|

시장보고서

상품코드

1850160

에어로겔 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Aerogel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

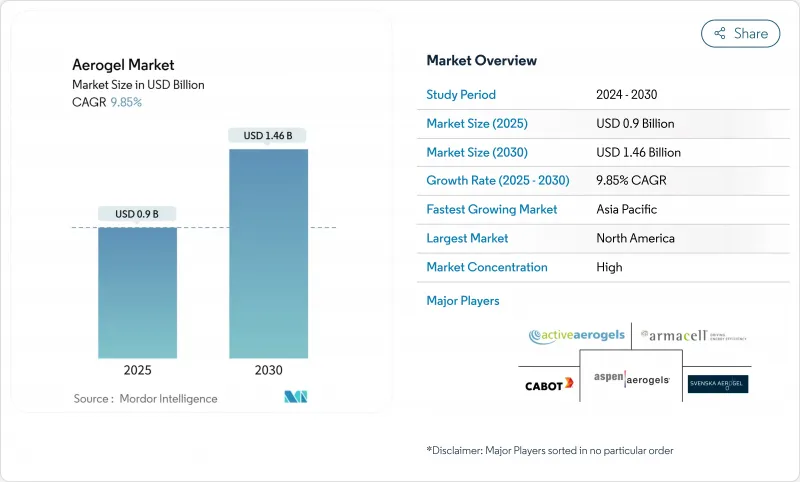

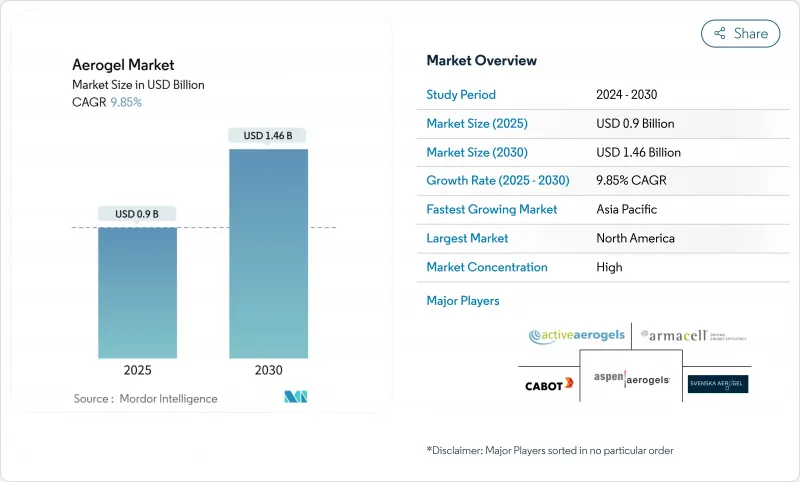

에어로겔 시장의 2025년 시장 규모는 9억 달러, 2030년에는 14억 6,000만 달러로 성장하고, 2025-2030년의 CAGR은 9.85%를 나타낼 것으로 전망됩니다.

고성능 단열재에 대한 지속적인 수요는 가속화하는 전기와 탄소 삭감 의무화와 함께 에어로겔 시장을 강력한 성장 궤도에 올리고 있습니다. 북미는 엄격한 에너지 효율 규제와 활발한 석유 및 가스 개수 사이클에 힘입어 현재 40%의 점유율로 선도하고 있습니다. 시장 통합이 진행되고 있으며, Aspen Aerogels와 Cabot Corporation은 세계적인 수익의 기둥이 되고 있습니다.

세계 에어로겔 시장 동향과 통찰

재사용성과 재활용성에 의한 에어로겔 채택 증가

제조업체는 재사용 가능성을 극대화하고 폐기물 발생을 최소화하는 생산 경로를 선호합니다. 새로운 실리카 에어로겔은 밀도가 75kg/m3인 저밀도로 95%의 기공률을 유지하여 열 손실 없이 여러 서비스 사이클을 가능하게 했습니다. ENERSENS는 컴퓨터 제어 증발 마이크로파 프로세스의 규모를 확대하고 생산량을 60% 향상시키고 재료를 회수하고 최종 사용자의 총 소유 비용을 절감했습니다. 라이프사이클 분석에서는 산업 규모의 에어로겔 합성이 기존의 단열재에 비해 환경 부하를 삭감하는 것이 확인되어 이 재료가 넷제로 경로에 있어서 매력적인 것으로 되어 있습니다. 각 브랜드가 그린 빌딩 라벨에 대한 CO2 감축을 수치화하면서 재사용 가능한 에어로겔 단열재는 특히 수명이 길어지는 외관 개수에서 사양의 우선 순위를 높이고 있습니다.

고성능 단열재에 대한 건설 수요 급증

2021년 국제 에너지 절약 기준과 유사한 EU 기준으로 강화되는 건축 기준은 외벽의 U 값을 낮추어야 합니다. 에어로겔 패널은 미네랄 울의 2-4배의 R값을 실현하면서 보다 얇은 공동을 차지하기 때문에 공간이 한정되어 있는 도시의 개수에는 필수적입니다. 2024년 기록적인 무더위는 햇빛을 희생하지 않고 일사 취득을 제한하는 에어로겔 충전 글레이징 시스템에 대한 관심을 가속화했습니다. 새로운 산불 저항성인 '모핑' 에어로겔은 현재 화재가 발생하기 쉬운 지역의 구조물을 보호하고 있으며 에너지 절약뿐만 아니라 보다 광범위한 탄력성(회복력)의 이점을 강조하고 있습니다.

높은 제조 비용

초임계 건조는 여전히 주류 제조 루트이며 고온 고압에서 작동하는 특수 용기가 필요합니다. 자본 집약은 단가가 주류 단열재보다 높게 유지되고 비용에 민감한 주택 분야의 도입을 방해합니다. 상압 건조의 조사는 유망하지만, 아직 상업 규모에는 이르지 않았습니다. 단기적인 완화책은 처리량 향상과 용매 회수에 초점을 맞추어 변동비를 낮추는 것입니다. 이러한 기술이 성숙하기 전까지는 프리미엄의 자리매김으로 선행투자액을 정당화할 수 있는 까다로운 성능 요구와 탄소삭감 인센티브가 있는 프로젝트에만 에어로겔의 보급이 제한됩니다.

부문 분석

실리카 그레이드는 2024년 에어로겔 시장에서 72%의 점유율을 차지하고, 2030년까지의 CAGR은 10.11%로 견고하게 선두 자리를 넓힐 것으로 예상됩니다. 이 리더십은 석유 및 가스 파이프라인, 외관 단열재, EV 배터리 모듈 등 다양한 용도에 적용할 수 있기 때문입니다. 중요한 연구 개발은 열적 가치를 희생하지 않고 12배의 압축 강도를 제공하는 실리카/폴리이미드 "석류" 복합재료를 생산하여 기계적 취급에 대한 역사적인 장벽을 제거했습니다.

2세대 실리카 시스템은 내습성과 마무리 용이성도 목표로 하고 있습니다. 조정된 소수성 코팅은 현재 120° 이상의 접촉각을 유지하며 습도가 높은 기후에서 외관 외벽을 사용할 수 있습니다. 한편, 배합 담당자는 솔벤트 소비를 줄이고 비용과 CO2 배출량을 줄이는 낮은 알콕사이드 졸 - 겔 루트를 찾고 있습니다. 이러한 다방면에 걸친 기술 혁신에 의해 실리카의 에어로겔 시장에서의 지위는 흔들리지 않게 되어, 그 기술적 진보가, 이 분야가 채워야 할 전체적인 성능 기준을 결정하게 될 것 같습니다.

블랭킷은 설치 용이성과 에너지 인프라에 사용되는 파이프 절연 코팅과의 호환성으로 2024년 에어로겔 시장 수익의 64%를 확보했습니다. 최근의 제품에서는 열전도율이 0.0143W/mK로 낮아 10분 만에 열평형에 이르기 때문에 건설 스케줄을 단축할 수 있습니다.

입자 형상은 브레이크아웃 카테고리이며, 배합자가 코팅, 리튬 이온 세퍼레이터, 폴리머 복합재료에 에어로겔 분말을 통합함으로써 2030년까지의 CAGR은 10.34%를 보일 것으로 예측됩니다. 캐봇의 ENTERA 입자는 EV 배터리의 양극에서 드롭 인형의 열 조절제로서 기능하여 두꺼운 장벽 없이 폭주 현상을 완화합니다.

지역 분석

북미가 2024년 수익 점유율 40%로 에어로겔 시장을 선도했습니다. 견고한 석유 및 가스 설비 투자와 함께 연방 및 주에 의한 효율화 지령이 견고한 수요를 지지하고 있습니다. Cabot Corporation이 배터리 등급 전도성 첨가제를 현지화하기 위해 에너지부에서 5,000만 달러를 수여한 것은 에어로겔과의 직접적인 시너지 효과를 가져오는 열 관리 물질에 대한 정책 주도의 투자를 확증하는 것입니다. 전미 과학재단의 조성금도 차세대 건축 단열재 연구의 종이 되고 있어 북미는 성능 약진의 최전선에 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 10.25%로 예측되어 가장 급성장하고 있는 지역입니다. LNG 인프라의 급속한 전개, 주택 건설의 활황, EV 생산의 가속이 이 지역의 소비를 급상승시킵니다. 중국의 연구기관은 구조하중을 견디면서 극단적인 온도를 견디는 탄소-에어로겔 복합재료를 도입하여 국내 고온산업을 지원하고 있습니다.

유럽은 EPBD의 개정을 활용하여 얇고 높은 R 재료 시스템을 지원하는 심층 에너지 리노베이션을 장려하고 규제 측면에서 리더십을 강력하게 유지하고 있습니다. 사회 주택 단지의 시험 프로그램은 외관의 미관을 유지하면서 40%의 공간 난방 삭감을 달성한 외관 에어로겔 패널을 소개했습니다. 중동 및 아프리카에서는 정화 및 석유화학 업그레이드에 에어로겔이 채택되고 있으며, 남미에서는 LNG 수입과 그린빌딩 인증의 기운이 높아짐이 성장의 요인이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 재이용성과 리사이클성에 의해 에어로겔의 채택이 증가

- 고성능 단열재에 대한 건설 수요의 급증

- EU 및 북미 수요를 촉진하는 에너지 효율 규제

- 아시아 전역의 LNG 인프라 확대

- 석유 및 가스 산업이 에어로겔 수요를 지배

- 시장 성장 억제요인

- 높은 생산 비용

- 원자재의 제한된 가용성

- 건축에 있어서의 고성능 폴리머 폼과의 경쟁

- 밸류체인 분석

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체 제품 및 서비스의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 유형별

- 실리카

- 탄소

- 알루미나

- 기타 유형

- 형태별

- 담요

- 입자

- 블록

- 패널

- 용도별

- 단열재

- 방음재

- 촉매와 흡착제

- 배터리와 에너지 저장

- 채광과 반투명 패널

- 기타 용도

- 최종 사용자 업계별

- 석유 및 가스

- 건설

- 자동차

- 해양

- 항공우주

- 기타 최종 사용자 산업

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 나이지리아

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Acoustiblok, Inc.

- Active Aerogels

- Aerogel Technologies, LLC

- aerogel-it

- Armacell

- Aspen Aerogels, Inc.

- BASF

- Blueshift Materials Inc.

- Cabot Corporation

- ENERSENS

- Guangdong Alison Technology Co., Ltd.

- Knauf Insulation

- Nano Tech Co., Ltd.

- Ningbo Surnano Aerogel Co., Ltd

- Porex

- Sino Aerogel

- Svenska Aerogel AB

- TAASI Corporation

- Thermablok Aerogels Ltd.

제7장 시장 기회와 장래의 전망

SHW 25.11.07The aerogel market is valued at USD 0.90 billion in 2025 and is projected to grow to USD 1.46 billion by 2030, advancing at a 9.85% CAGR in the 2025-2030 period.

Sustained demand for high-performance thermal insulation, coupled with accelerating electrification and carbon-reduction mandates, is placing the aerogel market on a strong growth trajectory. North America leads today with a 40% share, supported by strict energy-efficiency codes and an active oil-and-gas retrofit cycle. High market consolidation prevails; Aspen Aerogels and Cabot Corporation anchor global revenue, yet a host of regional specialists compete aggressively in formulation niches.

Global Aerogel Market Trends and Insights

Rise in Adoption of Aerogel Due to Reusability and Recyclability

Manufacturers are prioritizing production routes that maximize re-use potential and minimize waste generation. New silica aerogels now preserve 95% porosity at a low 75 kg/m3 density, allowing multiple service cycles without thermal loss. ENERSENS scaled a computer-controlled evaporation microwave process that lifts output 60% while enabling material recovery, lowering total cost of ownership for end users. Life-cycle analysis confirms industrial-scale aerogel synthesis slashes environmental burdens versus conventional insulants, making the material attractive in net-zero pathways. As brands quantify CO2 savings for green-building labels, reusable aerogel insulation is gaining specification priority, particularly in facade retrofits seeking long service life.

Rapidly Growing Construction Demand for High-performance Insulation

Building codes tightened under the 2021 International Energy Conservation Code and similar EU standards mandate lower envelope U-values. Aerogel panels deliver R-values 2-4 times times higher than mineral wool while occupying thinner cavities, critical for urban refurbishments where space is limited. Record heatwaves in 2024 accelerated interest in aerogel-filled glazing systems that limit solar gain without sacrificing daylight. Novel wildfire-resistant "morphing" aerogels now protect structures in fire-prone regions, highlighting broader resilience benefits beyond energy savings.

High Production Cost

Super-critical drying remains the dominant manufacturing route and demands specialized vessels operating at high pressure and temperature. Capital intensity keeps unit prices above mainstream insulation, discouraging uptake in cost-sensitive residential segments. Research into ambient pressure drying shows promise, but it is not yet commercial at scale. Short-term mitigation focuses on throughput gains and solvent recovery to lower variable costs. Until those techniques mature, premium positioning will constrain aerogel penetration to projects with stringent performance needs or carbon-reduction incentives that justify a higher upfront outlay.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Regulations Boosting EU and North American Demand

- Expansion of LNG Infrastructure Across Asia

- Limited Availability of Raw Materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silica grades commanded a 72% share of the aerogel market in 2024 and are expected to widen their lead by posting a robust 10.11% CAGR through 2030, a rare scenario where the largest slice also grows fastest. This leadership stems from broad applicability in oil-and-gas pipelines, facade insulation, and EV battery modules. Significant research and development produced silica/polyimide "pomegranate" composites that yield 12-fold higher compressive strength without sacrificing thermal values, removing a historic barrier to mechanical handling.

Second-generation silica systems are also targeting moisture resistance and easier finishing. Tailored hydrophobic coatings now sustain contact angles above 120°, allowing exterior facade usage in humid climates. Meanwhile, formulators are exploring low-alkoxide sol-gel routes that cut solvent consumption, reducing cost and CO2 footprint. Given this multi-pronged innovation, silica's hold on the aerogel market appears secure, and its technological progress will likely dictate overall performance benchmarks the sector must meet.

Blankets secured 64% of the aerogel market revenue in 2024, owing to installation ease and compatibility with pipe-insulation jacketing used in energy infrastructure. Recent iterations achieve thermal conductivity as low as 0.0143 W/mK and reach thermal equilibrium in 10 minutes, shortening construction schedules.

Particle form is the breakout category, forecast to log a 10.34% CAGR through 2030 as formulators incorporate aerogel powders into coatings, lithium-ion separators, and polymer composites. ENTERA particles from Cabot serve as drop-in thermal modifiers in EV battery cathodes, mitigating runaway events without thick barriers.

The Aerogel Market Report Segments the Industry by Type (Silica, Carbon, Alumina, and Other Types), Form (Blanket, Particle, Block, and Panel), Application (Thermal Insulation, Acoustic Insulation, Catalyst and Adsorbent, and More), End-User Industry (Oil and Gas, Construction, Automotive, Marine, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the aerogel market with a 40% revenue share in 2024. Federal and state efficiency mandates, alongside robust oil-and-gas capital expenditure, underpin solid demand. Cabot Corporation's USD 50 million Department of Energy award to localize battery-grade conductive additives affirms policy-driven investment in thermal-management materials with direct aerogel synergies. National Science Foundation grants are also seeding next-generation building insulation research, keeping North America at the forefront of performance breakthroughs.

Asia-Pacific is projected to register a 10.25% CAGR to 2030, making it the fastest-growing region. Rapid LNG infrastructure deployment, booming residential construction, and accelerating EV production converge to raise regional consumption sharply. Chinese institutes have introduced carbon-aerogel composites that withstand extreme temperatures while bearing structural loads, supporting domestic high-temperature industries.

Europe remains strong in regulatory leadership, leveraging EPBD revisions to encourage deep-energy retrofits that favor thin, high-R material systems. Pilot programs in social housing blocks showcase facade aerogel panels achieving 40% space-heating cuts while preserving exterior aesthetics. The Middle East and Africa continue to adopt aerogel in refining and petrochemical upgrades, while South America's growth is tied to LNG imports and rising green-building certification momentum.

- Acoustiblok, Inc.

- Active Aerogels

- Aerogel Technologies, LLC

- aerogel-it

- Armacell

- Aspen Aerogels, Inc.

- BASF

- Blueshift Materials Inc.

- Cabot Corporation

- ENERSENS

- Guangdong Alison Technology Co., Ltd.

- Knauf Insulation

- Nano Tech Co., Ltd.

- Ningbo Surnano Aerogel Co., Ltd

- Porex

- Sino Aerogel

- Svenska Aerogel AB

- TAASI Corporation

- Thermablok Aerogels Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Adoption of Aerogel Due to Reusability and Recyclability

- 4.2.2 Rapidly Growing Construction Demand for High-performance Insulation

- 4.2.3 Energy-Efficiency Regulations Boosting EU and North-American Demand

- 4.2.4 Expansion of LNG Infrastructure Across Asia

- 4.2.5 Oil and Gas Industry Dominating the Aerogel Demand

- 4.3 Market Restraints

- 4.3.1 High Production Cost

- 4.3.2 Limited Availability of Raw Materials

- 4.3.3 Competition from High-performance Polymer Foams in Buildings

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products and Services

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Silica

- 5.1.2 Carbon

- 5.1.3 Alumina

- 5.1.4 Other Types

- 5.2 By Form

- 5.2.1 Blanket

- 5.2.2 Particle

- 5.2.3 Block

- 5.2.4 Panel

- 5.3 By Application

- 5.3.1 Thermal Insulation

- 5.3.2 Acoustic Insulation

- 5.3.3 Catalyst and Adsorbent

- 5.3.4 Battery and Energy Storage

- 5.3.5 Day-lighting and Translucent Panels

- 5.3.6 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Oil and Gas

- 5.4.2 Construction

- 5.4.3 Automotive

- 5.4.4 Marine

- 5.4.5 Aerospace

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Acoustiblok, Inc.

- 6.4.2 Active Aerogels

- 6.4.3 Aerogel Technologies, LLC

- 6.4.4 aerogel-it

- 6.4.5 Armacell

- 6.4.6 Aspen Aerogels, Inc.

- 6.4.7 BASF

- 6.4.8 Blueshift Materials Inc.

- 6.4.9 Cabot Corporation

- 6.4.10 ENERSENS

- 6.4.11 Guangdong Alison Technology Co., Ltd.

- 6.4.12 Knauf Insulation

- 6.4.13 Nano Tech Co., Ltd.

- 6.4.14 Ningbo Surnano Aerogel Co., Ltd

- 6.4.15 Porex

- 6.4.16 Sino Aerogel

- 6.4.17 Svenska Aerogel AB

- 6.4.18 TAASI Corporation

- 6.4.19 Thermablok Aerogels Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment