|

시장보고서

상품코드

1850008

스마트 제조 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Smart Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

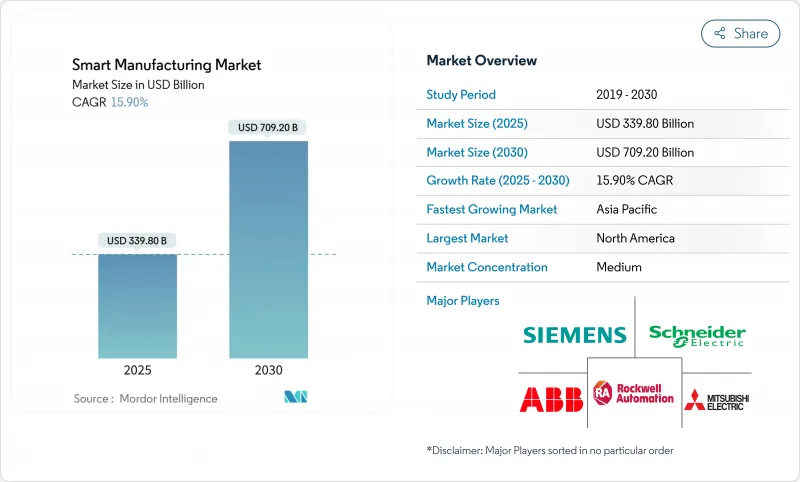

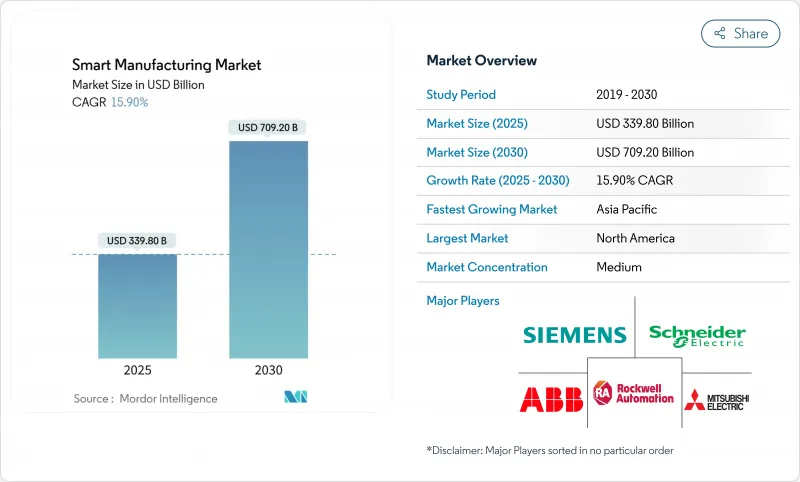

스마트 제조 시장 규모는 2025년에 3,398억 달러로 평가되었고, 2030년에 7,092억 달러로 상승하여 15.90%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다.

실시간 분석, 기계 연결성, AI 기반 공정 제어 기술이 융합되어 대규모 효율성 향상을 이끌어내는 한편, 정부는 탄력적인 국내 생산 역량 구축을 위한 인센티브를 집중하고 있습니다. 에너지 비용 상승과 탄소 가격 책정 제도는 공장 수준의 투명성 솔루션에 대한 관심을 높이고 있으며, 노동력 부족은 협동 로봇과 자율 물류 시스템에 대한 수요를 가속화하고 있습니다. 공급업체들은 신규 제품에 사설 5G 및 에지 분석 기술을 내장하여 안전이 중요한 공정에 마이크로초 단위의 응답 시간을 구현하고 있습니다. 경쟁 초점은 하드웨어 교체 주기에서 예측 인사이트과 에너지 최적화를 수익화하는 소프트웨어 구독 모델로 전환되고 있습니다.

세계의 스마트 제조 시장 동향 및 인사이트

효율성 향상을 위한 인더스트리 4.0/IIoT 도입 증가

공장이 센서, 분석, 클라우드 대시보드를 통합함에 따라 IIoT 도입은 현재 52%의 생산성 향상과 25%의 비용 절감을 실현하고 있습니다. 미국 제조업 확장 파트너십(MEP)은 2024년 36,000개 기업을 지원하여 스마트 제조 프로그램을 통해 162억 달러의 매출을 추가했습니다. 연결된 자산이 통합 데이터 레이크에 데이터를 공급함에 따라 운영자는 라인 정지를 제거하고 동적으로 생산 능력을 재조정할 수 있습니다. 항공우주와 같은 정밀도가 중요한 분야는 폐기물과 보증 클레임을 줄이기 위해 디지털 추적성을 도입하여 연결성 아키텍처의 지속적인 업그레이드를 촉진하고 있습니다.

디지털 공장에 대한 정부의 인센티브와 정책적 의무

연방 및 주 차원의 자금 지원 계획은 맞춤형 재정 지원과 규제 프레임워크를 통해 스마트 제조 도입을 가속화하고 있습니다. 주 제조 리더십 프로그램은 중소기업 제조업체를 위한 고성능 컴퓨팅 자원 및 기술 지원을 통해 제조 역량을 강화하기 위해 5천만 달러를 제공합니다. 독일의 인더스트리 4.0 계획은 중소기업에 기술 도입 지침을 제공하는 미텔슈탄트 4.0 우수 센터의 지원을 받아 2020년까지 연간 400억 유로의 투자를 예상하고 있습니다.

높은 자본 지출(CAPEX) 및 불확실한 중소기업 투자 수익률(ROI)

중소기업은 상당한 초기 자본 요구 사항과 불분명한 투자 수익률(ROI) 시기로 인해 스마트 제조 도입에 상당한 장벽에 직면합니다. 포괄적인 스마트 제조 시스템의 구현 비용은 수십만 달러에서 수백만 달러에 이를 수 있어, 제한된 자원을 가진 기업에 재정적 부담을 야기합니다. 상호 연결된 시스템의 ROI 계산 복잡성은 중소기업 의사 결정권자가 투자를 정당화하기 어렵게 만듭니다. 특히 혜택이 2-3년 후에야 실현될 수 있는 경우 더욱 그렇습니다.

부문 분석

2024년 제조 실행 시스템(MES)은 스마트 제조 시장의 22.4%를 차지하며 공장 운영의 디지털 백본으로서의 역할을 부각시켰습니다. 제조업체들이 글로벌 공장 전반에 걸쳐 실시간 가시성을 요구함에 따라 MES의 스마트 제조 시장 규모는 2032년까지 417억 8천만 달러에 달할 것으로 전망됩니다. 연평균 18.7% 성장률을 보이는 디지털 트윈 플랫폼은 엔지니어가 다양한 부하 조건에서 장비 동작을 시뮬레이션하여 시운전 시간을 30% 단축할 수 있게 합니다. PLC와 SCADA는 여전히 핵심 기반이지만, 공급업체들은 매개변수를 자율적으로 조정하는 AI 모듈을 내장하고 있습니다. 에지 분석 소프트웨어는 고속 포장 라인의 의사결정 루프를 단축하여 중앙 집중식 서버에서 현장 마이크로 데이터 센터로의 전환을 보여줍니다.

소프트웨어 정의 업그레이드는 지속적인 연간 반복 수익을 창출하여 기존 업체들이 라이선스 갱신과 분석 기능을 묶어 판매하도록 유도합니다. 인간-기계 인터페이스 도구는 증강 현실로 진화하여 현장 기술자에게 안내형 작업 흐름을 제공합니다. 제품 수명주기 관리 솔루션은 공급망 포털과 통합되어 설계자가 조기에 제조 가능성을 검증할 수 있게 합니다. 이러한 혁신들은 종합적으로 스마트 제조 시장을 지속적인 개선 투자의 주요 통로로 공고히 합니다.

소프트웨어는 2024년 매출의 49.6%를 차지하며 데이터 기반 워크플로로의 전환을 반영했습니다. 산업용 로봇은 17.5%의 연평균 성장률(CAGR)을 기록할 전망으로, 만성적인 노동력 부족과 유연한 배치 규모 요구에 대응합니다. 스마트 센서와 머신 비전 장치는 고해상도 영상을 AI 모델에 공급하여 수 밀리초 내에 결함을 식별합니다. 제어 장치에는 이제 온디바이스 추론 엔진이 내장되어 클라우드 지연 없이 자율적 조정이 가능합니다. 공장들이 통합, 교육, 관리형 사이버보안을 아웃소싱함에 따라 서비스 매출이 확대되고 있습니다.

프라이빗 5G 네트워크는 단일 층에서 수만 개의 엔드포인트를 결정론적 지연 시간으로 지원하며 통신 부문을 재편하고 있습니다. 공급업체들은 통신 사업자와 스펙트럼 전략을 공동 개발하여 연결성을 전략적 경쟁 우위로 전환하고 있습니다. 그 결과, 스마트 제조 시장은 OT 하드웨어와 IT 소프트웨어 간의 경계를 계속 모호하게 만들며 디지털 가치 창출을 위한 통합 플랫폼을 구축하고 있습니다.

지역 분석

북미는 2024년 매출의 42.3%를 차지했으며, 이는 미국 에너지부의 3,300만 달러 규모 보조금 프로그램과 제조업 확장 파트너십(MEP)의 전국적 지원 활동에 힘입은 결과입니다. 벤처 캐피털 유입은 기술 확산을 가속화하고 있으며, 사모펀드는 MES(제조 실행 시스템), 로봇 통합, 사이버 보안 서비스를 묶은 플랫폼 통합을 추진하고 있습니다. 지역 공급업체들은 원격 용접과 같은 지연 시간에 민감한 사용 사례를 검증하기 위해 사설 5G 테스트베드를 채택하고 있습니다.

아시아태평양 지역은 “메이드 인 차이나 2025” 기치 아래 중국의 33개 혁신 센터와 1만 명당 1,012대의 세계 최고 수준의 로봇 보유 밀도를 자랑하는 한국의 추진으로 15.9%의 CAGR을 기록하며 가장 빠르게 성장하는 지역입니다. 3자 파트너가 지원하는 인도의 디지털 인프라 성장 이니셔티브는 스마트 제조 스타트업의 진입 장벽을 낮추고, 인도를 현지화된 MES 개발의 떠오르는 허브로 자리매김하고 있습니다.

유럽은 독일의 인더스트리 4.0을 기반으로 꾸준한 도입을 이어가고 있으며, 연간 400억 유로(440억 달러) 투자 전망과 미텔슈탄트 4.0 역량 센터가 이를 뒷받침합니다. 탄소 국경 조정 메커니즘은 에너지 집약도 대시보드 수요를 증폭시켜 유럽 공급업체들이 탄소 회계 모듈 분야에서 선점 우위를 점하게 합니다. 이러한 역학은 종합적으로 스마트 제조 시장 내 지역별 전문화를 강화하며 공급업체의 시장 진출 전략을 형성합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 효율성 향상을 위한 인더스트리 4.0/IIoT 도입 증가

- 디지털 팩토리를 위한 정부 인센티브 및 정책 의무화

- 숙련된 노동력 부족으로 가속화되는 자동화 도입

- 탄소국경조정제도(CBAM)로 촉진되는 공장 수준의 에너지 투명성

- 디지털 트윈 기반 예측 유지보수 서비스 수익

- 초저지연 제어를 가능하게 하는 사설 5G 네트워크 구축

- 시장 성장 억제요인

- 높은 자본 지출(CAPEX) 및 중소기업(SME)의 불확실한 투자 수익률(ROI)

- 사이버 보안/데이터 주권에 대한 우려

- 상호 운용성을 제한하는 기존 아날로그 장비

- 제어 하드웨어 지연을 초래하는 반도체 공급망 변동성

- 가치/공급망 분석

- 규제 상황

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 투자분석

제5장 시장 규모와 성장 예측

- 기술별

- 프로그래머블 로직 컨트롤러(PLC)

- 모니터링 제어 및 데이터 수집(SCADA)

- 전사적 자원 계획(ERP)

- 분산 제어 시스템(DCS)

- 휴먼 머신 인터페이스(HMI)

- 제품 수명주기 관리(PLM)

- 제조 실행 시스템(MES)

- 디지털 트윈 플랫폼

- 엣지 분석 소프트웨어

- 기타 기술

- 컴포넌트별

- 하드웨어

- 로봇 공학

- 센서

- 머신 비전 시스템

- 제어 디바이스

- 소프트웨어

- MES

- PLM

- SCADA/ERP 스위트

- 디지털 트윈/AI 및 분석

- 서비스

- 통합 및 구현

- 컨설팅 및 교육

- 관리형 서비스

- 통신 부문

- 하드웨어

- 전개 모드별

- 온프레미스

- 클라우드

- 하이브리드

- 최종 사용자 업계별

- 자동차

- 반도체 및 전자

- 석유 및 가스

- 화학 및 석유화학

- 의약품 및 생명과학

- 항공우주 및 방위

- 식품 및 음료

- 금속 및 광업

- 에너지 및 유틸리티

- 물류와 창고

- 기타 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- ASEAN-5

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- ABB Ltd.

- Emerson Electric Co.

- FANUC Corporation

- General Electric Co.

- Honeywell International Inc.

- Mitsubishi Electric Corp.

- Robert Bosch GmbH

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Texas Instruments Inc.

- Yokogawa Electric Corp.

- Cisco Systems Inc.

- IBM Corp.

- Oracle Corp.

- SAP SE

- Johnson Controls Intl. plc

- PTC Inc.

- Dassault Systems SE

- 3D Systems Corp.

- Stratasys Ltd.

- Delta Electronics Inc.

- Capgemini SE

제7장 시장 기회와 장래의 전망

HBR 25.11.14The smart manufacturing market size is valued at USD 339.80 billion in 2025 and is projected to climb to USD 709.20 billion by 2030, registering a 15.90% CAGR.

Real-time analytics, machine connectivity, and AI-powered process control are converging to unlock large efficiency gains, while governments channel incentives toward resilient domestic production capacity. Rising energy costs and carbon-pricing schemes heighten interest in factory-level transparency solutions, and labor shortages intensify demand for collaborative robots and autonomous material-handling systems. Vendors are embedding private 5G and edge analytics in new offerings, enabling micro-second response times for safety-critical processes. Competitive focus is shifting from hardware refresh cycles to software subscription models that monetize predictive insights and energy optimization.

Global Smart Manufacturing Market Trends and Insights

Rising adoption of Industry 4.0 / IIoT for efficiency

IIoT deployments now deliver 52% productivity gains and 25% cost reductions as factories integrate sensors, analytics, and cloud dashboards. The U.S. Manufacturing Extension Partnership supported 36,000 firms in 2024, adding USD 16.2 billion in sales through smart manufacturing programs.As connected assets feed unified data lakes, operators can eliminate line stoppages and dynamically rebalance capacity. Precision-critical sectors such as aerospace embrace digital traceability to reduce scrap and warranty claims, fueling sustained upgrades in connectivity architectures.

Government incentives & policy mandates for digital factories

Federal and state-level funding initiatives are accelerating smart manufacturing adoption through targeted financial support and regulatory frameworks. The State Manufacturing Leadership Program offers USD 50 million to enhance manufacturing capacity through high-performance computing resources and technical assistance for small and medium manufacturers.Germany's Industrie 4.0 initiative projects EUR 40 billion annual investment by 2020, supported by Mittelstand 4.0 centers of excellence that provide SMEs with technology adoption guidance.

High CAPEX & uncertain SME ROI

Small and medium enterprises face significant barriers to smart manufacturing adoption due to substantial upfront capital requirements and unclear return on investment timelines. Implementation costs for comprehensive smart manufacturing systems can range from hundreds of thousands to millions of dollars, creating financial strain for companies with limited resources. The complexity of calculating ROI for interconnected systems makes it difficult for SME decision-makers to justify investments, particularly when benefits may not materialize for 2-3 years.

Other drivers and restraints analyzed in the detailed report include:

- Skilled-labour shortages accelerating automation uptake

- Carbon-Border Adjustment Mechanism spurring factory-level energy transparency

- Cyber-security / data-sovereignty concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manufacturing Execution Systems held 22.4% of the smart manufacturing market in 2024, underscoring their role as the digital backbone of plant operations. The smart manufacturing market size for MES is projected to reach USD 41.78 billion by 2032 as manufacturers mandate real-time visibility across global plants. Digital-twin platforms, expanding at an 18.7% CAGR, let engineers simulate equipment behavior under varying loads, trimming commissioning times by 30% . PLCs and SCADA remain foundational, yet vendors embed AI modules that autonomously tune parameters. Edge-analytics software shortens decision loops for high-speed packaging lines, illustrating the shift from centralized servers to shop-floor micro-data centers.

Software-defined upgrades create sticky annual recurring revenue, prompting incumbents to bundle analytics with license renewals. Human-machine interface tools migrate toward augmented reality, giving line technicians guided workflows. Product lifecycle management solutions integrate with supply-chain portals so designers validate manufacturability early. Collectively, these innovations reinforce the smart manufacturing market as the primary conduit for continuous improvement investments.

Software commanded 49.6% of 2024 revenue, reflecting the pivot toward data-driven workflows. Industrial robotics, projected to post a 17.5% CAGR, responds to chronic labor gaps and the need for flexible batch sizes.Smart sensors and machine-vision units feed high-resolution imagery to AI models that flag defects within milliseconds. Control devices now incorporate on-device inference engines, enabling autonomous adjustments without cloud latency. Service revenues expand as factories outsource integration, training, and managed cybersecurity.

Private 5G networks reshape the communication segment by supporting tens of thousands of end-points on a single floor with deterministic latency. Vendors co-develop spectrum strategies with telecom operators, turning connectivity into a strategic moat. As a result, the smart manufacturing market continues to blur lines between OT hardware and IT software, creating a unified platform for digital value creation.

The Smart Manufacturing Market is Segmented by Technology (Programmable Logic Controller (PLC), Supervisory Controller and Data Acquisition (SCADA), and More), Component (Hardware and More), Deployment Mode (On-Premise, Cloud and More), End-User Industry (Automotive, Semiconductors, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 42.3% of 2024 revenue, underpinned by the U.S. Department of Energy's USD 33 million grant program and the Manufacturing Extension Partnership's nationwide outreach . Venture capital flows accelerate technology diffusion, and private equity funds pursue platform roll-ups that bundle MES, robotics integration, and cybersecurity services. Regional suppliers adopt private 5G testbeds to validate latency-sensitive use cases such as remote welding.

Asia Pacific is the fastest-growing region with a 15.9% CAGR, propelled by China's 33 Innovation Centers under the "Made in China 2025" banner and South Korea's world-leading robot density of 1,012 units per 10,000 employees. India's Digital Infrastructure Growth Initiative, backed by trilateral partners, lowers entry barriers for smart manufacturing startups, positioning the country as a rising hub for localized MES development.

Europe delivers steady adoption rooted in Germany's Industrie 4.0, backed by EUR 40 billion (USD 44 billion) annual investment projections and Mittelstand 4.0 competence centers. The Carbon Border Adjustment Mechanism amplifies demand for energy-intensity dashboards, giving European vendors first-mover advantage in carbon accounting modules. Collectively, these dynamics reinforce regional specialization within the smart manufacturing market, shaping vendor go-to-market playbooks.

- ABB Ltd.

- Emerson Electric Co.

- FANUC Corporation

- General Electric Co.

- Honeywell International Inc.

- Mitsubishi Electric Corp.

- Robert Bosch GmbH

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Texas Instruments Inc.

- Yokogawa Electric Corp.

- Cisco Systems Inc.

- IBM Corp.

- Oracle Corp.

- SAP SE

- Johnson Controls Intl. plc

- PTC Inc.

- Dassault Systems SE

- 3D Systems Corp.

- Stratasys Ltd.

- Delta Electronics Inc.

- Capgemini SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption of Industry 4.0 / IIoT for efficiency

- 4.2.2 Government incentives and policy mandates for digital factories

- 4.2.3 Skilled-labour shortages accelerating automation uptake

- 4.2.4 Carbon-Border Adjustment Mechanism (CBAM) spurring factory-level energy transparency

- 4.2.5 Digital-twin-based predictive-maintenance service revenues

- 4.2.6 Roll-out of private 5G networks enabling ultra-low-latency control

- 4.3 Market Restraints

- 4.3.1 High CAPEX and uncertain SME ROI

- 4.3.2 Cyber-security / data-sovereignty concerns

- 4.3.3 Legacy analogue equipment limiting interoperability

- 4.3.4 Semiconductor supply-chain volatility delaying control hardware

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porters Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Programmable Logic Controller (PLC)

- 5.1.2 Supervisory Control and Data Acquisition (SCADA)

- 5.1.3 Enterprise Resource Planning (ERP)

- 5.1.4 Distributed Control System (DCS)

- 5.1.5 HumanMachine Interface (HMI)

- 5.1.6 Product Lifecycle Management (PLM)

- 5.1.7 Manufacturing Execution System (MES)

- 5.1.8 Digital-Twin Platforms

- 5.1.9 Edge-Analytics Software

- 5.1.10 Other Technologies

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.1.1 Robotics

- 5.2.1.2 Sensors

- 5.2.1.3 Machine-Vision Systems

- 5.2.1.4 Control Devices

- 5.2.2 Software

- 5.2.2.1 MES

- 5.2.2.2 PLM

- 5.2.2.3 SCADA / ERP Suites

- 5.2.2.4 Digital-Twin / AI and Analytics

- 5.2.3 Services

- 5.2.3.1 Integration and Implementation

- 5.2.3.2 Consulting and Training

- 5.2.3.3 Managed Services

- 5.2.4 Communication Segment

- 5.2.1 Hardware

- 5.3 By Deployment Mode

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.3.3 Hybrid

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Semiconductors and Electronics

- 5.4.3 Oil and Gas

- 5.4.4 Chemical and Petrochemical

- 5.4.5 Pharmaceuticals and Life Sciences

- 5.4.6 Aerospace and Defense

- 5.4.7 Food and Beverage

- 5.4.8 Metals and Mining

- 5.4.9 Energy and Utilities

- 5.4.10 Logistics and Warehousing

- 5.4.11 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Netherlands

- 5.5.3.7 Russia

- 5.5.3.8 Rest of Europe

- 5.5.4 APAC

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 ASEAN-5

- 5.5.4.7 Rest of APAC

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.2 Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Emerson Electric Co.

- 6.4.3 FANUC Corporation

- 6.4.4 General Electric Co.

- 6.4.5 Honeywell International Inc.

- 6.4.6 Mitsubishi Electric Corp.

- 6.4.7 Robert Bosch GmbH

- 6.4.8 Rockwell Automation Inc.

- 6.4.9 Schneider Electric SE

- 6.4.10 Siemens AG

- 6.4.11 Texas Instruments Inc.

- 6.4.12 Yokogawa Electric Corp.

- 6.4.13 Cisco Systems Inc.

- 6.4.14 IBM Corp.

- 6.4.15 Oracle Corp.

- 6.4.16 SAP SE

- 6.4.17 Johnson Controls Intl. plc

- 6.4.18 PTC Inc.

- 6.4.19 Dassault Systems SE

- 6.4.20 3D Systems Corp.

- 6.4.21 Stratasys Ltd.

- 6.4.22 Delta Electronics Inc.

- 6.4.23 Capgemini SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment