|

시장보고서

상품코드

1850105

유럽의 보안 테스트 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Europe Security Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

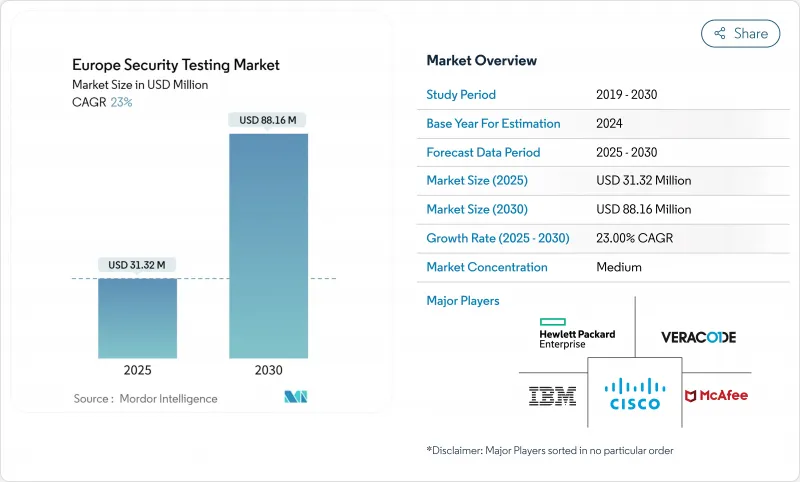

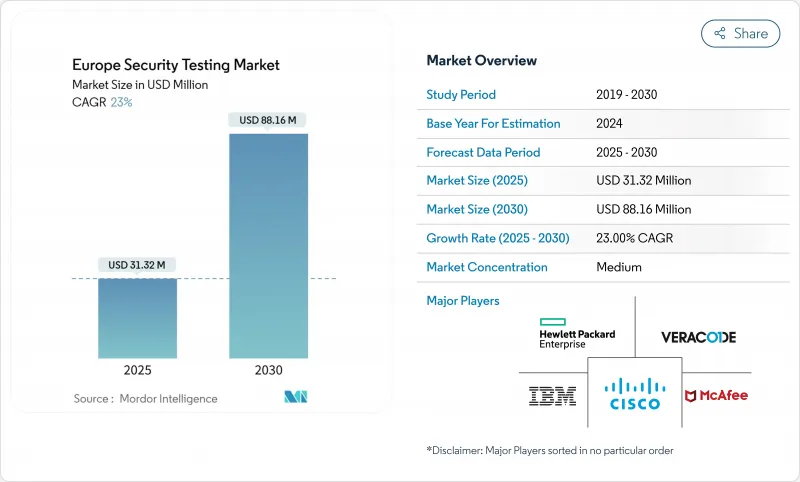

유럽의 보안 테스트 시장 규모는 2025년에 313억 2,000만 달러, 2030년에는 881억 6,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR은 23%를 나타낼 전망입니다.

이 3배 가까운 성장은 디지털 변혁에 대한 노력이 가속화되고 있는 가운데, 조직이 점점 더 정교해지고 있는 사이버 위협에 직면하고 있는 유럽 전역의 디지털 위협 상황의 격화를 반영합니다. 이 시장의 성장 궤도는 과거의 패턴을 크게 상회하고 있으며, 유럽 전역에서 보안 우선 순위가 근본적으로 변화하고 있음을 보여줍니다.

이 시장은 엄격한 규제, 특히 중요 부문에 종합적인 보안 테스트를 의무화하는 네트워크 정보 보안 지령 2(NIS2)와 디지털 운용 회복법(DORA)의 시행에 의해 재구축되고 있습니다. 2024년 시장 점유율은 클라우드 배포가 61%로 압도적이고 용도 보안 테스트가 39%로 가장 큰 부문을 차지하고 있습니다. 지역별로는 영국이 23.11% 시장 점유율로 선도하고 있지만, 2030년까지의 CAGR은 26.4%를, 프랑스가 가장 빠른 성장을 나타내고 있습니다.

Accenture 및 IBM과 같은 기존 기업은 보다 효율적인 테스트 솔루션을 제공하기 위해 AI 중심 자동화를 활용하는 유럽의 보안 테스트 전문 공급업체의 압력에 직면해 시장 경쟁이 치열해지고 있습니다. 조직은 오감지를 줄이고 개발 사이클 초기에 보안을 통합하려고 하기 때문에 시장은 대화형 용도 보안 테스트(IAST)로의 현저한 변화를 목격하고 있으며 CAGR 27.8%로 성장하고 있습니다. 이 동향은 특히 제조업에서 두드러지며 산업용 IoT의 채택이 증가하고 IT와 OT의 보안 요건이 융합되어 있기 때문에 CAGR 25.2%와 최종 사용자 중에서 가장 급성장하고 있습니다.

EU 회원국 간에 데이터 주권에 관한 규칙이 분리되어 클라우드 기반 보안 검사 솔루션을 구현하는 데 어려움이 발생했지만, 이는 동시에 운영 및 규정 준수 요구 사항을 모두 충족할 수 있는 하이브리드 배포 모델의 혁신을 촉구하고 있습니다. 특히 금융서비스나 정부기관에서는 양자화 후 보안위협에 대비하기 위한 초기단계의 시험운용이 이미 시작되고 있습니다.

유럽 보안 테스트 시장 동향과 통찰

2023년 이후 급증하는 중요 인프라 사이버 공격

2024년에 유럽의 송전망과 철도 시스템에 대한 성공적인 공격이 잇따랐고, 중요한 인프라 사업자는 테스트 설계도의 재검토를 강요받았습니다. ENISA에 따르면 인시던트 건수는 38% 증가하여 OT 침입 기술이 기존 경계 제어를 우회했다고 합니다. 보안 예산은 특히 모니터링 제어 및 데이터 수집 트래픽을 다루는 배전 네트워크에서 IT와 OT의 융합 환경 전반의 취약성을 매핑할 수 있는 서비스에 착수하고 있습니다. 레드 팀과 블루 팀을 결합하여 대응하는 공급자는 이제 여러 국가에 걸쳐 계약 규모에서 이익을 얻고 있습니다. 인시던트 보고 의무 제도가 확대됨에 따라 실시간 테스트의 증거가 규제 당국에 제출하는 데 필수적이며 수요가 더욱 높아지고 있습니다.

EU의 NIS2 및 DORA 규정 준수 기한 이전

NIS2는 2024년 10월에 시행되었으며, DORA는 2025년 1월에 가동되기 때문에 컴플라이언스의 기한이 단축되어 기업은 정기적인 보안 평가를 제도화할 수밖에 없었습니다. DORA의 3년 주기 위협이 주도한 은행 침입 테스트는 이미 외부 테스터와의 다년간 프레임워크 계약을 야기했으며, NIS2공급망에 중점을 두어 타사 코드 저장소의 다운스트림 검증을 추진하고 있습니다. 국경을 넘어서는 콩그로말리트는 감사의 중복을 피하기 위해 테스트 오케스트레이션을 중앙 집중화하고, 여러 규제 당국을 위해 스케줄을 세우고, 실행하고, 증거를 문서화하는 통합 플랫폼의 도입에 박차를 가하고 있습니다.

CREST 인증 보안 테스트 실시자 부족

유럽의 인력 부족은 여전히 심각하며 영국에서만 매년 7,000명의 전문가가 추가로 필요합니다. 이 격차는 특히 클라우드와 OT 분야에서 두드러지며 대규모 혁신 프로그램의 프로젝트 킥오프를 늦추고 있습니다. 자동화를 통해 루틴 워크는 완화되는 것이며, 고객이 고급 테스터에 기대하는 컨텍스트 분석을 대체할 수 없기 때문에 유럽의 보안 테스트 시장의 절대적인 딜리버리 능력은 제약되고 있습니다.

부문 분석

클라우드 기반 모델은 2024년 유럽 보안 테스트 시장의 61%를 차지했으며 2030년까지 연평균 복합 성장률(CAGR)은 26.01%가 될 전망입니다. 클라우드 배포의 유럽 보안 테스트 시장 규모는 2030년까지 540억 달러에 이를 것으로 예측됩니다. 이는 공격자의 지역을 몇 분 안에 복제하는 탄력적인 테스트 환경에 대한 수요 증가를 반영합니다. 영국 기업은 일반적으로 클라우드 네이티브 플랫폼에서 매주 외부 공격 시뮬레이션을 시작하고 독일 기업은 암호화 키를 On-Premise로 유지하는 하이브리드 구성을 선호합니다. 공급자는 현재 프랑스의 엄격한 데이터 지역 법령을 충족하기 위해 지역 내 키 관리 및 전임 SOC 직원 배치와 같은 소블린 클라우드 관리를 번들하고 있습니다. On-Premise의 설치는 특히 방위성 등 기밀 정보가 처리되는 장소에서는 여전히 중요하지만, 이러한 기관에서도, 원시의 데이터 유출을 제한하면서 테스트 로그를 오프 사이트에 보관하는 안전한 「컴퓨트 아웃, 데이터 인」패턴을 시험적으로 도입하고 있습니다. 유럽의 하이퍼스케일러가 지역 존에 수십억 유로의 투자를 맹세하는 가운데, 하이브리드 오케스트레이션은 운영 민첩성과 국가 보안 의무와의 균형을 이루는 조직의 실용적인 교역 역할로 부상하고 있습니다. 따라서 유럽의 보안 테스트 시장은 감사 추적을 중단시키지 않으면서 프라이빗 랙과 규제 클라우드 간에 워크로드를 원활하게 이동시키는 통합 도입 포트폴리오로 계속 전환하고 있습니다.

Application Security Test(AST)는 2024년 유럽 보안 테스트 시장 매출의 39%를 창출해 웹, 모바일 및 서버리스 워크로드가 증가함에 따라 채택 곡선을 선도하고 있습니다. AST 가운데, 클라우드에 특화된 평가가 CAGR 31%로 가장 급상승하고 있으며, 금융기관에 레거시 코드와 컨테이너화 코드의 양쪽의 리뷰를 의무화하는 DORA 조항이 뒷받침하고 있습니다. AST의 유럽 보안 테스트 시장 점유율은 커밋 파이프라인에 동적 스캔을 통합하고 프로덕션 가동 전에 리스크를 제거할 수 있는 지속적인 통합 도구로 강화되었습니다. 네트워크 보안 테스트는 특히 M&A가 구축한 플랫 네트워크를 세분화하기 위해 제로 트러스트 롤아웃의 핵심을 담당합니다. VPN 평가는 다중 요소 인증을 우회하는 원격 액세스의 악용이 발표되었기 때문에 긴급성을 높였습니다. 방화벽 테스트는 이전에는 규칙 세트의 위생 관리였지만 현재는 도메인 프론팅을 사용하는 상대에게 검사 깊이를 측정하기 위해 회피 트래픽 에뮬레이션을 통합했습니다. 클라우드, 모바일 및 API의 표면이 융합됨에 따라 기업은 여러 테스트 유형에서 얻은 지식을 상호 참조하고 예산을 늘리지 않고 커버리지를 극대화하는 통합 참여를 요청하는 경우가 늘어나고 있습니다.

유럽의 보안 테스트 시장은 배포(On-Premise, 클라우드, 하이브리드), 유형(네트워크 보안 테스트, 용도 보안 테스트 등), 테스트 도구(웹 용도 테스트 도구, 코드 검토 도구 등), 최종 사용자 산업(정부 기관, BFSI 등), 국가별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 2023년 이후 중요 인프라에 대한 사이버 공격이 증가(전력 및 철도)

- EU NIS2 및 DORA 규정 준수 기한 가속

- 소프트웨어 공급망에서 Shift-left DevSecOps 채택

- 독일의 미텔스탠드 공장에서 산업용 IoT의 보급

- 유럽의 공공 부문의 입찰에 있어서의 침입 테스트의 의무화 조항

- 양자 내성 암호 이행 파일럿 프로젝트(비공식 진행)

- 시장 성장 억제요인

- CREST 인증 보안 테스터 부족

- 2024년 신용 계약을 받아 EU27개국 중소기업의 예산 동결

- 분산된 데이터 주권 규칙이 클라우드 기반 테스트를 늦추고 있다

- 거짓 양성 피로를 완화하기 위해 검사 빈도 감소(비공식 진행)

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 전개별

- On-Premise

- 클라우드

- 하이브리드

- 유형별

- 네트워크 보안 테스트

- VPN 테스트

- 방화벽 테스트

- 기타 서비스 유형

- 용도 보안 테스트

- 용도 유형별

- 모바일 애플리케이션의 보안 테스트

- 웹 용도의 보안 테스트

- 클라우드 애플리케이션의 보안 테스트

- 엔터프라이즈 용도의 보안 테스트

- 네트워크 보안 테스트

- 테스트 유형별

- SAST

- DAST

- IAST

- RASP

- 최종 사용자 업계별

- 정부

- BFSI

- 헬스케어

- 제조업

- IT 및 통신

- 소매

- 기타 최종 사용자 업계

- 테스트 툴별

- 웹 용도 테스트 툴

- 코드 리뷰 도구

- 침입 테스트 도구

- 소프트웨어 테스트 툴

- 기타 테스트 툴

- 국가별

- 영국

- 독일

- 프랑스

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Accenture

- Atos

- Cisco Systems

- Core Security Technologies

- CrowdStrike

- Fortinet

- Hewlett Packard Enterprise

- IBM

- Kaspersky

- Micro Focus(CyberRes)

- McAfee

- Netcraft

- Offensive Security

- Orange Cyberdefense

- 팔라디온(Tech Mahindra)

- PwC

- Qualys

- Securonix

- Synopsys

- Veracode

제7장 시장 기회와 장래의 전망

SHW 25.11.17The Europe Security Testing Market size is estimated at USD 31.32 billion in 2025 and is projected to reach USD 88.16 billion by 2030, growing at a robust CAGR of 23% during the forecast period.

This nearly threefold expansion reflects the intensifying digital threat landscape across Europe, where organizations face increasingly sophisticated cyber threats amid accelerated digital transformation initiatives. The market's growth trajectory is significantly steeper than historical patterns, indicating a fundamental shift in security priorities across the continent.

The market is being reshaped by stringent regulatory forces, particularly the implementation of the Network and Information Security Directive 2 (NIS2) and Digital Operational Resilience Act (DORA), which mandate comprehensive security testing for critical sectors. Cloud deployment dominates with 61% market share in 2024, while application security testing represents the largest type of segment at 39%. The United Kingdom leads geographically with 23.11% market share, though France exhibits the fastest growth at 26.4% CAGR through 2030, driven by substantial government investments in cybersecurity infrastructure.

Competitive intensity in the market is escalating as established players like Accenture and IBM face pressure from specialized European security testing providers leveraging AI-driven automation to deliver more efficient testing solutions. The market is witnessing a notable shift toward Interactive Application Security Testing (IAST), growing at 27.8% CAGR, as organizations seek to reduce false positives and integrate security earlier in development cycles. This trend is particularly pronounced in the manufacturing sector, which is experiencing the fastest growth among end-users at 25.2% CAGR due to increasing industrial IoT adoption and the convergence of IT and OT security requirements.

The fragmented data sovereignty rules across EU member states are creating implementation challenges for cloud-based security testing solutions, though this is simultaneously driving innovation in hybrid deployment models that can satisfy both operational and compliance requirements. The market's evolution is further characterized by the emergence of specialized testing methodologies for quantum-resistant cryptography, particularly in financial services and government sectors, where early pilots are already underway to prepare for post-quantum security threats.

Europe Security Testing Market Trends and Insights

Heightened Post-2023 Critical-Infrastructure Cyber-Attacks

A succession of sophisticated attacks on European power grids and rail systems in 2024 pushed critical-infrastructure operators to overhaul testing blueprints. ENISA logged a 38% rise in incidents, with OT infiltration techniques bypassing legacy perimeter controls. Security budgets have been redirected toward services capable of mapping vulnerabilities across converged IT-OT environments, especially in distribution networks handling supervisory control and data acquisition traffic. Providers responding with combined red- and blue-team engagements are benefiting from contract sizes that now extend across multi-country footprints. Expansion of mandatory incident reporting regimes further cements demand, as real-time testing evidence becomes essential for regulatory filings.

Accelerated EU NIS2 & DORA Compliance Deadlines

NIS2 enforcement in October 2024 and DORA's go-live in January 2025 compressed compliance windows and forced organizations to institutionalize recurring security assessments. DORA's three-year threat-led penetration-testing cycle for banks has already triggered multiyear framework agreements with external testers, while NIS2's supply-chain focus is driving downstream validation of third-party code repositories. Cross-border conglomerates are centralizing test orchestration to avoid audit duplication, spurring uptake of unified platforms that schedule, execute, and document evidence for multiple regulators.

Shortage of CREST-Certified Security Testers

Europe's talent deficit remains acute, with the United Kingdom alone needing 7,000 additional professionals every year. The gap is especially sharp in cloud and OT disciplines, delaying project kick-offs for large transformation programs. Automation mitigates routine tasks yet cannot replace the contextual analysis clients expect from senior testers, thereby constraining the absolute delivery capacity of the Europe security testing market.

Other drivers and restraints analyzed in the detailed report include:

- Shift-Left DevSecOps Adoption in the Software Supply Chain

- Industrial IoT Penetration in German Mittelst and Factories

- Budget Freeze Across EU-27 SMEs Amid 2024 Credit-Tightening

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based models delivered 61% of the Europe security testing market in 2024 and are on track for a 26.01% CAGR through 2030. The Europe security testing market size for cloud deployment is projected to reach USD 54 billion by 2030, reflecting mounting demand for elastic test environments that replicate attacker geographies within minutes. United Kingdom enterprises typically launch weekly external attack simulations from cloud-native platforms, while German firms favour hybrid configurations that retain encryption keys on-premises. Providers now bundle sovereign-cloud controls such as in-region key management and dedicated SOC staffing to satisfy France's strict data-locality statutes. On-premises installations remain relevant where classified information is processed, notably in defense ministries, yet even these agencies pilot secure "compute-out, data-in" patterns that keep test logs offsite while restricting raw data exfiltration. As European hyperscalers pledge multibillion-euro investments in regional zones, hybrid orchestration has emerged as a pragmatic bridge for organizations balancing operational agility with national-security mandates. The Europe security testing market therefore continues to pivot toward integrated deployment portfolios that shift workloads seamlessly between private racks and regulated clouds without disrupting audit trails.

Application security testing (AST) generated 39% of the Europe security testing market revenue in 2024 and leads adoption curves as web, mobile, and serverless workloads multiply. Within AST, cloud-specific assessments post the steepest climb at 31% CAGR, propelled by DORA clauses obliging financial entities to review both legacy and containerized code. The Europe security testing market share for AST is bolstered by continuous integration tools that embed dynamic scans into commit pipelines, enabling risk triaging before production. Network security testing still anchors zero-trust rollouts, particularly for segmenting flat networks amassed through M&A activity. VPN assessments gained urgency following publicized remote-access exploits that bypassed multi-factor authentication. Firewall testing, formerly a ruleset hygiene exercise, now incorporates evasive-traffic emulation to gauge inspection depth against adversaries using domain fronting. As cloud, mobile, and API surfaces converge, enterprises increasingly commission unified engagements that cross-reference findings from multiple test types, maximizing coverage without inflating budgets.

Europe Security Testing Market Segmented by Deployment (On-Premises, Cloud and Hybrid), Type (Network Security Testing, Application Security Testing and More), Testing Tool (Web Application Testing Tool, Code Review Tool and More), End-User Industry (Government, BFSI and More) and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Accenture

- Atos

- Cisco Systems

- Core Security Technologies

- CrowdStrike

- Fortinet

- Hewlett Packard Enterprise

- IBM

- Kaspersky

- Micro Focus (CyberRes)

- McAfee

- Netcraft

- Offensive Security

- Orange Cyberdefense

- Paladion (Tech Mahindra)

- PwC

- Qualys

- Securonix

- Synopsys

- Veracode

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Heightened post-2023 critical-infrastructure cyber-attacks (Power and Rail)

- 4.2.2 Accelerated EU NIS2 and DORA compliance deadlines

- 4.2.3 Shift-left DevSecOps adoption in software supply-chain

- 4.2.4 Industrial IoT penetration in German Mittelstand factories

- 4.2.5 Mandatory penetration-testing clauses in European public-sector tenders

- 4.2.6 Quantum-resistant crypto migration pilots (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 Shortage of CREST-certified security testers

- 4.3.2 Budget freeze across EU-27 SMEs amid 2024 credit-tightening

- 4.3.3 Fragmented data-sovereignty rules slowing cloud-based testing

- 4.3.4 False-positive fatigue reducing test frequency (under-the-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Type

- 5.2.1 Network Security Testing

- 5.2.1.1 VPN Testing

- 5.2.1.2 Firewall Testing

- 5.2.1.3 Other Service Types

- 5.2.2 Application Security Testing

- 5.2.2.1 By Application Type

- 5.2.2.1.1 Mobile Application Security Testing

- 5.2.2.1.2 Web Application Security Testing

- 5.2.2.1.3 Cloud Application Security Testing

- 5.2.2.1.4 Enterprise Application Security Testing

- 5.2.2.2 By Testing Type

- 5.2.2.2.1 SAST

- 5.2.2.2.2 DAST

- 5.2.2.2.3 IAST

- 5.2.2.2.4 RASP

- 5.2.1 Network Security Testing

- 5.3 By End-User Industry

- 5.3.1 Government

- 5.3.2 BFSI

- 5.3.3 Healthcare

- 5.3.4 Manufacturing

- 5.3.5 IT and Telecom

- 5.3.6 Retail

- 5.3.7 Other End-User Industries

- 5.4 By Testing Tool

- 5.4.1 Web Application Testing Tool

- 5.4.2 Code Review Tool

- 5.4.3 Penetration Testing Tool

- 5.4.4 Software Testing Tool

- 5.4.5 Other Testing Tools

- 5.5 By Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture

- 6.4.2 Atos

- 6.4.3 Cisco Systems

- 6.4.4 Core Security Technologies

- 6.4.5 CrowdStrike

- 6.4.6 Fortinet

- 6.4.7 Hewlett Packard Enterprise

- 6.4.8 IBM

- 6.4.9 Kaspersky

- 6.4.10 Micro Focus (CyberRes)

- 6.4.11 McAfee

- 6.4.12 Netcraft

- 6.4.13 Offensive Security

- 6.4.14 Orange Cyberdefense

- 6.4.15 Paladion (Tech Mahindra)

- 6.4.16 PwC

- 6.4.17 Qualys

- 6.4.18 Securonix

- 6.4.19 Synopsys

- 6.4.20 Veracode

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis