|

시장보고서

상품코드

1849938

체외(In Vitro) 진단 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)In Vitro Diagnostic - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

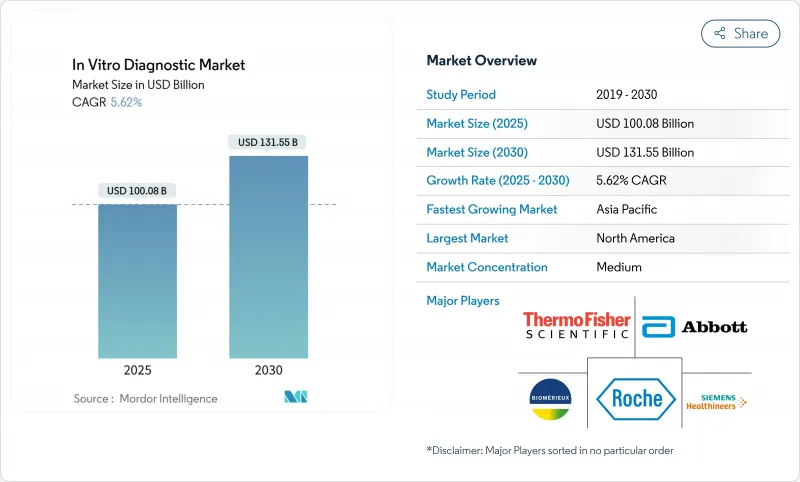

체외 진단 시장은 2025년에 1,000억 8,000만 달러로 평가되었고, 2030년에 CAGR은 5.62%로 성장하여 1,315억 5,000만 달러에 이를 전망입니다.

인공지능 기반 병리학, 플랫폼 자동화, 신속한 현장진단(POC) 기술이 검사 처리 시간을 단축하고 고부가가치 검사의 접근성을 확대하며 시장 확장을 주도하고 있습니다. 만성 질환 부담 증가, 고령화 인구, 조기 검진에 대한 보험사 지원이 꾸준한 검사량 증가를 유지하는 가운데, 소프트웨어 중심 혁신은 데이터 기반 임상 의사결정을 가능케 합니다. 기존 기업들이 차세대 역량을 확보하기 위해 틈새 혁신 기업들을 인수하면서 통합이 가속화되고 있으나, 효소 부족부터 허리케인 관련 정맥주사액 공급 차질에 이르기까지 공급망 취약성은 조달 전략을 형성하는 운영 위험을 부각시키고 있습니다. 규제 변화도 병행되고 있습니다. FDA의 실험실 개발 검사 규정은 준수 비용을 증가시키는 반면, 유럽의 IVDR 전환 기한 연장은 표준화 압박을 제거하지 않고 단지 지연시킬 뿐입니다.

세계의 체외 진단 시장 동향 및 인사이트

만성 질환의 높은 유병률

2024년 미국 성인의 76%가 최소 한 가지 만성 질환을 보고했으며, 이는 당뇨병, 심혈관 질환, 종양학, 신장학 치료 분야의 지속적인 진단 수요를 주도하고 있습니다. 빈번한 모니터링은 하류 치료 비용을 절감하는 조기 개입에 대한 지불자의 인센티브와 부합합니다. 검사실들은 증상 발현 전 신장 손상을 경고하는 NGAL, 시스타틴 C, KIM-1 검사법 도입으로 대응하고 있습니다. AI 모델은 종단적 결과 패턴을 분류해 악화 조기 예측이 가능해졌으며, 인력 부족 속에서도 자동화로 처리량 유지가 가능합니다. 이러한 역학은 체외진단 시장을 만성질환 치료 경로의 필수 기둥으로 자리매김하게 합니다.

현장진단(POC)의 확대 적용

POC 플랫폼은 단일 분석 스트립에서 15분 이내에 실험실 수준의 결과를 제공하는 다중 분자 시스템으로 진화했습니다. 로슈의 12종 표적 호흡기 PCR과 드래곤플라이의 휴대용 원숭이두창 검사는 95% 이상의 민감도와 현장 휴대성을 결합한 이러한 도약을 보여줍니다. 소매 클리닉이 이러한 도구를 주류화하고 있습니다. CVS는 현재 1,600개 지점에서 3-in-1 독감-코로나 패널을 제공하며 접근성을 확대하는 동시에 병원 부담을 완화하고 있습니다. 지불자에게는 급성 감염 관리에서 절약된 매 순간이 전파 위험과 고비용 입원을 억제하여 POC 경제성을 강화합니다. 결과적으로 아시아태평양 지역 일차 진료 체인에서 보급 가속화가 전체 체외진단 시장 성장을 촉진합니다.

엄격한 다지역 규제 승인 일정

FDA의 실험실 개발 검사 규정은 최대 35억 6,000만 달러의 신규 준수 비용을 부과하여 중소 혁신 기업의 예산을 압박하고 제품 출시를 지연시키고 있습니다. 유럽의 IVDR 연장은 시간을 벌어주지만, 제조사들은 여전히 품질 시스템을 업그레이드하고 인증기관(Notified Body) 슬롯을 확보해야 합니다. 이는 일정 지연을 초래하는 자원 병목 현상입니다. 관할권 간 이중 제출은 전략을 분산시키고 신기술 분석법 탐색에 투입될 R&D 예산을 전용시킵니다. 역사적 선례가 부족한 AI 기반 도구의 경우 서류 준비와 심사관 교육이 복잡해져 시장 성장 궤도에 제동이 걸리는 현상이 두드러집니다.

부문 분석

2024년 체외진단 시장 점유율에서 면역진단(Immunodiagnostics)이 29.05%를 차지했으며, 이는 감염병 및 대사성 검사 필수 요소인 단백질 검사에 기반합니다. 그러나 차세대 시퀀싱, 멀티플렉스 PCR, 등온 증폭 기술이 정밀의학의 주류로 자리잡으면서 분자진단 시장은 연간 6.59% 성장할 것으로 전망되어 해당 부문의 체외진단 시장 규모를 끌어올릴 전망입니다. 로슈의 온도 트리거 방식 12종 병원체 PCR은 실행 시간을 더욱 단축시켜, 분산형 환경에서 분자진단 도입을 제한했던 처리량 제약을 해소합니다.

교차 수정이 증가하고 있습니다. 하이브리드 플랫폼은 동일한 카트리지에서 핵산과 항원을 검출하여 분자 특이성과 면역분석법의 편의성을 결합합니다. AI 알고리즘은 유전자 발현 결과와 혈청학적 표지자를 결합하여 종양학 및 항생제 관리 분야의 예후 정확도를 개선합니다. 이에 따라 실험실들은 기존 면역분석법에서 저비용, 고복합 핵산 형식으로 작업 부하를 이전하며, 2030년까지 분자진단의 우수한 성과를 지속할 것입니다.

2024년 체외진단 시장 규모에서 시약이 55.35%를 차지했으며, 이는 소모품의 반복 구매 경제성을 반영합니다. 그러나 실험실이 워크플로우 효율성과 예측적 인사이트을 제공하는 AI 분석에 투자함에 따라 소프트웨어 및 서비스 부문은 연평균 9.35% 성장률을 보이고 있습니다. 필립스와 아이벡스는 병리학자 검토 전 디지털 병리학 AI가 슬라이드를 선별했을 때 37%의 생산성 향상을 보고했습니다.

구독 모델은 불규칙한 분석기 판매를 반복 수익으로 전환하여 공급업체 인센티브를 성과 기반 성과와 연계합니다. 클라우드 네이티브 플랫폼은 지속적인 학습을 위한 야간 알고리즘 업그레이드 및 다중 사이트 데이터 풀링을 가능하게 합니다. 그 결과 시약 선도 기업들은 키트 판매와 알고리즘 라이선스를 묶어 체외진단 시장 전반에 걸쳐 고객 잠금을 공고히 하고 있습니다.

지역 분석

북미는 강력한 보험급여, 확고한 연구개발(R&D), 선도적인 인공지능(AI) 도입을 바탕으로 2024년 체외진단 시장 점유율 38.08%를 유지했습니다. FDA의 LDT 규정은 비용이 많이 들지만, 주간 조화를 이루면 품질 기준을 높이고 전국적인 데이터 상호운용성을 촉진할 수 있습니다. 소매 의료는 접근성을 재정의하고 있습니다. CVS와 월그린스는 진단 과정을 단축하고 새로운 매출 흐름을 창출하는 POC 분자 패널을 도입했습니다. 한편, 공급망 충격, BD 배지 부족, 박스터 정맥주사액 공급 차질은 국내 제조 회복탄력성에 대한 재투자를 촉발했습니다.

아시아태평양 지역은 일본, 중국, 인도의 인구 고령화와 정부 자금 확대에 힘입어 연평균 6.85% 성장률로 가장 빠르게 성장하는 지역입니다. 랩코프(Labcorp)의 BML 재팬과의 확장된 협력 및 산슈어(Sansure)의 패혈증 검사 중국 합작 투자는 정밀의학 도입을 가속화하는 국경 간 기술 이전을 보여줍니다. 중국 국내 기업들은 방대한 현지 검진 사업 경험을 활용해 수출용 비용 효율적인 분석기 규모를 확대하고 있습니다. 이러한 움직임들은 종합적으로 지역 체외진단 시장 역량을 확대하고 전 세계적으로 경쟁적 가격 압박을 촉진합니다.

유럽은 IVDR(체외진단기기규정) 혼란 속에서도 꾸준한 성장을 기록합니다. 전환 지연으로 당장의 검사 부족은 막았으나 장기적 규격 조화는 불가피해 소규모 제조사들은 전략적 파트너 확보 또는 시장 철수를 모색하게 됩니다. 필립스-아이벡스의 AI 우위와 병리 검사 처리 시간을 단축하는 디아그네시아의 전립선 AI 협력 사례에서 드러나듯, 유럽은 공간오믹스와 디지털 병리학 분야에서 선도적 위치를 차지하고 있습니다. 중동, 아프리카, 라틴아메리카는 주로 POC(현장진단) 및 약물 스크리닝 프로그램을 통해 역량을 구축하고 있습니다. 인텔리전트 바이오(Intelligent Bio)와 아이비 진단(IVY Diagnostics)의 협력은 규제 및 문화적 격차를 해소하는 유통망을 확장하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성 질환의 높은 유병률

- 현장진단(POC)의 확대 적용

- 지속적인 플랫폼 혁신(AI, 자동화, 다중화)

- 맞춤형/동반진단(Companion Diagnostics)의 수용 확대

- 소매 클리닉 및 가정 내 검체 채취 생태계

- 공간 오믹스와 IVD 워크플로우의 융합

- 시장 성장 억제요인

- 엄격한 다지역 규제 승인 일정

- 신흥 검사 분야 전반에 걸친 보험급여 불확실성

- 연결형 IVD의 사이버 보안 및 데이터 상호운용성 격차

- 효소/시약 공급망의 지정학적 수출 규제에 대한 익스포저

- 공급망 분석

- 기술의 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 검사 유형별

- 임상 화학

- 면역진단

- 분자진단

- 혈액학

- 응고

- 미생물학

- 기타 검사 유형

- 제품별

- 기기

- 시약 및 키트

- 소프트웨어 및 서비스

- 사용성별

- 일회용 IVD 기기

- 재사용 가능 기기

- 용도별

- 감염증

- 당뇨병

- 종양학

- 심장병학

- 자가면역질환

- 신장학

- 기타 용도

- 최종 사용자별

- 독립형 실험실

- 병원 기반 검사실

- 현장진료(Point-of-Care) 환경

- 재택 케어와 자기 검사 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- F. Hoffmann-La Roche Ltd

- Abbott Laboratories

- Siemens Healthineers AG

- Danaher Corp(Beckman Coulter, Cepheid)

- Thermo Fisher Scientific Inc.

- Sysmex Corp

- bioMerieux SA

- Becton, Dickinson and Company

- Bio-Rad Laboratories Inc.

- Qiagen NV

- DiaSorin SpA

- Grifols SA

- Agilent Technologies Inc.

- Ortho Clinical Diagnostics/QuidelOrtho

- Hologic Inc.

- Illumina Inc.

- PerkinElmer Inc.

- Randox Laboratories Ltd

- Meril Diagnostics Pvt Ltd

제7장 시장 기회와 장래의 전망

HBR 25.11.14The in vitro diagnostics market stood at USD 100.08 billion in 2025 and is forecast to reach USD 131.55 billion by 2030, advancing at a 5.62% CAGR.

Expansion is propelled by AI-enabled pathology, platform automation, and rapid point-of-care (POC) technologies that compress turnaround times and broaden access to high-value testing. Intensifying chronic disease burdens, an aging population, and payer support for early detection sustain steady test volume growth, while software-centric innovations unlock data-driven clinical decisions. Consolidation has accelerated as incumbents purchase niche innovators to secure next-generation capabilities, though supply-chain fragilities, from enzyme shortages to hurricane-related IV-fluid disruptions, highlight operational risks that shape sourcing strategies. Regulatory shifts run in parallel: the FDA's laboratory-developed test rule raises compliance costs even as Europe's IVDR transition extensions delay, not remove, standardization pressures.

Global In Vitro Diagnostic Market Trends and Insights

High Prevalence of Chronic Diseases

Seventy-six percent of US adults reported at least one chronic ailment in 2024, driving sustained diagnostic demand in diabetes, cardiovascular, oncology, and nephrology care. Frequent monitoring aligns with payer incentives for early intervention that trims downstream treatment costs. Laboratories respond by introducing assays for NGAL, cystatin C, and KIM-1 that flag kidney injury before symptoms appear. AI models now triage longitudinal result patterns to predict exacerbations earlier, while automation sustains throughput amid workforce shortages. These dynamics establish the in vitro diagnostics market as an indispensable pillar of chronic-care pathways.

Expanding Adoption of Point-of-Care Diagnostics

POC platforms have evolved from single-analyte strips to multiplex molecular systems that deliver laboratory-grade results in under 15 minutes. Roche's 12-target respiratory PCR and Dragonfly's portable mpox test exemplify this leap, pairing sensitivity above 95% with field portability. Retail clinics are mainstreaming such tools: CVS now offers 3-in-1 flu-COVID panels across 1,600 sites, broadening access while easing hospital load. For payers, every minute saved in acute infection management curbs transmission risk and costly admissions, reinforcing POC economics. Consequently, penetration in Asia-Pacific primary-care chains accelerates overall in vitro diagnostics market growth.

Stringent Multi-Region Regulatory Approval Timelines

The FDA's laboratory-developed test rule imposes up to USD 3.56 billion in new compliance costs, stretching smaller innovators' budgets and delaying product launches. Europe's IVDR extension buys time, yet manufacturers must still upgrade quality systems and secure notified-body slots, a resource bottleneck that inflates timelines. Dual submissions across jurisdictions fragment strategies and divert R&D spend away from new assay exploration. The drag is acute for AI-based tools that lack historical precedents, complicating dossier preparation and reviewer training, thereby tempering the overall in vitro diagnostics market trajectory.

Other drivers and restraints analyzed in the detailed report include:

- Continuous Platform Innovation (AI, Automation, Multiplexing)

- Growing Acceptance of Personalized / Companion Diagnostics

- Reimbursement Uncertainty Across Emerging Test Classes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Immunodiagnostics captured 29.05% of in vitro diagnostics market share in 2024, anchored by protein assays indispensable to infectious disease and metabolic testing. Yet molecular diagnostics is forecast to grow 6.59% annually, lifting the segment's in vitro diagnostics market size as next-generation sequencing, multiplex PCR, and isothermal amplification become mainstays of precision medicine. Roche's temperature-triggered 12-pathogen PCR further compresses run-times, removing throughput constraints that once limited molecular adoption in decentralized settings.

Cross-fertilization is rising: hybrid platforms detect nucleic acids and antigens in the same cartridge, blending molecular specificity with immunoassay ease. AI algorithms stitch gene-expression results with serological markers, refining prognostic accuracy in oncology and antimicrobial stewardship. Laboratories thus migrate workloads from legacy immunoassays to low-cost, high-plex nucleic-acid formats, sustaining molecular's outperformance through 2030.

Reagents represented 55.35% of in vitro diagnostics market size in 2024, reflecting repeat-purchase economics of consumables. However, software and services are growing at 9.35% CAGR as laboratories invest in AI analytics that unlock workflow efficiencies and predictive insights. Philips and Ibex reported 37% productivity gains when digital pathology AI triaged slides before pathologist review.

Subscription models convert lumpy analyzer sales into recurring revenue, aligning vendor incentives with outcome-based performance. Cloud-native platforms enable overnight algorithm upgrades and multi-site data pooling for continuous learning. As a result, reagent leaders are bundling algorithm licenses with kit sales, cementing customer lock-in across the in vitro diagnostics market.

The in Vitro Diagnostics Market Report is Segmented by Test Type (Clinical Chemistry, Molecular Diagnostics, and More), Product (Instruments, Reagents and More), Usability (Disposable IVD Devices, Reusable Equipment), Application (Infectious Diseases, Oncology, Cardiology, and More), End User (Stand-Alone Laboratories, and More), Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 38.08% in vitro diagnostics market share in 2024 on the back of robust reimbursement, entrenched R&D, and pioneering AI deployments. The FDA's LDT rule, while costly, could lift quality standards and foster nationwide data interoperability if harmonized across states. Retail health continues to redefine access; CVS and Walgreens deploy POC molecular panels that shorten diagnostic journeys and create new volume streams. Meanwhile, supply-chain shocks, BD culture-media shortages and Baxter IV-fluid disruptions, have prompted renewed investment in domestic manufacturing resiliency.

Asia-Pacific is the fastest-growing region at 6.85% CAGR, propelled by demographic aging and government funding expansions in Japan, China, and India. Labcorp's extended tie-up with BML Japan and Sansure's China joint venture for sepsis assays illustrate cross-border technology transfer that accelerates precision medicine uptake. Domestic Chinese firms are scaling cost-efficient analyzers for export, leveraging experience from vast local screening initiatives. These moves collectively enlarge regional in vitro diagnostics market capacity and foster competitive pricing pressures globally.

Europe posts steady gains despite IVDR turbulence. Transition delays prevent immediate test shortages, yet long-term harmonization is unavoidable, compelling smaller manufacturers to seek strategic partners or exit. The continent commands leadership in spatial-omics and digital pathology, evidenced by Philips-Ibex's AI edge and Diagnexia's prostate AI partnership that shortens pathology turnaround. Middle East, Africa, and Latin America build capacity mainly through POC and drug-screening programs, as Intelligent Bio's collaboration with IVY Diagnostics expands distribution networks that bridge regulatory and cultural gaps.

- Roche

- Abbott Laboratories

- Siemens Healthineers

- Danaher Corp (Beckman Coulter, Cepheid)

- Thermo Fisher Scientific

- Sysmex Corp

- bioMerieux

- Beckton Dickinson

- Bio-Rad Laboratories

- QIAGEN

- DiaSorin

- Grifols

- Agilent Technologies

- Ortho Clinical Diagnostics / QuidelOrtho

- Hologic

- Illumina

- PerkinElmer

- Randox Laboratories

- Meril Diagnostics Pvt Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Prevalence Of Chronic Diseases

- 4.2.2 Expanding Adoption Of Point-Of-Care (POC) Diagnostics

- 4.2.3 Continuous Platform Innovation (AI, Automation, Multiplexing)

- 4.2.4 Growing Acceptance Of Personalized / Companion Diagnostics

- 4.2.5 Retail-Clinic & At-Home Sampling Ecosystems

- 4.2.6 Convergence Of Spatial-Omics & IVD Workflows

- 4.3 Market Restraints

- 4.3.1 Stringent Multi-Region Regulatory Approval Timelines

- 4.3.2 Reimbursement Uncertainty Across Emerging Test Classes

- 4.3.3 Cyber-Security & Data-Interoperability Gaps In Connected IVD

- 4.3.4 Enzyme / Reagent Supply-Chain Exposure To Geo-Political Export Controls

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Test Type

- 5.1.1 Clinical Chemistry

- 5.1.2 Immunodiagnostics

- 5.1.3 Molecular Diagnostics

- 5.1.4 Hematology

- 5.1.5 Coagulation

- 5.1.6 Microbiology

- 5.1.7 Other Test Types

- 5.2 By Product

- 5.2.1 Instruments

- 5.2.2 Reagents & Kits

- 5.2.3 Software & Services

- 5.3 By Usability

- 5.3.1 Disposable IVD Devices

- 5.3.2 Re-usable Equipment

- 5.4 By Application

- 5.4.1 Infectious Diseases

- 5.4.2 Diabetes

- 5.4.3 Oncology

- 5.4.4 Cardiology

- 5.4.5 Auto-immune Disorders

- 5.4.6 Nephrology

- 5.4.7 Other Applications

- 5.5 By End User

- 5.5.1 Stand-alone Laboratories

- 5.5.2 Hospital-based Laboratories

- 5.5.3 Point-of-Care Settings

- 5.5.4 Home-care & Self-testing Users

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 F. Hoffmann-La Roche Ltd

- 6.3.2 Abbott Laboratories

- 6.3.3 Siemens Healthineers AG

- 6.3.4 Danaher Corp (Beckman Coulter, Cepheid)

- 6.3.5 Thermo Fisher Scientific Inc.

- 6.3.6 Sysmex Corp

- 6.3.7 bioMerieux SA

- 6.3.8 Becton, Dickinson and Company

- 6.3.9 Bio-Rad Laboratories Inc.

- 6.3.10 Qiagen NV

- 6.3.11 DiaSorin SpA

- 6.3.12 Grifols SA

- 6.3.13 Agilent Technologies Inc.

- 6.3.14 Ortho Clinical Diagnostics / QuidelOrtho

- 6.3.15 Hologic Inc.

- 6.3.16 Illumina Inc.

- 6.3.17 PerkinElmer Inc.

- 6.3.18 Randox Laboratories Ltd

- 6.3.19 Meril Diagnostics Pvt Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment