|

시장보고서

상품코드

1849904

기업 컨텐츠 관리 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Enterprise Content Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

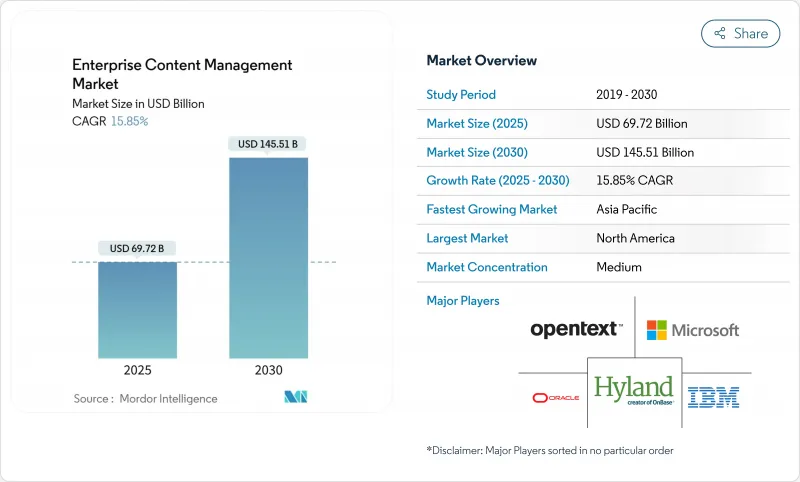

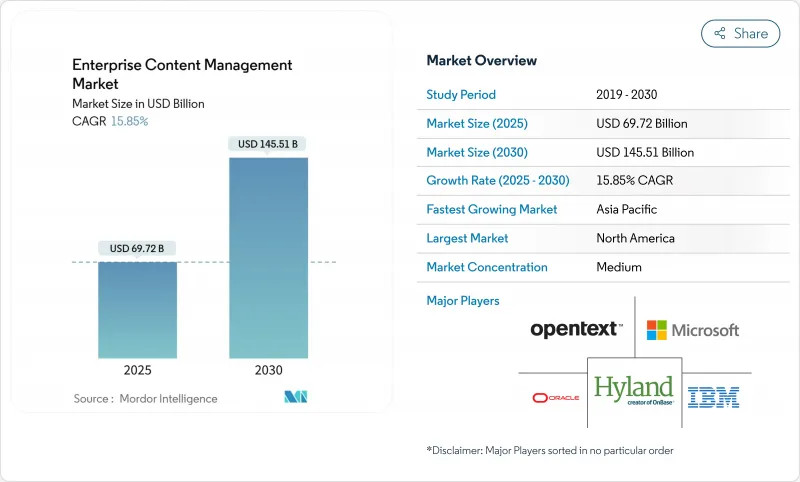

현재 시장 추정 및 예측은 기업 컨텐츠 관리 시장 규모가 2025년 697억 2,000만 달러, 2030년 1,455억 1,000만 달러에 이르며 CAGR 15.85%를 나타낼 것으로 예측됩니다.

급속한 성장은 기존의 파일 저장소에서 비정형 데이터를 사용 가능한 인텔리전스로 변환하는 AI 지원 플랫폼으로의 결정적인 전환을 반영합니다. 규제의 의무화, 원격 워크의 급증, 클라우드 네이티브 아키텍처에 대한 축족이 합쳐져 탄력적인 수요 곡선이 형성되고 있습니다. 컴플라이언스 기능과 확장 가능한 클라우드 서비스를 융합하는 공급업체는 큰 비즈니스 기회를 얻을 수 있는 반면, 조기에 현대화를 진행하는 조직은 생산성을 높이고 비용을 절감할 수 있습니다. 경쟁이 치열해지고 있는 것은 내장 애널리틱스와 일상적인 워크플로우에 컨텐츠 관리를 통합하는 협업 제품군과의 통합입니다.

세계의 기업 컨텐츠 관리 시장 동향 및 인사이트

컨텐츠 라이프 사이클 거버넌스에 대한 규제 준수 의무화

증가하는 데이터 보호법에 따라 컨텐츠 거버넌스는 이사회 수준의 의무로 전환되고 있습니다. 유럽에서의 GDPR(EU 개인정보보호규정)의 시행은 컴플라이언스 위반의 금전적·풍평적 비용을 실증해, 기업이 유지, 삭제, 감사 로깅을 자동화하는 플랫폼을 채용하는 동기부여가 되었습니다. 현재 논의되고 있는 새로운 인공지능법은 투명한 데이터의 취급이 요구되고 있으며, 업그레이드 사이클에 긴급성이 증가하고 있습니다. 금융기관은 바젤 III를 충족시키기 위해 불변의 감사 추적을 취득해야 하며, 의료 제공업체는 HIPAA 하에서 원격 의료 기록을 보호해야 합니다. 벌칙이 강화됨에 따라 기업은 단편 리포지토리보다 통합 솔루션을 선호하고 일관된 정책 실행을 보장하며 법적 위험을 줄일 수 있습니다.

기업의 비정형 데이터 양의 폭발적 증가

페타바이트급 멀티미디어 파일, 센서 로그, 소셜 상호작용이 기존의 파일 공유를 압도하고 있습니다. 은행은 수백만 명의 고객과 채팅 및 화상 통화를 보관하고, 제조업에서는 CAD 설계 및 검사 이미지를 관리하며, 세계 설계 팀은 실시간 피드백 루프를 생성합니다. 원격 근무에서는 개인 장치나 다른 클라우드 애플리케이션에 컨텐츠가 분산되어 검색 지연과 중복 작업이 발생합니다. 머신러닝을 적용하여 컨텐츠를 분류하고 표면화하는 최신 플랫폼을 통해 기업은 흩어져 있는 데이터를 액세스 가능한 지식으로 변환하여 협업 향상과 의사결정 주기를 가속화할 수 있습니다.

클라우드/모바일 ECM의 보안 및 개인정보 보호 우려

위험을 피하는 부문은 규제 대상 컨텐츠를 사내 구축 환경으로 옮기는 것을 망설입니다. 암호화 키 관리, 관할권 관리, 공급업체 잠금은 여전히 CISO의 가장 큰 문제입니다. 모바일 액세스는 기업의 하드닝이 부족한 엔드포인트를 도입하여 공격 대상 영역을 확장합니다. 클라우드 제공업체는 지속적인 침입 테스트와 기밀 컴퓨팅에 투자하고 있지만, 인식이 현실에서 늦어지기 때문에 승인주기가 불필요하고 특히 데이터 잔여 조항이 심한 유럽에서는 롤아웃이 지연됩니다.

부문 분석

2024년 기업 컨텐츠 관리 시장에서는 문서 관리가 32.3%의 최고 점유율을 유지하여 규제 대상 기록과 일상적인 파일의 백본 역할을 명확히 했습니다. 체크인/아웃, 버전 관리, 감사 기능이 필요한 금융, 헬스케어, 공공기관 수요는 계속 안정되고 있습니다. 디지털 자산 관리와 관련된 기업 컨텐츠 관리 시장 규모는 마케팅 담당자가 옴니채널 캠페인에서 리치 미디어를 구성함에 따라 2030년까지 연평균 복합 성장률(CAGR)이 16.2%로 가속화되고 있습니다.

하이브리드 플랫폼은 공급업체가 DAM, 워크플로우 오케스트레이션 및 레코드 관리를 단일 인터페이스에 통합하여 기존 경계를 모호하게 만듭니다. 이 수렴은 통합된 라이선싱과 낮은 통합 오버헤드에 대한 구매자의 선호도를 반영합니다. 사례 관리 도구는 소송 팀, 보험 회사 및 공공 혜택 프로그램에 유용하며 워크플로우 관리는 보다 광범위한 프로세스 자동화 제품군과 함께 작동합니다. 기록 관리는 보관 기간이 수십 년에 걸쳐 분실했을 경우의 벌칙이 엄격한 에너지, 제약, 항공우주 분야에서 장기적인 아카이브를 확보하고 있습니다.

2024년 기업 컨텐츠 관리 시장 규모는 On-Premise 유형이 57.1%를 차지했는데, 이는 정착된 인프라와 엄격한 컴플라이언스 제약의 증거입니다. 그럼에도 불구하고 클라우드 계약은 15.3%의 연평균 복합 성장률(CAGR)을 나타내며 다른 모든 형태를 초과할 것으로 예상됩니다. 일본 정부가 2025년까지 기간 시스템의 전환을 의무화하고 있는 것은 도입의 배경에 있는 정책적인 뒷받침의 일례이며, 각 기관은 엄격한 스케줄 하에서 노후화된 스택의 근대화를 강요하고 있습니다.

조직은 현재 운영 탄력성과 실시간 협업을 과거의 설비 투자 금액보다 강조하고 있습니다. 공급업체가 고객 관리 키와 지역 데이터센터를 제공하게 되어 보안에 대한 이론이 감소하고 있습니다. SaaS를 협업을 위해 활용하면서 기밀성이 높은 아카이브를 사내 데이터센터에 보관하는 하이브리드형도 뿌리 깊습니다. 이러한 단계적 접근은 기술 격차와 예산 계획을 완화하고 최종 풀 클라우드에 대한 헌신에 대한 교량 역할을 하는 경우가 많습니다.

기업 컨텐츠 관리 시장은 구성 요소별(컨텐츠 관리, 문서 관리 등), 솔루션 유형별(On-Premise, 클라우드 등), 도입 형태별(On-Premise, 클라우드 등), 기업 규모별(중소기업, 대기업 등), 최종 사용자 산업별(통신 및 IT, BFSI 등), 지역별로 분류되어 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 2024년 매출의 31.6%를 차지하며 가장 성숙한 지역이었습니다. 이는 깊은 파트너 생태계와 프로젝트 승인 위험을 줄이는 명확한 규제 환경에 의해 지원됩니다. 미국 은행은 레거시 이미징 시스템을 현대화하고 의료 서비스 제공업체는 상호 운용성 규칙을 충족하기 위해 환자 기록을 디지털화합니다. 캐나다의 연방 및 주 정부 기관은 투명성을 높이기 위해 종이 아카이브를 클라우드로 마이그레이션. 멕시코 제조업이 국경을 넘은 공급망 문서 작성에 ECM을 채용하여 USMCA 회랑 전체에 파급 효과를 나타냅니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 17.4%를 나타낼 전망입니다. 일본의 퍼블릭·클라우드·프로그램이 부처나 도도부현에서의 채용을 가속. 인도의 Digital India 이니셔티브는 국가 서비스 및 공립 대학에 ECM을 도입하고 한국과 호주는 기존 배포에서 AI 강화를 추진하고 있습니다. 이러한 요인들과 함께 기업 컨텐츠 관리 시장은 아시아태평양에서 가장 역동적으로 확대되고 있습니다.

유럽에서는 비즈니스 기회와 컴플라이언스의 복잡성이 균형을 이룹니다. GDPR(EU 개인정보보호규정)은 데이터 주권을 보장하는 솔루션에 대한 지출을 지속적으로 유도하고 AI 규정안은 문서 관리를 강화합니다. 독일 산업 기반은 ECM을 Industry 4.0 워크플로우에 통합하고 영국 금융 부문은 모기지 인수를 종이 없이 추구하고 프랑스는 병원과 대학 리포지토리를 업그레이드하고 있습니다. 북유럽과 같은 소규모 경제권은 에너지 및 생명 과학을 위한 수직 솔루션에 투자하고 고도로 전문화된 수출에 적합한 탄력성과 추적 가능한 워크플로우를 추구합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 컨텐츠 라이프사이클 거버넌스의 규제 준수 의무

- 기업의 비구조화 데이터량의 폭발적 증가

- 클라우드 네이티브 ECM 도입으로의 이행을 가속

- AI 구동형 컨텐츠 인텔리전스와 하이퍼 오토메이션

- ECM과 협업 허브(Teams, Slack)의 통합

- EU의 디지털 주권 호스팅 요건

- 시장 성장 억제요인

- 클라우드/모바일 ECM의 보안 및 개인정보 보호 우려

- MandA 후의 레거시 리포지토리의 통합의 복잡성

- 국경을 넘은 데이터 전송 제한(GDPR(EU 개인정보보호규정), DPDPA 등)

- 정보 거버넌스 전문가의 인력 부족

- 공급망 분석

- 규제 상황

- 기술 전망

- 거시 경제 요인이 시장에 미치는 영향

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 솔루션 유형별

- 콘텐츠 관리

- 문서 관리

- 사례 관리

- 워크플로우 관리

- 기록 관리

- 디지털 자산 관리

- 기타

- 배포 모드별

- On-Premise

- 클라우드

- 기업 규모별

- 중소기업

- 대기업

- 최종 사용자 업계별

- 통신 및 IT

- BFSI

- 소매 및 전자상거래

- 교육

- 제조

- 미디어 및 엔터테인먼트

- 정부 및 공공 부문

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 기타 중동

- 아프리카

- 남아프리카

- 케냐

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Microsoft Corporation

- OpenText Corporation

- IBM Corporation

- Hyland Software Inc.

- Oracle Corporation

- Box Inc.

- Adobe Inc.

- Xerox Corporation

- M-Files Corp.

- Alfresco Software Inc.(Hyland)

- DocuWare GmbH

- Datamatics Global Services Ltd.

- Hewlett Packard Enterprise Co.

- Capgemini SE

- Newgen Software Technologies Ltd.

- Laserfiche Inc.

- SER Group

- Fabasoft AG

- Everteam Global Services

- KnowledgeLake Inc.

- iManage LLC

- Egnyte Inc.

제7장 시장 기회와 향후 전망

KTH 25.11.03Current estimates place the enterprise content management market size at USD 69.72 billion in 2025 and forecast it to reach USD 145.51 billion by 2030, expanding at a 15.85% CAGR.

Rapid gains reflect a decisive move from traditional file repositories toward AI-enabled platforms that transform unstructured data into usable intelligence. Regulatory mandates, the surge in remote work, and a pivot to cloud-native architectures combine to create a resilient demand curve. Vendors that marry compliance capabilities with scalable cloud offerings stand to capture outsized opportunities, while organizations that modernize early benefit from productivity lifts and cost avoidance. Intensifying competition centers on embedded analytics and integration with collaboration suites that embed content management inside daily workflows.

Global Enterprise Content Management Market Trends and Insights

Regulatory compliance mandates for content lifecycle governance

Growing data-protection laws turn content governance into a board-level obligation. GDPR enforcement in Europe demonstrated the financial and reputational costs of non-compliance, motivating enterprises to adopt platforms that automate retention, deletion, and audit logging. New AI legislation now under debate requires transparent data handling, adding urgency to the upgrade cycle. Financial institutions must capture immutable audit trails to satisfy Basel III, while healthcare providers secure telemedicine records under HIPAA.As penalties tighten, enterprises prioritize unified solutions over fragmented repositories, ensuring consistent policy execution and lowering legal exposure.

Explosion of enterprise unstructured data volumes

Petabytes of multimedia files, sensor logs, and social interactions overwhelm legacy file shares. Banks archive millions of customer chats and video calls, manufacturers manage CAD designs and inspection images, and global design teams generate real-time feedback loops.Remote work has scattered content across personal devices and disparate cloud apps, causing retrieval delays and duplicated effort. Modern platforms that apply machine learning to classify and surface content give organizations a path to transform data sprawl into accessible knowledge, unlocking collaboration gains and faster decision cycles.

Security and privacy concerns in cloud/mobile ECM

Risk-averse sectors hesitate to move regulated content off-premises. Encryption key management, jurisdictional control, and vendor lock-in remain top questions for CISOs. Mobile access introduces endpoints lacking enterprise hardening, expanding the attack surface. Although cloud providers invest in continuous penetration testing and confidential computing, perception lags reality, adding extra approval cycles and slowing rollouts, especially in Europe where data-residency clauses are stringent.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated shift to cloud-native ECM deployments

- AI-driven content intelligence and hyper-automation

- Complexity of merging legacy repositories post-M&A

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Document Management retained a 32.3% leading share of the enterprise content management market in 2024, underscoring its role as the backbone for regulated records and everyday files. Demand remains steady among finance, healthcare, and public agencies that require check-in/out, version control, and audit capabilities. The enterprise content management market size linked to Digital Asset Management is accelerating at a 16.2% CAGR through 2030 as marketers orchestrate rich media across omnichannel campaigns.

Hybrid platforms blur traditional boundaries because vendors embed DAM, workflow orchestration, and records management inside a single interface. This convergence reflects buyer preference for unified licensing and lower integration overhead. Case Management tools serve litigation teams, insurers, and public benefits programs, while Workflow Management aligns with broader process automation suites. Record Management continues to secure long-term archives in energy, pharmaceutical, and aerospace sectors where retention spans decades and penalties for loss are severe.

On-premises deployments held 57.1% of the enterprise content management market size in 2024, a testament to entrenched infrastructure and strict compliance constraints. Nevertheless, cloud subscriptions registered a 15.3% CAGR that outpaced all other modes. The Japanese government's mandate to migrate core systems by 2025 exemplifies the policy push behind adoption, forcing agencies to modernize aging stacks under tight timelines.

Organizations now weigh operational resilience and real-time collaboration more heavily than historical capex accounting. Security objections decline as providers offer customer-managed keys and regional data centers. Hybrid patterns persist, keeping sensitive archives in internal data centers while leveraging SaaS for collaboration. This phased approach eases skills gaps and budget planning yet often serves as a bridge to eventual full-cloud commitment.

Enterprise Content Management Market is Segmented by Component by Solution Type (Content Management, Document Management, and More), by Deployment Mode (On-Premises, Cloud), by Enterprise Size (Small and Medium Enterprises and Large Enterprises), by End-User Industry (Telecom and IT, BFSI, and More), by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 31.6% revenue in 2024 and remains the most mature territory, supported by a deep partner ecosystem and clarified regulatory environment that de-risks project approvals. United States banks modernize legacy imaging systems, and healthcare providers digitize patient records to meet interoperability rules. Canadian federal and provincial agencies migrate their paper archives to the cloud to enhance transparency. Mexican manufacturers adopt ECM for cross-border supply-chain documentation, illustrating spillover effects across the USMCA corridor.

Asia-Pacific delivers the highest 17.4% CAGR through 2030. Japan's public cloud program accelerates adoption across ministries and prefectures. India's Digital India initiative brings ECM to state services and public universities, while South Korea and Australia push AI enhancements in established deployments. These factors combine to give the enterprise content management market its most dynamic regional expansion in Asia-Pacific.

Europe balances opportunity with compliance complexity. GDPR continues to direct spending toward solutions that guarantee data sovereignty, and proposed AI rules tighten documentation controls. Germany's industrial base embeds ECM in Industry 4.0 workflows, the United Kingdom's finance sector pursues paperless mortgage underwriting, and France upgrades hospital and university repositories. Smaller economies such as the Nordics invest in vertical solutions for energy and life sciences, seeking resilience and traceable workflows suitable for highly specialized exports.

- Microsoft Corporation

- OpenText Corporation

- IBM Corporation

- Hyland Software Inc.

- Oracle Corporation

- Box Inc.

- Adobe Inc.

- Xerox Corporation

- M-Files Corp.

- Alfresco Software Inc. (Hyland)

- DocuWare GmbH

- Datamatics Global Services Ltd.

- Hewlett Packard Enterprise Co.

- Capgemini SE

- Newgen Software Technologies Ltd.

- Laserfiche Inc.

- SER Group

- Fabasoft AG

- Everteam Global Services

- KnowledgeLake Inc.

- iManage LLC

- Egnyte Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory compliance mandates for content lifecycle governance

- 4.2.2 Explosion of enterprise unstructured data volumes

- 4.2.3 Accelerated shift to cloud-native ECM deployments

- 4.2.4 AI-driven content intelligence and hyper-automation

- 4.2.5 Convergence of ECM with collaboration hubs (Teams, Slack)

- 4.2.6 EU digital-sovereignty hosting requirements

- 4.3 Market Restraints

- 4.3.1 Security and privacy concerns in cloud/mobile ECM

- 4.3.2 Complexity of merging legacy repositories post-MandA

- 4.3.3 Cross-border data-transfer restrictions (GDPR, DPDPA, etc.)

- 4.3.4 Talent gap in information-governance professionals

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macro Economic Factors on the Market

- 4.8 Porters Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution Type

- 5.1.1 Content Management

- 5.1.2 Document Management

- 5.1.3 Case Management

- 5.1.4 Workflow Management

- 5.1.5 Record Management

- 5.1.6 Digital Asset Management

- 5.1.7 Others

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises (SME)

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 Telecom and IT

- 5.4.2 BFSI

- 5.4.3 Retail and E-commerce

- 5.4.4 Education

- 5.4.5 Manufacturing

- 5.4.6 Media and Entertainment

- 5.4.7 Government and Public Sector

- 5.4.8 Others

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Kenya

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 OpenText Corporation

- 6.4.3 IBM Corporation

- 6.4.4 Hyland Software Inc.

- 6.4.5 Oracle Corporation

- 6.4.6 Box Inc.

- 6.4.7 Adobe Inc.

- 6.4.8 Xerox Corporation

- 6.4.9 M-Files Corp.

- 6.4.10 Alfresco Software Inc. (Hyland)

- 6.4.11 DocuWare GmbH

- 6.4.12 Datamatics Global Services Ltd.

- 6.4.13 Hewlett Packard Enterprise Co.

- 6.4.14 Capgemini SE

- 6.4.15 Newgen Software Technologies Ltd.

- 6.4.16 Laserfiche Inc.

- 6.4.17 SER Group

- 6.4.18 Fabasoft AG

- 6.4.19 Everteam Global Services

- 6.4.20 KnowledgeLake Inc.

- 6.4.21 iManage LLC

- 6.4.22 Egnyte Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment