|

시장보고서

상품코드

1849999

3D 프린팅 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)3D Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

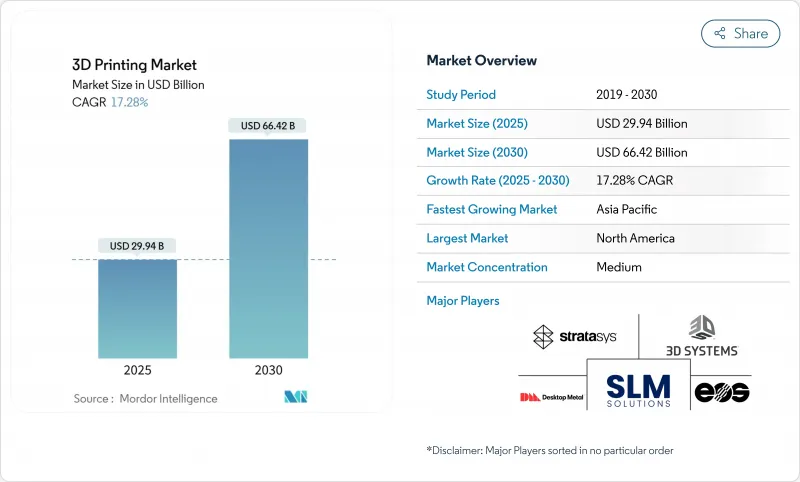

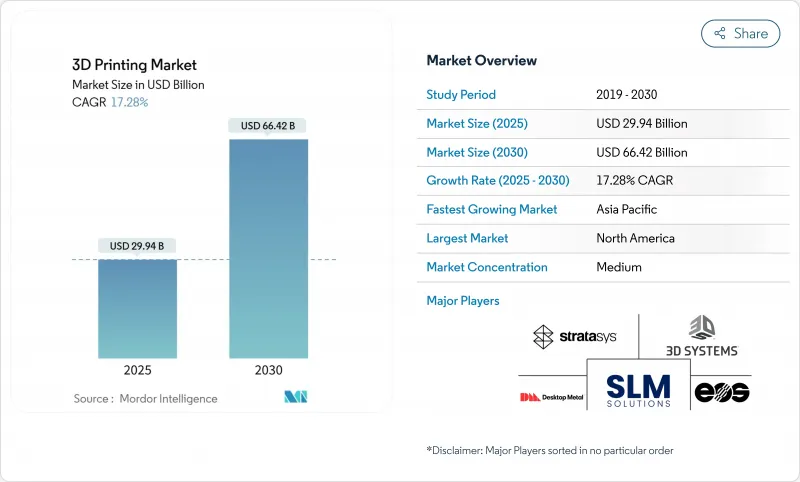

3D 프린팅 시장 규모는 2025년에 299억 4,000만 달러로 추정되고, 예측 기간(2025-2030년)의 CAGR은 17.28%를 나타내, 2030년에는 664억 2,000만 달러에 달할 것으로 예상됩니다.

이 성장 호를 지원하는 것은 기계 처리 능력의 향상, 풍부한 재료 포트폴리오, 래피드 프로토타이핑에서 소량·중량의 최종 용도 생산으로의 기술의 단계적 이행입니다. 항공우주, 헬스케어, 자동차의 각 기업은 현재 비행 하드웨어, 임베디드 장치, 구조용 브래킷용 금속·폴리머 부품을 검증하고 있어 인증 파우더와 클로즈드 루프 모니터링 수요를 가속화하고 있습니다. 동시에 서비스 뷰로는 멀티 레이저 시스템을 확장하고 클라우드 기반 용량을 제공함으로써 신규 채용 기업의 설비 투자 위험을 완화합니다. 미국과 중국의 전략적 정부 자금 지원은 인증 일정을 단축하고 설비 비용을 상쇄하는 반면, ASTM 주도 표준화는 지역 간 시험 프로토콜의 조화를 기대합니다. 나노 차원의 데스크톱 금속 인수와 같은 통합은 가법적 워크플로우가 차세대 공급망을 지원한다는 투자자의 확신을 보여줍니다.

세계의 3D 프린팅 시장 동향과 인사이트

북미의 정부 출자 적층 조형 허브

연방 및 주정부 프로그램은 국내 채용을 가속화하고 있습니다. 2025년 1월, America Makes는 in-situ 측정, 지속 가능한 분말 재활용 및 저비용 알루미늄 파라미터 세트에 초점을 맞춘 프로젝트에 210만 달러를 수여했습니다. 이 이니셔티브는 RTX 기술 연구센터, 에디슨 용접 연구소, 지역 작업점을 연결하는 공동 테스트 침대를 구축하는 것입니다. 1,500만 달러의 ASTM 표준화 센터 오브 엑셀런스(ASTM Standardization Center of Excellence) 하에서 보완적인 자금을 제공함으로써 데이터 포맷과 테스트 쿠폰의 조화를 이루고, 연구 프로토타입과 공인 생산품 사이에 존재하는 지속적인 갭을 메울 수 있습니다. 제조 파라미터의 엔벨로프를 성문화함으로써 생태계는 중복 시험을 줄이고, 특히 항공우주 및 의료기기 공급망에서 3D 프린팅 시장의 인증 주기를 단축합니다.

유럽에서 온 디맨드 항공우주 예비 부품에 금속 AM 채택 급증

유럽의 MRO 공급자는 창고 보관의 오버헤드 없이 생산 중단 부품을 교체하기 위해 분말 야금 융합을 점점 더 활용하고 있습니다. 멀티레이저 레이저 파우더 베드 융합에 의해 제조된 SpaceX사의 Raptor 3 챔버는 시연자로부터 비행 가능한 부품까지의 경로를 보여줍니다. 유럽의 규제기관은 비중요 금속 내장품 가이드라인을 명확히 하여 30개 이하의 생산량에서도 소량 생산이 경제적으로 유리하게 되었습니다. 루프트한자 테크니크, 사프란, 롤스 로이스는 현재 유지보수 시점에 인쇄 주문을 트리거하는 디지털 재고를 보유하고 있으며, 리드 타임을 몇 주에서 48시간 미만으로 단축하고 있습니다. 티타늄과 인코넬 파우더가 항공우주 등급의 재현성에 도달함에 따라 유럽의 3D 프린팅 시장은 현지 생산과 관련된 탄소 발자국의 감소로 이익을 얻고 있습니다.

비행 크리티컬 부품의 지속적인 인증 병목

터빈 노즐 및 가압 밸브와 같은 비행 하드웨어는 엄격한 파괴 인성 및 피로 시험을 준수해야 합니다. 현재의 룰북은 서브트랙티브 가공용으로 작성된 것이므로, Additive 부품은 중복 쿠폰 시험을 받고, 스케줄이 최대 18개월 연장됩니다. 이 비용을 흡수할 수 있는 것은 대규모의 프라임 기업뿐이며, 중소의 티어 투 공급업체가 진입할 수 있는 3D 프린팅 시장은 한정되어 있습니다. ASTM과 ISO의 작업부회가 방법별 표준을 초안하고 있지만, 세계적인 정합에는 아직 수년의 노력이 필요합니다.

부문 분석

2024년, 하드웨어 부문은 세계 매출의 60.23%를 차지하고, 공업 규모의 금속 용융, 고온 폴리머, 자동 후처리에의 설비 투자가 그 원동력이 되었습니다. 그러나 2025년부터 2030년까지는 서비스가 CAGR 25.21%를 나타낼 전망입니다. Stratasys Direct Manufacturing(Stratasys Direct Manufacturing), Materialization(Materialize), Protralabs(Protolabs) 등의 계약 제조업체는 여러 사이트의 네트워크를 활용하여 부하를 분산하고 고객이 프로토타입을 작성하여 ISO-13485의 제조 부품을 10 일 이내에 받습니다. 서비스 붐은 경제적 장벽을 낮추고 3D 프린팅 시장의 사용자 기반을 확장합니다. 하지만 3MF가 STL을 추월함에 따라 격자 생성기와 비용 추정 엔진을 통합한 클라우드 네이티브 빌드 전개 도구에 기회가 있습니다.

3D 프린팅 시장은 OEM이 구독 기반 기계 임대와 원격 모니터링을 번들로 이익을 얻습니다. 신규 참가 기업은 복사기의 리스를 모방해, 유지관리, 캘리브레이션, 파우더 보충을 1개의 청구서에 정리한 시간당의 인쇄 매수 모델을 제공합니다. 이 하이브리드 접근 방식은 하드웨어와 서비스의 경계를 모호하게 만들고 거시 경제 사이클을 통해 수익 흐름을 원활하게합니다.

자동차, 에너지, 항공우주 분야가 프로토타입 투어링에서 연속생산으로 이행함에 따라 산업용 플랫폼이 2024년 지출의 72.14%를 차지했습니다. 멀티 레이저 분말 용융로는 인코넬에서 매시간 150cc의 성막에 도달하여 지금까지의 속도의 상한을 초과했습니다. 제조업체 각사는 토폴로지를 최적화한 브라켓을 활용하는 것으로, 중량을 40% 삭감해, 조립 공정을 통합. 빌드 챔버에 파우더 재활용과 실시간 용융 풀 분석이 통합되면 첫 번째 합격률이 CNC 밀링 가공에 가까워지므로 3D 프린팅 시장은 신뢰성을 높입니다.

데스크톱 시스템은 판매 규모가 작고 20,000mm/s2의 가속도를 실현하는 Bambu Lab의 고속 CoreXY 아키텍처에 상징되는 르네상스를 경험합니다. 대학에서는 1,000대 이하의 클러스터를 도입하여 가법 설계의 원리를 가르쳐 산업계에서 활약하는 인재의 파이프라인을 형성합니다. 치과의사와 보석점은 30μm의 XY 해상도를 달성하는 LCD 수지 프린터를 채용해, 3D 프린팅 시장을 엔지니어링 오피스 이외에도 넓히고 있습니다.

3D 프린팅 시장 보고서는 구성 요소별(하드웨어, 소프트웨어, 서비스), 프린터 유형별(산업용 3D 프린터, 데스크톱 3D 프린터), 기술별(광중합법(SLA, DLP), 기타), 재료별(폴리머, 금속·합금, 기타), 최종 사용자 산업별(자동차, 항공우주 및 방위, 기타), 지역별로 분류되어 있습니다.

지역 분석

북미는 세계 전체의 41.68%를 차지하며 포춘 500사의 채용 벤더와 분말 분무기 제조업체, 소프트웨어 벤더, 수탁 제조 제조업체가 밀집하고 있습니다. 미국 메이크업은 보조금을 분말 재활용 및 실시간 모니터링에 착수하기 위해 재료 데이터 시트의 갭을 메우고 있습니다. 미국 해군은 함선용 FDM 장치에서 저장소 수준의 DED 수리에 이르기까지 적층 조형에 중층적인 접근을 취하여 구조화된 수요 파이프라인을 구축하고 있습니다. GE 에어로스페이스가 새로운 적층조형시설에 10억 달러를 투입해 항공용 합금 공급 확보 강화 metal-am.com 전략 금속 수출규제가 강화되는 가운데, 육상에서의 분말생산이 북미의 3D 프린팅 시장을 더욱 차별화합니다.

아시아태평양은 CAGR 26.47%를 나타낼 것으로 예측되며 중국의 기기 보조금과 인도의 의료 도입의 영향을 받습니다. 2027년까지 디지털 R&D를 90% 보급한다는 베이징의 목표는 디자인 스위트와 시뮬레이션 소프트웨어에 대한 광범위한 수요를 지원하고 있습니다. 일본은 반도체 리소그래피에 사용되는 미세 해상도 세라믹 부품에 적층 조형을 활용하고 있습니다. 한국에서는 EV 모터용 구리의 금속 바인더 제트 가공을 완성하기 위해 산학 공동 실험실에 자금을 제공하고 국내 전동화 목표를 지원하고 있습니다. 동남아시아에서는 싱가포르의 고급 리마뉴 팩처링 & 테크놀로지 센터가 해양 및 석유 드릴링 장비의 유지 보수에 어필하는 하이브리드 가법 분해 셀의 인큐베이션을 실시했습니다.

유럽은 여전히 연구 및 생산 분야의 강국입니다. 에어버스, 사프란, MTU 에어로 엔진은 표준 개발 컨소시엄을 공동으로 주도하여 OEM간에 기하 공차가 일치하도록 하고 있습니다. 독일의 자동차 제조업체는 대시보드의 서포트 브라켓에 바인더 제트·스테인리스 부품을 채용해, 연간 2만대 이하의 생산량이면 프레스 가공보다 사이클 타임이 단축된다고 하고 있습니다. 스칸디나비아에서는 재활용 분말의 흐름을 통합하여 서큘러 이코노미(순환형 경제)의 인증을 얻고 있습니다. 동유럽의 수탁 제조 기업은 서양 OEM에서 오버플로우 주문을 받고 이 지역의 3D 프린팅 시장의 이질성을 높이고 있습니다.

중동은 에너지와 헬스케어 프로그램으로 성장을 가속. 사우디 알람코가 고염분 농도의 염수에 노출되는 해수 담수화 밸브용의 내식성 격자 인서트를 시험적으로 채용. UAE 병원은 대학과 제휴하여 복잡한 심장 수술을위한 해부학 모델을 인쇄합니다. 아프리카에서는 의지 장비와 예비 부품의 테스트 생산이 진행되고 있지만 인프라 격차는 여전히 남아 있습니다. 브라질의 SENAI 네트워크는 미래의 노동력을 준비하기 위해 디자인 포 애디티브 커리큘럼을 가르치고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 북미의 정부 자금에 의한 적층 조형 허브

- 유럽의 온 디맨드 항공우주 예비 부품용 금속 AM 채용의 급증

- 중국의 「중국 제조 2025」산업용 3DP 기기에의 보조금

- 인도에 있어서의 환자 고유의 정형외과 임플란트 수요 증가

- GCC에서의 경량 격자 열교환기의 AM에의 에너지 부문의 이행

- EV 플랫폼의 세계의 보급에 의해 급속한 툴 요구 증가

- 시장 성장 억제요인

- 비행에 불가결한 부품의 지속적인 인증 병목 현상

- 고성능 금속 분말의 가격 변동

- 식품 접촉 용도용의 인쇄 가능한 재료 팔레트가 한정

- AM 소프트웨어와 기존 PLM 스위트 사이의 상호 운용성의 갭

- 밸류체인/공급망 분석

- 규제 전망

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 시장에 대한 COVID-19의 영향

- 투자분석

제5장 시장 규모와 성장 예측

- 구성 요소별

- 하드웨어

- 소프트웨어

- 서비스

- 프린터 유형별

- 산업용 3D 프린터

- 데스크톱 3D 프린터

- 기술별

- 수조 광중합 방식(SLA, DLP)

- 분말 침적 방식(SLS, SLM, EBM)

- 재료 압출 방식(FDM, FFF)

- 재료 분사

- 바인더 분사

- 에너지 집중 적층

- 시트 적층

- 소재별

- 폴리머

- 금속 및 합금

- 세라믹

- 복합재료

- 기타 재료

- 용도별

- 프로토 타이핑

- 제조 및 생산 부품

- 공구 및 고정구

- 연구 개발

- 맞춤형 소비자 제품

- 최종 사용자 업계별

- 자동차

- 항공우주 및 방위

- 헬스케어 및 치과

- 가전

- 건설 및 건축

- 에너지(석유 및 가스, 전력)

- 식품 및 조리

- 교육 및 연구 기관

- 기타 산업

- 지역별

- 북미

- 미국

- 캐나다

- 라틴아메리카

- 멕시코

- 브라질

- 아르헨티나

- 기타 라틴아메리카

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 기타 아시아태평양

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Stratasys Ltd

- 3D Systems Corporation

- EOS GmbH

- General Electric Company(GE Additive)

- Hewlett Packard Inc.

- Desktop Metal Inc.

- Materialise NV

- SLM Solutions Group AG

- Velo3D Inc.

- Renishaw plc

- Ultimaker BV

- Formlabs Inc.

- Markforged Holding Corp.

- Nano Dimension Ltd.

- Prodways Group

- Tritone Technologies

- Carbon Inc.

- HP Inc.(Personalization division)

- UnionTech Inc.

- Sisma SpA

제7장 시장 기회와 향후 전망

KTH 25.11.04The 3D Printing Market size is estimated at USD 29.94 billion in 2025, and is expected to reach USD 66.42 billion by 2030, at a CAGR of 17.28% during the forecast period (2025-2030).

This growth arc is sustained by higher machine throughput, richer material portfolios, and the technology's gradual migration from rapid prototyping to low- and mid-volume end-use production. Aerospace, healthcare, and automotive firms now validate metal and polymer parts for flight hardware, implantable devices, and structural brackets, accelerating demand for certified powders and closed-loop monitoring. At the same time, service bureaus are scaling multi-laser systems to provide cloud-based capacity that de-risks capital investments for new adopters. Strategic government funding in the United States and China compresses qualification timelines and offsets equipment costs, while ASTM-led standardization is expected to harmonize testing protocols across regions. Consolidation, such as Nano Dimension's purchase of Desktop Metal, signals investor conviction that additive workflows will underpin next-generation supply chains.

Global 3D Printing Market Trends and Insights

Government-funded Additive Manufacturing Hubs in North America

Federal and state programs continue to accelerate domestic adoption. In January 2025, America Makes awarded USD 2.1 million to projects focused on in-situ metrology, sustainable powder recycling, and low-cost aluminum parameter sets. The initiative creates collaborative testbeds linking RTX Technology Research Center, Edison Welding Institute, and regional job-shops. Complementary funding under a USD 15 million ASTM Standardization Center of Excellence harmonizes data formats and test coupons, closing a persistent gap between research prototypes and qualified production. By codifying build-parameter envelopes, the ecosystem reduces redundant trials and shortens certification cycles for the 3D printing market, particularly in aerospace and medical device supply chains.

Surging Metal AM Adoption for On-demand Aerospace Spare Parts in Europe

European MRO providers increasingly rely on powder bed fusion to replace out-of-production parts without the overhead of warehousing. SpaceX's Raptor 3 chamber, produced through multi-laser laser-powder-bed fusion, illustrates the pathway from demonstrator to flight-ready part. Euro-control agencies have clarified guidelines for non-critical metallic interiors, making small-batch economics favorable even at volumes below 30 units. Lufthansa Technik, Safran, and Rolls-Royce now stock digital inventories that trigger print orders at the point of maintenance, cutting lead times from weeks to under 48 hours. As titanium and inconel powders reach aerospace-grade repeatability, the 3D printing market in Europe benefits from reduced carbon footprints tied to localized manufacturing.

Persistent Certification Bottlenecks for Flight-critical Parts

Flight hardware like turbine nozzles or pressurization valves must comply with rigorous fracture-toughness and fatigue tests. Current rulebooks were written for subtractive machining; hence, additive parts undergo redundant coupon testing that extends schedules by up to 18 months. Only large primes can absorb the cost, limiting the 3D printing market's reach within smaller tier-two suppliers. Though ASTM and ISO working groups are drafting method-specific standards, global alignment remains a multi-year endeavor.

Other drivers and restraints analyzed in the detailed report include:

- China's 'Made in China 2025' Subsidies for Industrial 3DP Equipment

- Growing Demand for Patient-specific Orthopedic Implants in India

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, the hardware segment drew 60.23% of global revenue, driven by capital outlays for industrial-scale metal fusion, high-temperature polymers, and automated post-processing. Yet, from 2025 to 2030, services outpace with a 25.21% CAGR. Contract manufacturers such as Stratasys Direct Manufacturing, Materialize, and Protolabs leverage multi-site networks to distribute load, allowing customers to prototype and receive production ISO-13485 parts within ten days. The services boom lowers financial barriers, expanding the user base of the 3D printing market. By contrast, software suppliers evolve more slowly, hampered by fragmented data formats; however, as 3MF overtakes STL, opportunity emerges for cloud-native build-prep tools that embed lattice generators and cost estimation engines.

The 3D printing market benefits when OEMs bundle subscription-based machine leasing with remote monitoring. New entrants mimic copier leasing, offering print-per-hour models that fold maintenance, calibration, and powder refills into a single invoice. This hybrid approach blurs the line between hardware and services, smoothing revenue streams across macroeconomic cycles.

Industrial platforms command 72.14% of 2024 spending as automotive, energy, and aerospace segments transition from prototype tooling to serial production. Multi-laser powder bed fusion now reaches 150 cc/hour deposition for Inconel, cracking a historical speed ceiling. Manufacturers exploit topology-optimized brackets that drop weight by 40% and consolidate assembly steps. The 3D printing market gains credibility because first-time pass rates approach those of CNC milling when build chambers incorporate powder recycling and real-time melt-pool analytics.

Desktop systems, while smaller in revenue, experience a renaissance marked by Bambu Lab's high-speed CoreXY architectures delivering 20,000 mm/s2 accelerations. Universities deploy clusters of sub-USD 1,000 units to teach design-for-additive principles, forming a talent pipeline for industrial roles. Dentists and jewelers adopt LCD resin printers that achieve 30 µm XY resolution, widening the 3D printing market beyond engineering offices.

The 3D Printing Market Report is Segmented by Component (Hardware, Software, and Services), Printer Type (Industrial 3D Printer and Desktop 3D Printer), Technology (Vat Photopolymerization [SLA, DLP], and More), Material Type (Polymers, Metals and Alloys, and More), End-User Industry (Automotive, Aerospace and Defense, and More), and Geography.

Geography Analysis

North America holds 41.68% of global spending, anchored by Fortune 500 adopters and a tight cluster of powder atomizers, software vendors, and contract manufacturers. America Makes funnels grant dollars toward powder recycling and real-time monitoring, closing material data sheet gaps. The U.S. Navy's layered approach to additive manufacturing, from shipboard FDM units to depot-level DED repair, creates a structured demand pipeline. GE Aerospace's USD 1 billion commitment to new additive facilities cements supply security for aviation alloys metal-am.com. As export controls tighten on strategic metals, onshore powder production further differentiates the North American 3D printing market.

Asia Pacific is forecast to expand at a 26.47% CAGR, influenced by China's equipment subsidies and India's medical adoption. Beijing's 90% digital R&D penetration target by 2027 underpins broad-based demand for design suites and simulation software. Japan leverages additive manufacturing for micro-resolution ceramic components used in semiconductor lithography. South Korea funds joint university-industry labs to perfect metal binder jetting of copper for EV motors, supporting domestic electrification goals. In Southeast Asia, Singapore's Advanced Remanufacturing and Technology Centre incubates hybrid additive-subtractive cells that appeal to marine and oil-rig maintenance.

Europe remains a powerhouse for both research and production. Airbus, Safran, and MTU Aero Engines co-lead standard-development consortia, ensuring geometric tolerances align across OEMs. German automakers deploy binder-jet stainless components into dashboard support brackets, citing faster cycle times than stamped alternatives at volumes under 20,000 units annually. Scandinavia seeks circular-economy credentials by integrating recycled powder streams. Eastern Europe's contract manufacturers attract overflow orders from Western OEMs, adding to the heterogeneity of the regional 3D printing market.

Middle East oxygenates growth through energy and healthcare programs. Saudi Aramco trials corrosion-resistant lattice inserts for desalination valves exposed to high-salinity brines. UAE hospitals partner with universities to print anatomical models for complex cardiac surgeries. Africa shows pilot activity in prosthetics and spare parts, though infrastructure gaps persist. Latin America cultivates in-house tooling for consumer appliance plants; Brazil's SENAI network teaches design-for-additive curricula, prepping a future workforce.

- Stratasys Ltd

- 3D Systems Corporation

- EOS GmbH

- General Electric Company (GE Additive)

- Hewlett Packard Inc.

- Desktop Metal Inc.

- Materialise NV

- SLM Solutions Group AG

- Velo3D Inc.

- Renishaw plc

- Ultimaker B.V.

- Formlabs Inc.

- Markforged Holding Corp.

- Nano Dimension Ltd.

- Prodways Group

- Tritone Technologies

- Carbon Inc.

- HP Inc. (Personalization division)

- UnionTech Inc.

- Sisma S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-funded additive manufacturing hubs in North America

- 4.2.2 Surging metal AM adoption for on-demand aerospace spare-parts in Europe

- 4.2.3 China's 'Made in China 2025' subsidies for industrial 3DP equipment

- 4.2.4 Growing demand for patient-specific orthopedic implants in India

- 4.2.5 Energy-sector shift to AM for lightweight lattice heat-exchangers in GCC

- 4.2.6 Rapid tooling needs driven by EV platform proliferation globally

- 4.3 Market Restraints

- 4.3.1 Persistent certification bottlenecks for flight-critical parts

- 4.3.2 Volatility in high-performance metal powder pricing

- 4.3.3 Limited printable material palette for food-contact applications

- 4.3.4 Inter-operability gaps between AM software and legacy PLM suites

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of COVID-19 on the Market

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Printer Type

- 5.2.1 Industrial 3D Printer

- 5.2.2 Desktop 3D Printer

- 5.3 By Technology

- 5.3.1 Vat Photopolymerization (SLA, DLP)

- 5.3.2 Powder Bed Fusion (SLS, SLM, EBM)

- 5.3.3 Material Extrusion (FDM, FFF)

- 5.3.4 Material Jetting

- 5.3.5 Binder Jetting

- 5.3.6 Directed Energy Deposition

- 5.3.7 Sheet Lamination

- 5.4 By Material

- 5.4.1 Polymers

- 5.4.2 Metals and Alloys

- 5.4.3 Ceramics

- 5.4.4 Composites

- 5.4.5 Other Materials

- 5.5 By Application

- 5.5.1 Prototyping

- 5.5.2 Manufacturing / Production Parts

- 5.5.3 Tooling and Fixtures

- 5.5.4 Research and Development

- 5.5.5 Personalized Consumer Products

- 5.6 By End-user Industry

- 5.6.1 Automotive

- 5.6.2 Aerospace and Defense

- 5.6.3 Healthcare and Dental

- 5.6.4 Consumer Electronics

- 5.6.5 Construction and Architecture

- 5.6.6 Energy (Oil and Gas, Power)

- 5.6.7 Food and Culinary

- 5.6.8 Education and Research Institutes

- 5.6.9 Other Industries

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.2 Latin America

- 5.7.2.1 Mexico

- 5.7.2.2 Brazil

- 5.7.2.3 Argentina

- 5.7.2.4 Rest of Latin America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Middle East and Africa

- 5.7.4.1 United Arab Emirates

- 5.7.4.2 Saudi Arabia

- 5.7.4.3 South Africa

- 5.7.4.4 Rest of Middle East and Africa

- 5.7.5 Asia-Pacific

- 5.7.5.1 China

- 5.7.5.2 Japan

- 5.7.5.3 South Korea

- 5.7.5.4 India

- 5.7.5.5 Rest of Asia-Pacific

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Stratasys Ltd

- 6.4.2 3D Systems Corporation

- 6.4.3 EOS GmbH

- 6.4.4 General Electric Company (GE Additive)

- 6.4.5 Hewlett Packard Inc.

- 6.4.6 Desktop Metal Inc.

- 6.4.7 Materialise NV

- 6.4.8 SLM Solutions Group AG

- 6.4.9 Velo3D Inc.

- 6.4.10 Renishaw plc

- 6.4.11 Ultimaker B.V.

- 6.4.12 Formlabs Inc.

- 6.4.13 Markforged Holding Corp.

- 6.4.14 Nano Dimension Ltd.

- 6.4.15 Prodways Group

- 6.4.16 Tritone Technologies

- 6.4.17 Carbon Inc.

- 6.4.18 HP Inc. (Personalization division)

- 6.4.19 UnionTech Inc.

- 6.4.20 Sisma S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment