|

시장보고서

상품코드

1850217

모바일 백홀 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Mobile Backhaul - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

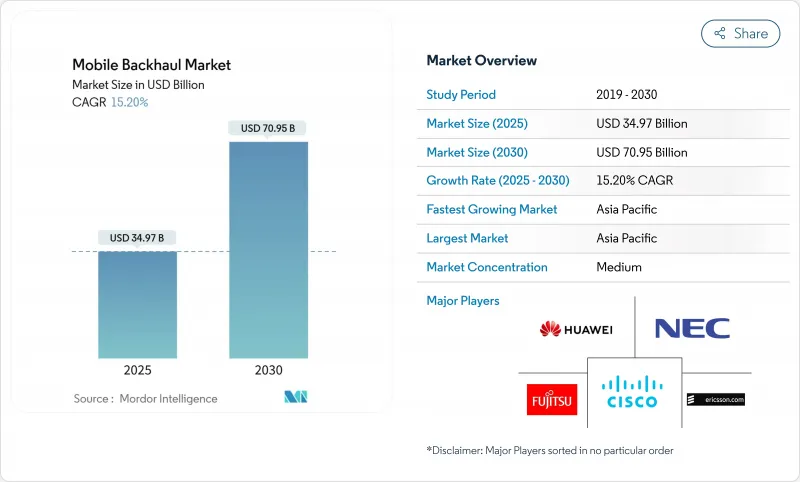

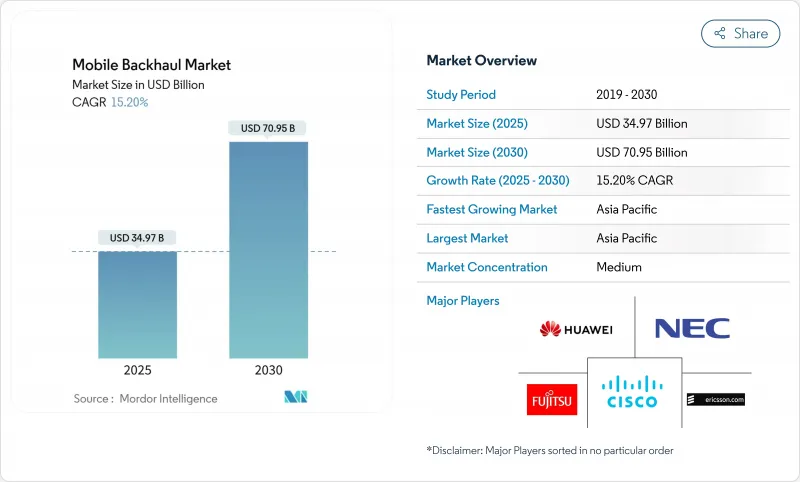

모바일 백홀 시장 규모는 2025년에 349억 7,000만 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR은 15.20%를 나타낼 것으로 예측되며 2030년에는 709억 5,000만 달러에 달할 전망입니다.

성장은 스마트폰 보급률 증가, 동영상 스트리밍 급증, 그리고 셀당 사이트당 10Gbps, 곧 100Gbps 용량을 요구하는 고밀도 5G 구축에 힘입어 추진되고 있습니다. 통신사들은 구리선을 광섬유 및 대용량 무선 링크로 교체하고 있으며, 중립 호스트 모델은 중복을 줄여 2020년부터 2025년까지 5G 투자액이 1조 1천억 달러를 넘어설 전망입니다. 개방형 아키텍처, 소프트웨어 정의 전송, 엣지 컴퓨팅은 백홀에 새로운 성능 및 보안 부담을 주지만, 상용 하드웨어를 통해 수명 주기 비용을 절감할 수 있습니다. 아시아태평양 지역은 매출 기여도 35%로 선두를 달리며, 중국, 일본, 한국, 인도가 수백만 개의 소형 셀을 설치함에 따라 지역별 최고 연평균 성장률(CAGR) 17.3%를 기록하고 있습니다. 전 세계 통신사들은 이제 광섬유의 확장성과 마이크로파, 밀리미터파, 저궤도(LEO) 위성 중계를 결합해 커버리지 공백을 메우고 구축 속도를 높이고 있습니다.

세계의 모바일 백홀 시장 동향 및 인사이트

모바일 데이터 트래픽 증가와 스마트폰 보급

스마트폰 1대당 월평균 데이터 사용량은 2023년 21GB에서 2029년 56GB로 급증할 전망이며, 모바일 트래픽의 75%를 영상이 차지할 것으로 예상됩니다. 지역별 격차도 나타나고 있습니다. 북미 사용자는 월 66GB에 달할 수 있는 반면, 사하라 이남 아프리카는 23GB 수준에 머물러 사업자들이 국가별 맞춤형 백홀 조합을 설계해야 합니다. 광섬유 트렁크와 고대역 마이크로파 중계망을 결합한 하이브리드 토폴로지가 도시 밀집 지역에서 주류로 부상 중입니다. 이는 장기간의 도로 굴착 허가 없이도 용량 수요를 충족시키기 때문입니다. 소형 셀의 확산으로 수천 개의 단거리 링크가 추가되면서, 사이트별 용량을 실시간으로 조정할 수 있는 자동화 네트워크 관리 플랫폼에 대한 신규 투자가 촉진되고 있습니다.

급속한 5G 전개가 용량 요구를 촉진

5G 클러스터에서 기지국 밀도가 km²당 4-5개에서 40-50개로 증가하며 백홀 종단점이 급증하고 있습니다. 중국만 해도 60만 개 이상의 5G 매크로 및 소형 셀을 구축 중이며, 이는 4G를 1.3-1.5배 초과할 것으로 예상됩니다. 현재 각 5G 셀은 10Gbps 업링크와 5ms 미만의 엄격한 지연 시간을 요구하여, 70/80GHz E-밴드 무선 장비와 광섬유 기반 시간 민감형 네트워킹(TSN)의 도입을 가속화하고 있습니다. 자본 부담으로 인해 많은 통신사들이 공유 타워와 임대형 다크 파이버를 선택하며, 초기 비용을 낮추면서도 100Gbps 인터페이스로의 업그레이드 경로를 확보하고 있습니다.

섬유 및 스펙트럼 비용을 위한 고액의 설비 투자

밀집 도시에서의 광케이블 매설 비용은 킬로미터당 10만 달러를 초과할 수 있으며, 도로 개통 허가가 제한적인 지역에서는 이 비용이 급증합니다. 전기 요금 상승으로 4G와 5G 대역이 중첩되는 매크로 사이트의 전력 소비량이 두 배로 증가하여 운영 비용이 부풀어 오릅니다. 개발도상국에서는 저금리 자금 조달 접근성 부족으로 광케이블 구축이 지연되어, 장기적 경제성이 광케이블에 유리함에도 통신사들이 마이크로파에 의존할 수밖에 없습니다. 그 결과 도시와 농촌 간 경험 품질(QoE) 격차가 발생하여 디지털 포용 목표 달성을 저해하고 있습니다.

부문 분석

광섬유 기반 링크는 탁월한 용량과 낮은 지연 시간 덕분에 2024년 모바일 백홀 시장의 55%를 차지했습니다. 이 점유율은 2024년 192억 달러 규모의 모바일 백홀 시장에서 가장 큰 비중을 차지하는 전개 형태입니다. 그러나 무선 대안은 2030년까지 연평균 16.4% 성장률을 기록하며 격차를 좁힐 전망입니다. 도시 밀집화와 팝업 이벤트가 신속한 가동 개시를 요구하기 때문입니다. 사업자들은 70/80GHz E-밴드 라디오를 임대 암섬유 트렁크와 결합해 홉당 10Gbps를 제공하면서도 고비용 토목 공사를 피합니다.

하이브리드 아키텍처가 표준화되고 있습니다. 광섬유는 코어 집선용 선호 매체로 남지만, 마이크로파 및 밀리미터파는 허가 문제나 지형적 제약으로 매설이 어려운 엣지 소형 셀 및 기업 시설에 활용됩니다. 신흥 W-밴드 및 D-밴드 링크는 1-2km 거리에서 멀티기가비트 처리량을 제공하며, 고밀도 클러스터에서 광섬유를 보완합니다. 인구 밀도가 낮은 지역에서는 사업자들이 저궤도(LEO) 위성 백홀을 마이크로파 링에 접합해 예산 한도를 초과하지 않으면서 연속적인 커버리지를 구축합니다. 이러한 유연성은 모바일 백홀 시장의 장기적 경쟁력을 뒷받침합니다.

2024년 마이크로파 라디오는 모바일 백홀 시장 규모에서 41%를 차지했으며, 이는 수십 년간 현장 검증된 신뢰성을 반영합니다. 공급업체들은 스펙트럼 효율을 16bps/Hz까지 끌어올리면서 비연속 채널을 집계하는 링크 본딩 방식을 추가했습니다. 소형 셀 백홀 장비는 현재 매출의 일부에 불과하지만, 경기장, 쇼핑몰, 교통 허브에서 실내 5G를 도입함에 따라 17.4%의 연평균 성장률(CAGR)을 기록할 전망입니다.

모바일 백홀 시장은 통합 액세스 및 백홀(IAB)로의 전환을 목격하고 있으며, 28GHz 라디오가 사용자 기기를 동시에 서비스하고 트래픽을 상류로 중계합니다. 이는 옥상 혼잡을 줄이고 구역 설정을 단순화합니다. 밀리미터파 칩셋 기술 발전으로 2023년 대비 전력 소모량이 30% 감소하여 최소한의 현장 작업만 필요한 폴 마운트 및 윈도우 마운트 노드 구축이 가능해졌습니다. 자체 구성 네트워크(SON) 소프트웨어를 번들로 제공하는 벤더들은 복잡한 환경에서 현장 방문 횟수를 줄이고 링크 정렬을 최적화함으로써 입찰에서 우위를 점하고 있습니다.

모바일 백홀 시장 보고서는 전개(유선 (섬유/광, 카퍼/DSL), 무선 (마이크로파, mm파, 기타)), 장비 유형(라우터 및 스위치, 마이크로파 라디오 등), 서비스 유형(전문 서비스, 관리 서비스 등), 네트워크 아키텍처(매크로셀 백홀, 기타), 최종 사용자(이동 통신 사업자, 중립 호스트 및 타워 기업 등), 지역별로 분류됩니다.

지역 분석

아시아태평양 지역은 5G에 대한 대규모 투자, 정부 보조금, 밀집된 도시 인구 덕분에 모바일 백홀 시장의 35%를 차지하며 연평균 17.3%의 성장률을 보이고 있습니다. 중국, 일본, 한국은 이미 주요 도시에 독립형 5G를 전면 구축하여 굴착 병목 현상을 우회하는 10Gbps 마이크로파 중계 수요를 급증시키고 있습니다. 인도의 최근 주파수 경매는 고속도로를 따라 2선급 도시까지 광케이블 설치 붐을 촉발했으며, 사업자들은 히말라야 및 섬 지역 커버리지를 위해 위성-마이크로파 하이브리드 기술도 시범 운영 중입니다. 농촌 광케이블 구축을 지원하는 정부 정책이 추가 성장 동력을 유지하고 있습니다.

북미는 규모는 작지만 가상화 RAN(무선접속망)과 다크파이버 집약 분야에서 혁신을 주도하고 있습니다. 버라이즌과 T-모바일은 2024년 지역 광케이블 업체를 인수해 광학 인프라를 확충했으며, 확장 가능한 백홀을 확보해 고정 무선 접속망 구축을 지원하고 있습니다. 연방통신위원회(FCC)의 90억 달러 규모 5G 기금은 지형적 제약으로 매설이 어려운 외딴 지역의 기지국 업그레이드를 장려하며, 마이크로파 및 위성 백홀에 투자를 유도합니다. 통신사들이 기가비트 광대역과 기지국 업링크에 광섬유를 재활용하면서 고정-이동통신 융합이 가속화되어 자본 수익률이 증대됩니다.

유럽의 성숙 시장은 엄격한 규제 심사와 범유럽 5G 회랑 구축 추진 사이에서 균형을 맞춥니다. 인프라 공유 체계는 중복 자본 지출을 줄이고, 공공-민간 파트너십은 연결 화물 운송 등 저지연 서비스에 필수적인 국경 간 광섬유 노선에 자금을 지원합니다. 한편 중동은 고밀도 소형 셀 그리드에 의존하는 스마트시티 비전을 신속 추진 중이며, 아프리카 통신사들은 원격 커버리지 섬 지역 백홀을 위해 저궤도(LEO) 위성군을 활용합니다. 라틴 아메리카에서는 17개국에서 5G 서비스를 출시했으며, 통신사들은 컨소시엄을 구성해 해저 케이블 용량을 임대하고 마이크로파 체인을 통해 내륙으로 분배함으로써 국가 네트워크에 복원력을 구축하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 모바일 데이터 트래픽과 스마트폰 보급 증가

- 급속한 5G 전개에 의해 용량 수요가 증가

- 클라우드 네이티브 및 오픈 RAN 아키텍처

- 농촌 지역 커버리지를 위한 저궤도 위성 백홀

- 유틸리티 기업 및 사설 LTE 네트워크의 광섬유 임대

- 시장 성장 억제요인

- 광섬유와 스펙트럼 비용에 대한 고액의 설비 투자

- 마이크로파 스펙트럼의 라이선싱 복잡성

- 초저지연 동기의 과제

- SDN 백홀 사이버 보안 위험

- 밸류체인/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 투자분석

- 시장에 대한 COVID-19의 영향

제5장 시장 규모와 성장 예측

- 전개별

- 유선

- 광섬유

- 구리선/DSL

- 무선

- 마이크로파

- mm파(E-BAND 및 V-BAND)

- 위성

- 자유 공간광

- 유선

- 기기별

- 라우터와 스위치

- 마이크로파 라디오

- 광전송장치

- 소형 셀 백홀 장비

- 기타

- 서비스 유형별

- 전문 서비스

- 관리형 서비스

- 설치 및 통합

- 유지보수 및 지원

- 네트워크 아키텍처별

- 매크로셀 백홀

- 소형 셀 백홀

- 클라우드 RAN/프런트 홀

- 최종 사용자별

- 이동 통신 사업자

- 중립 호스트 및 타워 기업

- 인터넷 서비스 제공업체

- 민간기업과 유틸리티

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 중동

- GCC

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일(세계 레벨 개요 포함)

- Market level overview

- Huawei Technologies Co.

- Ericsson AB

- Nokia Corporation

- ZTE Corporation

- NEC Corporation

- Cisco Systems

- Fujitsu Limited

- Aviat Networks

- Ceragon Networks Ltd.

- BridgeWave Communications

- ATandT Inc.

- Verizon Communications Inc.

- Ciena Corporation

- Juniper Networks

- Siklu Communication Ltd.

- Infinera Corporation

- CommScope Holding Company

- Telefonica SA

- Intelsat SA

- Parallel Wireless

제7장 시장 기회와 장래의 전망

HBR 25.11.17The Mobile Backhaul Market size is estimated at USD 34.97 billion in 2025, and is expected to reach USD 70.95 billion by 2030, at a CAGR of 15.20% during the forecast period (2025-2030).

Growth is propelled by escalating smartphone penetration, the sharp rise in video streaming, and dense 5G rollouts that demand 10 Gbps and soon 100 Gbps per cell per site capacity. Operators are swapping copper lines for fiber and high-capacity wireless links, while neutral-host models reduce duplication as 5G investments top USD 1.1 trillion between 2020 and 2025. Open architectures, software-defined transport, and edge compute place new performance and security pressures on backhaul, yet they can lower life-cycle costs through commercial off-the-shelf hardware. Asia Pacific leads with a 35% revenue contribution and shows the fastest regional CAGR at 17.3% as China, Japan, South Korea, and India install millions of small cells. Operators everywhere now blend fiber's scale with microwave, millimeter-wave, and low-Earth-orbit (LEO) satellite hops to fill coverage gaps and accelerate rollouts.

Global Mobile Backhaul Market Trends and Insights

Growing Mobile Data Traffic & Smartphone Adoption

Average monthly data per smartphone is forecast to soar from 21 GB in 2023 to 56 GB by 2029, with video expected to account for 75% of mobile traffic. Regional divergence is emerging: North American users may hit 66 GB per month while Sub-Saharan Africa lingers near 23 GB, forcing operators to engineer country-specific backhaul mixes. Hybrid topologies that splice fiber trunks with high-band microwave hops now dominate urban densification because they meet capacity needs without prolonged street-dig permitting. Small-cell proliferation adds thousands of short-haul links, prompting fresh investment in automated network-management platforms that can tune capacity per site in real time.

Rapid 5G Rollout Driving Capacity Needs

Base-station density is climbing from 4-5 to 40-50 sites per km2 in 5G clusters, multiplying backhaul terminations. China alone is building more than 600,000 5G macro and small cells, a count projected to outstrip 4G by 1.3-1.5 times . Each 5G cell now requires 10 Gbps uplinks and stringent latency of sub-5 ms, accelerating the adoption of 70/80 GHz E-band radios and time-sensitive networking over fiber. Capital stress is nudging many operators toward shared towers and leased dark fiber, lowering up-front costs while ensuring upgrade paths to 100 Gbps interfaces.

High Capex for Fiber & Spectrum Costs

Fiber trenching in dense cities can run beyond USD 100,000 per Kilometer, a figure that climbs sharply where road-opening permits are scarce. Rising electricity prices also double macro-site power draw when 4G and 5G bands overlap, inflating operational overhead. In developing economies, limited access to low-interest financing delays fiber build-outs, forcing carriers to rely on microwave even where long-term economics favor fiber. The result is uneven quality-of-experience across urban and rural divides, hindering digital-inclusion goals.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-Native & Open RAN Architectures

- Satellite LEO Backhaul for Rural Reach

- SDN Backhaul Cybersecurity Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fiber-based links constituted 55% of the mobile backhaul market in 2024 due to their unrivalled capacity and low latency. This share translates to the largest deployment slice of the mobile backhaul market size at USD 19.2 billion in 2024. Wireless alternatives, however, are set to post a 16.4% CAGR through 2030, narrowing the gap as urban densification and pop-up events demand rapid turn-ups. Operators mesh 70/80 GHz E-band radios with leased dark fiber trunks, delivering 10 Gbps per hop while avoiding costly civil works.

Hybrid architectures are now standard: fiber remains the preferred medium for core aggregation, but microwave and millimeter-wave serve edge small cells and enterprise venues where permits or geography stall trenching. Emergent W-band and D-band links promise multi-gigabit throughput over 1-2 km, complementing fiber for dense clusters. In sparsely populated regions, operators splice LEO satellite backhaul into microwave rings, creating contiguous coverage without exceeding budget ceilings. This flexibility underpins the long-term competitiveness of the mobile backhaul market.

Microwave radios held 41% of the mobile backhaul market size in 2024, reflecting decades of field-proven reliability. Vendors have pushed spectral efficiency to 16 bps/Hz while adding link-bonding schemes that aggregate non-contiguous channels. Small cells backhaul gear, though only a fraction of revenue today, is set for a 17.4% CAGR as stadiums, malls, and transport hubs adopt indoor 5G.

The mobile backhaul market is witnessing a pivot toward integrated access and backhaul (IAB), where a 28 GHz radio simultaneously serves user devices and relays traffic upstream. This reduces rooftop congestion and simplifies zoning. Millimeter-wave chipset advances cut power draw by 30% since 2023, enabling pole-mount and window-mount nodes that require minimum site work. Vendors that bundle self-organizing-network software are winning tenders because they lower truck rolls and optimize link alignment in cluttered environments.

The Mobile Backhaul Market Report is Segmented by Deployment (Wired [Fiber/Optical and Copper/DSL], Wireless [Microwave, Millimetre-Wave, and More]), Equipment Type (Routers and Switches, Microwave Radios, and More), Service Type (Professional Services, Managed Services, and More), Network Architecture (Macro-Cell Backhaul, and More), End-User (Mobile Network Operators, Neutral-Host and Tower Companies, and More), and Geography.

Geography Analysis

Asia Pacific commands 35% of the mobile backhaul market, expanding at 17.3% CAGR thanks to outsized 5G investments, state subsidies, and dense urban populations. China, Japan, and South Korea already blanket major cities with standalone 5G, driving steep demand for 10 Gbps microwave hops that skirt excavation bottlenecks. India's recent spectrum auctions have unleashed a fiber-laying spree along highways and into tier-2 cities, while operators also pilot satellite-plus-microwave hybrids for Himalayan and island coverage. Government schemes that underwrite rural fiber further sustain momentum.

North America, while smaller by volume, leads innovation in virtualized RAN and dark-fiber aggregation. Verizon and T-Mobile bolstered their optical footprints by acquiring regional fiber players in 2024, locking in scalable backhaul to support fixed-wireless access rollouts. The Federal Communications Commission's USD 9 billion 5G Fund incentivizes cell-site upgrades in remote counties, channeling investments toward microwave and satellite backhaul where terrain hampers trenching. Fixed-mobile convergence accelerates as operators reuse fiber for both gigabit broadband and cell-site uplinks, amplifying return on capital.

Europe's mature markets balance stringent regulatory reviews with a push for pan-EU 5G corridors. Infrastructure-sharing frameworks lower duplicate capex, while public-private partnerships finance cross-border fiber routes vital for low-latency services such as connected freight. Meanwhile, the Middle East fast-tracks smart-city visions that rely on dense small-cell grids, and African carriers tap LEO constellations to backhaul remote coverage islands. Latin America sees 5G launches in 17 countries, with carriers forming consortia to lease submarine-cable capacity and distribute it inland via microwave chains, weaving resilience into national networks.

- Market level overview

- Huawei Technologies Co.

- Ericsson AB

- Nokia Corporation

- ZTE Corporation

- NEC Corporation

- Cisco Systems

- Fujitsu Limited

- Aviat Networks

- Ceragon Networks Ltd.

- BridgeWave Communications

- ATandT Inc.

- Verizon Communications Inc.

- Ciena Corporation

- Juniper Networks

- Siklu Communication Ltd.

- Infinera Corporation

- CommScope Holding Company

- Telefonica S.A.

- Intelsat S.A.

- Parallel Wireless

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing mobile data traffic and smartphone adoption

- 4.2.2 Rapid 5G rollout driving capacity needs

- 4.2.3 Cloud-native and Open RAN architectures

- 4.2.4 Satellite LEO backhaul for rural reach

- 4.2.5 Fiber leasing by utilities and private LTE networks

- 4.3 Market Restraints

- 4.3.1 High capex for fiber and spectrum costs

- 4.3.2 Microwave spectrum licensing complexity

- 4.3.3 Ultra-low-latency synchronisation challenges

- 4.3.4 SDN backhaul cybersecurity risks

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

- 4.9 Impact of COVID-19 on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 Wired

- 5.1.1.1 Fiber/Optical

- 5.1.1.2 Copper/DSL

- 5.1.2 Wireless

- 5.1.2.1 Microwave

- 5.1.2.2 Millimetre-Wave (E- and V-band)

- 5.1.2.3 Satellite

- 5.1.2.4 Free-Space Optics

- 5.1.1 Wired

- 5.2 By Equipment Type

- 5.2.1 Routers and Switches

- 5.2.2 Microwave Radios

- 5.2.3 Optical Transport Equipment

- 5.2.4 Small-Cell Backhaul Equipment

- 5.2.5 Others

- 5.3 By Service Type

- 5.3.1 Professional Services

- 5.3.2 Managed Services

- 5.3.3 Installation and Integration

- 5.3.4 Maintenance and Support

- 5.4 By Network Architecture

- 5.4.1 Macro-Cell Backhaul

- 5.4.2 Small-Cell Backhaul

- 5.4.3 Cloud RAN/Fronthaul

- 5.5 By End-user

- 5.5.1 Mobile Network Operators

- 5.5.2 Neutral-Host and Tower Companies

- 5.5.3 Internet Service Providers

- 5.5.4 Private Enterprises and Utilities

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 GCC

- 5.6.5.2 Turkey

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Egypt

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview

- 6.4.1 Market level overview

- 6.4.2 Huawei Technologies Co.

- 6.4.3 Ericsson AB

- 6.4.4 Nokia Corporation

- 6.4.5 ZTE Corporation

- 6.4.6 NEC Corporation

- 6.4.7 Cisco Systems

- 6.4.8 Fujitsu Limited

- 6.4.9 Aviat Networks

- 6.4.10 Ceragon Networks Ltd.

- 6.4.11 BridgeWave Communications

- 6.4.12 ATandT Inc.

- 6.4.13 Verizon Communications Inc.

- 6.4.14 Ciena Corporation

- 6.4.15 Juniper Networks

- 6.4.16 Siklu Communication Ltd.

- 6.4.17 Infinera Corporation

- 6.4.18 CommScope Holding Company

- 6.4.19 Telefonica S.A.

- 6.4.20 Intelsat S.A.

- 6.4.21 Parallel Wireless

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment