|

시장보고서

상품코드

1849951

미국의 피임기구 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)U.S. Contraceptive Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

미국의 피임기구 시장은 2025년에 53억 9,000만 달러, 2030년에는 71억 2,000만 달러에 이르며, 예측 기간 중 CAGR은 5.71%를 나타낼 전망입니다.

소비자가 생식의 자율성을 중시하고, 메디케이드의 상환이 확대되고, 고용자 부담의 급여가 기세를 늘리는 가운데, 도브스 후의 규제의 혼란에도 불구하고, 성장은 안정되고 있습니다. 장시간 작용하는 가역적 피임약(LARC)은 뛰어난 효능과 편리성으로부터 인기를 끌고 있는 한편, 소비자 직접 판매 채널과 원격 의료는 액세스를 합리화해, 대면 진찰의 필요성을 제한하고 있습니다. 통증이 적은 IUD 삽입 기구 등 기술 업그레이드는 복용을 막아 온 역사적인 장벽에 대처하고 기존의 층 이외에도 널리 어필합니다. 남성용 피임기구의 연구개발에 대한 병행투자는 책임분담의 진화를 나타내는 것으로, 소매 약국은 온라인 플랫폼이 가장 빠른 성장을 이루는 중에서도 매우 중요한 액세스 포인트로서의 역할을 확고하게 하고 있습니다. IUD의 유해 사건과 관련된 소송이 계속되고 있거나 일부 지역에서 문화적인 반발이 있는 것이 전체적인 수요를 억제하고 있지만, 좌석에는 이르지 못하고 있습니다.

미국의 피임기구 시장 동향과 인사이트

메디케이드 상환 확대가 공정한 접근을 촉진

2024년 8월 CMS 고시는 각 주에 가족계획서비스를 비용부담 없이 커버할 것을 의무화하고 LARC 보급에 대한 길을 원활하게 했습니다. JAMA Health Forum의 연구에서는 산후 60일 이내의 LARC 사용률이 1.58% 상승한 것과 산후 LARC의 보험상환을 관련시켰습니다.

LARC는 원하는 피임법의 선택으로 기세를 늘립니다.

도브스 후의 보다 장기적인 피임에 대한 수요는 더 많은 소비자를 IUD나 임플란트로 향하게 합니다. 빅스비 센터는 LARC의 요구가 더 높다고 보고했으며, 2024년 2,855개의 IUD와 임플란트를 2024년에 배포했는데, 이는 비용 효율성과 신뢰성에 대한 의식 증가를 반영했습니다.

도브스 판결 이후 규제 불확실성이 액세스 문제를 일으킵니다.

낙태가 전면적으로 금지된 주에서는 도브스 1년 후에 긴급 피임약 처방이 65% 감소했고, 경구 피임약 처방도 25.6% 감소했습니다.

부문 분석

콘돔이 31.36%에서 가장 큰 단일 피임기구 발판을 유지하고 있지만 호르몬 IUD는 사용자가 장기적인 솔루션으로 이동함에 따라 2030년까지 연평균 복합 성장률(CAGR)이 8.43%로 가장 높은 성장을 예측했습니다. 미국의 피임용 IUD 시장 규모는 CDC의 2024년 실천 권고가 장착 프로토콜을 합리화하고 공정한 케어를 강조함에 따라 확대되었습니다. 구리 IUD의 기술 혁신은 세베라의 MIUDELLA(40년만에 허가 된 호르몬이없는 시스템)에 의해 가속화됩니다. 다이어프램과 자궁 경관 캡과 같은 틈새 장벽 장치는 온 디맨드 비 호르몬 보호를 요구하는 소비자를 수용하며, 에보펨의 Phexxi 젤은 호르몬이없는 질 옵션에 대한 관심을 다시 높입니다.

비호르몬 피임법은 2024년에는 54.56%의 리드를 유지하며 콘돔의 보급과 구리 기반 기구에 의해 지원되었습니다. 그러나 호르몬 대체 방법은 첨단 전달 시스템이 전신 노출과 부작용을 줄여 CAGR 7.98%를 나타낼 전망입니다. 바이엘과 데어의 글루콘산 제일철 링은 편의성과 저호르몬 부하의 양립을 목표로 한 혁신의 일례입니다. 한편, 아연과 철로 만들어진 형상 적응 IUD 프레임의 조사는 확실한 피임을 보장하는 호르몬이없는 디자인에 대한 시장 의욕을 반영합니다.

미국의 피임기구 시장은 기구 유형(콘돔, 자궁내 기구, 질링, 피하 임플란트 등), 기술(호르몬 기구, 비호르몬 기구), 성별(남성, 여성), 최종 사용자(홈 케어/개인 사용자, 병원 등), 유통 채널(소매 약국 및 드럭스토어, 병원 약국 등)으로 구분됩니다. 시장 및 예측은 금액(달러)으로 제공됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 피임기구에 대한 메디케이드의 상환 확대와 고용주에 의한 피임 급부의 확대(2023년 이후)

- 장기 작용형 가역적 피임약(LARC)의 도입 촉진

- IUD 삽입·전달 시스템에 있어서의 기술적 진보

- 소비자 직접 판매 및 원격 의료 플랫폼이 기구의 매출 증진

- 10대의 임신 방지와 원치 않는 임신을 타겟으로 한 캠페인

- 여성의 건강에 대한 관심 증가와 남성 피임약의 연구 개발 확대

- 시장 성장 억제요인

- 도부스 판결 후의 규제의 불확실성은 액세스에 영향

- IUD의 유해 사건과 관련된 리콜과 소송

- 특정 인구통계에서 문화적 및 종교적 갈등

- 신규 및 고액 피임기구에 대한 보험 적용의 제한

- 가치/공급망 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 기구 유형별

- 콘돔

- 자궁 내 장치(구리 IUD, 호르몬 IUD)

- 질 링

- 피하 임플란트

- 자궁경부 캡

- 자궁경부 캡

- 스폰지

- 기타 장치(패치, 젤 기반 장벽)

- 기술별

- 호르몬 기구

- 비호르몬 기구

- 성별

- 남성

- 여성

- 최종 사용자별

- 홈 케어/개인 사용자

- 병원

- 진료소 및 지역 보건소

- 전문 외래 수술 센터(ASC)

- 유통 채널별

- 소매 약국 및 드럭스토어

- 병원 약국

- 온라인 채널 및 소비자 직거래 플랫폼

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- CooperSurgical Inc.

- Bayer AG

- Teva Pharmaceutical Industries Ltd

- Church & Dwight Co., Inc.(Trojan)

- Reckitt Benckiser Group plc(Durex)

- AbbVie Inc.

- Pfizer Inc.

- Viatris Inc.

- Pregna International Ltd.

- DKT International

- Evofem Biosciences, Inc.

- Agile Therapeutics, Inc.

- Perrigo(HRA Pharma)

- Veru Inc.

- HLL Lifecare Ltd.

- Femcap Inc.

- Okamoto Industries, Inc.

- Mayne Pharma Commercial LLC

- Amneal Pharmaceuticals Inc.

제7장 시장 기회와 향후 전망

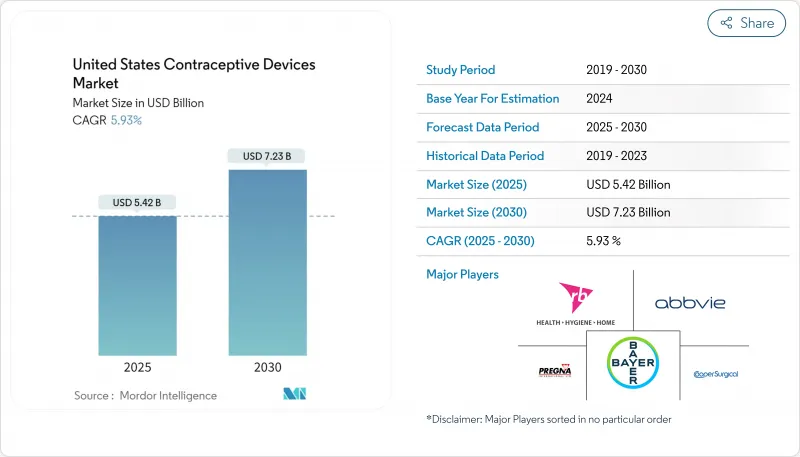

KTH 25.11.04The United States contraceptive devices market is valued at USD 5.39 billion in 2025 and is on track to hit USD 7.12 billion by 2030, supported by a 5.71% CAGR during the forecast period.

Growth holds steady despite post-Dobbs regulatory turbulence as consumers place higher priority on reproductive autonomy, Medicaid reimbursement expands, and employer-sponsored benefits add momentum. Long-acting reversible contraceptives (LARCs) gain popularity because of superior efficacy and convenience, while direct-to-consumer channels and telehealth streamline access and limit the need for in-person visits. Technology upgrades, such as less-painful IUD insertion tools, address historic barriers to uptake and broaden appeal beyond traditional demographics. Parallel investment in male contraceptive R&D signals an evolving view of shared responsibility, and retail pharmacies solidify their role as pivotal access points even as online platforms post the fastest growth. Ongoing litigation linked to IUD adverse events and cultural pushback in select regions temper, but do not derail, overall demand.

U.S. Contraceptive Devices Market Trends and Insights

Expansion of Medicaid Reimbursement Drives Equitable Access

The August 2024 CMS bulletin obliges states to cover family-planning services without cost-sharing, smoothing the path to LARC uptake. A JAMA Health Forum study linked separate postpartum LARC reimbursement with a 1.58 percentage-point jump in overall LARC use within 60 days after delivery, underscoring how policy shifts remove long-standing cost barriers for underserved groups.

LARCs Gain Momentum as Preferred Contraceptive Choice

Post-Dobbs demand for longer-term protection pushes more consumers toward IUDs and implants. The Bixby Center reported higher LARC requests, while Tulsa County's Take Control Initiative distributed 2,855 IUDs and implants in 2024, reflecting heightened awareness of cost-effectiveness and reliability.

Post-Dobbs Regulatory Uncertainty Creates Access Challenges

States with full abortion bans saw a 65% plunge in emergency contraceptive fills one year after Dobbs, along with a 25.6% fall in oral contraceptive prescriptions, stoking confusion among providers about legal parameters and hindering timely dispensing.

Other drivers and restraints analyzed in the detailed report include:

- Technological Innovation Enhances User Experience

- Telehealth Transforms Contraceptive Access

- IUD Litigation Dampens Market Confidence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Condoms retain the largest single-device foothold at 31.36%, yet hormonal IUDs deliver the highest projected growth at 8.43% CAGR through 2030 as users shift toward longer-term solutions. The United States contraceptive devices market size for IUDs is expanding as CDC's 2024 practice recommendations streamline placement protocols and emphasize equitable care. Copper IUD innovation accelerates with Sebela's MIUDELLA, the first hormone-free system cleared in four decades. Niche barrier devices such as diaphragms and cervical caps serve consumers seeking on-demand, non-hormonal protection, while Evofem's Phexxi gel re-energizes interest in hormone-free vaginal options.

Non-hormonal methods preserved a 54.56% lead in 2024, anchored by condom ubiquity and copper-based devices. Hormonal alternatives, however, are climbing at 7.98% CAGR as advanced delivery systems lower systemic exposure and side-effects. Bayer and Dare's ferrous gluconate ring exemplifies innovation aimed at combining convenience with lower hormonal loads. Meanwhile, research into shape-adaptive IUD frames crafted from zinc or iron reflects the market's appetite for hormone-free designs that still guarantee robust contraception.

U. S. Contraceptive Devices Market is Segmented by Device Type (Condoms, Intra-Uterine Devices, Vaginal Rings, Subdermal Implants and More), Technology (Hormonal Devices and Non-Hormonal Devices), Gender (Male and Female), End User (Home-Care / Individual Users, Hospitals and More) and Distribution Channel (Retail Pharmacies & Drug Stores, Hospital Pharmacies and More). The Market and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- The Cooper Companies

- Bayer

- Teva Pharmaceutical Industries

- Church & Dwight Co., Inc. (Trojan)

- Reckitt Benckiser Group plc (Durex)

- Abbvie

- Pfizer

- Viatris

- Pregna International Ltd.

- DKT International

- Evofem Biosciences, Inc.

- Agile Therapeutics, Inc.

- Perrigo(HRA Pharma)

- Veru

- HLL Lifecare Ltd.

- Femcap Inc.

- Okamoto Industries, Inc.

- Mayne Pharma Commercial LLC

- Amneal Pharmaceuticals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Medicaid Reimbursement for Contraceptive Devices Coupled with Employer-Sponsored Contraception Benefits Expansion (Post-2023)

- 4.2.2 Accelerating Adoption of Long-Acting Reversible Contraceptives (LARC)

- 4.2.3 Technological Advancements in IUD Insertion & Delivery Systems

- 4.2.4 Direct-to-Consumer & Telehealth Platforms Boosting Device Sales

- 4.2.5 Campaigns Targeting Teen Pregnancy Prevention and Unwanted Pregnancy

- 4.2.6 Increasing Focus on Women's Health and Growing male Contraceptive R&D

- 4.3 Market Restraints

- 4.3.1 Regulatory Uncertainty After Dobbs Decision Affecting Access

- 4.3.2 Recalls and Litigation Linked to IUD Adverse Events

- 4.3.3 Cultural and Religious Opposition in Specific Demographics

- 4.3.4 Limited Insurance Coverage for New and Premium Contraceptive Devices

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Device Type

- 5.1.1 Condoms

- 5.1.2 Intra-Uterine Devices (Copper IUD, Hormonal IUD)

- 5.1.3 Vaginal Rings

- 5.1.4 Subdermal Implants

- 5.1.5 Diaphragms

- 5.1.6 Cervical Caps

- 5.1.7 Sponges

- 5.1.8 Other Devices (Patches, Gel-Based Barriers)

- 5.2 By Technology

- 5.2.1 Hormonal Devices

- 5.2.2 Non-Hormonal Devices

- 5.3 By Gender

- 5.3.1 Male

- 5.3.2 Female

- 5.4 By End User

- 5.4.1 Home-care / Individual Users

- 5.4.2 Hospitals

- 5.4.3 Clinics and Community Health Centers

- 5.4.4 Specialty and Ambulatory Surgery Centers

- 5.5 By Distribution Channel

- 5.5.1 Retail Pharmacies and Drug Stores

- 5.5.2 Hospital Pharmacies

- 5.5.3 Online Channels and Direct-to-Consumer Platforms

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 CooperSurgical Inc.

- 6.4.2 Bayer AG

- 6.4.3 Teva Pharmaceutical Industries Ltd

- 6.4.4 Church & Dwight Co., Inc. (Trojan)

- 6.4.5 Reckitt Benckiser Group plc (Durex)

- 6.4.6 AbbVie Inc.

- 6.4.7 Pfizer Inc.

- 6.4.8 Viatris Inc.

- 6.4.9 Pregna International Ltd.

- 6.4.10 DKT International

- 6.4.11 Evofem Biosciences, Inc.

- 6.4.12 Agile Therapeutics, Inc.

- 6.4.13 Perrigo(HRA Pharma)

- 6.4.14 Veru Inc.

- 6.4.15 HLL Lifecare Ltd.

- 6.4.16 Femcap Inc.

- 6.4.17 Okamoto Industries, Inc.

- 6.4.18 Mayne Pharma Commercial LLC

- 6.4.19 Amneal Pharmaceuticals Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment