|

시장보고서

상품코드

1850091

치과용 소모품 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Dental Consumables - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

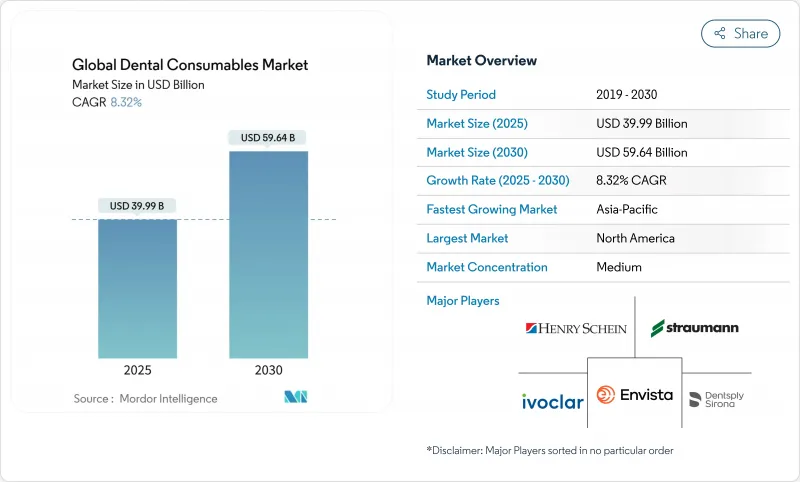

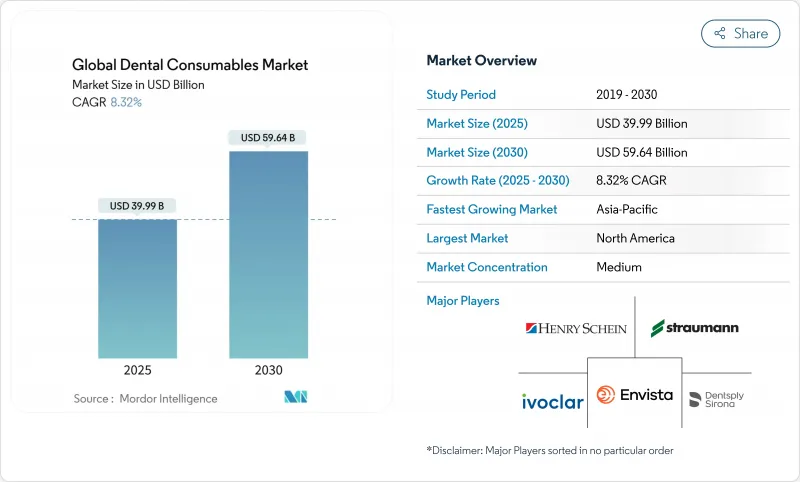

치과용 소모품 시장 규모는 2025년에 399억 9,000만 달러, 2030년에는 596억 4,000만 달러에 이르고, 예측 기간 동안 CAGR은 8.32%를 나타낼 전망입니다.

디지털 의자 사이드 워크플로우, 생물활성 임플란트 재료, 프리미엄 제품 라인으로의 수량 시프트를 도모하는 일괄 조달 모델 등이 꾸준한 성장을 가져오고 있습니다. DSO는 급속히 규모를 확대하고 조달 기준에 영향을 미치고 있지만, 아시아태평양이 가장 빠른 성장을 보이는 가운데 북미는 수익 리더로 계속되고 있습니다. 당일 수리, 예방 실란트 및 재생 재료에 대한 수요는 환자 1인당 지출을 증가시키고 통합 디지털 생태계를 갖춘 공급업체에게 유리합니다.

세계 치과용 소모품 시장 동향과 통찰

당일 사용 가능한 CAD/CAM 보철물에 대한 수요 증가

미국의 치과 진료소의 절반 이상이 이미 구강 내 스캐너를 도입하고 있으며, 치료 사이클의 단축과 프리미엄 수복 재료의 적응 확대가 진행되고 있습니다. 의자 사이드 밀링과 클라우드 설계 서비스의 조합은 실험실 오버헤드를 줄이고 수익성을 향상시킵니다. AI 지원 설계 모듈은 복잡한 마진 및 접촉 조정을 자동화하여 의자 시간을 더욱 단축합니다. 2024년에는 도입이 18% 가속되고, 2025년에는 스캐너 통합으로 이미지 정밀도가 향상되므로 재료 처리량도 연동하여 상승할 것으로 예측됩니다. 스캐너, 밀, 유효한 재료 블록을 번들할 수 있는 공급업체는 DSO와 장기 계약을 맺고 있습니다.

노인 인구 증가로 보철 치료 증가

65세 이상의 성인은 가장 빠르게 증가하는 환자 집단입니다. 일본에서는 이미 임플란트 지지형 오버덴처에 특화된 상환 경로가 할당되어 있으며 EU의 실버 이코노미 프로그램에서는 노인 치과 의료에 자금이 할당되어 있습니다. 디지털 의치 워크플로우는 예약 부담을 줄이고 이동에 제약이 있는 노인의 수용 태세를 개선하고 있습니다. 재료 공급업체는 구강 건조가 일어나기 쉬운 환자에 맞는 경량 폴리머베이스와 고충격 아크릴을 상용화하고 있습니다.

심미치과의 보험상환은 한정되어 있다.

심미 베니어, 표백, 잇몸 윤곽 형성은 여전히 자비 진료가 주류입니다. 메디케어는 2025년에 특정 의료 관련 치과 치료에 대한 보험 적용을 확대하지만, 선택적 심미 치과 치료에 대한 보험 적용은 제한된 채로 남아 있습니다. 이 때문에 시장은 이분화되어 고급품 부문은 유지되는 것, 총 개수는 제한됩니다. 제조업체 각사는 가격과 연마의 균형을 고려한 단계적인 컴포지트 라인을 제공함으로써 대항하고 있습니다.

부문 분석

2024년 치과용 소모품 시장 점유율은 치과 임플란트가 18.35%를 차지합니다. 성공률이 높은 생체 활성 코팅과 디지털 수술 계획이 더 부드러운 뼈에 대한 적응을 확대. 개인 보호복의 치과용 소모품 시장 규모는 아시아태평양의 노인 인구에 의해 지원되며 2030년까지 연평균 복합 성장률(CAGR) 10.11%를 보일 것으로 예측됩니다. 이 부문의 급성장은 ASTM 인증 인공 호흡기 및 오토 클레이브 가능한 아이 실드가 필요한 감염 관리 프로토콜에 의해 더욱 촉진됩니다.

보철 하위 부문에서는 지르코니아나 리튬디실리케이트의 크라운을 1시간 이내에 제작하는 CAD/CAM 워크플로우가 이익을 가져옵니다. 유니버설 본딩제는 여러 에칭 전략을 다루어 재고를 간소화합니다. 인산 칼슘 과립과 같은 재생 재료는 릿지 오그멘테이션 처리와 연동하여 성장합니다. 한편, 봉합사와 바도 성숙하고 있지만, 오퍼레이터의 피로를 경감하는 인체공학에 근거한 핸들의 재설계에 의해 약간이익을 누리고 있습니다.

2024년 치과용 소모품 시장에서는 보철 처리가 27.80%의 점유율을 차지했습니다. 클라우드 플래닝 소프트웨어와 인하우스의 3D 프린팅 얼라이너가 사이클 타임을 단축하고 사례 시작을 뒷받침하고 있습니다.

수복 치과에서는 불소와 칼슘 이온을 방출하고 수복물의 수명을 늘리는 생체 활성 복합체를 사용하여 낮은 침습 전처리가 채택되었습니다. 치내 요법학은 치료 시간을 단축하는 바이오 세라믹 실러와 레시 프로모션 파일이 혁신적입니다. 치주 병학은 재생 멤브레인과 에나멜 매트릭스 파생 상품을 통합하여 새로운 접착을 촉진합니다. 미용 치료는 자비 진료이지만 소셜 미디어에 노출이나 원격 상담의 편의성 향상으로 기세를 늘리고 있습니다.

지역 분석

북미는 2024년 세계 매출의 43.39%를 차지했습니다. 임플란트 치료와 클리어 얼라이너 사례는 가격이 비싸지만 보험사는 예방 급여를 확대하여 실란트와 불소 바니시의 취급량을 증가 시켰습니다. FDA 510(k)에 따른 규제의 명확화로 제품 출시가 가속화됩니다. 그러나 치과 의사의 노동 인구 증가로 인한 경쟁 격화로 인해 상품 분야의 가격 민감도가 높아질 수 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)은 9.54%를 보일 것으로 예측되며, 도시 중간층 확대와 인바운드 치과 관광이 이를 뒷받침합니다. 인도와 태국 정부는 농촌 클리닉을 정비하기 위한 관민 파트너십을 지지합니다. 현지 제조업체는 비용 경쟁력 있는 스캐너 및 임플란트 시스템을 제공함으로써 자본을 증진하는 반면, 재료 검증을 위해 세계 선도사와 제휴하여 공급망을 단축하고 수입 관세에 대응합니다.

견고한 상환 제도와 엄격한 제품 품질 기준에 힘입어 유럽의 CAGR은 8.38%를 유지하고 있습니다. 독일 정밀 공학의 기반은 고강도 세라믹 생산을 키우고 영국은 NHS 근대화 기금을 통해 디지털 치과 도입을 가속화하고 있습니다. 중동, 아프리카와 남미의 CAGR은 각각 7.65%와 7.81%를 나타내고 민간보험의 보급과 공적 구강위생 캠페인에 의해 액세스가 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 당일 CAD/CAM 의지 수요 증가

- 고령자 인구 증가에 의해 보철 치료가 증가

- 치과 서비스 조직(DSO)의 성장이 대량 조달을 촉진

- 클리어 얼라이너 교정의 급속한 도입

- 생체활성 및 재생 임플란트 재료로의 전환

- 예방 구강 케어 캠페인이 실란트의 소비를 촉진

- 시장 성장 억제요인

- 미용 치과에 대한 제한된 보험 환급

- 의자 사이드 CAD/CAM 워크플로우에서의 스킬 갭

- 휘발성 수지와 귀금속의 가격

- 신규 바이오세라믹의 승인에 관한 규제의 지연

- 공급망 분석

- 규제 전망

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 라이벌 관계의 격렬

제5장 시장 규모와 성장 예측

- 제품 유형별

- 얼라이너와 브레이스

- 마취약

- 접착제

- 치과용 바

- 치과 임플란트

- 치과용 스프린트

- 치과 봉합사

- 지혈제

- 개인 보호구

- 보철물

- 재생재료

- 수리 재료

- 기타 제품 유형

- 치료법별

- 복원

- 보철

- 근관치료

- 치주술

- 교정

- 미용/심미

- 기타

- 유통 채널별

- 오프라인

- B2B

- B2C

- 온라인

- 오프라인

- 최종 사용자별

- 치과 진료소

- 치과 병원

- DSO/그룹 프랙티스

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Coltene Holding AG

- Dentsply Sirona

- Envista Holdings

- GC Corporation

- Henry Schein Inc.

- Hu-Friedy Mfg Co. LLC

- Ivoclar Vivadent AG

- Jeil Medical Corporation

- Kuraray Noritake Dental

- Nakanishi Inc.

- Osstem Implant Co. Ltd

- Patterson Companies Inc.

- Septodont Holding

- Shofu Inc.

- Solventum Corporation

- Straumann Group

- Thommen Medical AG

- Ultradent Products Inc.

- Young Innovations Inc.

- Ziacom Medical

- ZimVie Inc.

제7장 시장 기회와 장래의 전망

SHW 25.11.17The dental consumables market size reached USD 39.99 billion in 2025 and is forecast to reach USD 59.64 billion by 2030, expanding at an 8.32% CAGR during the forecast period.

Steady gains stem from digital chairside workflows, bioactive implant materials, and bulk-procurement models that shift volumes toward premium product lines. DSOs are scaling rapidly, influencing procurement standards, while North America remains the revenue leader even as Asia-Pacific posts the fastest regional advance. Demand for same-day restorations, preventive sealants, and regenerative materials collectively elevate per-patient spending and favors suppliers with integrated digital ecosystems.

Global Dental Consumables Market Trends and Insights

Rising demand for same-day CAD/CAM prosthetics

More than half of U.S. dental practices already employ intraoral scanners, shortening treatment cycles and expanding indications for premium restorative materials. Chairside milling paired with cloud design services lowers laboratory overhead and lifts profitability. AI-enabled design modules automate complex margin and contact adjustments, further reducing chairtime. Adoption accelerated by 18% in 2024, and with scanner integration set to improve imaging precision in 2025, material throughput is expected to rise in tandem. Suppliers capable of bundling scanners, mills, and validated material blocks are securing long-term contracts with DSOs.

Elderly population expansion increasing prosthodontic procedures

Adults aged 65 plus represent the fastest-growing patient cohort. Japan already allocates specialized reimbursement pathways for implant-supported overdentures, and the EU's Silver Economy program earmarks funds for geriatric dental care. Digital denture workflows reduce appointment burden, improving acceptance among seniors with mobility constraints. Material suppliers are commercializing lightweight polymer bases and high-impact acrylics tailored to xerostomia-prone patients.

Limited insurance reimbursement for cosmetic dentistry

Aesthetic veneers, bleaching, and gingival contouring remain predominantly self-pay. While Medicare will extend coverage to certain medically-linked dental procedures in 2025, elective cosmetic benefits remain constrained. This bifurcates the market, sustaining luxury segments yet limiting total unit volumes. Manufacturers counteract by offering tiered composite lines that balance price and polish retention.

Other drivers and restraints analyzed in the detailed report include:

- Growth of dental service organizations (DSOs) driving bulk procurement

- Shift toward bioactive and regenerative implant materials

- Skills gap in chair-side CAD/CAM workflows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dental implants accounted for 18.35% of the dental consumables market share in 2024. High-success bioactive coatings and digital surgical planning expand indications into softer bone situations. The dental consumables market size for personal protective wear is forecast to climb at 10.11% CAGR to 2030, notably buoyed by Asia Pacific's geriatric cohorts. The segment's sharp trajectory is further propelled by infection-control protocols that demand ASTM-certified respirators and autoclavable eye shields.

The prosthetics sub-segment benefits from CAD/CAM workflows that fabricate zirconia and lithium-disilicate crowns in under one hour. Universal bonding agents streamline inventory by covering multiple etching strategies. Regenerative materials such as calcium-phosphate granules grow in tandem with ridge-augmentation procedures. Meanwhile, sutures and burs, although mature, enjoy marginal gains from ergonomic handle redesigns that reduce operator fatigue.

Prosthodontic procedures accounted for 27.80% share of the dental consumables market in 2024 as full-arch rehabilitation moves chairside through guided surgery and immediate loading. Orthodontics, driven by clear aligners, records the highest modality growth of 9.78%; cloud-planning software and in-house 3-D printed aligners reduce cycle time and boost case starts.

Restorative dentistry embraces minimally invasive preps using bioactive composites that release fluoride and calcium ions, prolonging restoration life. Endodontics innovates with bioceramic sealers and reciprocation-motion files that cut procedure time. Periodontics integrates regenerative membranes and enamel-matrix derivatives that encourage new attachment. Cosmetic procedures, although self-funded, gain momentum via social media exposure and rising tele-consultation convenience.

The Dental Consumables Market Report is Segmented by Product Type (Aligners & Braces, Anesthetics, and More), Treatment Modality (Restorative, Prosthodontic, and More), Distribution Channel (Offline [B2B and B2C] and Online), End-User (Dental Clinics, Dental Hospitals and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 43.39% of global revenue in 2024. Implant therapy and clear-aligner cases command premium pricing, while insurers expand preventive benefits that lift sealant and fluoride varnish volumes. Regulatory clarity under FDA 510(k) accelerates product launches; however competition among a growing dentist workforce may intensify price sensitivity in commodity segments.

Asia Pacific is projected to grow at 9.54% CAGR through 2030, buoyed by urban middle-class expansion and inbound dental tourism. Governments in India and Thailand endorse public-private partnerships to equip rural clinics. Local manufacturers capitalize by offering cost-competitive scanners and implant systems while partnering with global majors for material validation, shortening supply chains and countering import tariffs.

Europe maintains steady 8.38% CAGR supported by robust reimbursement frameworks and rigorous product-quality standards. Germany's precision-engineering base nurtures high-strength ceramic production, while the United Kingdom accelerates digital dentistry adoption via NHS modernization funds. The Middle East & Africa and South America post 7.65% and 7.81% CAGRs respectively as private insurance penetration and public oral-health campaigns broaden access.

- Coltene Holding

- Dentsply Sirona

- Envista Holdings

- GC Corporation

- Henry Schein

- Hu-Friedy Mfg Co. LLC

- Ivoclar Vivadent

- Jeil Medical

- Kuraray Noritake Dental

- Nakanishi

- Osstem Implant

- Patterson Companies

- Septodont

- Shofu Inc.

- Solventum Corporation

- Straumann Group

- Thommen Medical

- Ultradent Products

- Young Innovations

- Ziacom Medical

- ZimVie

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for same-day CAD/CAM prosthetics

- 4.2.2 Elderly population expansion increasing prosthodontic procedures

- 4.2.3 Growth of dental service organisations (DSOs) driving bulk procurement

- 4.2.4 Rapid adoption of clear-aligner orthodontics

- 4.2.5 Shift toward bio-active and regenerative implant materials

- 4.2.6 Preventive-oral care campaigns boosting sealant consumption

- 4.3 Market Restraints

- 4.3.1 Limited insurance reimbursement for cosmetic dentistry

- 4.3.2 Skills gap in chair-side CAD/CAM workflows

- 4.3.3 Volatile resin and precious-metal prices

- 4.3.4 Regulatory delays for novel bio-ceramic approvals

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Aligners & Braces

- 5.1.2 Anesthetics

- 5.1.3 Bonding Agents & Adhesives

- 5.1.4 Dental Burs

- 5.1.5 Dental Implants

- 5.1.6 Dental Splints

- 5.1.7 Dental Sutures

- 5.1.8 Hemostats

- 5.1.9 Personal Protective Wear

- 5.1.10 Prosthetics

- 5.1.11 Regenerative Materials

- 5.1.12 Restorative Materials

- 5.1.13 Other Product Types

- 5.2 By Treatment Modality

- 5.2.1 Restorative

- 5.2.2 Prosthodontic

- 5.2.3 Endodontic

- 5.2.4 Periodontic

- 5.2.5 Orthodontic

- 5.2.6 Cosmetic / Aesthetic

- 5.2.7 Others

- 5.3 By Distribution Channel

- 5.3.1 Offline

- 5.3.1.1 B2B

- 5.3.1.2 B2C

- 5.3.2 Online

- 5.3.1 Offline

- 5.4 By End-User

- 5.4.1 Dental Clinics

- 5.4.2 Dental Hospitals

- 5.4.3 DSO / Group Practices

- 5.4.4 Other End-Users

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Product Portfolio Analysis

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Coltene Holding AG

- 6.4.2 Dentsply Sirona

- 6.4.3 Envista Holdings

- 6.4.4 GC Corporation

- 6.4.5 Henry Schein Inc.

- 6.4.6 Hu-Friedy Mfg Co. LLC

- 6.4.7 Ivoclar Vivadent AG

- 6.4.8 Jeil Medical Corporation

- 6.4.9 Kuraray Noritake Dental

- 6.4.10 Nakanishi Inc.

- 6.4.11 Osstem Implant Co. Ltd

- 6.4.12 Patterson Companies Inc.

- 6.4.13 Septodont Holding

- 6.4.14 Shofu Inc.

- 6.4.15 Solventum Corporation

- 6.4.16 Straumann Group

- 6.4.17 Thommen Medical AG

- 6.4.18 Ultradent Products Inc.

- 6.4.19 Young Innovations Inc.

- 6.4.20 Ziacom Medical

- 6.4.21 ZimVie Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment