|

시장보고서

상품코드

1850144

유럽의 생검 기기 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Europe Biopsy Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

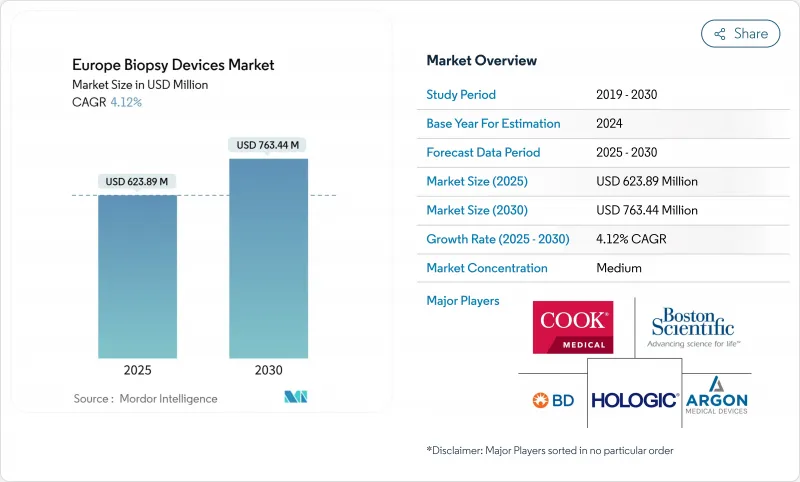

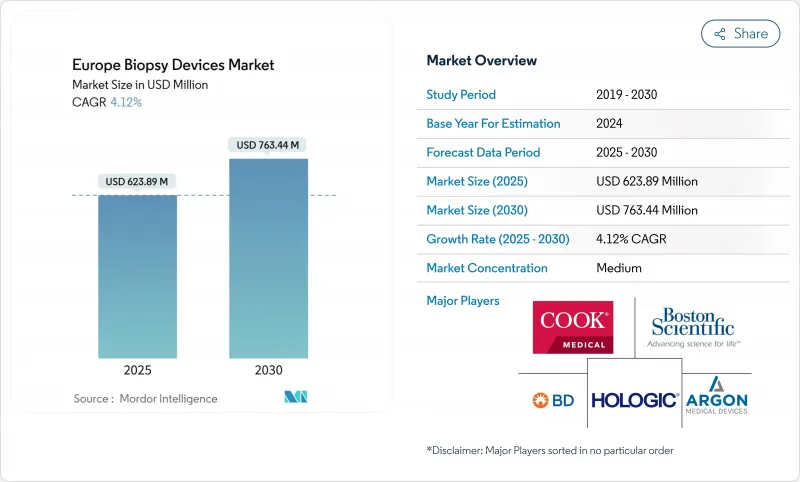

유럽의 생검 기기 시장 규모는 2025년에 6억 2,389만 달러, 2030년에는 7억 6,344만 달러에 이를 것으로 예측되며, CAGR은 4.12%를 나타낼 전망입니다.

조직 암 검진 프로그램이 확대되고, 병원이 EU 의료기기 규제(MDR)를 준수하는 장비로 업그레이드하고, 의사가 이미지 유도를 통한 저침습 기술로 이동함에 따라 수요가 증가하고 있습니다. 진공 어시스트나 코어 니들 시스템의 채택이 가속되고 있는 것은 샘플링 에러를 줄이고, 수기 시간을 단축해, MRI나 CT 가이던스와 용이하게 통합할 수 있기 때문입니다. 반대로 MDR 인증 지연과 관련된 공급 병목 현상은 특히 소규모 시설의 경우 가격 설정을 견고하고 조달 격차를 낳습니다. 안전과 관련된 제품 리콜은 시판 후 감시를 강화할 필요성을 강조하며, 병원은 강력한 품질 시스템을 입증할 수 있는 공급업체를 선호하게 됩니다. 이 지역 전체에서는 국가의 진료 보수 개혁에 의해 생검의 외래수술센터(ASC)에의 이행이 진행되고 있어, 복잡한 종양 증례에 대한 병원의 용량을 유지하면서, 수술 전체의 비용을 낮추고 있습니다.

유럽의 생검 기기 시장 동향과 통찰

낮은 침습 절차에 대한 선호도 증가

경회 음전립선 생검은 진단 정확도를 손상시키지 않고 기존의 경직장 루트보다 감염률이 낮은 것이 다 시설 시험에서 나타났기 때문에 현재는 주요 비뇨기과 센터에서 표준 치료가 되고 있습니다. 작은 간 병변에 대한 MRI 가이드 아래 프리핸드 방법은 90%의 임상적 성공을 거두었고, 이전에는 CT 가이드에 의존했던 종양 내과에의 보급을 촉진하고 있습니다. 이러한 환자 친화적인 치료법은 회복 시간을 단축하고, 입원 기간을 단축하며, 지불자의 비용 억제 목표에 부합합니다. 연구 그룹은 현재 통증 없이 세포내 바이오마커를 샘플링할 수 있는 나노 니들 패치를 테스트하고 있습니다. 이러한 진보로 유럽의 생검 기기 시장은 규제의 장애물이 오르더라도 안정된 채택 곡선을 그려나갈 것입니다.

EU27개국에서 암 검진 프로그램 증가

유럽위원회의 「암 박멸 계획(Beating Cancer Plan)」은 2025년까지 유방암, 자궁경부암, 대장암의 검진 진찰률 90%를 달성하기 위해 40억 유로를 계상해, 그 대상을 폐암이나 전립선암으로까지 넓혔습니다. 조직화된 프로그램은 장당한 검진을 대신하여 의료 시스템에 표준화된 생검 키트, 트레이닝용 마네킹, AI 대응 이미지 리뷰 소프트웨어를 구입하게 합니다. 2025년을 향해 갱신된 사망률 예측에 의하면, 50-69세 여성의 유방암 사망률은 이미 9.8% 감소하고 있어, 이 결과는 나라의 검진 예산에 대한 정치적 지지를 강화하고 있습니다. 중·동유럽 국가들은 역사적으로 설비가 충분하지 않았기 때문에 EU의 결속자금을 이동식 생검 기기에 투입하여 접근의 갭을 메우려 하고 있습니다. 이러한 정책 중심 수요는 장비 공급업체들에게 예측가능한 다년간 주문 파이프라인을 지원합니다.

제품 리콜 및 안전 알림

홀로직은 통증, 감염, 이동에 대한 188건의 부작용 보고를 받았으며 9만 1,000개 이상의 BioZorb 3D 마커를 자발적으로 회수했습니다. FDA는 또한 스테인레스 스틸 파편이 혼입될 위험이 있는 스테레오 택틱 일회용 바늘 키트에 경고를 발행하고 EU의 경계 통지와 조달 동결을 촉구했습니다. 병원은 현재 더 엄격한 공급업체 감사를 부과하고 실시간 배치 추적성을 요구하기 때문에 판매주기가 길어지고 제조업체 지원 비용이 증가하고 있습니다. 이러한 사건은 유럽의 생검 기기 시장의 단기 수량 성장을 약화하지만 견고한 품질 관리 시스템의 전략적 가치를 강화합니다.

부문 분석

2024년 유럽의 생검 기기 시장은 바늘 기반 시스템이 48.25%의 판매 점유율을 차지하고 2030년을 향해 CAGR 8.35%를 보일 것으로 예측됩니다. 코어 디바이스는 현재 더욱 선명한 팁 디자인, 독특한 코팅 및 유전체 분석을 위한 조직 아키텍처를 유지하는 조절 가능한 슬로우 길이를 특징으로 합니다. 진공 지원 핸드피스는 한 번의 절개로 여러 개의 연속 코어를 채취하여 재수술을 줄일 수 있습니다. VACIS 시험에서는 저악성도 유관암 in situ의 수술 회피 옵션으로 진공 절제가 위치하고 있습니다. 또한 유방 온존 수술을 유도하는 현지화 와이어와 방사성 시드 시스템에 대한 수요도 상환에 따라 다른 것, 꾸준히 계속되고 있습니다. 디지털 가이던스 콘솔은 전자기 유도와 실시간 초음파를 통합하여 바쁜 외래 센터에서 워크플로우를 완화합니다. 네오다이내믹스의 펄스 기술 장치는 수술 시간의 단축과 오퍼레이터의 학습 곡선의 단축을 목표로 하는 지속적인 기술 혁신을 강조하고 있습니다.

프로시저 트레이, 마커 및 보조 키트는 자본 예산 주기로부터 공급업체를 보호하는 일상적인 소모품 판매를 제공합니다. MDR 컴플라이언스 비용이 새로운 진입을 제한하기 때문에 가격 경쟁은 여전히 완만합니다. 병원은 핵심 바늘, 진공 시스템, 현지화 도구, AI 지원 콘솔 등 종합적인 포트폴리오를 제공하는 공급업체를 선호하고 스크리닝 워크플로우를 중단하지 않는 현장 서비스 기능을 갖추고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 낮은 침습 수술에 대한 관심 증가

- EU27개국에서의 암 검진 프로그램 증가

- 외래 생검 센터로의 이행

- 영상 유도 로봇의 기술적 융합

- EU의 체외 진단용 의료기기 규제가 기기의 업그레이드를 촉진

- 시장 성장 억제요인

- 제품 리콜 및 안전에 관한 알림

- 엄격한 MDR 인증 스케줄이 공급 갭을 초래하고 있다

- 신형 진공 보조 시스템에 대한 한정적인 상환

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품별

- 바늘식 생검 기구

- 코어 생검 디바이스

- 흡인생검침

- 진공 보조 생검 기기

- 처리 트레이

- 현지화 와이어

- 기타 제품

- 바늘식 생검 기구

- 용도별

- 유방 생검

- 폐 생검

- 대장 생검

- 전립선 생검

- 기타 용도

- 최종 사용자별

- 병원

- 진단 및 영상 진단센터

- 외래수술센터(ASC)

- 기타

- 지역

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Becton, Dickinson and Company

- Hologic Inc.

- Devicor Medical Products Inc.

- Cook Medical

- Boston Scientific Corporation

- Intact Medical Corporation

- Gallini Medical

- TSK Laboratory Europe BV

- Argon Medical Devices

- Medtronic plc

- Olympus Corporation

- Cardinal Health

- Danaher Corporation

- Stryker Corporation

- IZI Medical Products

- FUJIFILM Holdings Corporation

- Merit Medical Systems

제7장 시장 기회와 장래의 전망

SHW 25.11.07The Europe biopsy devices market size stood at USD 623.89 million in 2025 and is forecast to reach USD 763.44 million by 2030, advancing at a 4.12% CAGR.

Demand continues to rise as organized cancer-screening programs expand, hospitals upgrade to EU Medical Device Regulation (MDR)-compliant equipment, and physicians shift toward imaging-guided, minimally-invasive techniques. Adoption of vacuum-assisted and core needle systems is accelerating because they reduce sampling errors, shorten procedure time, and integrate easily with MRI or CT guidance. Conversely, supply bottlenecks linked to MDR certification delays keep pricing firm and create procurement gaps, especially for smaller facilities. Safety-related product recalls underscore the need for robust post-market surveillance, prompting hospitals to favor vendors that can demonstrate strong quality systems. Across the region, national reimbursement reforms are steering a growing share of biopsies to ambulatory surgical centers, lowering overall procedure costs while preserving hospital capacity for complex oncology cases.

Europe Biopsy Devices Market Trends and Insights

Increasing Preference for Minimally-Invasive Procedures

Transperineal prostate biopsies now represent standard-of-care across leading urology centers after a multicenter trial showed lower infection rates than the traditional transrectal route, without compromising diagnostic accuracy. MRI-guided freehand techniques for small liver lesions reach 90% clinical success, encouraging their dissemination to oncology units that previously relied on CT guidance. Such patient-friendly modalities shorten recovery time and reduce hospital stays, aligning with payer cost-containment goals. Research groups are now testing nanoneedle patches capable of sampling intracellular biomarkers painlessly, a breakthrough that could reach clinical practice by 2026. These advances should keep the Europe biopsy devices market on a steady adoption curve even as regulatory hurdles rise.

Rising Cancer Screening Programs Across EU-27

The European Commission's Beating Cancer Plan earmarked EUR 4 billion to achieve 90% screening coverage for breast, cervical, and colorectal cancers by 2025, and has broadened scope to lung and prostate cancers. Organized programs replace opportunistic screening, compelling health systems to buy standardized biopsy kits, training mannequins, and AI-enabled image-review software. Updated mortality projections for 2025 already show a 9.8% decline in breast-cancer deaths among women aged 50-69, a result that is reinforcing political support for national screening budgets. Central and Eastern European countries, historically under-equipped, are channeling EU cohesion funds into mobile biopsy units to close access gaps. This policy-driven demand supports a predictable, multi-year order pipeline for device suppliers.

Product Recalls & Safety Notices

Hologic voluntarily withdrew more than 91,000 BioZorb 3D markers after 188 adverse-event reports of pain, infection, and migration, triggering a Class I recall and heightening regulatory scrutiny. The FDA also flagged Stereotactic disposable needle kits that risked stainless-steel debris contamination, prompting EU vigilance notices and procurement freezes. Hospitals now impose stricter supplier audits and require real-time batch traceability, lengthening sales cycles and raising support costs for manufacturers. These episodes dampen near-term volume growth within the Europe biopsy devices market but reinforce the strategic value of robust quality-management systems.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Ambulatory & Outpatient Biopsy Centers

- EU In-Vitro Diagnostic Regulation Driving Device Upgrades

- Stringent MDR Certification Timelines Causing Supply Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Needle-based systems dominated the Europe biopsy devices market with a 48.25% revenue share in 2024, and they will grow at an 8.35% CAGR toward 2030 as physicians upgrade to core and vacuum-assisted platforms that minimize sampling errors. Core devices now feature sharper tip designs, proprietary coatings, and adjustable throw lengths that preserve tissue architecture for genomic assays. Vacuum-assisted handpieces collect multiple contiguous cores through a single incision, reducing repeat procedures; the VACIS trial even positions vacuum excision as a surgery-sparing option for low-grade ductal carcinoma in situ. Steady demand also persists for localization wires and radioactive seed systems that guide breast-conserving surgery, although adoption varies with reimbursement. Digital guidance consoles integrate electromagnetic tracking with real-time ultrasound, easing workflow in busy ambulatory centers. NeoDynamics' pulse-technology device underscores continuing innovation aimed at shortening procedure time and operator learning curves.

Procedure trays, markers, and ancillary kits deliver recurring consumable sales that insulate vendors from capital-budget cycles. Price competition remains moderate because MDR compliance costs limit new entrants. Hospitals prioritize suppliers that offer comprehensive portfolios-core needles, vacuum systems, localization tools, and AI-ready consoles-along with field-service capabilities that ensure uninterrupted screening workflows.

The Europe Biopsy Devices Market Report is Segmented by Product (Needle-Based Biopsy Instruments [Core Biopsy Devices, and More], Procedure Trays, and More), Application (Breast Biopsy, Lung Biopsy, Colorectal Biopsy, and More), End User (Hospitals, Diagnostic & Imaging Centers, and More), and Geography (Germany, United Kingdom, France, Italy, Spain, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Beckton Dickinson

- Hologic

- Devicor Medical Products

- Cook Group

- Boston Scientific

- Intact Medical

- Gallini Medical

- TSK Laboratory Europe

- Argon Medical Devices

- Medtronic

- Olympus

- Cardinal Health

- Danaher

- Stryker

- IZI Medical Products

- FUJIFILM

- Merit Medical Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Preference For Minimally-Invasive Procedures

- 4.2.2 Rising Cancer Screening Programs Across EU-27

- 4.2.3 Shift Toward Ambulatory & Outpatient Biopsy Centers

- 4.2.4 Technological Convergence Of Imaging-Guided Robotics

- 4.2.5 EU In-Vitro Diagnostic Regulation Driving Device Upgrades

- 4.3 Market Restraints

- 4.3.1 Product Recalls & Safety Notices

- 4.3.2 Stringent MDR Certification Timelines Causing Supply Gaps

- 4.3.3 Limited Reimbursement For Novel Vacuum-Assisted Systems

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Needle-based Biopsy Instruments

- 5.1.1.1 Core Biopsy Devices

- 5.1.1.2 Aspiration Biopsy Needles

- 5.1.1.3 Vacuum-assisted Biopsy Devices

- 5.1.2 Procedure Trays

- 5.1.3 Localization Wires

- 5.1.4 Other Products

- 5.1.1 Needle-based Biopsy Instruments

- 5.2 By Application

- 5.2.1 Breast Biopsy

- 5.2.2 Lung Biopsy

- 5.2.3 Colorectal Biopsy

- 5.2.4 Prostate Biopsy

- 5.2.5 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Diagnostic & Imaging Centers

- 5.3.3 Ambulatory Surgical Centers

- 5.3.4 Others

- 5.4 Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Becton, Dickinson and Company

- 6.3.2 Hologic Inc.

- 6.3.3 Devicor Medical Products Inc.

- 6.3.4 Cook Medical

- 6.3.5 Boston Scientific Corporation

- 6.3.6 Intact Medical Corporation

- 6.3.7 Gallini Medical

- 6.3.8 TSK Laboratory Europe BV

- 6.3.9 Argon Medical Devices

- 6.3.10 Medtronic plc

- 6.3.11 Olympus Corporation

- 6.3.12 Cardinal Health

- 6.3.13 Danaher Corporation

- 6.3.14 Stryker Corporation

- 6.3.15 IZI Medical Products

- 6.3.16 FUJIFILM Holdings Corporation

- 6.3.17 Merit Medical Systems

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment