|

시장보고서

상품코드

1850193

난연성 화학제품제품 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Flame Retardant Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

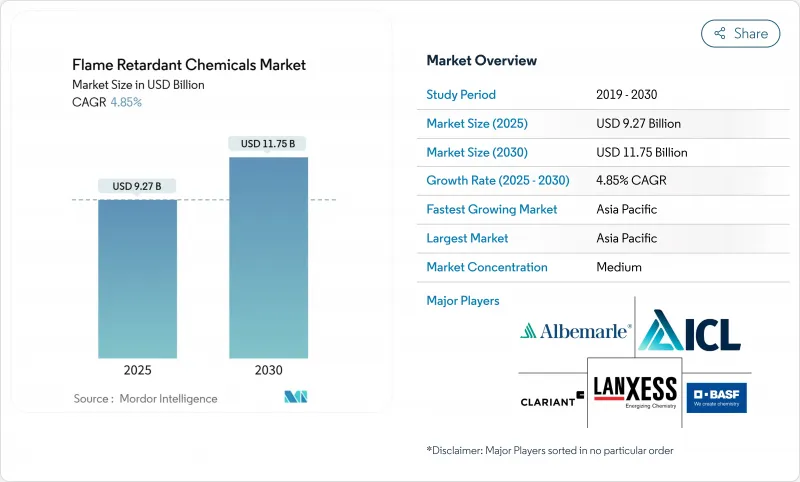

난연성 화학제품 시장의 2025년 시장 규모는 92억 7,000만 달러, 2030년에는 117억 5,000만 달러에 이르고, CAGR 4.85%를 보일 것으로 예측됩니다.

비할로겐계 솔루션을 지지하는 규제 기세, 에너지 효율적인 건물의 건설 증가, 전기 안전 기준의 엄격화가 이 궤도를 지원하고 있습니다. 브롬계 화합물이 규제 당국에 받아들여지지 않더라도 아시아태평양에서 확대되는 전자기기 제조 및 자동차의 전동화가 기준선 수요를 지지하고 있습니다. 인을 주성분으로 하는 무기 포트폴리오를 조기에 확대한 생산자는 현재 프리미엄 가격과 우선 공급업체로서의 지위로부터 이익을 얻고 있습니다. 한편, 안티몬과 인과 같은 중요한 광물의 가격 변동은 마진 위험을 초래하고 난연성 화학제품 시장에서 현지 조달 전략의 가치를 높이고 있습니다.

세계 난연성 화학제품제품 시장 동향과 통찰

엄격한 화재 안전 규제가 시장 확대를 촉진

2024년 국제건축기준법(International Building Code)의 갱신으로 외벽 어셈블리와 발포 플라스틱 단열재에 대한 규제가 강화되어 난연성 부하가 높은 건축재료의 재제조를 강요했습니다. 영국에서는 2026년 9월부터 개정 Approved Document B가 시행될 예정이며, 이 컴플라이언스 향상 동향은 더욱 강화됩니다. 비 할로겐 제품 라인을 판매하는 제조업체는 현재 건축가와 건설 업체가 발연 독성 및 재활용 테스트를 완료하는 제형을 지정하기 때문에 강력한 인출에 직면하고 있습니다. 유럽에서는 고층 외관의 개수가 잇따라 교환 수요가 확대되는 반면 보험업자는 보험료를 인정된 난연성능과 연결해 난연성 화학제품제품 시장의 안정성장을 지지하고 있습니다.

아시아태평양 인프라 붐이 수요 가속화

중국에서는 철도 회랑, 데이터센터, 배터리 공장 등의 유틸리티 파이프라인이 난연성 폴리올레핀과 폴리우레탄 단열재의 구매를 지원합니다. 클라리언트는 광동성의 2개의 무할로겐 공장에 1억 스위스 프랑을 투자하여 장기 수요에 대한 자신감을 보여줍니다. 중국, 한국, 인도에서 조립되는 전기자동차는 배터리 케이싱과 와이어 하네스용 1대당 약 1kg의 난연제가 필요합니다. 인도의 100개 시정촌에 걸쳐 있는 스마트 시티 프로그램은 새로운 국가 건축 기준법의 방화 테스트를 충족해야 하는 공공 주택 프로젝트를 추가합니다. 이러한 요인들과 함께 아시아태평양의 난연성 화학제품 시장의 CAGR은 세계 평균을 능가합니다.

규제상의 제약이 기존의 화학물질을 억제

유럽화학제품청은 2025년 2월 평가에서 방향족 브롬계 난연제를 난분해성, 생물 축적성, 유독하다고 했습니다. 스톡홀름 협약에 근거한 병행 협의는 Dechloran Plus를 잔류 유기 오염물질로 나열하는 것을 목표로 하고 있으며 전기 제품에 대한 사용이 금지될 가능성이 높습니다. 레거시 브롬 혼합물의 생산자는 포트폴리오의 재검토를 강요하고 잠정적인 수익 격차가 발생하여 난연성 화학제품제품 시장의 성장을 억제합니다.

부문 분석

비할로겐계 화학물질은 2024년에 64.94% 시장 점유율을 차지했으며, CAGR 5.02%로 추이하고 있습니다. 건축 기준법에 준거한 새로운 복합 패널의 대부분은 인산계 침투제와 수산화금속이 차지하고 있습니다. 클라리언트는 중국에서 Exolit 생산 능력을 두 배로 늘리고 아시아 컨버터의 리드 타임을 단축하고 지역의 난연성 화학제품 시장을 더욱 정착시켰습니다.

할로겐계 블렌드는 저첨가성이라는 점에서는 여전히 평가되고 있는 것, 사양의 축소에 직면하고 있습니다. 알베마르는 특정 브롬화 등급은 라이프 사이클의 온실 가스 강도가 낮고 최소한의 탈취 처리로 재활용할 수 있다고 주장합니다. 선도적인 제조업체는 용출과 직장 노출을 줄이는 캡슐화 브롬의 설계를 실험적으로 채택하고 그 지위를 유지합니다. 이러한 혁신의 성공 여부는 할로겐화 슬라이스가 더 광범위한 난연성 화학제품 시장에서 방어 가능한 틈새 시장을 유지할지 여부를 결정합니다.

지역 분석

아시아태평양은 2024년 난연성 화학제품 시장의 50.55%를 차지하고, 2030년까지의 CAGR은 5.56%를 나타낼 전망입니다. 중국은 여전히 세계 전자 장비 조립의 중심지이며, 난연성 케이블과 절연체를 필요로 하는 데이터센터 및 송전망 인프라에 많은 투자를 하고 있습니다. 배터리 전기자동차 제조에 대한 정부의 자극책은 모듈, 팩 및 인버터에서 고성능 폴리머 수요를 뒷받침하고 있습니다. 클라리언트, ICL 및 각 지역의 컴파운드 제조업체에 의한 현지 생산 능력 향상은 공급망의 단축과 운송 비용의 억제로 이어져 지역 경쟁력을 강화합니다.

북미는 성숙하지만 안정적인 시장입니다. 2024년 국제건축기준법의 개정은 단열재와 외관시스템에 높은 난연성을 요구하고 완만한 성장을 유지합니다. 소방 장비 및 가전제품에서 주 수준의 PFAS 금지령은 인과 질소 용액에 대한 대안을 가속화합니다. 그러나 중국의 안티몬 수출 규제가 첨가제 비용을 끌어 올려 수입 삼산화 안티몬에 의존하는 미국 마스터 배치 제조업체의 이폭을 압박하고 있습니다. 캐나다의 건축용 엔벨로프 리노베이션과 멕시코 자동차 조립의 성장은 계속해서 수량을 흡수하고 있습니다.

유럽은 세계에서 가장 엄격한 화재안전법과 화학물질 지속가능법에 힘입어 안정적인 수요를 보여주고 있습니다. 영국 외벽 시스템에 대한 새로운 규칙은 할로겐이없는 알루미늄 수산화물을 기반으로하는 분기성 페인트의 사용을 촉진합니다. 독일 자동차 부문에서는 순환형 경제의 목표에 따라 재활용 가능한 난연성 PP 및 폴리아미드 등급 지정이 증가하고 있습니다. 노르트리트(NORDTREAT)와 같은 북유럽 이노베이터는 바이오 대체품을 개발하고 난연성 화학제품 시장의 유럽 슬라이스에 차별화된 틈새 시장을 추가하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 건축 및 건설에 있어서의 엄격한 화재 안전 규제

- 아시아태평양의 급속한 인프라 정비

- 가전제품 및 전기제품의 생산량 증가

- 열가소성 플라스틱과 복합재료의 사용 증가

- ESG 규정 준수를 위한 비할로겐 솔루션으로의 전환

- 시장 성장 억제요인

- 브롬화/할로겐화 화학물질에 대한 규제의 억제

- 원재료비의 변동

- 나노금속 수산화물의 새로운 독성 조사

- 인광석 공급의 병목 현상

- 밸류체인 분석

- 원재료 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 제품 유형별

- 비할로겐계 난연제

- 무기

- 수산화알루미늄

- 수산화마그네슘

- 붕소 화합물

- 인

- 질소

- 기타 제품 유형

- 할로겐계 난연제

- 브롬 화합물

- 염소 화합물

- 비할로겐계 난연제

- 용도별

- 폴리올레핀

- PVC

- 에폭시 수지

- 엔지니어링 열가소성 플라스틱(PA, PBT, PEEK 등)

- 불포화 폴리에스테르 수지

- 폴리우레탄

- 최종 사용자 업계별

- 전기 및 전자공학

- 건축 및 건설

- 교통기관

- 섬유와 가구

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- Adeka Corporation

- Albemarle Corporation

- BASF

- Clariant AG

- DIC Corporation

- Dow Inc.

- Eti Maden

- ICL Group

- Italmatch Chemicals SpA

- JM Huber Corp.(Huber Engineered Materials)

- LANXESS AG

- Martin Marietta

- MPI Chemie BV

- Nabaltec AG

- Nyacol Nano Technologies Inc.

- RIN KAGAKU KOGYO Co. Ltd

- RTP Company

- Sanwa Chemical Co. Ltd

- Showa Denko KK

- Sibelco NV(Specialty Alumina)

- Thor Group

- Tosoh Corporation

- UFP Industries Inc.

제7장 시장 기회와 장래의 전망

SHW 25.11.07The flame retardant chemicals market is valued at USD 9.27 billion in 2025 and is forecast to reach USD 11.75 billion by 2030, advancing at a 4.85% CAGR.

Regulatory momentum favoring non-halogenated solutions, rising construction of energy-efficient buildings, and stricter electrical-safety codes anchor this trajectory. Expanding electronics manufacturing in Asia Pacific, coupled with the electrification of vehicles, sustains baseline demand even as brominated compounds lose regulatory acceptance. Producers that scaled phosphorus-based and inorganic portfolios early now benefit from premium pricing and preferred-supplier status. Meanwhile, price volatility for critical minerals like antimony and phosphorus introduces margin risk, heightening the value of localized sourcing strategies within the flame retardant chemicals market.

Global Flame Retardant Chemicals Market Trends and Insights

Stringent Fire-Safety Regulations Drive Market Expansion

The 2024 International Building Code update introduced tighter rules for exterior wall assemblies and foam-plastic insulations, compelling reformulation of construction materials with higher flame-retardant loading. The United Kingdom will enforce amended Approved Document B from September 2026, reinforcing this upward compliance trend. Manufacturers selling non-halogenated product lines now face strong pull-through as architects and builders specify formulations that clear smoke-toxicity and recyclability tests. Continuous retrofitting of high-rise facades in Europe extends replacement demand, while insurance providers tie premiums to certified flame performance, supporting stable growth in the flame retardant chemicals market.

Asia Pacific Infrastructure Boom Accelerates Demand

China's public-works pipeline, which includes rail corridors, data centers, and battery-cell factories, underpins flame-retardant polyolefins and polyurethane insulation purchases. Clariant committed CHF 100 million to two halogen-free plants in Guangdong, signaling confidence in long-cycle demand. Each electric vehicle assembled in China, South Korea, or India requires roughly 1 kg of flame retardants for battery casings and wiring harnesses. Smart-city programs across 100 Indian municipalities add public-housing projects that must meet new National Building Code fire tests. These factors collectively lift compound annual growth above the global average for the Asia Pacific flame retardant chemicals market.

Regulatory Restrictions Constrain Traditional Chemistries

The European Chemicals Agency flagged aromatic brominated flame retardants as persistent, bio-accumulative, and toxic in its February 2025 evaluation. Parallel consultations under the Stockholm Convention aim to list Dechlorane Plus as a persistent organic pollutant, signaling probable bans in electrical goods. Producers of legacy bromine blends must overhaul portfolios, creating interim revenue gaps that temper growth inside the flame retardant chemicals market.

Other drivers and restraints analyzed in the detailed report include:

- Electronics Electrification Creates Application Opportunities

- ESG Compliance Accelerates Non-Halogenated Adoption

- Supply Chain Volatility Pressures Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Non-halogenated chemistries held 64.94% market share in 2024 and are advancing at 5.02% CAGR, maintaining decisive leadership as environmental agencies tighten smoke-toxicity ceilings. Intumescent phosphates and metal hydroxides account for the bulk of new building-code compliant composite panels. Clariant doubled Exolit capacity in China, reducing lead times for Asian converters and further entrenching the flame retardant chemicals market in the region.

Halogenated blends, although still valued for low-additive loading, face shrinking specifications. Albemarle argues that certain brominated grades offer lower life-cycle greenhouse-gas intensity and can be recycled with minimal de-bromination treatment. Leading producers experimented with encapsulated bromine designs that cut leaching and workplace exposure to remain relevant. The success of those innovations will decide whether the halogenated slice retains a defensible niche in the broader flame retardant chemicals market.

The Flame Retardant Chemicals Market Report Segments the Industry by Product Type (Non-Halogenated Flame Retardants, and Halogenated Flame Retardants), Application (Polyolefins, PVC, and More), End-User Industry (Electrical and Electronics, Building and Construction, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific dominated with 50.55% of the flame retardant chemicals market in 2024 and is tracking a 5.56% CAGR to 2030. China remains the epicenter of global electronics assembly and is investing heavily in data-center and grid infrastructure that require flame-retardant cabling and insulation. Government stimulus for battery-electric vehicle manufacturing underpins demand for high-performing polymers in modules, packs, and inverters. Local capacity expansions from Clariant, ICL, and regional compounders shorten supply chains and curb freight costs, fortifying regional competitiveness.

North America is a mature but stable market. The 2024 International Building Code upgrade demands higher flame-retardant loading in insulation and facade systems, sustaining moderate growth. State-level PFAS prohibitions in firefighter gear and consumer electronics accelerate substitution toward phosphorus and nitrogen solutions. However, Chinese antimony export controls inflated additive costs, compressing margins for U.S. masterbatch suppliers that rely on imported antimony trioxide. Canadian building-envelope retrofits and Mexico's vehicle-assembly growth continue to absorb volumes.

Europe exhibits consistent demand underpinned by some of the world's strictest fire-safety and chemical-sustainability laws. The United Kingdom's new rules for external-wall systems drive usage of aluminum-hydroxide-based intumescent coatings that are halogen-free. Germany's automotive sector increasingly specifies recyclable flame-retardant PP and polyamide grades, aligning with circular-economy objectives. Nordic innovators such as NORDTREAT advance bio-based alternatives, adding differentiated niches to the European slice of the flame retardant chemicals market.

- Adeka Corporation

- Albemarle Corporation

- BASF

- Clariant AG

- DIC Corporation

- Dow Inc.

- Eti Maden

- ICL Group

- Italmatch Chemicals SpA

- J.M. Huber Corp. (Huber Engineered Materials)

- LANXESS AG

- Martin Marietta

- MPI Chemie BV

- Nabaltec AG

- Nyacol Nano Technologies Inc.

- RIN KAGAKU KOGYO Co. Ltd

- RTP Company

- Sanwa Chemical Co. Ltd

- Showa Denko K.K.

- Sibelco NV (Specialty Alumina)

- Thor Group

- Tosoh Corporation

- UFP Industries Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent fire-safety regulations in building & construction

- 4.2.2 Rapid infrastructure build-out across Asia Pacific

- 4.2.3 Rising output of consumer electronics & electrical goods

- 4.2.4 Increased Use of Thermoplastics and Composites

- 4.2.5 Shift toward non-halogenated solutions for ESG compliance

- 4.3 Market Restraints

- 4.3.1 Regulatory curbs on brominated / halogenated chemistries

- 4.3.2 Raw-material cost volatility

- 4.3.3 Emerging toxicity scrutiny on nano-metal hydroxides

- 4.3.4 Phosphorus ore supply bottlenecks

- 4.4 Value Chain Analysis

- 4.5 Raw Material Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Non-Halogenated Flame Retardants

- 5.1.1.1 Inorganic

- 5.1.1.1.1 Aluminum Hydroxide

- 5.1.1.1.2 Magnesium Hydroxide

- 5.1.1.1.3 Boron Compounds

- 5.1.1.2 Phosphorus

- 5.1.1.3 Nitrogen

- 5.1.1.4 Other Product Types

- 5.1.2 Halogenated Flame Retardants

- 5.1.2.1 Brominated Compounds

- 5.1.2.2 Chlorinated Compounds

- 5.1.1 Non-Halogenated Flame Retardants

- 5.2 By Application

- 5.2.1 Polyolefins

- 5.2.2 PVC

- 5.2.3 Epoxy Resins

- 5.2.4 Engineering Thermoplastics (PA, PBT, PEEK, etc.)

- 5.2.5 Unsaturated Polyester Resins

- 5.2.6 Polyurethane

- 5.3 By End-User Industry

- 5.3.1 Electrical and Electronics

- 5.3.2 Building and Construction

- 5.3.3 Transportation

- 5.3.4 Textiles and Furniture

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 North America

- 5.4.3.1 United States

- 5.4.3.2 Canada

- 5.4.3.3 Mexico

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%) / Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Adeka Corporation

- 6.4.2 Albemarle Corporation

- 6.4.3 BASF

- 6.4.4 Clariant AG

- 6.4.5 DIC Corporation

- 6.4.6 Dow Inc.

- 6.4.7 Eti Maden

- 6.4.8 ICL Group

- 6.4.9 Italmatch Chemicals SpA

- 6.4.10 J.M. Huber Corp. (Huber Engineered Materials)

- 6.4.11 LANXESS AG

- 6.4.12 Martin Marietta

- 6.4.13 MPI Chemie BV

- 6.4.14 Nabaltec AG

- 6.4.15 Nyacol Nano Technologies Inc.

- 6.4.16 RIN KAGAKU KOGYO Co. Ltd

- 6.4.17 RTP Company

- 6.4.18 Sanwa Chemical Co. Ltd

- 6.4.19 Showa Denko K.K.

- 6.4.20 Sibelco NV (Specialty Alumina)

- 6.4.21 Thor Group

- 6.4.22 Tosoh Corporation

- 6.4.23 UFP Industries Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Active R&D into Non-halogenated Flame Retardants