping clients cut mean-time-to-respond and satisfy regulators. Vendors increasingly embed AI-driven copilots into management consoles, yet human specialists remain essential for contextualising anomalies and aligning policies with evolving business objectives.

Enterprise Firewall Market is Segmented by Deployment Type (On-Premise Appliance, Cloud-Native Firewall-As-A-Service, and Hybrid/Virtual Appliance), Component (Hardware Appliance, Virtual Appliance/Software, and Managed and Professional Services), Enterprise Size (Small and Micro Enterprises, Mid-Sized Enterprises, and Large Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, and More), and Geography.

Geography Analysis

North America led with 35.4% of 2024 revenues, anchored by strict federal rules and high breach remediation costs that spur proactive purchasing. Enterprises there standardize on zero-trust architectures and increasingly choose consolidated platforms to cut operational fragments. Bell Canada's alliance with Palo Alto Networks shows how telcos bundle AI-driven firewalls with connectivity to serve a dispersed workforce.

Asia-Pacific is set for a 12.7% CAGR through 2030, the fastest across regions. Governments in India, Indonesia, and Japan press for local inspection of citizen data, encouraging procurement of firewalls deployable in country-specific clouds. Domestic vendors in China gain share by aligning with encryption rules and supplying inline machine-learning modules that process Mandarin threat intel. Multinational cloud providers partner with regional SOC operators to satisfy sovereignty clauses while maintaining global telemetry reach.

Europe maintains steady momentum on GDPR and the upcoming DORA framework, which requires demonstrable segmentation and incident reporting. SonicWall's new European SOC exemplifies vendor investment to provide local data handling and rapid response aligned with residency laws. Germany and the United Kingdom focus on industrial espionage defenses, whereas France and Spain invest in cloud firewalls capable of per-tenant policy isolation for multicloud expansion.

- Fortinet, Inc.

- Palo Alto Networks, Inc.

- Check Point Software Technologies Ltd.

- Cisco Systems, Inc.

- Juniper Networks, Inc.

- Sophos Ltd.

- WatchGuard Technologies, Inc.

- SonicWall LLC

- Forcepoint LLC

- Barracuda Networks, Inc.

- Hillstone Networks Co., Ltd.

- Stormshield SAS

- AhnLab, Inc.

- Clavister AB

- Untangle, Inc.

- GajShield Infotech (India) Pvt. Ltd.

- F-Secure Corp.

- OPNsense (Deciso B.V.)

- Gateworks Corp.

- Sangfor Technologies Inc.

- Huawei Technologies Co., Ltd.

- Hillstone Networks

- Array Networks, Inc.

- Stonesoft Oy (a McAfee company)

- Netgate (ESF)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating sophistication of multi-vector cyber-attacks

- 4.2.2 Rapid adoption of hybrid/remote work architectures

- 4.2.3 Regulatory mandates for zero-trust and segmentation

- 4.2.4 Cloud workload proliferation requiring east-west security

- 4.2.5 AI-driven polymorphic malware forcing adaptive firewalls

- 4.2.6 Sovereign traffic-inspection clauses in emerging economies

- 4.3 Market Restraints

- 4.3.1 Budget constraints among SMBs

- 4.3.2 Skills shortage to manage complex policies

- 4.3.3 IPv6 transition delaying hardware refresh cycles

- 4.3.4 Data-residency-driven shift to regional cloud SOCs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Deployment Type

- 5.1.1 On-Premise Appliance

- 5.1.2 Cloud-Native Firewall-as-a-Service (FWaaS)

- 5.1.3 Hybrid/Virtual Appliance

- 5.2 By Component

- 5.2.1 Hardware Appliance

- 5.2.2 Virtual Appliance/Software

- 5.2.3 Managed and Professional Services

- 5.3 By Enterprise Size

- 5.3.1 Small and Micro Enterprises ( <100 employees )

- 5.3.2 Mid-sized Enterprises (100-999)

- 5.3.3 Large Enterprises (>=1,000)

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Manufacturing and Industrial

- 5.4.4 Government and Defense

- 5.4.5 Retail and E-commerce

- 5.4.6 Telecom and Media

- 5.4.7 Education and Research

- 5.4.8 Energy and Utilities

- 5.4.9 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Singapore

- 5.5.4.6 Malaysia

- 5.5.4.7 Australia

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Fortinet, Inc.

- 6.4.2 Palo Alto Networks, Inc.

- 6.4.3 Check Point Software Technologies Ltd.

- 6.4.4 Cisco Systems, Inc.

- 6.4.5 Juniper Networks, Inc.

- 6.4.6 Sophos Ltd.

- 6.4.7 WatchGuard Technologies, Inc.

- 6.4.8 SonicWall LLC

- 6.4.9 Forcepoint LLC

- 6.4.10 Barracuda Networks, Inc.

- 6.4.11 Hillstone Networks Co., Ltd.

- 6.4.12 Stormshield SAS

- 6.4.13 AhnLab, Inc.

- 6.4.14 Clavister AB

- 6.4.15 Untangle, Inc.

- 6.4.16 GajShield Infotech (India) Pvt. Ltd.

- 6.4.17 F-Secure Corp.

- 6.4.18 OPNsense (Deciso B.V.)

- 6.4.19 Gateworks Corp.

- 6.4.20 Sangfor Technologies Inc.

- 6.4.21 Huawei Technologies Co., Ltd.

- 6.4.22 Hillstone Networks

- 6.4.23 Array Networks, Inc.

- 6.4.24 Stonesoft Oy (a McAfee company)

- 6.4.25 Netgate (ESF)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment